1. What are the major growth drivers for the Dump Trucks And Mining Trucks Market market?

Factors such as are projected to boost the Dump Trucks And Mining Trucks Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

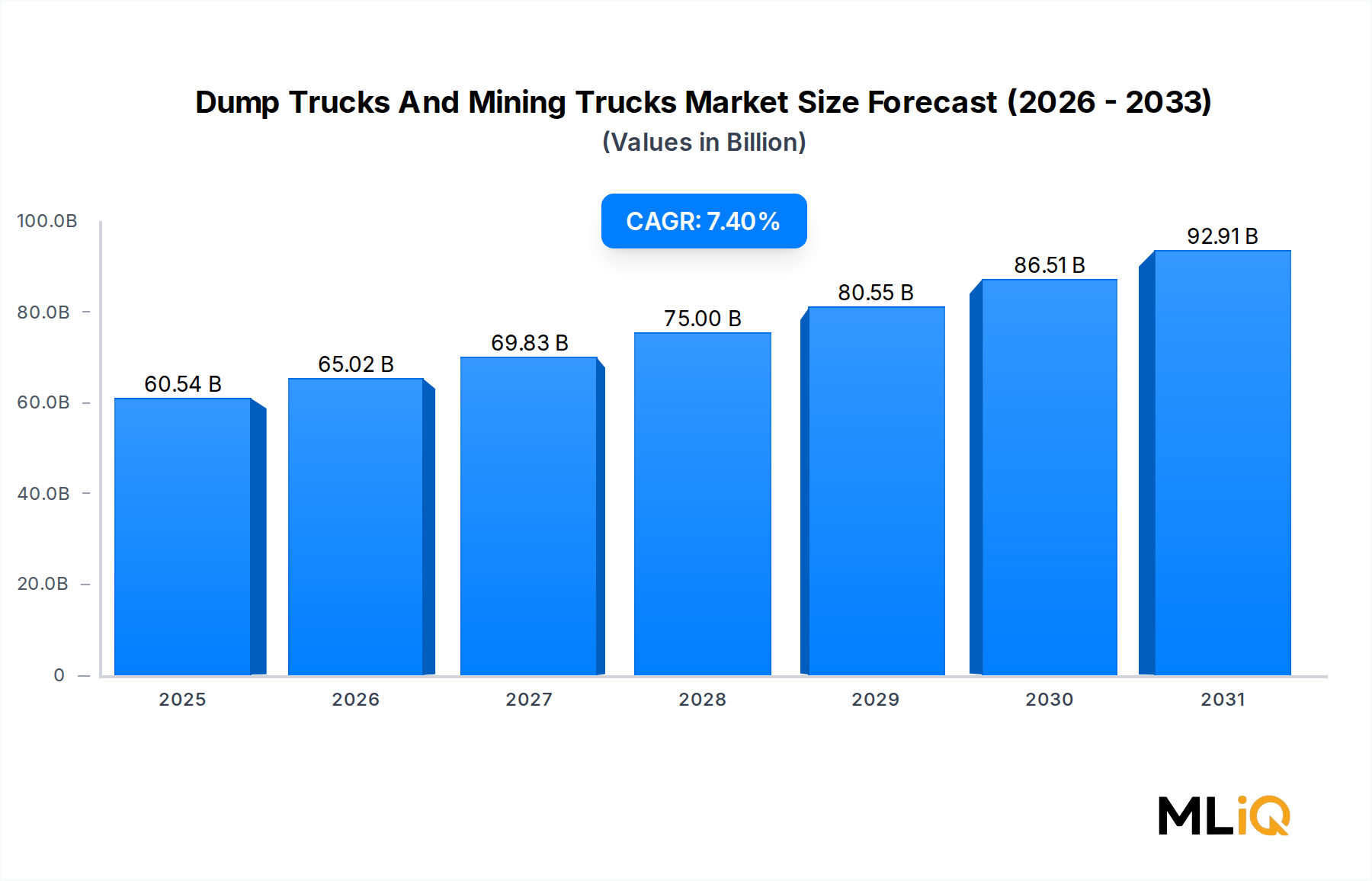

The global Dump Trucks And Mining Trucks Market is currently valued at $60.54 billion and is projected to expand at a compound annual growth rate (CAGR) of 7.4% over the forecast period, reflecting robust structural demand from both the construction and extractive industries. This valuation positions the market as one of the most capital-intensive segments within heavy equipment, underpinned by multi-decade infrastructure cycles, commodity price recovery, and accelerating electrification initiatives.

Primary demand catalysts include surging government-backed infrastructure spending across Asia Pacific, the Americas, and the Middle East, alongside a commodity supercycle driven by the global energy transition's appetite for copper, lithium, cobalt, and iron ore. Mining operators are accelerating fleet replacement programs to meet stricter emissions mandates and reduce total cost of ownership over vehicle lifecycles. Large open-pit mines across Australia, Chile, the Democratic Republic of Congo, and Indonesia have entered multi-year expansion phases, each requiring sustained procurement of ultra-class haul trucks in the greater-than-100-tonne payload class.

On the construction side, rapid urbanization in emerging economies is propelling earthmoving activity. India's National Infrastructure Pipeline, valued at over USD 1.4 trillion, and China's continued Belt and Road Initiative commitments are translating directly into sustained unit demand for articulated and rigid dump trucks in the sub-100-tonne class. In North America, the Bipartisan Infrastructure Law's USD 1.2 trillion allocation has reinvigorated road, bridge, and tunnel construction programs requiring high-cycle, medium-payload articulated machines.

Technological disruption is reshaping the competitive landscape. Battery-electric and trolley-assist haul trucks are moving from pilot deployments to commercial scale, with several OEMs announcing series production timelines between 2025 and 2028. Autonomous haulage technology, already operational at major iron ore and coal mines, is expanding into gold, copper, and phosphate operations, promising up to 15% improvement in haul cycle productivity. Connectivity and telematics platforms are enabling predictive maintenance, reducing unplanned downtime by 20–30% in mature deployments.

Macroeconomic tailwinds include favorable commodity price environments for gold (sustaining above USD 2,000 per troy ounce through 2024) and copper (exceeding USD 9,000 per metric tonne), which incentivize capital expenditure by mining companies. Simultaneously, the green-energy transition is increasing demand for raw material extraction, indirectly benefiting the mining truck segment.

The forward-looking outlook remains strongly positive. Market participants that invest in electrification roadmaps, autonomous integration, and digital fleet management solutions will command premium pricing power and stronger after-market revenue streams through 2030 and beyond. The convergence of sustainability mandates and productivity imperatives makes this market a strategic priority for both OEMs and end-users globally.

Within the broader Dump Trucks And Mining Trucks Market, rigid dump trucks constitute the single largest revenue-generating segment, commanding an estimated 55–60% share of total market value. Their dominance is fundamentally structural: rigid trucks are purpose-engineered for high-tonnage, high-frequency haulage in open-pit mining environments where road surface quality can be tightly controlled, and payload maximization directly determines cost-per-tonne haulage efficiency. Unlike articulated machines optimized for rough terrain maneuverability, rigid trucks achieve economies of scale at payload capacities ranging from 100 tonnes to over 360 tonnes, making them the workhorses of global copper, iron ore, coal, and oil sands operations.

The economics are compelling. In a large open-pit copper mine operating 24 hours per day with fleet sizes of 50–150 trucks, even a 1% improvement in payload utilization can translate to tens of millions of dollars in annual savings. OEMs have responded by relentlessly scaling up payload capacities — the Caterpillar 797F, for instance, carries 363 metric tonnes per cycle, while the Komatsu 980E-5 targets 290 metric tonnes with an AC electric drive system. These ultra-class machines sell at unit prices ranging from USD 3 million to over USD 6 million, making the segment highly capital-intensive and reliant on long-term customer relationships and aftermarket support networks.

Caterpillar and Komatsu collectively account for the majority of ultra-class rigid truck installations globally. Caterpillar maintains leadership through its Cat MineStar telematics ecosystem and a deep North American dealer network, while Komatsu competes aggressively on total-cost-of-ownership propositions backed by its Autonomous Haulage System (AHS), which is already deployed across more than 450 units at iron ore and coal mines in Australia. AB Volvo and Hitachi Construction Machinery Co., Ltd. also hold meaningful shares in the rigid segment, particularly in Asian and European mining operations.

The payload segmentation further reveals an important dynamic: the more-than-100-tonne class is growing faster than the less-than-100-tonne class in revenue terms, despite the latter being larger in unit volume. This is because ultra-class trucks carry disproportionately higher price tags and generate substantial lifecycle aftermarket revenue through parts, tires, rebuild kits, and digital service subscriptions. Mining companies operating in Tier 1 jurisdictions with high labor costs are especially motivated to invest in this segment, as automation and electrification retrofits are more economically viable on large platforms.

The rigid segment's share is consolidating rather than expanding proportionally. While absolute revenue continues to grow with the market, articulated trucks are gaining relative share at the margin due to growth in infrastructure construction, quarry operations, and smaller-scale mining in emerging markets. Nonetheless, rigid trucks' embedded position in the global mining supply chain — anchored by long-term OEM service agreements, proprietary fleet management systems, and billion-dollar mine-site infrastructure built around specific truck models — creates powerful switching costs that entrench incumbents and ensure the segment remains the dominant revenue pillar of the Dump Trucks And Mining Trucks Market through at least 2032.

Investment in electric rigid trucks is accelerating within this segment. Komatsu's 930E electric drive platform is being adapted for battery-electric operation, and Liebherr has unveiled its T 274 electric haul truck concept targeting 305 tonnes payload. These developments suggest that while the combustion-based rigid truck segment matures, electrification will extend the segment's growth trajectory well into the next decade.

Several quantifiable drivers and constraints define the trajectory of the Dump Trucks And Mining Trucks Market with high precision.

Driver 1 — Mining Capex Recovery: Global mining capital expenditures rebounded to approximately USD 131 billion in 2023, up from a trough of USD 82 billion in 2016, according to S&P Global data. This recovery directly drives fleet procurement. Copper mine expansions in Chile (e.g., Codelco's Chuquicamata underground conversion) and lithium operations in Australia are among the most active procurement fronts.

Driver 2 — Infrastructure Spending Cycles: The global infrastructure investment gap is estimated at USD 15 trillion through 2040 by the Global Infrastructure Hub. This gap, combined with legislative stimulus such as the U.S. Bipartisan Infrastructure Law and the EU's Global Gateway initiative (EUR 300 billion through 2027), sustains elevated demand for construction-grade dump trucks across road, dam, and port construction.

Driver 3 — Electrification Mandates: Regulatory frameworks in the European Union and Canada mandate that new mining equipment sold after 2030 must meet near-zero tailpipe emission standards. This is accelerating OEM R&D investment and driving replacement cycles for older diesel fleets, creating a replacement demand wave estimated to affect over 40,000 haul trucks globally.

Constraint 1 — Component Supply Shortages: Global semiconductor shortages between 2021 and 2023 caused delivery lead times for electronic control units to extend from 8 weeks to over 52 weeks in some cases, delaying truck deliveries and inflating OEM production costs by an estimated 12–18%.

Constraint 2 — High Upfront Capital Cost: The average price of an ultra-class rigid haul truck exceeds USD 4 million, limiting market access for smaller mining operators without access to project finance. This creates market concentration among Tier 1 miners and slows fleet modernization in developing economies.

Constraint 3 — Skilled Operator Shortage: A global shortage of qualified heavy equipment operators, estimated at over 2 million unfilled positions by the International Labour Organization, constrains utilization rates and increases pressure on mining companies to accelerate autonomous fleet adoption, which in turn reshapes OEM product road maps.

The Dump Trucks And Mining Trucks Market is characterized by a moderately concentrated competitive landscape, with a combination of Western multinational OEMs and Chinese state-backed manufacturers competing on technology, scale, and regional market access.

Caterpillar: The global market leader in large mining trucks, Caterpillar leverages its Cat MineStar fleet management platform and a comprehensive dealer service network spanning over 190 countries to maintain dominant share in North America, Australia, and Latin America.

Komatsu: A strong second globally, Komatsu differentiates through its Autonomous Haulage System, which is commercially deployed at scale, and is investing heavily in battery-electric truck development under its GHG Alliance program targeting 50% reduction in Scope 1 and 2 emissions by 2030.

AB Volvo: Volvo's trucks and construction equipment division holds significant share in the European and Scandinavian markets, with a strong articulated dump truck lineup and growing investments in electric drive systems for both surface and underground mining applications.

Liebherr: A privately held Swiss-German OEM with a reputation for high-reliability large mining trucks, Liebherr is notable for manufacturing its own diesel engines, electric drive systems, and hydraulic components in-house, providing strong vertical integration advantages.

Hitachi Construction Machinery Co., Ltd.: Specializing in AC electric drive rigid dump trucks, Hitachi maintains a strong position in Asia Pacific and is expanding its EH series lineup with digital mine optimization capabilities developed in partnership with major Japanese mining groups.

XCMG Group: China's largest construction and mining equipment manufacturer, XCMG Group is rapidly expanding its international footprint across Africa, Southeast Asia, and the Middle East, competing aggressively on price with a growing portfolio of rigid and articulated dump trucks.

SANY Group: Another leading Chinese OEM, SANY Group has invested substantially in R&D for electric and hybrid mining trucks and is leveraging its strong domestic market position to expand exports, particularly across Belt and Road Initiative project geographies.

Zoomlion Heavy Industry Science and Technology Co., Ltd.: Competing in the mid-range dump truck segment, Zoomlion Heavy Industry Science and Technology Co., Ltd. focuses on cost-competitive products for construction and quarrying markets in Asia and Africa.

Scania: Operating primarily in the on-road dump truck space, Scania is making inroads into mining site logistics with battery-electric rigid truck platforms designed for semi-autonomous operation in controlled mine environments.

Deere & Company: Through its construction equipment segment, Deere & Company targets articulated dump truck applications in construction and smaller-scale quarrying, with a strong North American dealer advantage and growing precision-grade telematics integration.

March 2024: Komatsu announced commercial availability of its 930E-5 AC electric drive haul truck with enhanced autonomous haulage integration, targeting iron ore and copper mine customers in Australia and Chile with a 363-tonne gross vehicle weight rating.

January 2024: Caterpillar unveiled its Cat 793 battery electric haul truck prototype, designed for 240-tonne payload capacity, and confirmed pilot deployments with two major North American copper mining clients scheduled for late 2024.

November 2023: Liebherr and Fortescue Metals Group signed a memorandum of understanding to co-develop a hydrogen fuel cell haul truck platform targeting 300-tonne class payloads, with initial field trials targeted for 2026.

September 2023: XCMG Group launched its XDE440 electric drive mining truck in the Chinese domestic market, rated at 440 tonnes gross vehicle weight and claiming a 30% reduction in energy cost per tonne-kilometre versus diesel equivalents.

June 2023: The European Union formally adopted updated Stage V emissions regulations extending to non-road mobile machinery above 560 kW, directly affecting large mining truck engines and setting a compliance timeline of 2026 for new type approvals.

February 2023: AB Volvo completed field validation of its A60H articulated dump truck with hybrid-electric powertrain at a quarry site in Sweden, demonstrating a 35% fuel consumption reduction in short-haul cycle operations.

October 2022: SANY Group inaugurated its dedicated mining truck manufacturing facility in Changsha, China, with an annual production capacity of 5,000 units targeting both domestic and export markets.

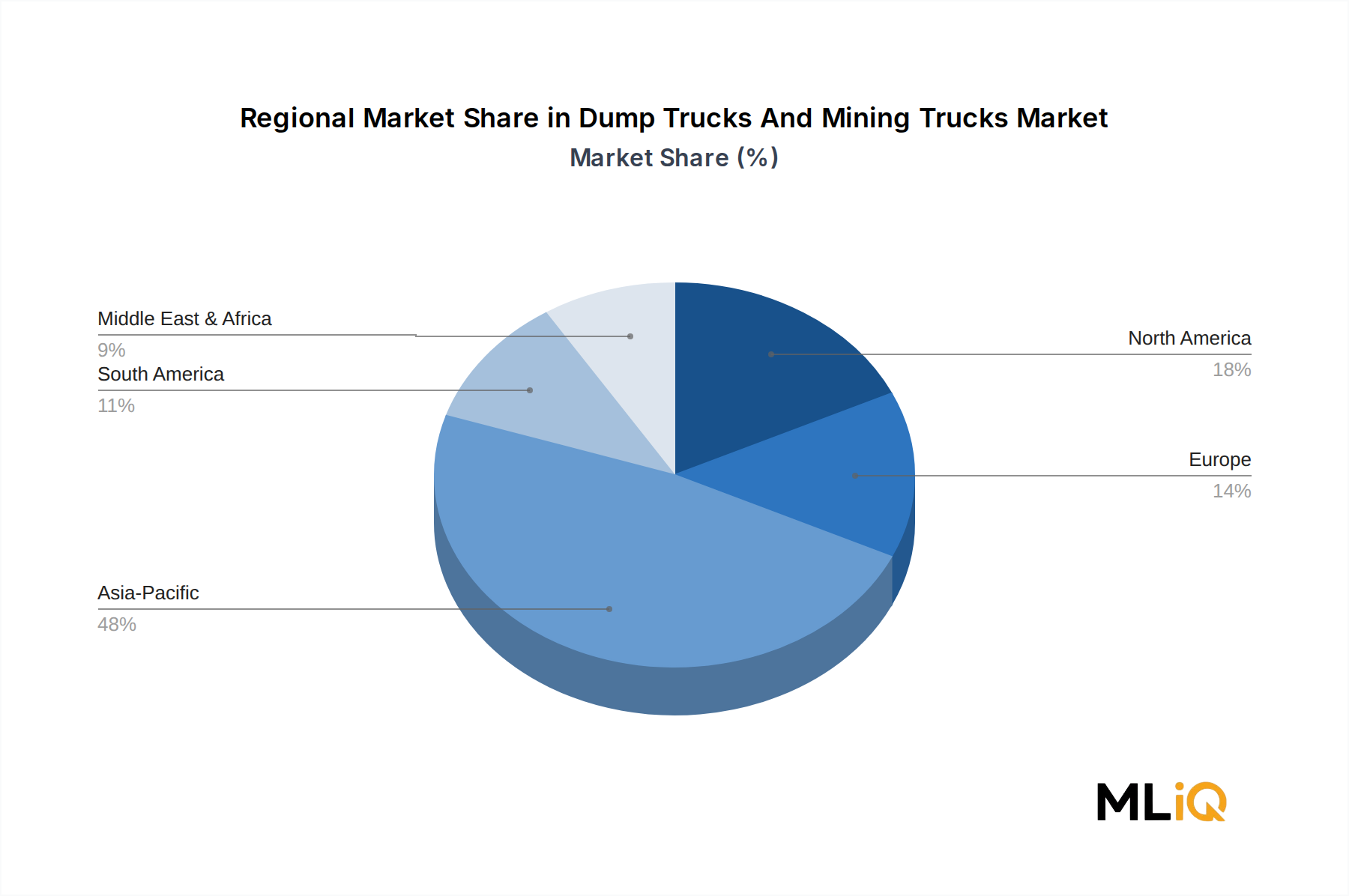

The Dump Trucks And Mining Trucks Market exhibits distinct regional demand profiles driven by varying infrastructure maturity, mining intensity, and regulatory environments.

Asia Pacific is both the largest and the fastest-growing regional market, accounting for approximately 38–42% of global revenue. China alone represents the single largest national market, driven by sustained infrastructure investment, coal and rare earth mining activity, and a domestic OEM ecosystem producing competitive price-point products. India is the region's fastest-growing sub-market, with a CAGR estimated at 9.1% through 2030, underpinned by its National Infrastructure Pipeline, coal mine expansions under the Ministry of Coal's auction program, and iron ore production increases in Odisha and Jharkhand. ASEAN markets — particularly Indonesia, the Philippines, and Vietnam — are experiencing strong growth in nickel, coal, and bauxite mining, sustaining robust procurement of mid- and large-class dump trucks.

North America represents the second-largest regional market, with a revenue share of approximately 22–25% and a CAGR of 6.2%. The United States is the primary growth engine, supported by the Bipartisan Infrastructure Law, reshoring of critical mineral supply chains (copper, lithium, cobalt), and ongoing expansion of Canadian oil sands operations. Mexico is emerging as a growth hotspot with increasing foreign direct investment in automotive manufacturing parks requiring extensive earthmoving activity.

Europe holds an estimated 15–18% market share, with growth at approximately 5.8% CAGR, driven by Scandinavian mining activities (iron ore, copper, nickel), German and French infrastructure renewal programs, and the EU's Critical Raw Materials Act mandating domestic sourcing of strategic minerals.

The Middle East and Africa region is the highest-potential emerging market, with a projected CAGR of 8.3%, propelled by large-scale Saudi Vision 2030 construction programs (NEOM, Red Sea Project), South African platinum and gold mining fleet renewal, and greenfield copper and cobalt mining developments in the Democratic Republic of Congo and Zambia.

South America, with a CAGR of approximately 7.0%, is underpinned by Chile and Peru's dominant copper mining sectors, and Brazil's expanding iron ore and agricultural infrastructure investments. Argentina's emerging lithium carbonate sector is also beginning to create incremental demand.

The supply chain underlying the Dump Trucks And Mining Trucks Market is complex, globally distributed, and exposed to multiple upstream volatility vectors that influence OEM production costs and delivery lead times.

Steel is the primary structural input, comprising approximately 60–70% of a typical haul truck's body mass. Hot-rolled coil and high-strength structural steel prices experienced sharp volatility between 2020 and **2023

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.4% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Dump Trucks And Mining Trucks Market market expansion.

Key companies in the market include AB Volvo, XCMG Group, Komatsu, Zoomlion Heavy Industry Science and Technology Co., Ltd., Liebherr, Caterpillar, Hitachi Construction Machinery Co., Ltd., Scania, Deere & Company, SANY Group.

The market segments include Type, Payload Class, Engine Type, End-use Industry.

The market size is estimated to be USD 60.54 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Dump Trucks And Mining Trucks Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Dump Trucks And Mining Trucks Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.