1. What are the major growth drivers for the Shoe Packaging Market market?

Factors such as are projected to boost the Shoe Packaging Market market expansion.

Shoe Packaging Market

Shoe Packaging Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

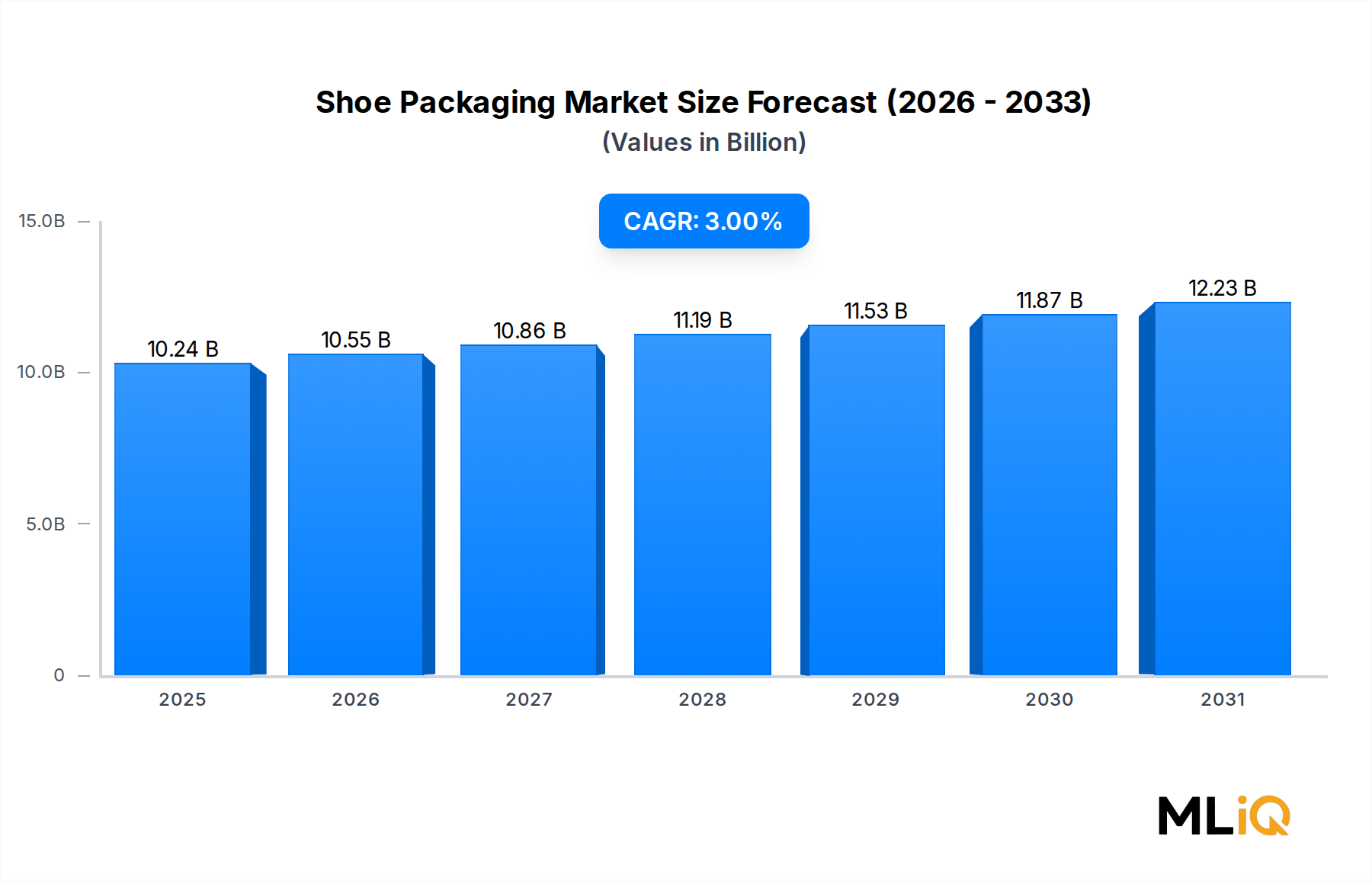

The global Shoe Packaging Market was valued at $10.24 billion in the base year and is projected to expand at a compound annual growth rate (CAGR) of 3% over the forecast period, reflecting steady, demand-driven growth underpinned by rising global footwear consumption, accelerating e-commerce adoption, and growing regulatory pressure toward sustainable materials. The market is poised to reach approximately $13.0 billion by the end of the forecast horizon, cementing its position as a structurally important subsegment of the broader packaging industry.

Demand fundamentals remain robust across both developed and emerging markets. The global footwear industry continues to expand in unit volume terms, with consumers in Asia Pacific and Latin America driving incremental purchases in athletic, casual, and formal categories. Each pair of shoes sold through retail or direct-to-consumer channels requires at minimum one primary packaging unit — most commonly a rigid paperboard box — creating a near-one-to-one correlation between footwear sales growth and packaging demand.

Macro tailwinds reinforcing this growth trajectory include the rapid scaling of online retail channels, which now demand more protective, brand-expressive, and damage-resistant packaging solutions than traditional brick-and-mortar formats. E-commerce penetration in footwear is estimated to exceed 35% globally, with certain markets in Southeast Asia and North America surpassing 45%, compelling brands to invest in secondary and tertiary packaging upgrades.

Sustainability megatrends represent both a driver and a constraint. Brands including premium athletic and luxury fashion labels are actively reformulating packaging portfolios to incorporate post-consumer recycled fibers, water-based adhesives, and soy-based inks, responding to both consumer sentiment surveys and incoming packaging legislation across the European Union and California. These reformulation efforts introduce near-term cost pressures but also catalyze product innovation and supplier differentiation.

From a materials perspective, paper-based substrates continue to command dominant share, benefiting from their recyclability profile and printability advantages. Plastic-based formats retain relevance in heavy-duty and industrial footwear segments where moisture resistance is non-negotiable. The flexible packaging sub-format is gaining traction in direct-to-consumer subscription and resale markets.

Key demand drivers include brand premiumization strategies among athletic footwear companies, the expansion of organized retail in India and Southeast Asia, and the rise of limited-edition and collectible sneaker culture, which elevates unboxing experience as a marketing channel. Forward-looking, the market is expected to benefit from increased investment in smart packaging — incorporating QR codes, NFC chips, and augmented-reality triggers — that transforms the shoebox from a commodity container into an interactive brand asset.

Rigid paper-based boxes constitute the single largest segment by revenue share within the Shoe Packaging Market, accounting for an estimated 58–62% of total market value in the base year. This dominance is deeply structural, rooted in decades of consumer expectation, retail shelf requirements, supply chain standardization, and material cost efficiency that collectively make rigid paper construction the default specification across mass-market, mid-tier, and premium footwear categories alike.

The primacy of rigid boxes traces historically to the logistical advantages they offered early footwear retailers: stackability for warehouse efficiency, printable surfaces for inventory SKU management, and sufficient structural integrity to protect shoes through multi-touch supply chains. These attributes remain as relevant today as they were at market inception, and they have been compounded by new advantages in the sustainability narrative. Paperboard and corrugated board derive from renewable fiber sources, are widely accepted in municipal recycling streams, and carry a lower perceived environmental impact relative to molded plastic clamshells or multi-layer laminate alternatives.

From a technical standpoint, rigid shoe boxes are typically fabricated from either solid bleached sulfate (SBS) board or clay-coated newsback (CCNB) substrates, with wall thicknesses calibrated to target weight classes — lightweight fashion heels requiring thinner caliper material than steel-toed work boots or basketball shoes. Grammages typically range from 300 gsm to 500 gsm for lid-and-base formats, while single-wall corrugated configurations for heavier footwear may reach 600 gsm equivalent combined flute and liner weights.

Key players operating at scale within the rigid segment include Samrat Box Mfg. Co. Pvt. Ltd., which has built a vertically integrated supply chain for premium shoebox manufacturing in India; Cross Country Box Company, which serves mid-market and athletic footwear brands across North America with standardized and custom die-cut configurations; and Zhuhai Zhuoya Packing Product Ltd., which leverages China's lower labor and raw material costs to produce high-volume rigid boxes for export-oriented footwear manufacturers across Guangdong Province.

Brand premiumization is accelerating within this segment. Premium and luxury shoe brands — including those in the fashion-forward and performance athletic categories — are increasingly specifying rigid boxes with special finishes such as soft-touch lamination, hot-foil stamping, UV spot varnish, and embossed logos. These value-added treatments elevate the average selling price of a shoebox from roughly $0.30–$0.80 for a commodity offset-printed configuration to $2.00–$5.00 or higher for full-premium specifications, substantially improving margin profiles for packaging converters with the requisite press and finishing capabilities.

The segment's revenue share is consolidating rather than expanding. Flexible packaging formats are capturing incremental share in the lightweight fashion and direct-to-consumer replenishment markets, while some sustainable-design-forward brands have experimented with molded pulp and honeycomb board formats. Nevertheless, rigid paper boxes retain an entrenched structural advantage in shelf-retail and wholesale distribution contexts, and the transition costs — tooling changes, supply chain requalification, consumer expectation management — are sufficient to deter rapid mass migration to alternative formats.

Distribution channel dynamics further reinforce rigid box dominance. Offline retail, which still represents a substantial majority of global footwear transaction volume by unit count, requires packaging that can withstand repeated handling, display stacking, and in-store customer interaction, criteria that rigid boxes satisfy more reliably than flexible alternatives. As long as physical retail remains a primary footwear go-to-market channel, rigid paper-based boxes will retain their commanding market position.

Several quantifiable forces are shaping the growth trajectory and structural evolution of the Shoe Packaging Market across the forecast period.

On the demand side, global footwear production volumes provide the most direct upstream driver. Industry data indicates that global footwear output exceeded 24 billion pairs annually in recent years, with China alone accounting for approximately 57% of global production by volume. Each production unit requires at minimum one packaging unit for domestic distribution or export logistics, creating a baseline demand floor that grows proportionally with footwear output. A projected annual footwear unit growth of 2–3% through the mid-2030s translates directly into sustained packaging volume expansion.

E-commerce channel penetration represents a second quantifiable driver. Online footwear sales require packaging that can withstand the rigors of last-mile delivery — typically involving 3–5 handling events between fulfillment center pick and consumer doorstep delivery — as compared to 1–2 handling events in traditional retail logistics. This structural difference drives both a quality upgrade cycle (thicker boards, tamper-evident closures, reinforced corners) and a secondary packaging layer requirement (outer cartons or mailer envelopes), effectively multiplying per-unit packaging spend.

Regulatory constraints are exerting measurable cost pressure. The European Union's Packaging and Packaging Waste Regulation (PPWR), which mandates minimum recycled content thresholds and recyclability standards, is requiring packaging suppliers serving EU-market footwear brands to reformulate material specifications. Compliance investment estimates suggest a 5–12% increase in input costs for converters transitioning to recycled-content paperboard substrates, a burden that is only partially offset by operational efficiencies.

Raw material price volatility constitutes a persistent constraint. Pulp and recovered fiber prices have exhibited significant cyclicality, with benchmark OCC (Old Corrugated Container) prices fluctuating by as much as 40–60% within single calendar years during recent commodity cycle peaks. These swings compress converter margins and introduce pricing uncertainty into long-term supply agreements, complicating strategic planning for both packaging producers and footwear brand procurement teams.

The competitive landscape of the Shoe Packaging Market is moderately fragmented, with a mix of large-format regional converters, specialty boutique suppliers, and vertically integrated manufacturers serving brand clients across price tiers and geographies.

Zhuhai Zhuoya Packing Product Ltd.: A China-based manufacturer with high-volume rigid and flexible shoebox production capabilities, primarily serving OEM footwear manufacturers across the Pearl River Delta, leveraging cost-competitive labor and close proximity to raw material suppliers.

Packaging of the World: A digital showcase and sourcing platform for innovative packaging designs that curates and promotes creative shoe packaging concepts, functioning as a design reference and supplier discovery channel for global footwear brands.

Elevated Packaging: Specializes in premium unboxing-centric packaging solutions for direct-to-consumer and luxury footwear brands, emphasizing soft-touch finishes, magnetic closures, and sustainable substrate options to support brand storytelling objectives.

Packman Packaging Pvt. Ltd.: An India-based packaging company offering a broad product range that includes customized shoe boxes manufactured from kraft and coated paperboard substrates, serving domestic footwear exporters and organized retail chains across South Asia.

Cross Country Box Company: A North America-focused corrugated and paperboard box manufacturer with dedicated shoe packaging product lines, serving athletic and casual footwear brands with standardized and custom configurations optimized for retail shelf and e-commerce logistics.

Packqueen: An Australia-based supplier offering custom-printed retail packaging with a strong focus on small-to-medium footwear and fashion brands, providing low minimum order quantities and rapid-turnaround digital print capabilities to serve emerging brand clients.

Precious Packaging: Operates in the premium and luxury packaging segment, delivering high-specification rigid shoe boxes with advanced embellishment techniques including foil stamping, embossing, and specialty lamination for high-end footwear and fashion accessory clients.

Royal Packers: A packaging manufacturer with production capabilities across multiple material types, serving footwear, apparel, and retail clients with a flexible product portfolio spanning folding cartons, rigid boxes, and corrugated solutions.

Samrat Box Mfg. Co. Pvt. Ltd.: A vertically integrated Indian manufacturer with deep expertise in rigid shoebox production, supplying both domestic branded footwear companies and export-oriented manufacturers across the Indian subcontinent.

Sneakerbox Co.: A niche supplier focused specifically on the collectible and premium sneaker segment, offering branded keepsake boxes and archival-quality packaging that caters to the rapidly growing sneaker resale and collector community.

January 2024: A major European athletic footwear conglomerate announced the rollout of 100% recycled-content paperboard shoeboxes across its entire product range in the EU market, targeting elimination of virgin fiber inputs by 2026 in compliance with incoming PPWR mandates.

March 2024: Cross Country Box Company expanded its production capacity at its Midwest manufacturing facility, commissioning a new high-speed flatbed die-cutting line capable of processing 15,000 blanks per hour, increasing output capacity for athletic shoe box formats by an estimated 22%.

June 2024: A prominent direct-to-consumer sneaker brand introduced NFC-chip-embedded shoeboxes in a limited-edition product run, enabling consumers to authenticate product provenance, access exclusive digital content, and register warranty claims via smartphone tap.

September 2024: Packman Packaging Pvt. Ltd. received FSC Chain of Custody certification for its shoe packaging production lines, enabling its footwear brand clients to include certified sustainable packaging claims in their product marketing materials across export markets.

November 2024: An Asia Pacific regional trade body published updated voluntary guidelines for shoe packaging recyclability labeling, recommending standardized iconography and material identification codes across member markets to reduce consumer confusion at end-of-life disposal.

February 2025: A luxury fashion group piloted a shoebox-return-and-reuse program in three European flagship cities, offering consumers incentive credits for returning intact packaging at point-of-sale, with recovered boxes refurbished and redeployed in secondary distribution channels.

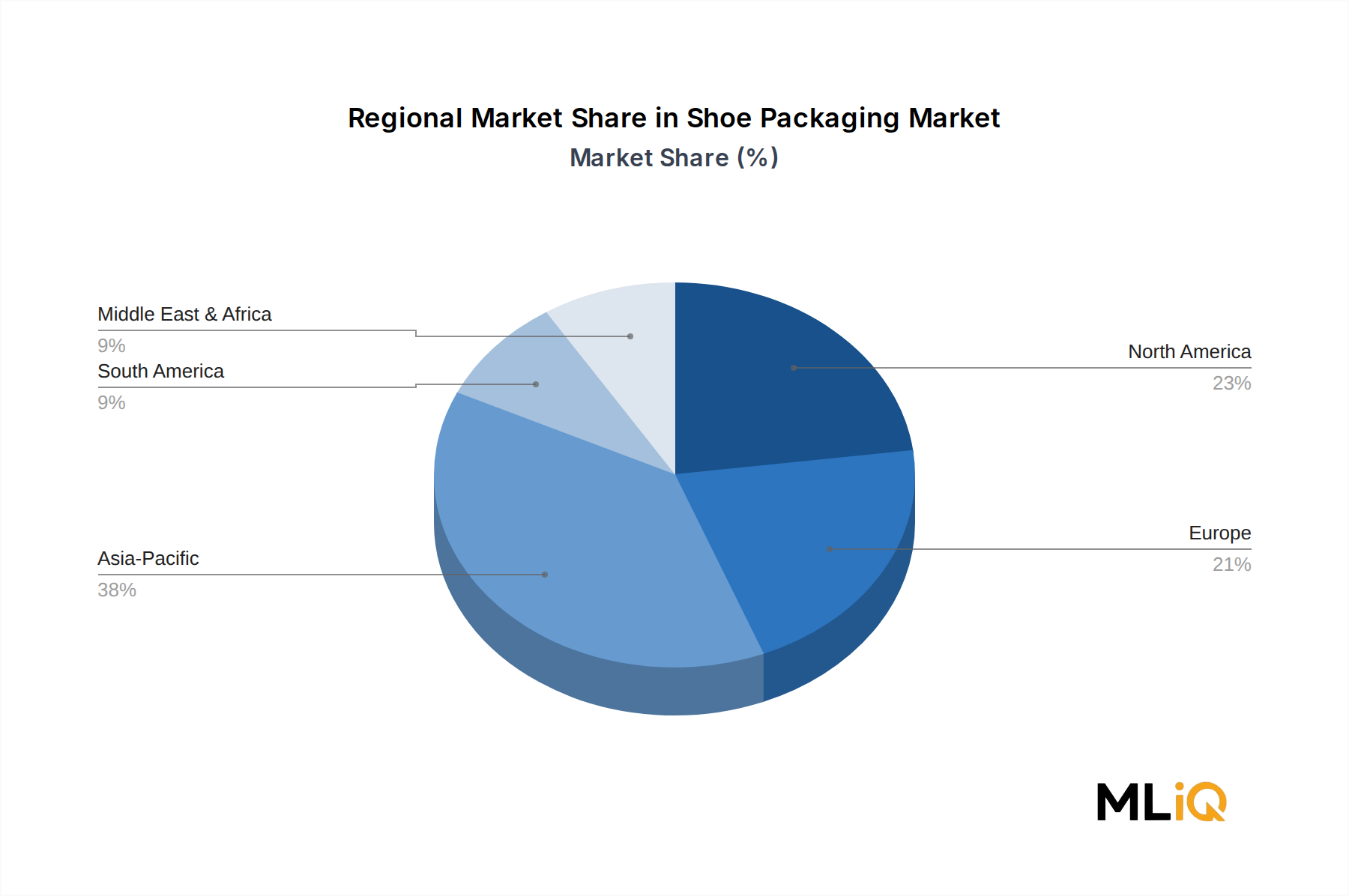

The Shoe Packaging Market exhibits significant regional variation in growth rates, market maturity, material preferences, and demand drivers, reflecting the underlying heterogeneity of global footwear production and consumption geographies.

Asia Pacific is unambiguously the largest regional market by both volume and value, estimated to account for approximately 42–46% of global Shoe Packaging Market revenue in the base year. China dominates within the region, functioning simultaneously as the world's largest footwear producer and a rapidly growing domestic consumer market. Regional CAGR is estimated at 4.1%, above the global average, driven by rising middle-class footwear consumption in India, Vietnam, Indonesia, and the Philippines, as well as continued export manufacturing expansion in Vietnam and Bangladesh as brands diversify supply chains away from China-only dependency. India's organized retail expansion and growing e-commerce footwear penetration make it a particularly high-velocity sub-market within Asia Pacific.

North America represents the most mature regional market, with estimated revenue share of 22–25% of global value. The United States dominates within the region, characterized by high per-capita footwear spend, a large athletic and performance footwear segment, and well-developed e-commerce infrastructure. Regional CAGR is estimated at 2.4%, reflecting market maturity but sustained by premiumization trends, growing demand for sustainable packaging specifications, and the resurgent collectible sneaker culture driving premium box investment. Canada and Mexico contribute incremental growth, with Mexico benefiting from nearshoring of footwear manufacturing for North American brands.

Europe accounts for an estimated 18–20% of global Shoe Packaging Market value, with regional CAGR of approximately 2.8%. Germany, the United Kingdom, France, and Italy are the primary demand centers, serving both domestic consumption and luxury footwear export manufacturing. The region is the most regulatory-advanced globally with respect to packaging sustainability mandates, which is accelerating reformulation investment and creating differentiation opportunities for converters with certified recycled-content supply chains. The Nordics and Benelux markets demonstrate above-average receptivity to premium sustainable packaging formats.

Latin America is an emerging growth market, with Brazil and Argentina as primary demand centers and estimated regional CAGR of 3.5%. Brazil's large domestic footwear manufacturing sector and growing retail formalization are the primary demand drivers. Middle East and Africa remains an early-stage market, with aggregate revenue share below 5%, but GCC markets and South Africa exhibit growing organized retail penetration that is creating new demand for branded shoe packaging solutions at sustainable above-average regional growth rates.

The Shoe Packaging Market serves a structurally layered customer base, ranging from global footwear conglomerates with centralized procurement functions to independent boutique brands purchasing in small batch quantities through distributors or online configurator platforms.

Mass-market footwear manufacturers, including those producing private-label and value-tier products for discount retail chains, represent the highest-volume buyer cohort. Their primary purchasing criteria are unit cost minimization, supply reliability, and dimensional standardization. Price sensitivity is extremely high; switching decisions are frequently triggered by as little as a 3–5% unit price differential between qualified suppliers. Procurement is typically centralized, contract-based with annual or biannual renegotiation cycles, and heavily influenced by raw material cost benchmarks rather than brand differentiation narratives.

Mid-tier branded footwear companies balance cost discipline with brand expression requirements. These buyers increasingly specify custom print and finish options — full-bleed lithographic printing, matte lamination, brand-color Pantone matching — while maintaining unit cost targets that constrain the degree of premiumization achievable. Their procurement

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Shoe Packaging Market market expansion.

Key companies in the market include Zhuhai Zhuoya Packing Product Ltd., Packaging of the World, Elevated Packaging, Packman Packaging Pvt. Ltd., Cross Country Box Company, Packqueen, Precious Packaging, Royal Packers, Samrat Box Mfg. Co. Pvt. Ltd., Sneakerbox Co..

The market segments include Type, Material, Distribution Channel.

The market size is estimated to be USD 10.24 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Shoe Packaging Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Shoe Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.