1. What are the major growth drivers for the Roofing Tiles Market market?

Factors such as are projected to boost the Roofing Tiles Market market expansion.

+1 2315155523

Roofing Tiles Market

Roofing Tiles Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

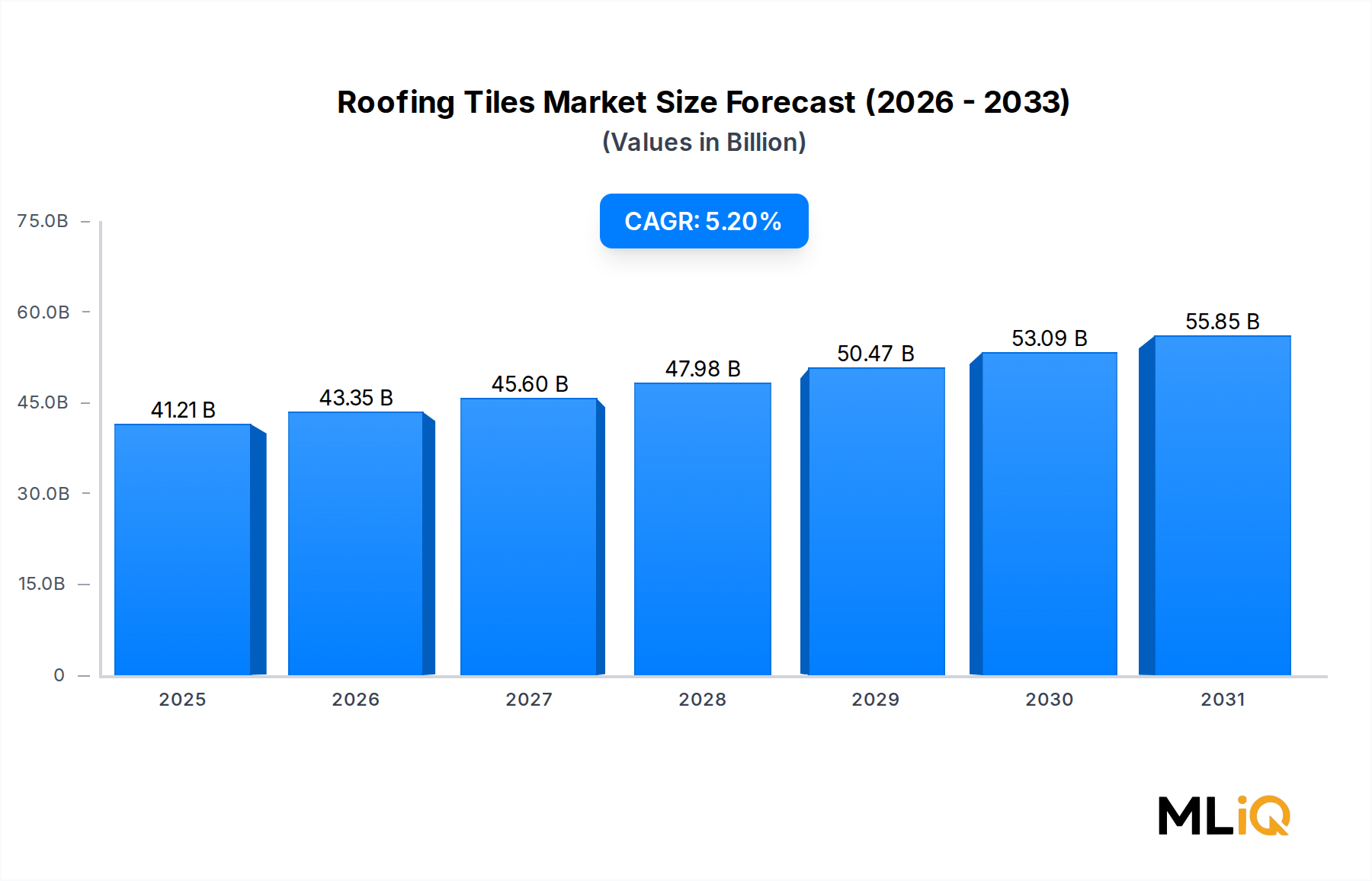

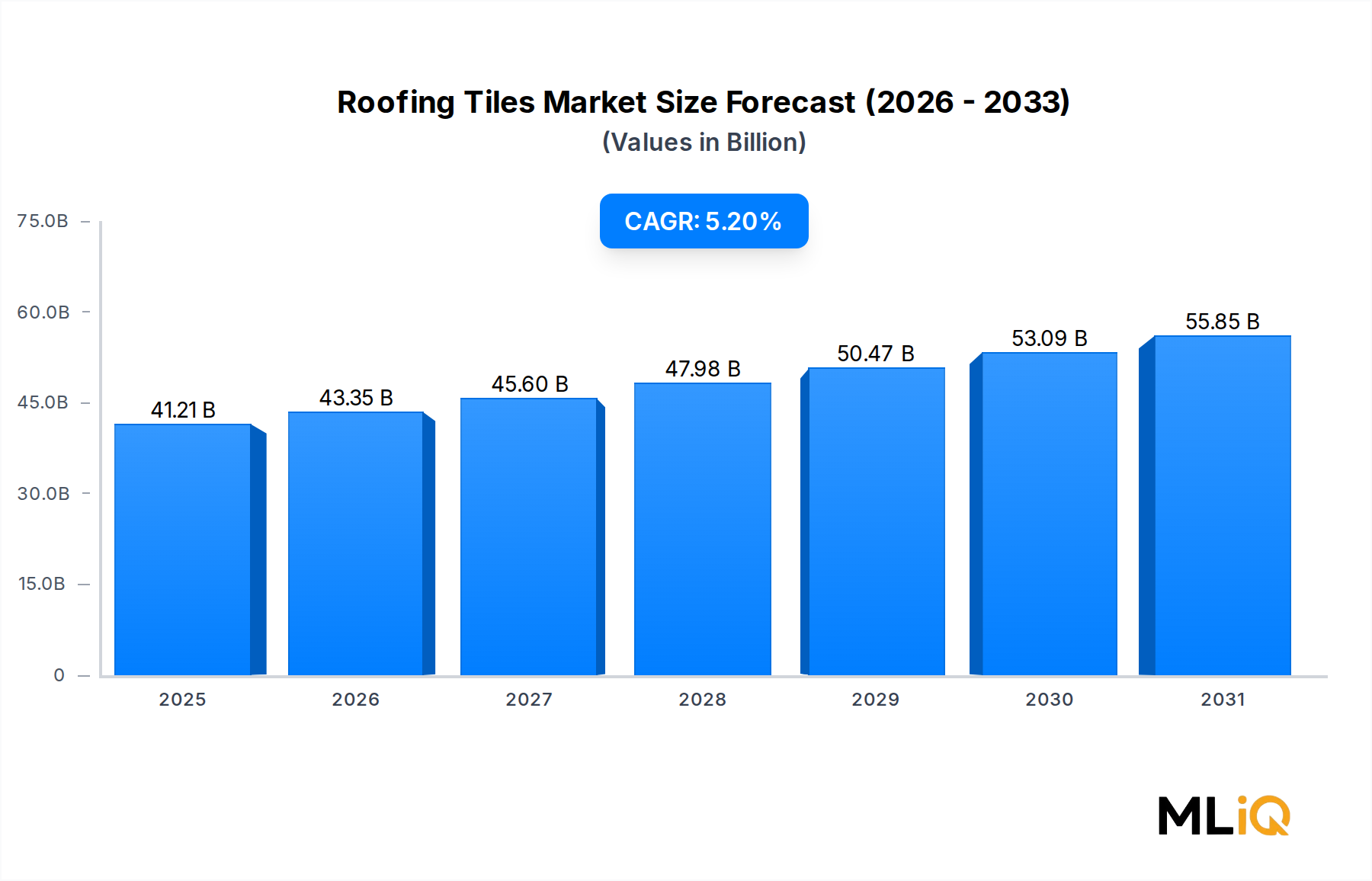

The global Roofing Tiles Market is valued at $41,206.72 million as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 5.2% through 2033. This sustained growth trajectory reflects a confluence of urbanization pressures, rising infrastructure investment, and an accelerating renovation cycle in both developed and emerging economies. The market sits at the intersection of materials science, construction demand, and sustainability policy, making it one of the more technically complex segments within the broader Building Materials Market.

Key demand drivers include the sustained housing boom across Asia Pacific, where urban population inflows are generating persistent demand for new residential construction. In parallel, Europe and North America are witnessing a structural renovation wave, driven by aging housing stock and tightening energy-efficiency codes that mandate thermally superior roofing solutions. Government stimulus programs in post-pandemic economies have also channeled capital into public infrastructure, indirectly boosting non-residential roofing demand.

Macro tailwinds include the global push toward low-carbon construction. Green building certifications such as LEED and BREEAM are increasingly specifying high-albedo, thermally efficient, or recycled-content roofing tiles, expanding the addressable premium segment of the market. The proliferation of solar-integrated roofing systems is further elevating the technical sophistication of tile products, blurring the boundary between roofing and energy generation.

From a material standpoint, clay tiles retain their dominant position due to their longevity, aesthetic appeal, and proven thermal properties. Concrete tiles are gaining ground on cost and versatility, while the "Others" category — encompassing composite, fiber-cement, and polymer-based tiles — is the fastest-growing sub-segment in percentage terms, albeit from a smaller base.

Looking forward to 2033, the market is expected to generate incremental value driven by product premiumization, digital manufacturing advances (including 3D-printed tile profiles), and the integration of photovoltaic cells. Supply-side consolidation among tier-one manufacturers is expected to improve margin profiles, while competitive pressure from low-cost Asian producers will continue to challenge incumbents in price-sensitive geographies. Overall, the Roofing Tiles Market presents a compelling combination of defensive demand characteristics and growth optionality through innovation.

Among all material segments within the Roofing Tiles Market, clay tiles command the largest revenue share, a position reinforced by centuries of proven performance, architectural tradition, and expanding modern reformulations that address legacy weight and installation cost concerns. Clay tiles typically account for over 40% of total market revenue globally, with particularly strong penetration in Europe, the Mediterranean region, Latin America, and parts of Southeast Asia where terracotta aesthetics remain culturally embedded in residential and commercial architecture.

The dominance of the clay tile segment is underpinned by several structural factors. First, clay tiles carry an industry-leading service life of 50 to 100 years, a lifecycle economic argument that resonates with homeowners, insurers, and institutional property owners alike. This longevity reduces total cost of ownership despite higher upfront installation costs relative to asphalt or concrete alternatives. Second, the thermal mass properties of fired clay contribute measurably to building energy efficiency, aligning the segment with evolving regulatory requirements across the European Union and North America.

The Clay Roof Tiles Market, as a standalone segment, has drawn sustained investment from leading manufacturers seeking to modernize production through tunnel kiln efficiency upgrades, automated glazing systems, and the development of lightweight clay tile variants that expand the range of roof structures capable of bearing clay products. These innovations are critical to overcoming the primary barrier to clay tile adoption — structural loading requirements that add cost to roof framing.

Key players operating prominently within the clay tile segment include Ludowici Roof Tile, whose handcrafted and machine-made product lines serve the premium residential and historic preservation segments across North America and Europe. Terreal Malaysia Sdn Bhd maintains a strong position in the ASEAN clay tile market, leveraging regional raw material access and cost-competitive manufacturing. MCA Clay Roof Tile is a significant North American producer focused on residential new construction and renovation, with a portfolio that emphasizes color durability and installation efficiency.

The segment's revenue share is consolidating rather than expanding in mature markets, as concrete and composite alternatives capture incremental growth in cost-sensitive new construction. However, in premium renovation, heritage districts, and high-end residential development, clay tile share is holding firm or growing modestly. The integration of solar-ready clay tile profiles — designed to accept flush-mounted photovoltaic cells — represents a significant near-term product development vector that could reignite growth in the segment.

Market participants in the clay tile segment are also navigating raw material sourcing complexity. Premium-grade ball clay and kaolin are geographically concentrated, creating supply chain dependencies that differentiate producers with vertically integrated quarrying operations. Dachziegelwerke Nelskamp GmbH exemplifies this model in Central Europe, maintaining proprietary clay extraction operations that provide quality consistency and cost insulation from spot market volatility.

Overall, the clay tile segment's leadership within the Roofing Tiles Market is durable, anchored in material science advantages and deep cultural adoption, but it is increasingly dependent on product innovation to defend share against the growing versatility and cost competitiveness of concrete and composite alternatives.

The Roofing Tiles Market is propelled by a set of measurable, data-supported demand drivers balanced against specific structural constraints that modulate the pace and geography of growth.

Urbanization is the single most powerful demand driver. The United Nations projects that 68% of the world's population will reside in urban areas by 2050, up from approximately 56% in 2023. This translates directly into housing construction demand across Asia Pacific, Sub-Saharan Africa, and Latin America. China and India alone account for a disproportionate share of global new residential starts, creating sustained volume demand for roofing materials, including tiles.

Renovation activity is the dominant demand driver in mature markets. In the European Union, approximately 75% of the building stock is considered energy-inefficient under current standards. The EU Renovation Wave initiative targets the deep renovation of 35 million buildings by 2030, with roofing upgrades a mandatory component of energy performance retrofits. This policy-driven renovation cycle adds a structural, non-cyclical demand floor to the European Roofing Tiles Market.

Climate resilience investment is an emerging driver. As extreme weather events increase in frequency and severity, property owners and insurers are investing in impact-resistant, fire-rated, and wind-resistant roofing systems. Tiles, particularly concrete and clay, carry inherently superior durability ratings versus asphalt shingles, driving specification upgrades in hurricane-prone and wildfire-adjacent regions.

On the constraints side, the high installation cost and structural weight of tile roofing remain the most significant adoption barriers, particularly in the Residential Roofing Market for entry-level and mid-market housing. Tile systems require specialized labor for installation, and skilled roofing tradespeople are in short supply across North America and Western Europe, inflating labor costs and extending project timelines. Raw material price volatility — particularly for cement, kaolin, and ball clay — creates margin compression risk for manufacturers operating on fixed-price contracts.

The competitive landscape of the Roofing Tiles Market is moderately consolidated at the global tier, with regional specialists maintaining significant share in local markets. Key participants include:

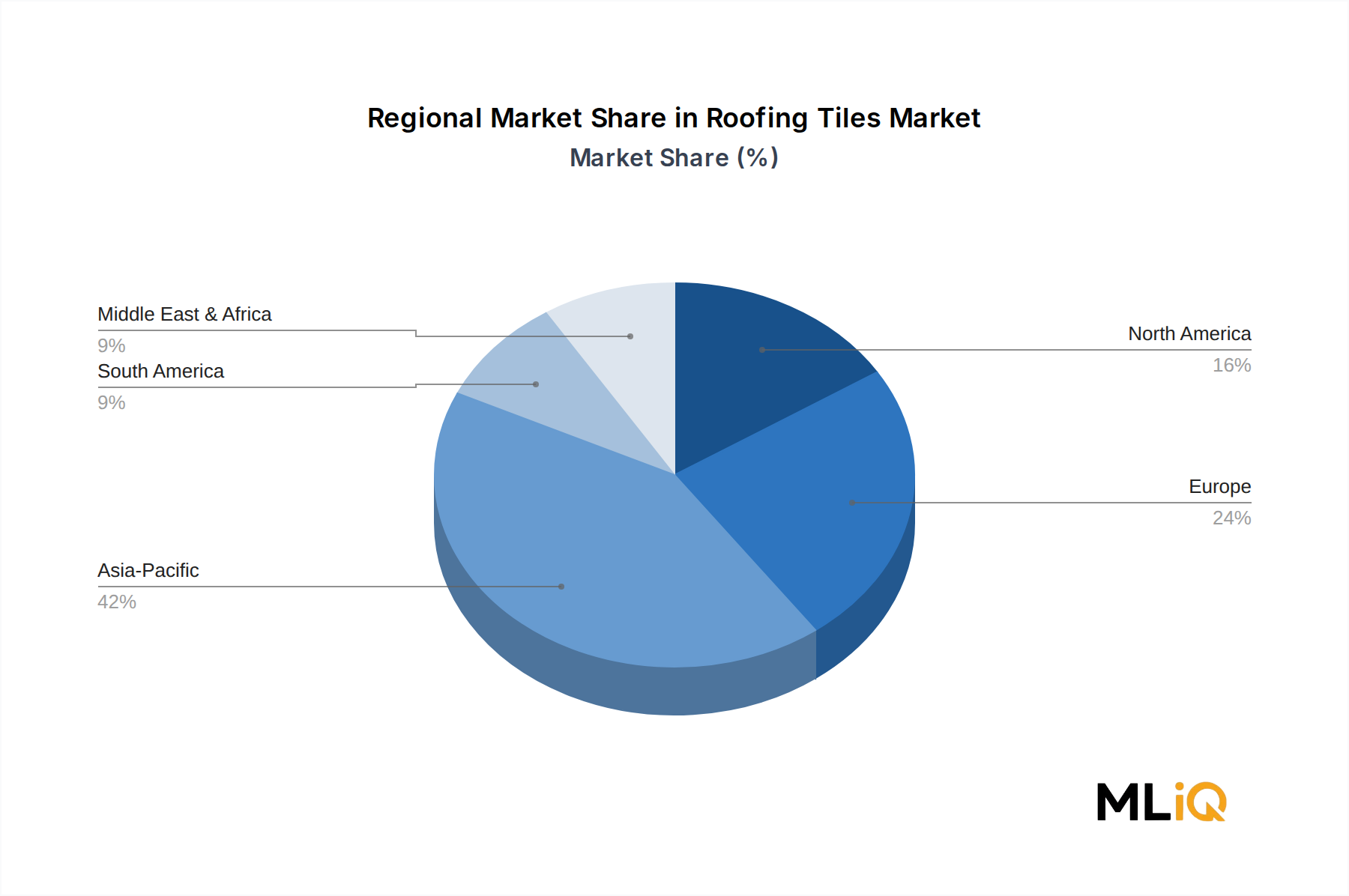

The Roofing Tiles Market exhibits distinct regional growth profiles driven by divergent construction cycles, regulatory environments, and material preference traditions.

Asia Pacific is both the largest regional market and the fastest-growing, accounting for an estimated 38–42% of global revenue. China and India are the primary growth engines, with China's housing completions — despite the ongoing real estate sector deleveraging — still generating enormous tile volume demand. India is emerging as the highest incremental growth market, with urbanization, government housing programs such as Pradhan Mantri Awas Yojana, and rising middle-class homeownership driving a structural demand uplift. The Asia Pacific regional CAGR is estimated at approximately 6.1% through 2033, outpacing the global average.

Europe represents the most technically sophisticated and premium-oriented regional market, with Germany, France, Italy, and the UK collectively generating the largest European revenue pool. European demand is increasingly renovation-driven, supported by the EU Renovation Wave and national energy efficiency grant programs. The regional CAGR is estimated at 4.2%, reflecting maturity tempered by regulatory tailwinds. France and Germany are the largest clay tile markets by volume within Europe.

North America is a mature but innovation-active market, with the U.S. Sun Belt states — Texas, Florida, Arizona, and California — representing the highest concentration of tile roofing adoption due to climate suitability and architectural style preferences. The North American market is growing at an estimated 4.8% CAGR, supported by hurricane hardening mandates in coastal states and rising demand for fire-resistant roofing in wildfire-prone western regions.

Middle East & Africa is an emerging growth region, with Gulf Cooperation Council (GCC) construction programs — particularly in Saudi Arabia under Vision 2030 — generating significant non-residential roofing demand. South Africa and North Africa represent the most developed tile markets within the broader African continent. The regional CAGR is estimated at 5.6%.

Latin America, led by Brazil and Argentina, holds a culturally deep clay tile tradition and is growing at an estimated 4.9% CAGR, driven by social housing programs and informal sector construction formalization.

The Roofing Tiles Market is exposed to a layered set of upstream supply chain dependencies that vary significantly by product type. For clay tiles, the primary raw materials are ball clay, kaolin, and red-firing earthenware clay. These inputs are geographically concentrated — premium kaolin deposits are located primarily in the United Kingdom, Germany, Brazil, and the United States — creating sourcing concentration risk for manufacturers lacking proprietary quarrying operations. Clay input prices have trended upward at approximately 3–5% annually over the past five years, driven by energy-intensive extraction and processing costs.

For concrete tiles, the primary inputs are Portland cement, fine aggregate (sand), and pigment oxides. The Cement and Aggregates Market has experienced significant price volatility since 2021, with global cement prices rising 15–20% in key markets due to energy cost inflation, carbon pricing mechanisms, and supply chain disruption from geopolitical events. Sand availability is an underappreciated constraint; construction-grade sand shortages have been documented in Southeast Asia and Sub-Saharan Africa, with implications for concrete tile producers operating in these regions.

Firing energy represents a critical cost input for clay tile manufacturers. Natural gas prices — the primary kiln fuel in Europe and North America — exhibited extreme volatility between 2021 and 2023, with European spot prices reaching unprecedented levels following the Russia-Ukraine conflict. This event structurally increased the cost of clay tile production in Europe and accelerated investment in alternative energy sources, including hydrogen-ready kilns and biomass co-firing systems.

Logistics costs have also elevated supply chain risk. Roofing tiles are heavy, fragile, and low-value-to-weight ratio products, making them highly sensitive to freight cost inflation. The 2021–2022 container shipping price surge increased delivered costs for Asian-manufactured tiles exported to North American and European markets by 30–50%, temporarily improving the competitiveness of domestic producers.

The Waterproofing Membranes Market is an adjacent supply chain component, as underlays and secondary waterproofing membranes are co-installed with roofing tiles; price movements in polymer and bitumen inputs that affect membrane costs can influence overall roofing system pricing dynamics and installer project economics.

The regulatory environment governing the Roofing Tiles Market is becoming progressively more demanding, particularly with respect to energy performance, fire resistance, and environmental content standards.

In the European Union, the revised Energy Performance of Buildings Directive (EPBD), adopted in 2024, mandates near-zero energy standards for all new buildings and establishes minimum energy performance requirements for major renovations. Roofing is explicitly addressed as a primary heat-loss pathway, driving specification upgrades toward thermally superior tile systems with compatible insulation assemblies. The EU Taxonomy for Sustainable Finance is

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Roofing Tiles Market market expansion.

Key companies in the market include Boral Limited, .Eagle Roofing, EcoStar LLC, Ludowici Roof Tile, Dachziegelwerke Nelskamp GmbH, Crown Roof Tiles, Marley Ltd, Shital Potteries, MCA Clay Roof Tile, Terreal Malaysia Sdn bhd.

The market segments include Material Type, Construction Type, End-User.

The market size is estimated to be USD 41206.72 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3456, USD 5769, and USD 10995 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Roofing Tiles Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Roofing Tiles Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.