1. What are the major growth drivers for the Metallizer Market market?

Factors such as are projected to boost the Metallizer Market market expansion.

+1 2315155523

Metallizer Market

Metallizer Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

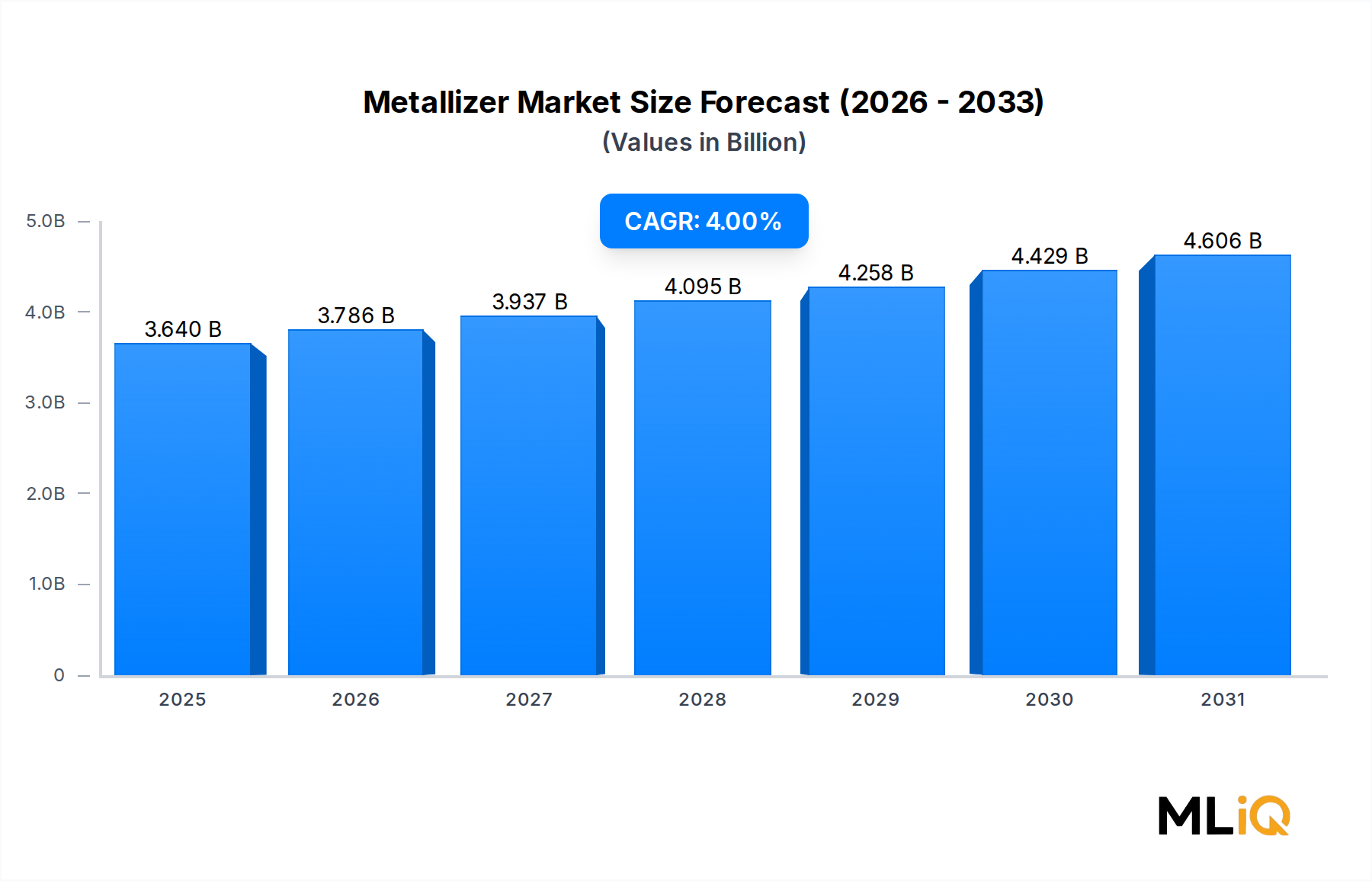

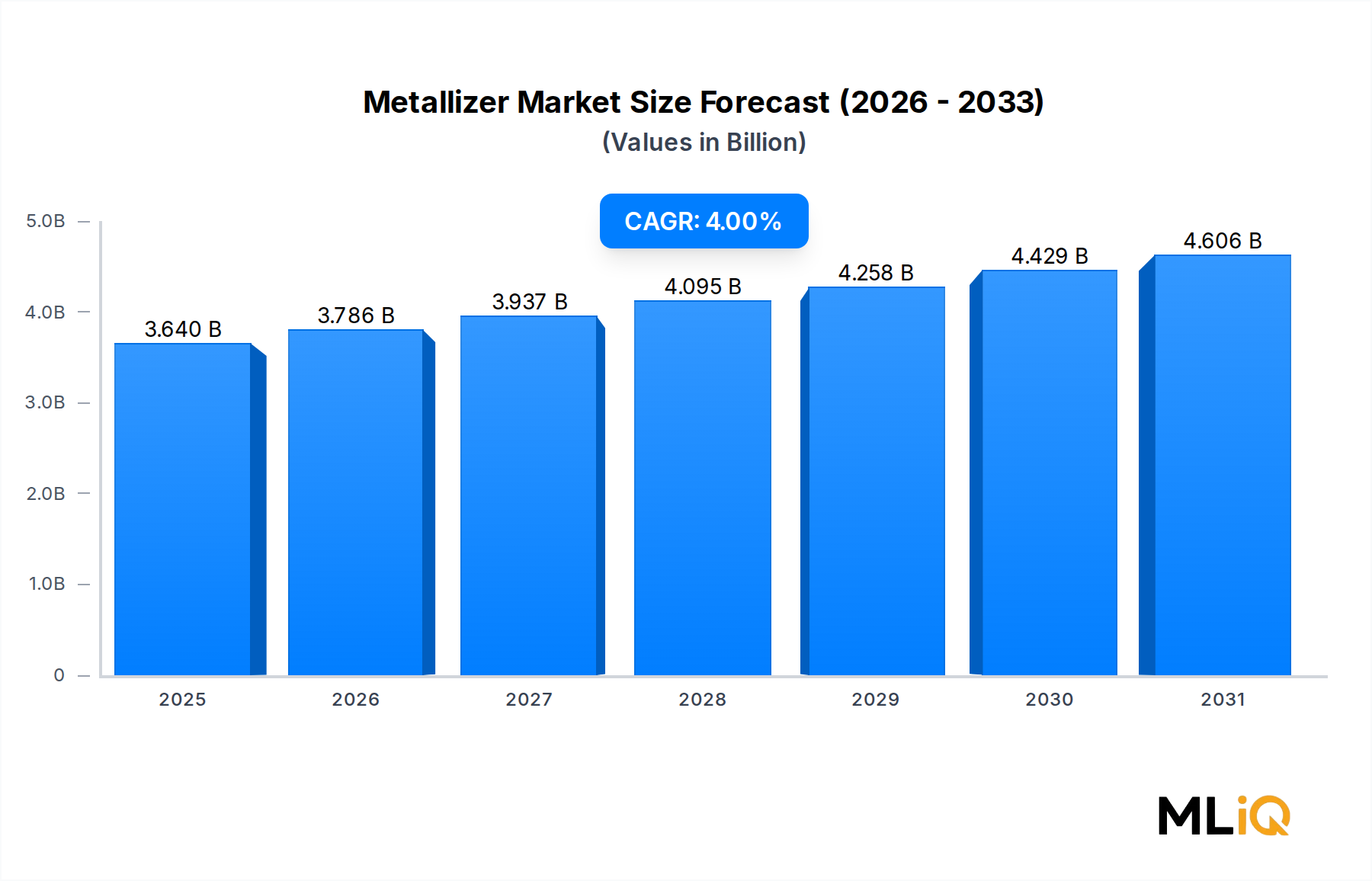

The global Metallizer Market is valued at $3.64 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 4% through 2033, reaching an estimated $4.98 billion by the end of the forecast period. This steady trajectory reflects robust industrial demand across packaging, cosmetics, laminations, and electronics sectors, underpinned by accelerating consumer goods production and technological upgrades in thin-film deposition systems.

Metallizers — machines and systems used to deposit ultra-thin metallic coatings, predominantly aluminum, onto substrates such as PET, PP, and BOPP films — play an indispensable role in modern packaging and functional film manufacturing. The surge in flexible and barrier packaging solutions across food and beverage, pharmaceutical, and personal care markets continues to act as the primary demand catalyst. End-use industries are under growing pressure to deliver extended shelf life, enhanced aesthetics, and material cost savings simultaneously, and metallized films satisfy all three requirements with unparalleled efficiency.

Macro tailwinds supporting sustained Metallizer Market growth include the global shift away from rigid packaging toward lightweight flexible solutions, heightened regulatory emphasis on food safety and barrier performance, and the rapid expansion of organized retail in emerging economies. Asia Pacific remains the epicenter of volume growth, driven by China's massive converting industry and India's accelerating flexible packaging sector. North America and Europe, while relatively mature, are experiencing renewed capital expenditure cycles as manufacturers replace aging metallizer lines with high-speed, energy-efficient platforms capable of processing next-generation substrates.

From a technology standpoint, the transition from conventional batch-type metallizers to continuous roll-to-roll vacuum systems is redefining throughput economics. Modern platforms achieve deposition speeds exceeding 800 meters per minute and optical densities (OD) tailored between 1.5 and 3.5, enabling precise performance engineering for specific packaging applications. Energy consumption per unit of metallized film has declined by approximately 12–15% over the past five years due to advances in crucible heating and electron-beam evaporation technology.

The competitive landscape is moderately consolidated, with a handful of vertically integrated players and specialty film converters dominating global capacity. Innovation in alternative barrier metallization substrates — including biodegradable PLA and paper-based films — is expanding the total addressable market while aligning the industry with circular economy mandates. Investment in R&D for transparent metallized barriers (replacing traditional opaque aluminum deposits) is an emerging frontier, particularly relevant for microwave-compatible and recyclable packaging formats.

Overall, the Metallizer Market presents a compelling investment thesis combining stable volume growth, technology-led margin expansion, and geographic diversification opportunities across both developed and high-growth emerging markets.

Among all application segments tracked within the Metallizer Market — packaging, laminations, cosmetics, and others — the packaging segment commands the largest revenue share, consistently accounting for an estimated 55–60% of total global market value. This dominance is structural, rooted in the irreplaceable functional and economic advantages metallized films provide to food and beverage, pharmaceutical, and consumer goods packaging supply chains.

Metallized packaging films deliver a unique combination of barrier properties (against oxygen, moisture, and light), reflective aesthetics, and compatibility with high-speed converting and printing lines. Aluminum-metallized PET and BOPP films, for instance, achieve oxygen transmission rates (OTR) below 0.5 cc/m²/day and water vapor transmission rates (WVTR) below 0.5 g/m²/day, performance parameters comparable to much heavier foil laminates at a fraction of the material cost and carbon footprint.

The food and beverages end-use sector alone accounts for the largest sub-segment within packaging applications, driven by the global processed and packaged food industry — valued at over $3.2 trillion globally — which relies on barrier films to preserve product integrity and extend shelf life without refrigeration. Snack food, confectionery, dry ingredients, and ready-to-eat meal packaging represent the highest-volume categories utilizing metallized films from metallizer equipment.

Pharmaceutical packaging constitutes the fastest-growing sub-application within the packaging segment, expanding at a sub-CAGR of approximately 5.2% over the forecast period. Blister packaging, pouch sealing, and sachet formats for nutraceuticals and OTC medications demand stringent barrier performance and tamper-evidence features, making metallized film an optimal substrate. Regulatory tightening around drug stability and packaging integrity standards — particularly under ICH Q1B and USP 671 guidelines — further reinforces the preference for high-barrier metallized solutions.

Key players concentrating their metallizer capacity within the packaging segment include Uflex Ltd, Jindal Polyfilms Ltd, SRF Limited, and Polyplex, all of which operate large-scale roll-to-roll vacuum metallizers dedicated to serving flexible packaging converters. Uflex Ltd, for example, operates one of the largest integrated flexible packaging complexes in Asia, with multiple metallizer lines producing metallized PET, BOPP, and cast PP films primarily destined for food packaging applications.

The packaging segment's share is not merely holding steady — it is consolidating further as secular trends reinforce its position. The global e-commerce boom has amplified demand for protective, lightweight packaging that maintains product condition during transit. Direct-to-consumer food delivery services require hermetically sealed, barrier-optimized pouches. Sustainability mandates are redirecting interest toward ultra-thin metallized films that reduce overall packaging mass while maintaining performance, further increasing the volume of substrate processed through metallizer equipment.

Laminations represent the second-largest application segment at approximately 20–22% of market revenue, supporting decorative and functional multilayer film constructions across apparel, printing, and industrial uses. The cosmetics segment, while smaller at approximately 8–10% of revenue, commands premium pricing and thus contributes disproportionately to margin profiles for metallizer operators serving high-end personal care and luxury goods brands. The "others" category encompasses agricultural films, insulation facers, and security printing substrates, rounding out a diversified application portfolio.

Looking ahead to 2033, the packaging segment is expected to retain its leadership position while gradually integrating newer metallized substrate types — including paper-based and compostable films — as consumer brands accelerate packaging sustainability commitments and demand recyclable barrier solutions compatible with existing metallizer infrastructure.

The Metallizer Market is propelled by a set of quantifiable demand drivers while simultaneously navigating structural and cyclical constraints that moderate growth velocity.

Driving forces begin with the accelerating global flexible packaging industry. The Flexible Packaging Market, a critical demand vector for metallizer output, is expanding at a CAGR of approximately 4.5–5% globally, directly pulling capacity investment in metallizing equipment and services. Every percentage point of flexible packaging penetration gained against rigid alternatives translates into measurable incremental demand for metallized film substrates.

Rising consumer spending in Asia Pacific and Latin America is a second quantified driver. Disposable income growth in India, Southeast Asia, and Brazil is fueling organized retail expansion and branded packaged goods consumption. India's packaged food sector alone is projected to grow from approximately $55 billion in 2024 to over $85 billion by 2030, generating sustained demand for domestically produced metallized packaging films and, consequently, for metallizer capacity additions.

Technology-driven efficiency gains represent a third driver, enabling manufacturers to reduce per-unit conversion costs. Modern high-speed metallizers process films at speeds up to 800 meters per minute, compared to 400–500 meters per minute for legacy systems installed in the early 2010s. This throughput doubling effectively halves per-square-meter processing cost, accelerating return on capital and incentivizing capacity reinvestment cycles.

On the constraints side, raw material input volatility poses a persistent challenge. Aluminum, the primary evaporant material, is subject to global commodity price fluctuations influenced by energy costs and smelting capacity constraints. A 10% increase in aluminum ingot prices directly compresses conversion margins for metallizer operators who cannot immediately pass costs through to converting customers on long-term contracts.

Environmental regulatory pressure presents a structural constraint in developed markets. European Union packaging regulations under the Packaging and Packaging Waste Regulation (PPWR), finalized in 2024, are pushing brand owners to redesign packaging for recyclability, which in some cases disadvantages traditional aluminum-metallized multilayer constructions that are difficult to separate during mechanical recycling. This drives near-term reformulation costs and some demand displacement toward alternative barrier technologies.

High capital intensity for metallizer equipment — with new wide-web vacuum metallizing systems priced between $3 million and $8 million per unit — restricts market entry for smaller converters and concentrates capacity expansion decisions among well-capitalized incumbents.

The Metallizer Market features a competitive landscape shaped by vertically integrated film manufacturers, dedicated metallizing service providers, and equipment technology specialists. Below is a strategic profile of the principal market participants:

Sumilon Industries Ltd.: A major Indian flexible packaging manufacturer with significant metallizer capacity dedicated to producing metallized PET and BOPP films for domestic and export packaging markets. The company leverages cost-competitive production and scale in India to serve price-sensitive regional converters.

Sumilon Polyester Ltd: Operates as a complementary entity within the Sumilon group, focusing on polyester film production that feeds directly into metallizing lines, enabling tightly integrated supply chain control from resin to finished metallized product.

Ester Industries Ltd: One of India's leading polyester film manufacturers, Ester Industries has invested in vacuum metallizing capacity to produce value-added metallized PET films targeted at packaging and industrial lamination applications across domestic and international markets.

Jindal Polyfilms Ltd: A flagship company of the B.C. Jindal Group, Jindal Polyfilms operates one of the largest BOPP and PET film manufacturing complexes globally, with extensive metallizer capacity serving food packaging, labeling, and industrial application segments across Asia, Europe, and the Americas.

Toray Industries Ltd: A global materials science leader headquartered in Japan, Toray brings advanced polymer and film technology expertise to metallized film production, with particular strength in high-performance, ultra-thin substrates for electronics and specialty packaging applications.

Uflex Ltd: India's largest flexible packaging conglomerate, Uflex operates an integrated platform spanning films, inks, adhesives, and machinery — including in-house metallizer lines — that serves clients across 140+ countries with metallized packaging solutions.

Surtech Industries, Inc.: A specialized metallizing service provider offering toll metallizing and surface treatment services to converters seeking outsourced metallizing capacity without capital commitment to dedicated equipment.

Polyplex: A global manufacturer of PET and BOPP base films with metallizing operations across multiple continents, Polyplex supplies metallized films to packaging converters across Asia, Europe, and North America with a strong emphasis on product consistency and barrier performance reliability.

Tapematic Spa: An Italian manufacturer of vacuum metallizing equipment for the cosmetics and luxury packaging sector, Tapematic specializes in batch metallizers used for decorative applications on caps, closures, and rigid cosmetic packaging components.

SRF Limited: A diversified Indian chemicals and packaging films conglomerate, SRF operates advanced metallizer lines producing BOPET and BOPP metallized films for food packaging, agricultural applications, and industrial laminates across global markets.

January 2024: Uflex Ltd announced the commissioning of a new wide-web vacuum metallizing line at its Noida facility, increasing annual metallized film capacity by approximately 15,000 metric tons and targeting growing demand from the snack food and confectionery packaging sector.

March 2024: Jindal Polyfilms Ltd unveiled a strategic investment plan of approximately INR 1,200 crore for capacity expansion across its film and metallizing operations in India, with new lines expected to come online by 2026.

June 2024: SRF Limited completed qualification trials for a new ultra-thin 8-micron metallized BOPET film for pharmaceutical blister and sachet applications, achieving barrier performance compliant with ICH Q1B stability testing requirements.

September 2024: Toray Industries Ltd announced a partnership with a European flexible packaging converter to develop a recyclable monomaterial metallized film structure compatible with polyolefin recycling streams, targeting EU PPWR compliance requirements effective 2030.

November 2024: Polyplex Corporation disclosed the commissioning of a new electron-beam metallizing system at its Thailand facility, capable of processing films at speeds of 750 meters per minute with enhanced uniformity for high-optical-density applications.

February 2025: Tapematic Spa launched the "Galaxy 3.0" batch metallizer platform at the Milano Unica trade exhibition, featuring AI-driven process control for cosmetic packaging metallization with cycle time reductions of 18% versus the previous generation.

April 2025: Ester Industries Ltd signed a long-term supply agreement with a leading Indian FMCG company for metallized PET film supply, securing forward volume commitments through 2027 and supporting planned metallizer capacity utilization above 85%.

The Metallizer Market exhibits distinct regional dynamics, with Asia Pacific, North America, Europe, and the Middle East & Africa each representing differentiated growth profiles, demand structures, and investment intensities.

Asia Pacific is the dominant and fastest-growing region, accounting for approximately 48–52% of global Metallizer Market revenue in 2025. The region is projected to grow at a regional CAGR of 5.2–5.5% through 2033, outpacing the global average. China anchors this leadership through its massive flexible packaging converting industry and extensive domestic film manufacturing base. India is the highest-momentum market within the region, with metallizer capacity investments accelerating in line with food processing sector formalization and rising packaged consumer goods penetration. Southeast Asian nations — particularly Thailand, Vietnam, and Indonesia — are emerging as secondary investment destinations as global packaging converters establish regional manufacturing footprints.

North America represents the most mature Metallizer Market geography, holding approximately 20–22% of global revenue. The region grows at an estimated CAGR of 2.8–3.2%, reflecting market saturation in core flexible packaging applications offset by demand from pharmaceutical and specialty industrial uses. The United States drives North American volumes, with capacity investment concentrated on equipment modernization — replacing older batch metallizers with high-speed continuous systems — rather than net new capacity additions. Mexico is an emerging manufacturing hub within North America, attracting capacity relocation from higher-cost locations.

Europe accounts for approximately 18–20% of global Metallizer Market revenue, growing at a CAGR of 2.5–3.0%. Western European markets are navigating the tension between strong existing flexible packaging infrastructure and regulatory pressure under EU PPWR mandates requiring recyclable packaging by 2030. This is driving investment into next-generation transparent barrier metallization and monomaterial recyclable film structures, creating technology-led demand for upgraded or new metallizer equipment. Germany, France, Italy, and the United Kingdom lead European market activity.

The Middle East & Africa region, while representing only approximately 5–7% of global market value, is expanding at an above-average regional CAGR of 4.5–5.0%, driven by food processing investment in GCC countries, packaging infrastructure build-out in Turkey, and rising consumer goods demand across North Africa and South Africa. This region represents a long-term growth frontier for metallizer equipment suppliers and metallized film exporters from Asia.

South America contributes approximately 5–6% of global revenue, with Brazil and Argentina as primary markets, growing at a regional CAGR of approximately 3.5–4.0% supported by expanding retail food sectors.

The Metallizer Market is deeply embedded in global trade flows, with metallized films, base substrates, and metallizing equipment moving through complex cross-border supply chains connecting raw material producers, film manufacturers, metallizing converters, and end-use packaging markets.

Asia — led by India,

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Metallizer Market market expansion.

Key companies in the market include Sumilon Industries Ltd., Sumilon Polyester Ltd, Ester Industries ltd, Jindal polyfilms ltd, Toray Industries ltd, Uflex ltd, Surtech Industries, Inc., Polyplex, Tapematic Spa, SRF Limited.

The market segments include Type, Application, End Users.

The market size is estimated to be USD 3.64 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Metallizer Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Metallizer Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.