1. What are the major growth drivers for the Pneumatic Positioner Market market?

Factors such as are projected to boost the Pneumatic Positioner Market market expansion.

Pneumatic Positioner Market

Pneumatic Positioner Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

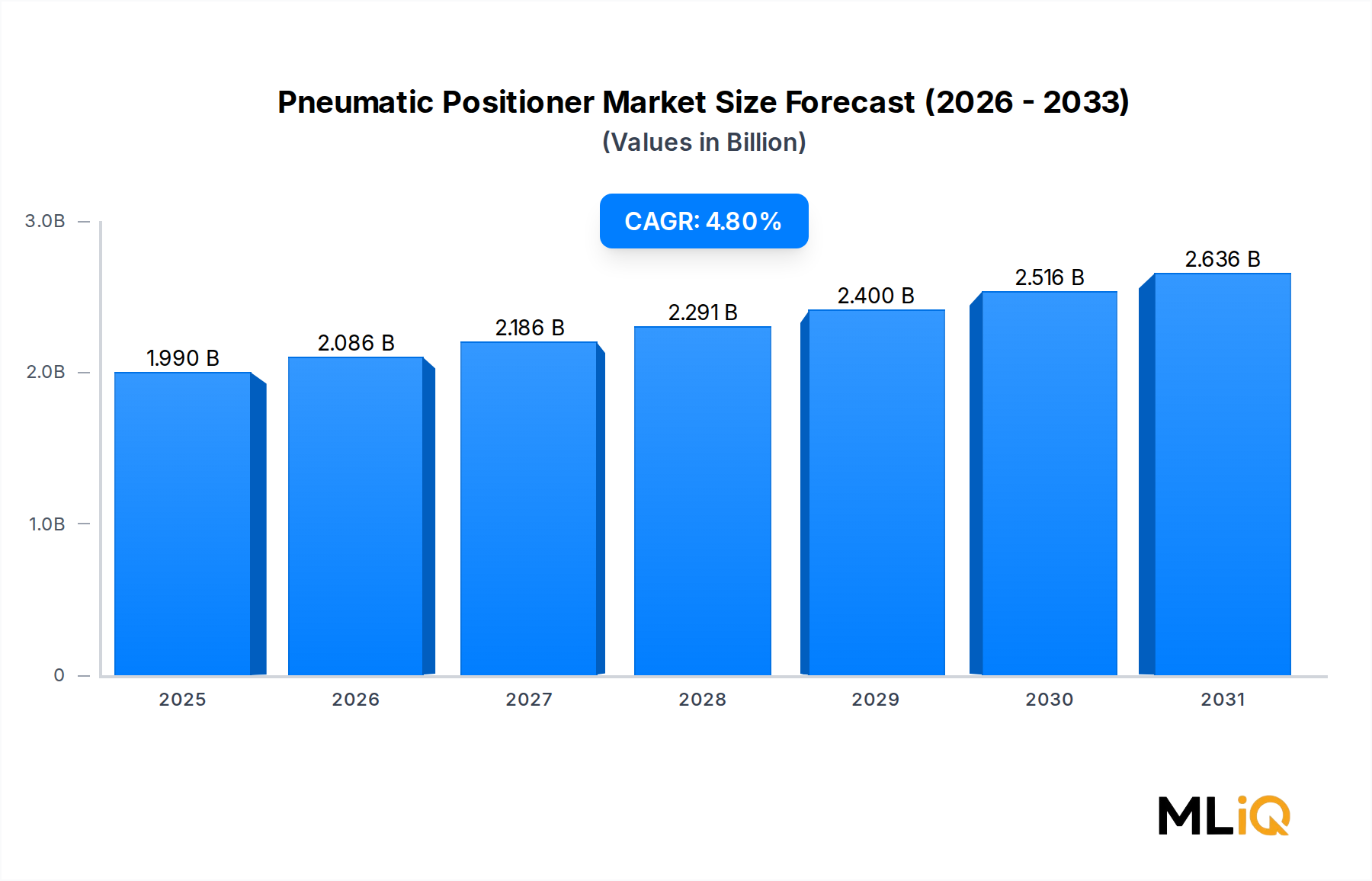

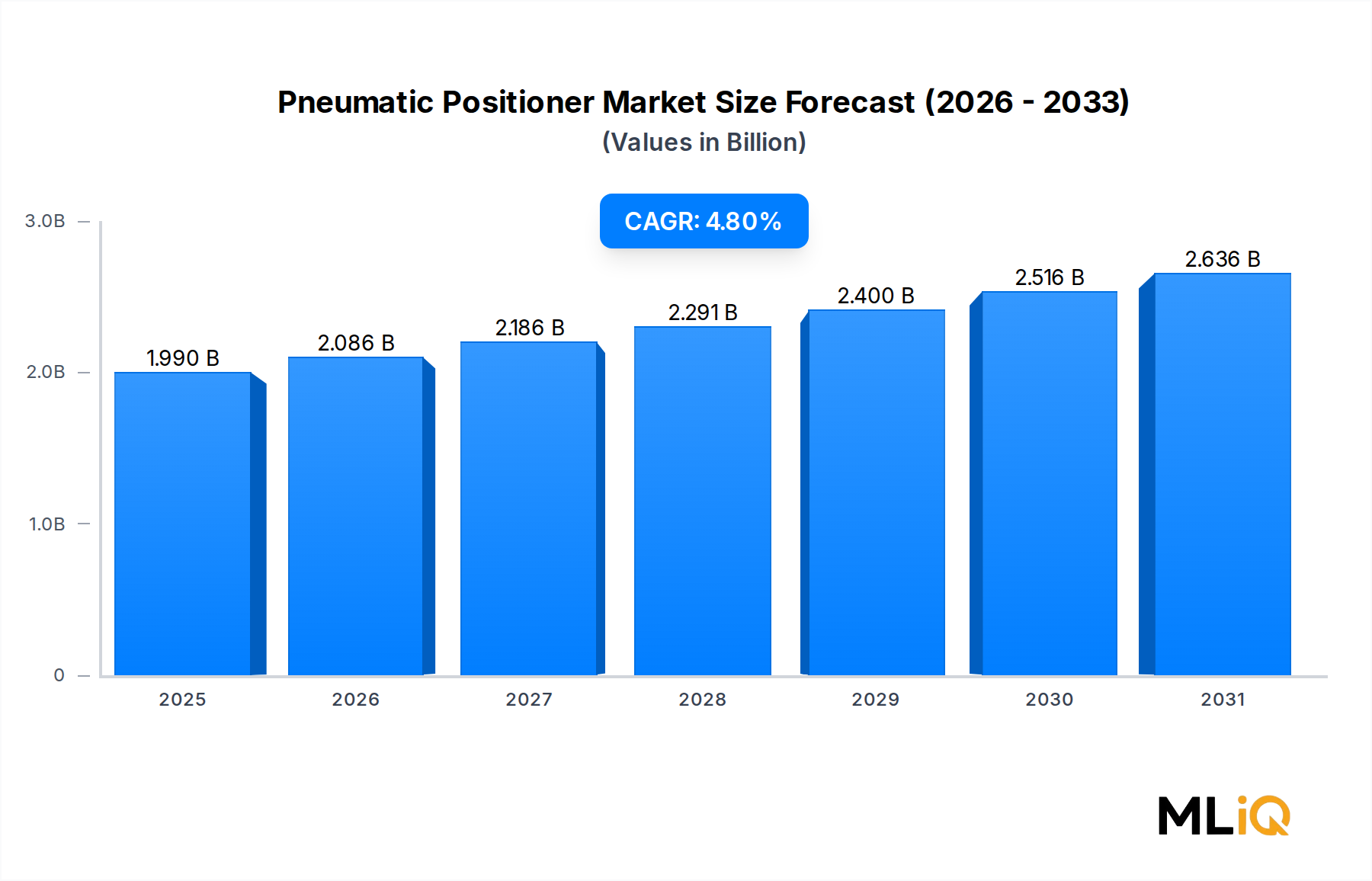

The global Pneumatic Positioner Market was valued at $1.99 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 4.8% through 2033, reflecting sustained capital investment in process automation, energy infrastructure, and industrial modernization. By the end of the forecast horizon, the market is expected to surpass $3.0 billion, driven by deepening penetration of automated control systems across oil and gas, chemical processing, and metals and mining end-use verticals.

Pneumatic positioners serve as critical feedback-and-control devices that regulate valve stem or rotary shaft positioning in response to pneumatic signals, ensuring that final control elements respond accurately to setpoint commands from distributed control systems (DCS) or programmable logic controllers (PLC). Their role as precision instruments in high-consequence process environments underpins persistent demand even as electro-pneumatic and digital variants gain traction.

Key demand drivers include rising global refinery throughput capacity expansions, particularly across the Middle East and Asia Pacific, where greenfield and brownfield projects are accelerating. The International Energy Agency (IEA) has noted continued capital expenditure in upstream and midstream oil and gas infrastructure, directly translating into valve and positioner procurement cycles. Simultaneously, the global push toward plant digitalization and Industry 4.0 frameworks is encouraging end-users to upgrade legacy pneumatic positioning devices to smart, diagnostics-capable units, creating replacement demand layered atop baseline growth.

Macro tailwinds include elevated commodity prices sustaining mining and petrochemical plant investments, tightening process safety regulations in the European Union and North America mandating precise valve control, and the proliferation of liquefied natural gas (LNG) terminals requiring high-performance instrumentation. In parallel, the expanding chemical manufacturing base in India, China, and Southeast Asia is generating substantial first-time installation demand.

The competitive landscape remains moderately consolidated, with Rotork, Emerson Electric, ABB, Siemens, and Honeywell collectively accounting for a substantial portion of global revenue. These incumbents are differentiating through integrated digital positioner portfolios that offer HART, FOUNDATION Fieldbus, and PROFIBUS communication protocols, as well as predictive maintenance analytics. Smaller regional players and niche specialists compete on price and delivery lead times, particularly in Asia Pacific and Latin America.

Looking forward, the convergence of pneumatic reliability with digital intelligence is expected to define the market's growth trajectory. Manufacturers investing in hybrid electro-pneumatic architectures and cloud-connectable valve diagnostics will command premium pricing and stronger aftermarket revenue streams, while commoditized single-acting and double-acting pneumatic units will face margin compression from low-cost Asian suppliers.

Among all product type segments, linear positioners represent the largest revenue-generating category within the Pneumatic Positioner Market, commanding an estimated 55–60% of total global revenue in 2024. This dominance is structural rather than cyclical, rooted in the widespread deployment of globe valves, gate valves, and diaphragm valves across high-volume process industries where straight-line stem movement is the standard actuation mode.

Linear positioners translate a pneumatic input signal — typically 3–15 psi or 0.2–1.0 bar — into a proportional mechanical displacement of the valve stem, ensuring tight correspondence between the controller output and the actual valve opening position. Their mechanical simplicity, proven reliability in aggressive environments, and compatibility with a broad range of valve body geometries make them the default specification for engineers across oil and gas, chemical and petrochemical, and power generation applications.

In oil and gas operations, linear positioners are extensively used on control valves in wellhead pressure regulation, pipeline flow control, separator level control, and heat exchanger bypass loops. The sector's exacting standards for leakage performance and shutoff classification (per ANSI/FCI 70-2 and IEC 60534-4) necessitate precise linear positioning, particularly for throttling service in high-differential-pressure applications. As global upstream and midstream capital expenditures remain elevated — with deepwater and LNG projects driving valve procurement — linear positioner demand in oil and gas is expected to grow at approximately 5.1% CAGR through 2033.

In the chemical and petrochemical sector, linear positioners are fundamental to reactor feed control, distillation column reflux management, and heat exchanger duty regulation. The chemical industry's trend toward continuous processing over batch manufacturing amplifies positioner utilization rates, as continuously operating valves require positioners with low hysteresis, high repeatability (within ±0.5% of full scale), and robust seat materials resistant to corrosive media.

Key players active in the linear positioner segment include Emerson Electric, which markets the Fisher FIELDVUE DVC6200 series with advanced diagnostics; Rotork, with its IQ3 and CK range; and ABB, whose TZIDC intelligent positioner family supports multiple fieldbus protocols. Siemens' SIPART PS2 positioner and Honeywell's SVI II AP series are also prominent specifications in large-scale EPC (Engineering, Procurement, and Construction) project bids globally.

The linear positioner segment's share is consolidating rather than expanding, as rotary positioners gain ground in applications utilizing ball, butterfly, and plug valves — equipment categories growing rapidly in water treatment and HVAC applications. Nevertheless, the absolute revenue contribution from linear positioners continues to increase in line with the overall market expansion, and the category is expected to remain dominant throughout the 2024–2033 forecast window.

Original equipment manufacturers (OEMs) are increasingly bundling linear positioners with valve bodies as factory-mounted, pre-calibrated assemblies, shortening installation timelines and reducing site commissioning costs. This integrated supply model strengthens long-term aftermarket relationships and creates recurring service revenue through scheduled re-calibration, diagnostic audits, and spare-parts contracts — all of which enhance the revenue quality of the leading linear positioner segment players.

The Pneumatic Positioner Market is shaped by a constellation of quantifiable drivers and material constraints that together determine growth velocity and investment attractiveness.

Driver 1 — Oil and Gas Capital Expenditure Recovery: Global upstream oil and gas capital expenditure rebounded to approximately $500 billion in 2023 and is expected to sustain levels above $480 billion annually through 2026, per the International Energy Forum. Each major greenfield refinery or LNG terminal project specifies several thousand control valves, each requiring a positioner, generating direct procurement volume. The Middle East GCC alone has announced over $150 billion in refinery and petrochemical expansion through 2030, representing a significant forward demand pipeline for pneumatic positioning equipment.

Driver 2 — Process Safety Regulation: The U.S. EPA's Risk Management Program (RMP) amendments finalized in 2024 and the EU's Seveso III Directive mandate tighter process integrity controls at chemical and refining facilities, indirectly driving positioner retrofit and upgrade cycles. Non-compliance penalties and incident liability exposure incentivize plant operators to replace aging, drift-prone positioners with calibrated, diagnostics-capable devices.

Driver 3 — Industrial Automation Adoption: Global spending on industrial automation hardware exceeded $200 billion in 2023, with DCS and PLC penetration increasing particularly in emerging markets. Every incremental control loop added to a process plant requires at least one positioner, creating a durable link between automation capital spending and positioner demand.

Constraint 1 — Electro-Pneumatic Substitution: Smart electro-pneumatic and fully electric actuator-positioner combinations are eroding the addressable market for pure pneumatic units in new installations. Digital positioners with HART or Fieldbus integration now represent a growing share of specification wins, compressing the volume growth available to traditional analog pneumatic positioners.

Constraint 2 — Supply Chain Disruptions: Precision-machined components, including spool valves, feedback linkages, and diaphragm assemblies, are subject to lead-time extensions during periods of manufacturing congestion. Post-pandemic supply normalization has improved but not fully resolved allocation challenges for specialty alloy components used in high-pressure positioner bodies.

The Pneumatic Positioner Market features a moderately consolidated competitive landscape dominated by global instrumentation and automation conglomerates, supplemented by regional specialists. Below is a strategic profile of the leading participants:

Rotork: A UK-headquartered actuator and flow control specialist, Rotork maintains a strong pneumatic positioner portfolio complemented by its IQ3 electric actuator range, enabling cross-selling across pneumatic and electric positioning solutions to EPC contractors globally.

Siemens: Siemens leverages its SIPART PS2 intelligent positioner platform, which supports HART, PROFIBUS PA, and FOUNDATION Fieldbus protocols, integrating seamlessly with its broader PCS 7 and SIMATIC process automation ecosystem.

ABB: ABB's TZIDC and TZID-C positioner families are engineered for high-cycle valve applications, and the company benefits from a global service network spanning over 100 countries, enabling lifecycle support contracts that generate recurring revenue.

Honeywell: Honeywell's SVI II AP smart valve interface positioner combines advanced diagnostics with HART 7 communication, targeting refineries and chemical plants where predictive maintenance is a strategic priority.

Emerson Electric: Emerson's Fisher FIELDVUE DVC series represents one of the most widely specified digital valve controllers globally, with an installed base numbering in the millions of units and a robust asset management software ecosystem via AMS Device Manager.

General Electric: GE's presence in the positioner space is anchored through its industrial controls and instrumentation divisions, serving power generation and pipeline infrastructure customers with ruggedized positioning solutions.

Azbil: The Japan-headquartered Azbil Corporation offers the AVP series of smart valve positioners with dual-nozzle flapper mechanisms, targeting high-precision applications in semiconductor manufacturing and pharmaceutical processing.

Baker Hughes: Baker Hughes competes primarily through its control valve and actuation solutions for upstream oil and gas and LNG applications, where positioners are specified as integrated valve-actuator package assemblies.

Schneider Electric: Schneider Electric integrates positioner offerings within its EcoStruxure plant automation architecture, appealing to customers seeking unified hardware-software control environments.

Flowserve: Flowserve's Valtek and Logix positioner brands serve the chemical processing and power generation sectors, with a focus on severe-service valve assemblies where positioner reliability under extreme temperature and pressure conditions is paramount.

January 2024: Emerson Electric announced the expansion of its Fisher FIELDVUE DVC6200 SIS series to support IEC 61511 Safety Instrumented System applications, targeting the rapidly growing safety valve positioner segment in LNG terminals and offshore platforms.

March 2024: ABB launched an enhanced version of its TZIDC positioner featuring an integrated partial stroke test (PST) function with on-board data logging, enabling compliance with IEC 61508 SIL 2 requirements without external test equipment.

May 2024: Rotork completed the acquisition of a European pneumatic actuator specialist, strengthening its positioner-actuator package integration capabilities for chemical and pharmaceutical end-users across continental Europe.

August 2024: Siemens introduced a firmware update for the SIPART PS2 positioner enabling native integration with its MindSphere Industrial IoT platform, allowing remote positioner health monitoring and predictive diagnostics via cloud dashboards.

October 2024: Honeywell announced a long-term supply agreement with a major Middle Eastern refinery operator to provide SVI III positioners and associated lifecycle services across a 2,500-valve instrumented pipeline network.

December 2024: Azbil received certification under the ATEX Directive for its AVP300 explosion-proof positioner variant, expanding its addressable market in European Zone 1 and Zone 2 classified hazardous areas in the chemical sector.

February 2025: Flowserve launched the Logix 3800MD positioner with modular diagnostic hardware, enabling field-upgradeable communication modules supporting both HART 7 and WirelessHART protocols without replacing the base positioner unit.

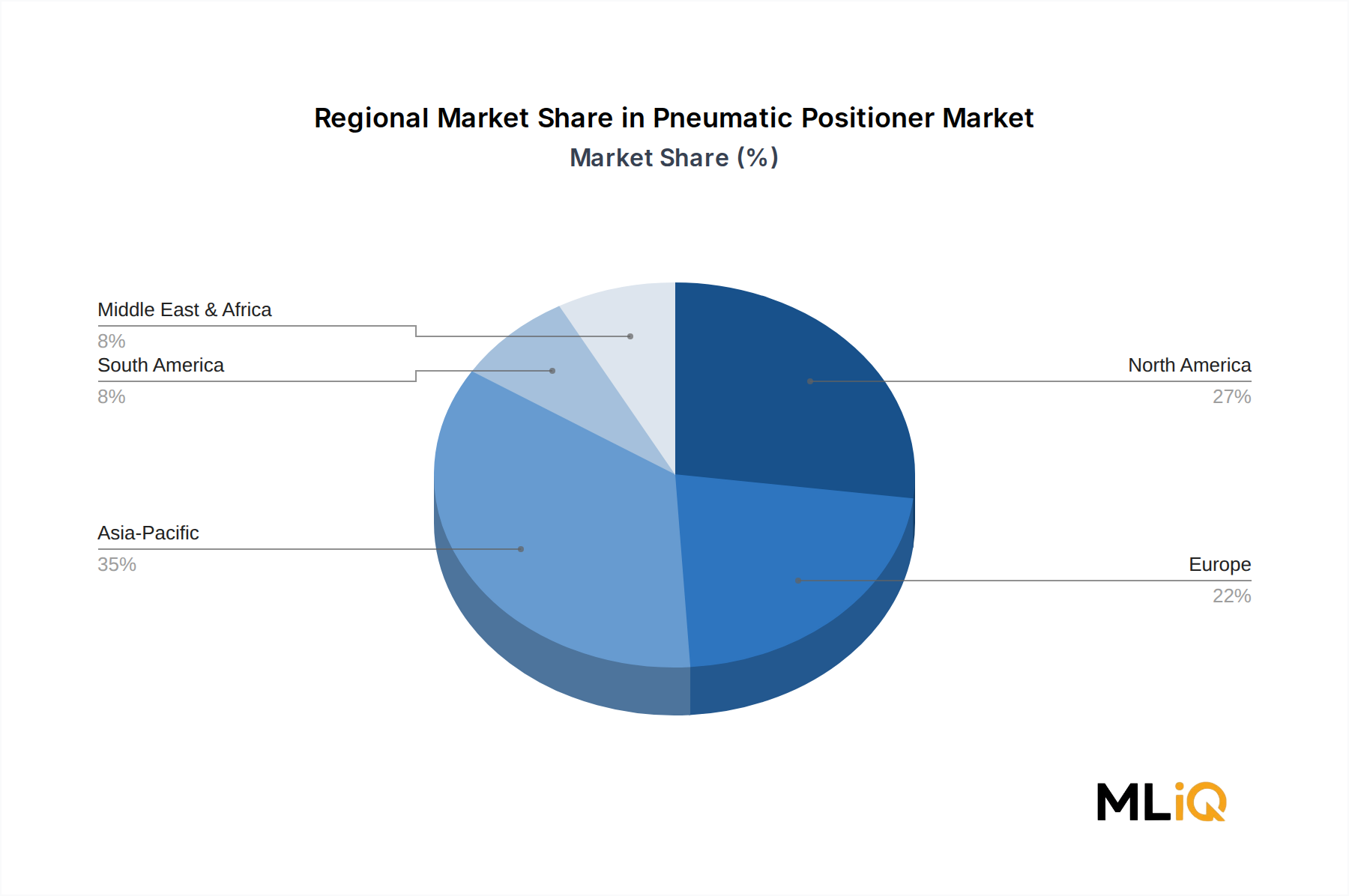

The Pneumatic Positioner Market exhibits meaningful regional variation in growth rates, revenue concentration, and demand drivers, reflecting differences in industrialization stage, energy investment cycles, and regulatory environments.

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of 6.2% from 2024 to 2033, supported by large-scale chemical complex expansions in China's Yangtze River Delta, India's Petroleum, Chemicals and Petrochemicals Investment Region (PCPIR) clusters, and ASEAN refinery capacity additions. China alone accounts for over 28% of Asia Pacific positioner demand, driven by state-owned enterprise capital programs in refining, fertilizer production, and natural gas distribution. India represents the highest incremental growth opportunity, with its chemical manufacturing sector targeting $300 billion in output by 2030.

North America is the largest mature market, generating an estimated $620 million in revenue in 2024, with a projected CAGR of 4.2% through 2033. Growth is driven by natural gas infrastructure expansion — particularly LNG export terminal development on the U.S. Gulf Coast — combined with chemical plant modernization under the CHIPS and Science Act's industrial policy framework. The United States accounts for approximately 80% of North American demand, with Canada contributing through oil sands and pipeline instrumentation projects.

Europe holds a significant revenue share, estimated at $480 million in 2024, growing at approximately 3.8% CAGR. Demand is underpinned by stringent process safety regulations under the Seveso III Directive and the EU's REACH chemical regulation, which mandate frequent positioner calibration and documentation. Germany, the United Kingdom, and France are the primary demand centers, with activity concentrated in specialty chemicals, pharmaceuticals, and power generation.

The Middle East and Africa region is growing at 5.4% CAGR, driven by GCC refinery and petrochemical megaprojects. Saudi Arabia's NEOM industrial zones and the UAE's downstream chemical investment program represent the most significant near-term procurement pipelines.

Latin America, led by Brazil and Argentina, is growing at 4.0% CAGR, with offshore pre-salt field development in Brazil and mining sector expansion providing the primary demand base.

The Pneumatic Positioner Market is characterized by concentrated manufacturing in a limited number of high-precision industrial economies, with trade flows radiating toward capital-intensive project markets in the Middle East, Asia, and Latin America.

Germany and Japan are the leading net exporters of high-specification pneumatic positioners, benefiting from deep precision engineering ecosystems and established brands such as Siemens, ABB (European manufacturing), and Azbil. Germany's positioner export value is estimated at over $180 million annually, with primary destinations including the GCC, India, and Southeast Asia. Japan exports approximately $120 million in positioner value per year, led by Azbil and Yokogawa-affiliated instrumentation channels.

The United States is both a significant producer and importer, with domestic manufacturing by Emerson Electric and Honeywell serving North American project markets, while importing lower-cost variants from China and Taiwan for commercial and light industrial applications. Section 301 tariffs on Chinese instrumentation components — currently ranging from 7.5% to 25% depending on Harmonized Tariff Schedule (HTS) classification — have added meaningful landed-cost pressure on U.S. buyers sourcing Chinese-manufactured pneumatic assemblies since 2019.

China is a major producer of commodity-grade pneumatic positioners, primarily serving domestic demand in its chemical and heavy manufacturing sectors. Chinese exports of positioners face tariff barriers in the European Union under anti-dumping surveillance frameworks and encounter qualification hurdles in oil and gas markets where ATEX,

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.8% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Pneumatic Positioner Market market expansion.

Key companies in the market include Rotork, Siemens, ABB, Honeywell, Emerson Electric, General Electric, Azbil, Baker Hughes, Schneider Electric, Flowserve.

The market segments include Type, Industry Verticals.

The market size is estimated to be USD 1.99 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Pneumatic Positioner Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Pneumatic Positioner Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.