1. What are the major growth drivers for the Industrial Brakes Market market?

Factors such as are projected to boost the Industrial Brakes Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

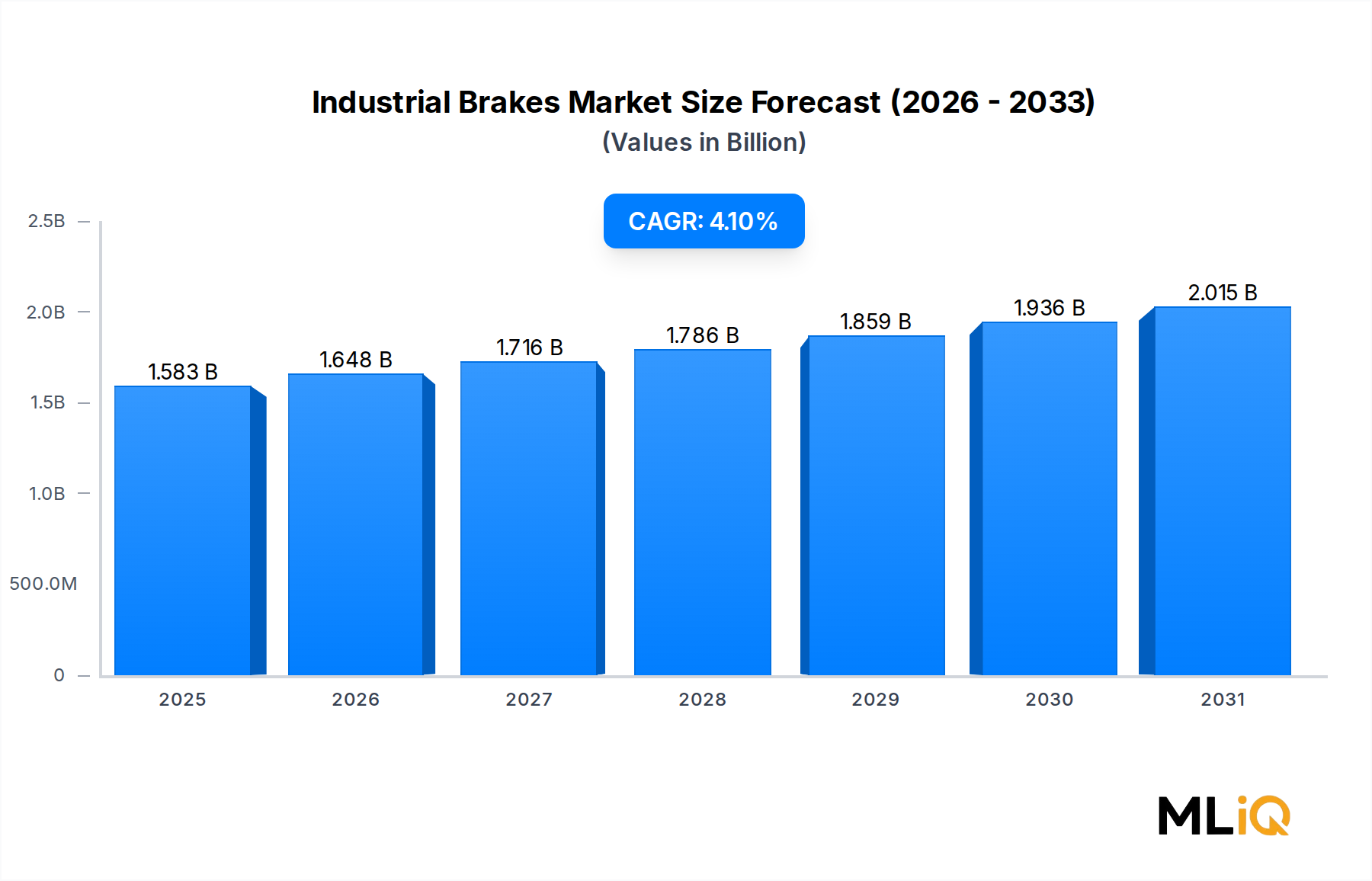

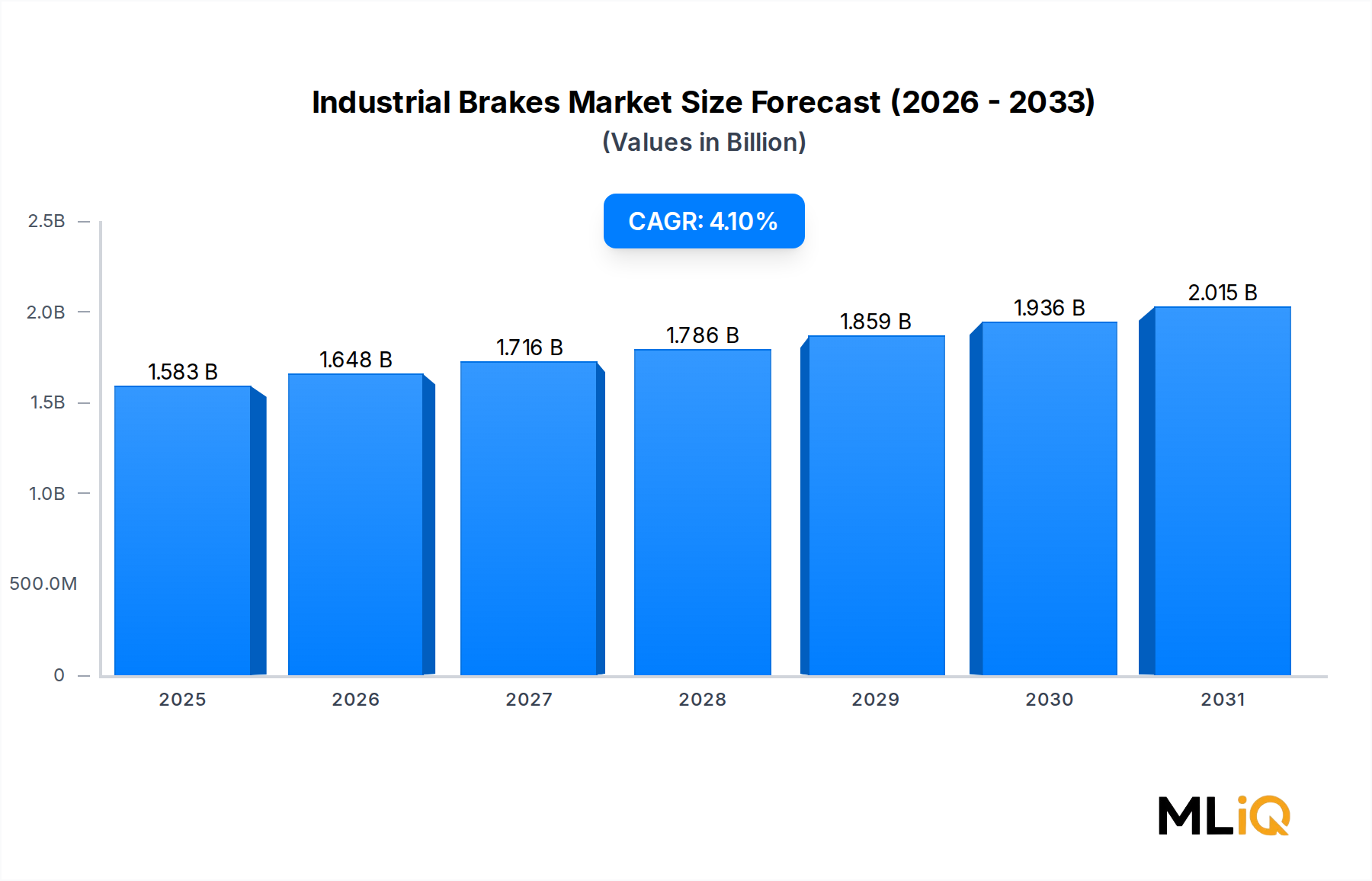

The global Industrial Brakes Market is valued at $1,583.40 million in the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 4.1% through 2033, reflecting steady, broad-based demand across capital-intensive industries. This growth trajectory is underpinned by rising mechanization in mining and construction, the accelerating adoption of automated manufacturing systems, and tightening workplace safety regulations that mandate reliable braking solutions across heavy machinery platforms.

Industrial brakes are critical safety and performance components embedded across a wide spectrum of equipment — from overhead cranes and hoisting systems to conveyors, wind turbines, and marine winches. The proliferation of automated production lines, particularly in Asia Pacific and Europe, is generating consistent replacement and retrofit demand. As industrial operators upgrade aging mechanical infrastructure, the market is benefiting from both greenfield installations and brownfield modernization cycles.

Macroeconomic tailwinds include sustained infrastructure investment programs in emerging economies, particularly across Southeast Asia, the Middle East, and parts of Africa, where governments are channeling capital into port development, mining operations, and heavy manufacturing. In mature markets such as North America and Western Europe, stringent occupational safety standards continue to drive demand for high-performance braking systems with advanced monitoring and fail-safe capabilities.

From a technology standpoint, the transition toward electrification and smart factory architectures is reshaping product development priorities. Electrically actuated brakes with embedded sensors are gaining traction as industrial operators seek real-time diagnostics and predictive maintenance capabilities. This shift is particularly relevant in wind energy, where pitch and yaw braking systems must deliver exceptional precision and durability.

Looking ahead to 2033, the market is expected to surpass $2,200 million, driven by continued end-user diversification beyond traditional manufacturing and mining sectors into offshore energy, automated warehousing, and robotics-integrated production environments. The competitive landscape is intensifying, with global conglomerates and specialized OEM suppliers both investing in product innovation and geographic expansion. Companies that can offer integrated braking solutions — combining mechanical, hydraulic, and electronic elements — are positioned to capture disproportionate share in this evolving market.

Within the Industrial Brakes Market, the hydraulic segment represents the single largest revenue-generating product category by type, commanding a dominant share driven by its widespread application across high-torque, heavy-duty industrial environments. Hydraulic brakes offer superior clamping force relative to their footprint, making them the preferred solution in demanding sectors such as metal and mining, offshore drilling, and large-scale material handling. Their ability to generate consistent braking force under variable load conditions — without the degradation in performance seen in purely mechanical alternatives — has cemented their position as the workhorse braking technology across critical infrastructure.

The Hydraulic Brakes Market encompasses a range of caliper, drum, and disc configurations adapted to specific torque and environmental requirements. In crane and hoist applications, hydraulic disc brakes are preferred for their modulation capability and suitability for frequent start-stop cycles. In rolling mill and metal processing environments, hydraulic brakes must withstand extreme thermal loads and contamination, driving demand for sealed, high-durability designs. The intersection of hydraulic braking technology with digital control systems — including proportional hydraulic valves and closed-loop feedback — is further extending the segment's relevance in automation-intensive environments.

Mechanical brakes, while yielding some ground to hydraulic and electrical alternatives in precision applications, retain a strong installed base due to their simplicity, low maintenance requirements, and cost-effectiveness in lower-torque environments. The mechanical segment is particularly resilient in cost-sensitive emerging markets where total cost of ownership considerations favor straightforward, field-serviceable designs.

From a competitive standpoint, leading players in the hydraulic segment include Dellner Bubenzer, a specialist known for its heavy-duty caliper and disc brake systems deployed extensively in offshore, steel, and port applications. SIBRE and Coremo Ocmea S.p.A. also hold significant positions within hydraulic product lines, offering custom-engineered solutions for specialized industrial environments. Eaton leverages its broad power management portfolio to bundle hydraulic braking solutions within integrated drivetrain and motion control offerings, providing a competitive advantage in large system-level procurement decisions.

The hydraulic segment's share is not merely holding steady — it is consolidating, as the operational complexity of modern industrial machinery increasingly demands the force density and controllability that hydraulic systems provide. Key growth vectors for the segment through 2033 include expansion in renewable energy infrastructure (particularly offshore wind, where pitch braking systems require high hydraulic force in compact, corrosion-resistant packages), increasing crane and hoist deployments at automated container terminals, and retrofitting of legacy mining equipment with modern hydraulic braking assemblies to meet updated safety standards.

The Pneumatic Brakes Market, while smaller by revenue, plays a complementary role in the broader industrial brakes ecosystem, particularly in conveyor systems, packaging machinery, and applications where compressed air infrastructure is already in place. Pneumatic solutions offer rapid response times and intrinsic simplicity, making them valued in environments with explosion risks where electrical actuation is constrained. However, pneumatic brakes face competitive pressure from both hydraulic and electronic alternatives as precision and controllability requirements intensify.

All segments are being influenced by the broader rise of condition monitoring and IIoT integration, which is blurring boundaries between product categories as manufacturers embed sensors and data communication capabilities across mechanical, hydraulic, and pneumatic platforms alike.

Several high-impact drivers are sustaining the 4.1% CAGR projected for the Industrial Brakes Market through 2033, while a distinct set of structural constraints tempers the pace of expansion in specific geographies and segments.

On the demand side, the global mining sector remains one of the most significant volume drivers. Ore extraction volumes in key producing nations — particularly Chile, Australia, South Africa, and Indonesia — continue to rise, requiring ongoing investment in hoisting, conveyor, and grinding equipment, all of which rely on industrial brake systems for both operational control and safety compliance. Mining equipment modernization programs, accelerated by the push toward deeper, higher-productivity mines, are generating parallel demand for upgraded braking systems capable of handling higher torques and dynamic loads.

Construction activity in Asia Pacific, particularly in China, India, and the ASEAN bloc, is generating sustained demand for construction machinery equipped with reliable braking systems. China's infrastructure stimulus spending and India's National Infrastructure Pipeline — targeting over $1.4 trillion in project investment — are tangible macro drivers translating into crane, excavator, and heavy vehicle deployments, each requiring certified braking components.

Safety regulation is a compounding driver. Updated ISO and EN standards for crane and hoist braking systems, alongside evolving OSHA-aligned requirements in North America and similar frameworks in the EU, are forcing operators to replace or upgrade legacy braking systems on a defined compliance timeline. This regulatory compulsion creates non-cyclical demand that is largely insulated from short-term economic downturns.

On the constraint side, raw material cost volatility — particularly in steel, cast iron, and specialty friction composites — compresses margins for brake manufacturers and can delay purchasing decisions among cost-sensitive end users. Extended lead times for precision-machined brake components in tight supply environments add further friction to the procurement cycle. Additionally, the relatively long replacement cycle of industrial brakes in stable operating environments means that organic volume growth depends heavily on new equipment installation rates rather than aftermarket replacement velocity.

The Industrial Brakes Market features a mix of diversified industrial conglomerates and specialized OEM brake manufacturers, competing on the basis of product performance, geographic reach, application expertise, and after-sales service networks.

Antec Group: A specialist in industrial braking systems with a focus on customized solutions for heavy-duty applications in mining, cranes, and offshore environments; the company emphasizes engineering agility and close customer collaboration.

SIBRE: A leading global manufacturer of industrial brakes with an extensive portfolio spanning hydraulic caliper, drum, and disc brakes; SIBRE is particularly well positioned in steel, mining, and port crane applications with a strong European manufacturing base.

Comer Industries Spa (Walterscheid Powertrain Group): Operating within the broader Walterscheid Powertrain Group, Comer Industries brings integrated drivetrain and braking expertise to agricultural, construction, and industrial markets, leveraging group-level scale for competitive procurement.

Eaton: A global power management leader offering industrial braking solutions as part of its broader motion and control portfolio; Eaton's market advantage lies in its system integration capability and deep presence across multiple end-user verticals including manufacturing, oil and gas, and utilities.

AKEBONO BRAKE INDUSTRY CO., LTD.: A globally recognized brake technology company with strong roots in precision friction engineering; AKEBONO applies its friction materials expertise to industrial segments, differentiating on pad and lining performance under extreme thermal and mechanical stress.

Dellner Bubenzer: A prominent specialist in heavy industrial braking, particularly for offshore, port, steel, and mining applications; known for its engineered-to-order approach and global service infrastructure supporting safety-critical installations.

ringspann gmbh: A German-based manufacturer specializing in clamping, backstop, and braking technology for industrial machinery; ringspann competes on precision engineering and product longevity in automation and material handling applications.

Coremo Ocmea S.p.A.: An Italian OEM specializing in hydraulic and pneumatic caliper brakes for cranes, winches, and industrial hoists; the company is recognized for its modular product architecture and strong presence in European industrial markets.

Altra Motion: A diversified motion control and power transmission company with a broad brake portfolio spanning electromagnetic, hydraulic, and mechanical types; Altra's competitive strength lies in its multi-brand platform and cross-selling capability across industrial end markets.

carlisle brake & friction: A global supplier of friction-based braking and motion control solutions serving off-highway, mining, and industrial markets; the company competes on materials science depth and OEM supply relationships.

Q1 2024: Dellner Bubenzer announced the expansion of its manufacturing and service footprint in the Asia Pacific region, targeting growing demand from the Australian mining sector and Southeast Asian port development projects, reinforcing its position in heavy-duty offshore and crane braking systems.

Q2 2024: Altra Motion completed the integration of newly acquired friction and braking product lines into its unified go-to-market structure, enabling cross-portfolio bundling across electromagnetic and hydraulic brake categories and strengthening its value proposition for OEM customers in North America and Europe.

Q3 2024: AKEBONO BRAKE INDUSTRY CO., LTD. published results from a multi-year R&D initiative focused on next-generation friction materials for industrial applications, demonstrating improved thermal stability and reduced wear rates under cyclic loading conditions relevant to crane and hoist environments.

Q4 2024: Eaton expanded its industrial braking product certification portfolio to comply with updated EN 13001 crane design standard revisions, enabling market access across a broader segment of European OEM crane manufacturers subject to the revised regulatory framework.

Q1 2025: SIBRE launched a new generation of hydraulic disc brakes optimized for offshore wind turbine yaw and pitch control systems, addressing the growing intersection of renewable energy infrastructure demand and precision industrial braking requirements.

Q2 2025: ringspann gmbh introduced an enhanced modular backstop and braking system series for conveyor and material handling applications, emphasizing reduced installation time and improved predictive maintenance compatibility through integrated sensor options.

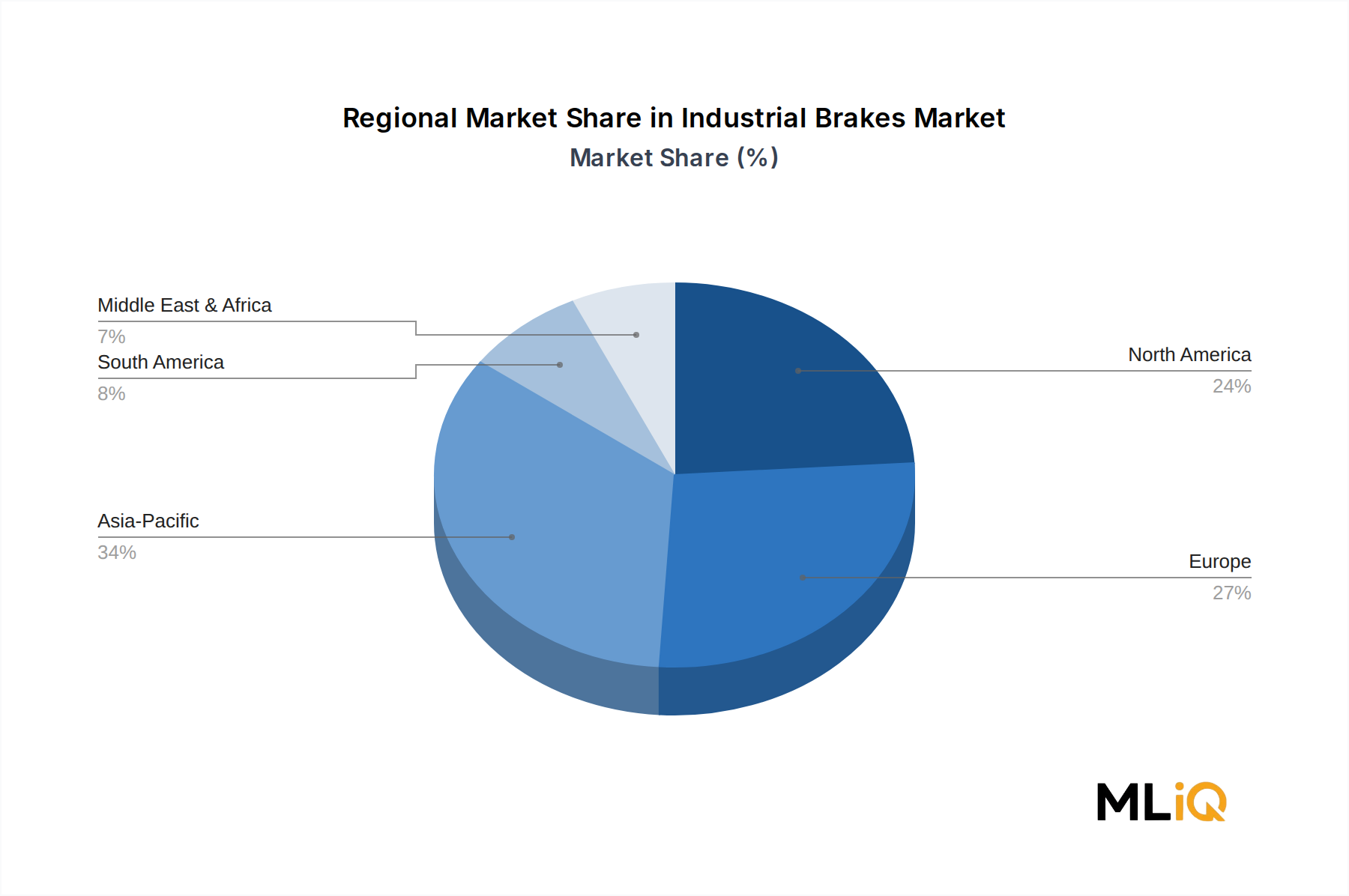

The Industrial Brakes Market exhibits meaningful regional variation in growth rates, demand composition, and end-user mix, with Asia Pacific emerging as the dominant growth engine while North America and Europe maintain premium positioning anchored by safety regulation and advanced manufacturing demand.

Asia Pacific accounts for the largest absolute revenue share of the global Industrial Brakes Market, driven by China's massive installed base of manufacturing, mining, and construction machinery. China alone represents a substantial proportion of regional demand, supported by state-directed infrastructure investment and continued expansion of the steel and cement sectors. India is the fastest-growing national market within the region, with infrastructure development under programs such as the National Infrastructure Pipeline generating sustained crane, conveyor, and heavy equipment deployments. The broader ASEAN bloc — particularly Indonesia, Vietnam, and Thailand — is contributing incremental demand as industrial base expansion accelerates. The Asia Pacific region is projected to grow at a CAGR modestly above the global average of 4.1%, driven by volume-led expansion rather than premium product adoption.

North America is a mature market characterized by high average selling prices, strong regulatory compliance demand, and a well-developed aftermarket services ecosystem. The United States represents the bulk of regional revenue, with demand anchored by mining, oil and gas, and automated manufacturing applications. Canada contributes meaningfully through its mining sector, while Mexico is an emerging assembly and light manufacturing hub generating incremental brake demand. North America's CAGR is estimated at approximately 3.5–3.8%, with value growth supported by safety regulation-driven replacements and technology upgrades.

Europe represents a sophisticated market where stringent EN and ISO standards drive consistent product upgrade cycles. Germany, the United Kingdom, France, and the Nordics are the primary revenue contributors, reflecting their concentration of crane manufacturing, steel processing, and offshore energy activity. European OEMs are at the forefront of integrating condition monitoring and IIoT capabilities into braking systems, commanding price premiums. Regional CAGR is estimated at approximately 3.6–4.0%.

Middle East & Africa is an emerging high-potential region, with infrastructure investment in GCC nations and mining expansion across South Africa and North Africa generating durable demand. Port and logistics infrastructure development across the GCC is particularly relevant for heavy-duty crane braking applications. South America — led by Brazil and Argentina — is mining-dependent, with regional growth correlated closely to commodity cycle investment patterns.

The Industrial Brakes Market operates within a complex, multi-layered regulatory environment that spans international standards bodies, national safety agencies, and sector-specific certification frameworks. Compliance with these frameworks is not optional — it is a prerequisite for product commercialization across major end-user segments, making regulatory alignment a structural demand driver rather than a mere compliance cost.

The International Organization for Standardization (ISO) and the European Committee for Standardization (CEN) are the two most influential standards-setting bodies governing industrial braking systems globally. ISO 4301 (crane classification), ISO 7752 (hydraulic control system components), and EN 13001 (crane design and safety) collectively establish the performance, testing, and documentation requirements that brake manufacturers must satisfy to supply into crane and hoist applications across most regulated markets. The 2023 revision of EN 13001 introduced updated fatigue and load spectrum requirements that effectively obsolete certain legacy brake designs, compelling both OEMs and end operators to upgrade installed systems.

In North America, OSHA 1910.179 governs overhead and gantry crane operations, with specific provisions for brake system performance and inspection intervals. The Mine Safety and Health Administration (MSHA) enforces brake requirements for mining machinery, including hoisting and conveyor systems. These frameworks create a recurring compliance-driven replacement market that is largely insulated from economic cycles.

Across the Asia Pacific region, regulatory harmonization is progressing unevenly. China's GB standards for crane and lifting equipment are being progressively aligned with ISO frameworks, expanding the addressable market for internationally certified brake products. India's Bureau of Indian Standards (BIS) has updated equipment safety standards as part of broader manufacturing regulatory modernization, creating both compliance costs and market opportunities for certified suppliers.

The energy transition is introducing new regulatory vectors. Wind turbine safety standards — including IEC 61400 — specify braking system requirements for pitch and yaw control, embedding industrial brake manufacturers into the renewable energy regulatory compliance ecosystem. As offshore wind deployment scales globally, this intersection of energy policy and industrial safety regulation is expected to generate incremental product certification activity through 2033.

Pricing dynamics in the Industrial Brakes Market reflect the interplay between raw material input costs, competitive intensity at the OEM supply level, and the value premium commanded by safety-certified, application-engineered products in regulated end markets.

At the product level, industrial brakes

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.1% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Industrial Brakes Market market expansion.

Key companies in the market include Antec Group, SIBRE, Comer Industries Spa (Walterscheid Powertrain Group), Eaton, AKEBONO BRAKE INDUSTRY CO., LTD., Dellner Bubenzer, ringspann gmbh, Coremo Ocmea S.p.A., Altra Motion, carlisle brake & friction.

The market segments include Type, Application, End User Industry.

The market size is estimated to be USD 1583.40 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3456, USD 5769, and USD 10995 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Industrial Brakes Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Industrial Brakes Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.