1. What are the major growth drivers for the Hollow Concrete block Market market?

Factors such as are projected to boost the Hollow Concrete block Market market expansion.

+1 2315155523

Hollow Concrete block Market

Hollow Concrete block Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

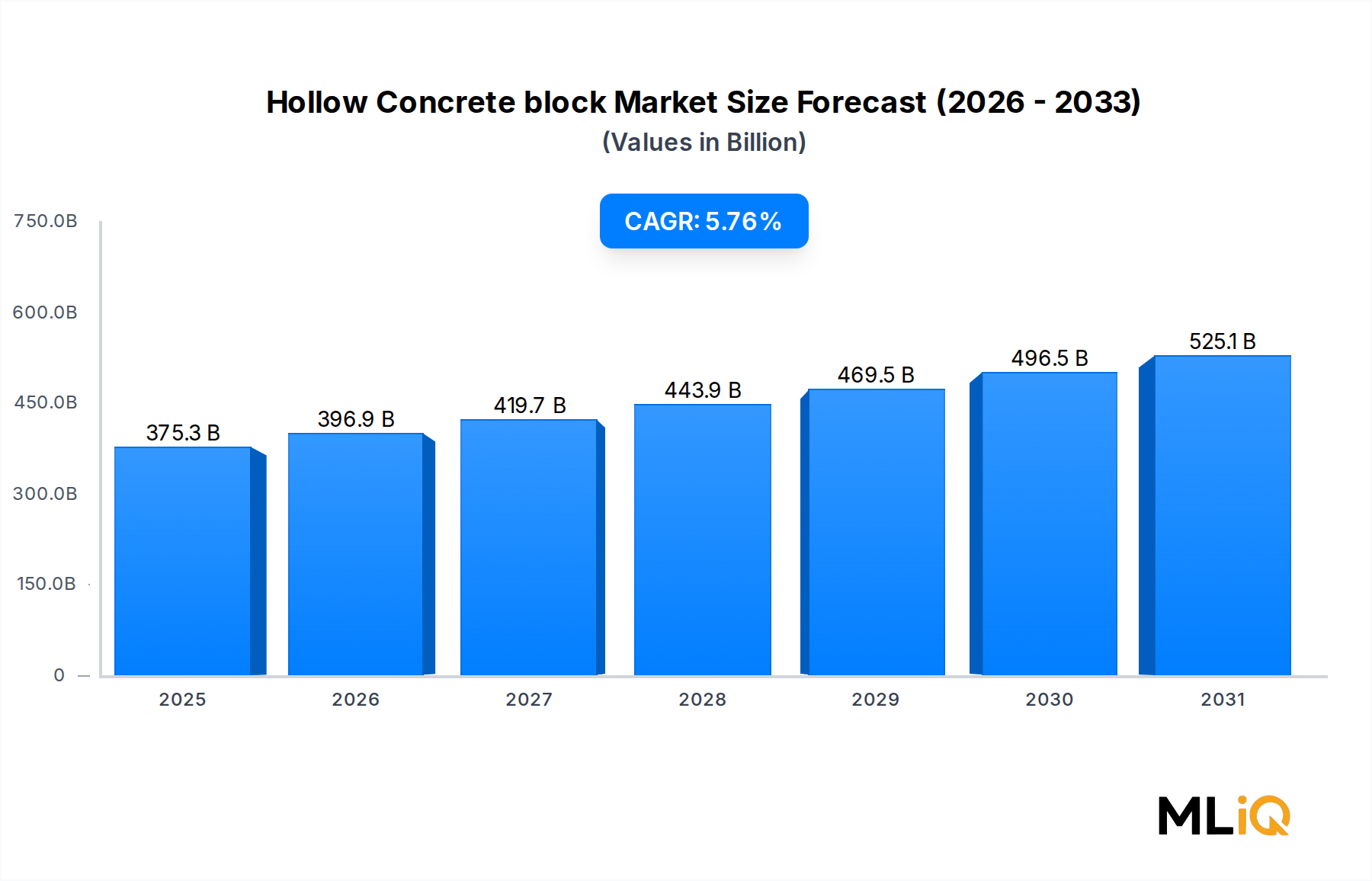

The global hollow concrete block market was valued at $375.26 billion in 2024 and is forecast to expand at a compound annual growth rate (CAGR) of 5.76% through the period 2025–2033. This trajectory reflects robust, sustained demand driven by urbanization, infrastructure investment cycles, and the material's intrinsic cost-performance advantages relative to competing walling systems.

Hollow concrete blocks occupy a structurally critical role in the modern construction supply chain. Their internal void geometry reduces dead-load weight by up to 25–40% compared with solid masonry alternatives, simultaneously lowering material consumption and improving thermal resistance—an attribute increasingly prized as energy codes tighten across North America, Europe, and the Asia Pacific. The global push toward resilient, low-carbon built environments has reinforced the product's relevance, as manufacturers advance blended-cement and supplementary cementitious material (SCM) formulations that reduce embodied carbon without sacrificing compressive strength ratings that typically range from 5 MPa to 20 MPa depending on application class.

Macro tailwinds supporting the market include an estimated 2.5 billion people globally expected to migrate to urban centers by 2050, according to United Nations projections. This urbanization wave compresses timelines for affordable housing delivery, logistics parks, and civic infrastructure—all end-uses where hollow concrete blocks dominate due to fast lay rates, dimensional consistency, and compatibility with standard mortar and reinforcement schedules. Government stimulus programs, particularly the Infrastructure Investment and Jobs Act in the United States and the European Union's cohesion fund disbursements, are injecting capital into public construction at a pace that directly benefits masonry product suppliers.

On the supply side, vertical integration among large cement conglomerates has enhanced margin stability, while regional players have focused on product differentiation through textured finishes, enhanced fire ratings (ASTM E119 compliance), and acoustic performance. The two principal product-type segments—smooth-faced and split-faced blocks—address distinct aesthetic and structural specifications, allowing manufacturers to serve both utilitarian industrial and premium commercial projects from a single production platform.

Looking forward through 2033, the market is positioned to absorb demand from emerging economies in Southeast Asia, Sub-Saharan Africa, and South Asia, where conventional masonry remains the default structural system for sub-five-story construction. Pricing pressure from alternative walling technologies such as light-gauge steel framing and engineered timber panels will temper volume growth in premium segments, yet the cost differential ensures that hollow concrete blocks remain the value-dominant solution across the broadest addressable market.

Among the four principal application segments—residential, commercial, industrial, and others—the residential sector commands the largest revenue share within the hollow concrete block market, accounting for an estimated 48–52% of total demand by value in 2024. This dominance is structural rather than cyclical: residential buildings represent the single largest category of new floor-area additions globally, and hollow concrete blocks are the preferred walling material for load-bearing and partition systems in markets where masonry construction is culturally and economically entrenched.

The drivers of residential dominance are multi-layered. First, affordable housing shortfalls across emerging markets create a persistent, policy-backed demand stream. India's Pradhan Mantri Awas Yojana (PMAY) program targets the delivery of tens of millions of housing units, a significant proportion of which rely on concrete masonry construction. Similarly, social housing programs in Brazil, Mexico, and across Sub-Saharan Africa mandate cost-effective, locally sourced materials, with hollow concrete blocks satisfying both criteria. In these geographies, blocks are frequently produced by semi-industrial regional manufacturers who supply within a 100–200 km radius, minimizing logistics costs and supporting local employment.

Second, the structural engineering economics of residential construction favor hollow concrete blocks at building heights of one to five stories, a range that accounts for the overwhelming majority of residential new-builds globally. The blocks' ability to accept vertical rebar through the hollow cores, when grouted and reinforced, achieves seismic and wind-load compliance without the need for supplementary structural frames—a dual-function economy that significantly reduces per-square-meter structural cost relative to frame-plus-infill systems.

Third, the Residential Construction Market is experiencing a documented shift toward energy-efficient envelope design. Hollow blocks with expanded polystyrene (EPS) inserts, integrally cast insulation, or double-wythe cavity wall configurations now meet or exceed energy code requirements in ASHRAE 90.1 climate zones, expanding the product's competitive footprint in North American and European residential applications where it previously lost share to wood-frame or insulated concrete form alternatives.

Key players active within the residential segment include Magicrete Building Solutions Pvt. Ltd, which has built a strong franchise in India's rapidly urbanizing tier-2 and tier-3 city markets. UltraTech Cement Ltd leverages its upstream cement capacity to maintain competitive block pricing at scale. CEMEX SAB de CV operates an integrated building products business that supplies residential developers across Latin America and the United States with a full masonry system encompassing blocks, mortar, and grout products.

The residential segment's share is gradually consolidating as larger manufacturers displace informal producers through superior dimensional tolerances, product certifications, and just-in-time delivery capabilities. However, the informal sector retains meaningful volume in markets with limited regulatory enforcement, tempering the pace at which market share concentrates among industrial-scale participants. Over the 2025–2033 forecast horizon, residential demand growth is expected to track closely with national housing completion rates, with the fastest absolute volume gains occurring in India, China's lower-tier cities, and Francophone Africa.

The hollow concrete block market is shaped by a set of quantifiable drivers and measurable constraints that collectively determine the pace and distribution of growth across the forecast period.

Primary Driver — Urbanization and Infrastructure Spending: Global urban population is growing at approximately 1.8% per year, adding roughly 70 million new urban residents annually. Each percentage-point increase in urbanization rate historically correlates with a 2.1–2.4% increase in masonry unit demand in developing economies, based on cross-sectional analyses of construction intensity indices. Government capital expenditure on roads, bridges, and civic buildings—collectively exceeding $4 trillion annually globally—anchors demand for commercial and industrial hollow block applications.

Secondary Driver — Product Cost Competitiveness: Hollow concrete blocks deliver structural walling at a cost of approximately $8–$18 per square meter of wall face area (inclusive of mortar and labor) in most emerging-market geographies, compared with $25–$45 per square meter for light-gauge steel framing or $30–$60 per square meter for engineered timber panels. This cost gap sustains demand inertia across price-sensitive markets.

Tertiary Driver — Sustainability Regulatory Push: Tightening building energy codes in the European Union (Energy Performance of Buildings Directive revision), the United States (IBC energy provisions), and China (GB50189 standard) are incentivizing insulated masonry wall systems, expanding the premium-product segment and supporting average selling price improvement of 3–5% annually.

Primary Constraint — Raw Material Price Volatility: Cement and aggregate account for 65–75% of hollow block manufacturing cost. Portland cement prices have exhibited year-on-year volatility of ±12–18% in key markets between 2021 and 2024, compressing manufacturer margins when price pass-through is contractually limited. This volatility is detailed further in the supply chain section of this report.

Secondary Constraint — Alternative Material Competition: Growth of the Autoclaved Aerated Concrete Market is directly competitive with hollow concrete blocks in the residential and commercial segments, offering lighter weight and superior thermal performance, though at a 20–35% cost premium. In Europe and parts of Southeast Asia, this substitution pressure is measurable, with AAC capturing an estimated 8–12 percentage points of walling market share over the past decade.

The competitive landscape of the hollow concrete block market is characterized by a blend of multinational conglomerates with vertically integrated upstream positions and regional specialists with deep local distribution networks. The following profiles outline the strategic posture of the ten key participants identified in this report:

Magicrete Building Solutions Pvt. Ltd: An India-based manufacturer with a growing product portfolio spanning AAC blocks, hollow blocks, and ready-mix plaster; the company has aggressively expanded its distributor network across western and southern India to capture residential construction demand in tier-2 cities.

MIDLAND BRICK: An Australian masonry specialist recognized for premium clay and concrete masonry products; the company serves the residential and commercial construction segments in the Asia Pacific region with a focus on aesthetic differentiation and technical support services.

Xella Group: A European leader in masonry and insulation products operating across more than 30 countries; Xella's Ytong and Silka brands compete directly with hollow concrete blocks in the European residential market, and the company invests significantly in digitalized production to reduce unit energy consumption.

Acme Brick Company: A Fort Worth-based manufacturer and wholly owned subsidiary of Berkshire Hathaway; Acme operates one of the largest brick and concrete masonry distribution networks in the United States, serving residential builders, commercial contractors, and landscaping specifiers.

Brampton Brick: A Canadian producer of concrete and clay masonry products serving the North American residential and commercial markets; the company differentiates through a broad color and texture range and strong relationships with regional architectural specification communities.

Taylor Concrete Products Inc.: A regional North American manufacturer focused on concrete masonry units for commercial and industrial applications; Taylor competes on delivery reliability and product consistency for large-scale developer accounts.

UltraTech Cement Ltd: India's largest cement producer with an integrated building products division encompassing ready-mix concrete and concrete blocks; the company leverages raw material captivity and a pan-India distribution infrastructure to sustain price competitiveness at national scale.

CRH plc: A global building materials leader headquartered in Dublin with operations across North America and Europe; CRH's Americas Materials and Europe Materials divisions both carry concrete masonry unit product lines, and the company pursues strategic bolt-on acquisitions to consolidate regional positions.

Tristar Brick and Block Ltd: A UK-based masonry manufacturer serving the residential and commercial building sectors; Tristar focuses on high-specification concrete masonry products meeting stringent UK Building Regulations compliance criteria.

CEMEX SAB de CV: A Mexican multinational with a diversified building materials portfolio spanning cement, ready-mix, and aggregates; CEMEX's vertically integrated model enables full masonry system supply and positions the company as a preferred partner for large residential development programs across Latin America and the United States.

January 2023: CRH plc announced a strategic review of its European distribution businesses, signaling a portfolio reorientation toward higher-margin manufactured products including concrete masonry units, with capital redeployment earmarked for North American market consolidation.

March 2023: UltraTech Cement Ltd commissioned a new automated hollow block production line at its Rajasthan facility, adding an estimated 50,000 units per day of additional capacity to serve PMAY-linked affordable housing demand across northern India.

June 2023: The European Committee for Standardization (CEN) published updated harmonized standards for concrete masonry units under EN 771-3, tightening dimensional tolerance and thermal performance declaration requirements, effectively raising the technical bar for market participation across EU member states.

September 2023: CEMEX SAB de CV entered a strategic supply agreement with a major U.S.-based residential developer for the provision of hollow concrete block systems across a multi-state affordable housing program encompassing an estimated 12,000 housing units.

February 2024: Xella Group announced a €150 million investment program to upgrade production facilities across Central and Eastern Europe, including enhanced automation for concrete masonry unit lines aimed at reducing per-unit CO₂ emissions by 20% by 2026.

May 2024: India's Bureau of Indian Standards (BIS) revised IS 2185 specifications for hollow and solid concrete blocks, incorporating new durability and water absorption criteria aligned with international practice, impacting procurement specifications for government-funded construction projects nationwide.

November 2024: Magicrete Building Solutions Pvt. Ltd secured Series B funding to accelerate geographic expansion into eastern Indian states, targeting the underserved masonry market in West Bengal and Odisha.

The hollow concrete block market exhibits pronounced regional heterogeneity in growth rates, demand drivers, and competitive structure.

Asia Pacific — Fastest-Growing Region: Asia Pacific represents the highest-velocity demand environment, accounting for an estimated 38–42% of global market value in 2024 and projected to grow at a regional CAGR of approximately 7.2–7.8% through 2033. China and India are the dual engines of this expansion. China's ongoing urbanization—despite a moderated pace relative to the 2010–2020 decade—continues to generate substantial concrete masonry demand for infrastructure and secondary city residential construction. India's construction intensity is accelerating, with the government's national infrastructure pipeline (NIP) allocating over ₹111 trillion (approximately $1.3 trillion) to infrastructure over five years. Southeast Asian markets including Indonesia, Vietnam, and the Philippines are emerging secondary growth poles.

North America — Mature but Stable: North America holds the second-largest revenue share, estimated at 22–26% of global value in 2024, growing at a regional CAGR of approximately 3.8–4.2%. The United States market is driven by commercial construction, institutional buildings, and the ongoing rebuild of aging infrastructure. Canada's residential market supports sustained demand in urban centers including Toronto and Vancouver. The Commercial Building Construction Market in North America is a critical demand anchor for premium split-faced and ground-faced concrete masonry unit specifications.

Europe — Regulatory-Driven Transition: Europe accounts for approximately 18–22% of global hollow concrete block market value, with a regional CAGR of 3.2–3.6%. Growth is constrained by competition from AAC, prefabricated panel systems, and timber-frame construction, but regulatory mandates for energy-efficient building envelopes are sustaining demand for insulated masonry wall systems. Germany, France, and the UK are the largest national markets.

Middle East & Africa — High-Potential Emerging Segment: The Middle East and Africa region, while currently representing 10–14% of global value, is projected to grow at a regional CAGR of 6.0–6.5%, driven by Gulf Cooperation Council (GCC) megaproject construction activity, and Sub-Saharan Africa's demographic-led housing demand. Saudi Arabia's NEOM and Vision 2030 program represent a concentrated demand stimulus.

South America — Moderate Growth with Brazil as Anchor: South America contributes approximately 6–9% of global market value, growing at 4.5–5.0% regionally, with Brazil accounting for over 60% of regional demand, underpinned by the Minha Casa Minha Vida affordable housing program's renewed funding cycle.

Investment activity in the hollow concrete block market over the 2022–2024 period has been characterized by strategic consolidation among large building materials conglomerates and targeted venture and growth-equity funding directed at technology-forward manufacturers.

CRH plc completed the acquisition of multiple regional concrete products businesses across North America during 2022–2023, deploying approximately $2.1 billion in bolt-on M&A consistent with its strategy to build density in high-growth metropolitan markets. This acquisition program included concrete masonry unit producers in the southeastern and southwestern United States, where residential construction volume is growing above the national average.

Within the Building Materials Market broadly, private equity interest has focused on manufacturers deploying automated production technology capable of reducing labor cost per unit by 30–45% relative to conventional block plants. Investments in robotic cubing, automated quality inspection using machine vision, and kiln optimization systems have attracted growth-equity commitments from

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.76% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Hollow Concrete block Market market expansion.

Key companies in the market include Magicrete Building Solutions Pvt. Ltd, MIDLAND BRICK, Xella Group, Acme Brick Company, Brampton Brick, Taylor Concrete Products Inc., UltraTech Cement Ltd, CRH plc, Tristar Brick and Block Ltd, CEMEX SAB de CV.

The market segments include Product Type, Application.

The market size is estimated to be USD 375.26 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Hollow Concrete block Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Hollow Concrete block Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.