1. What are the major growth drivers for the Wheat Protein Isolates Market market?

Factors such as are projected to boost the Wheat Protein Isolates Market market expansion.

+1 2315155523

Wheat Protein Isolates Market

Wheat Protein Isolates Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

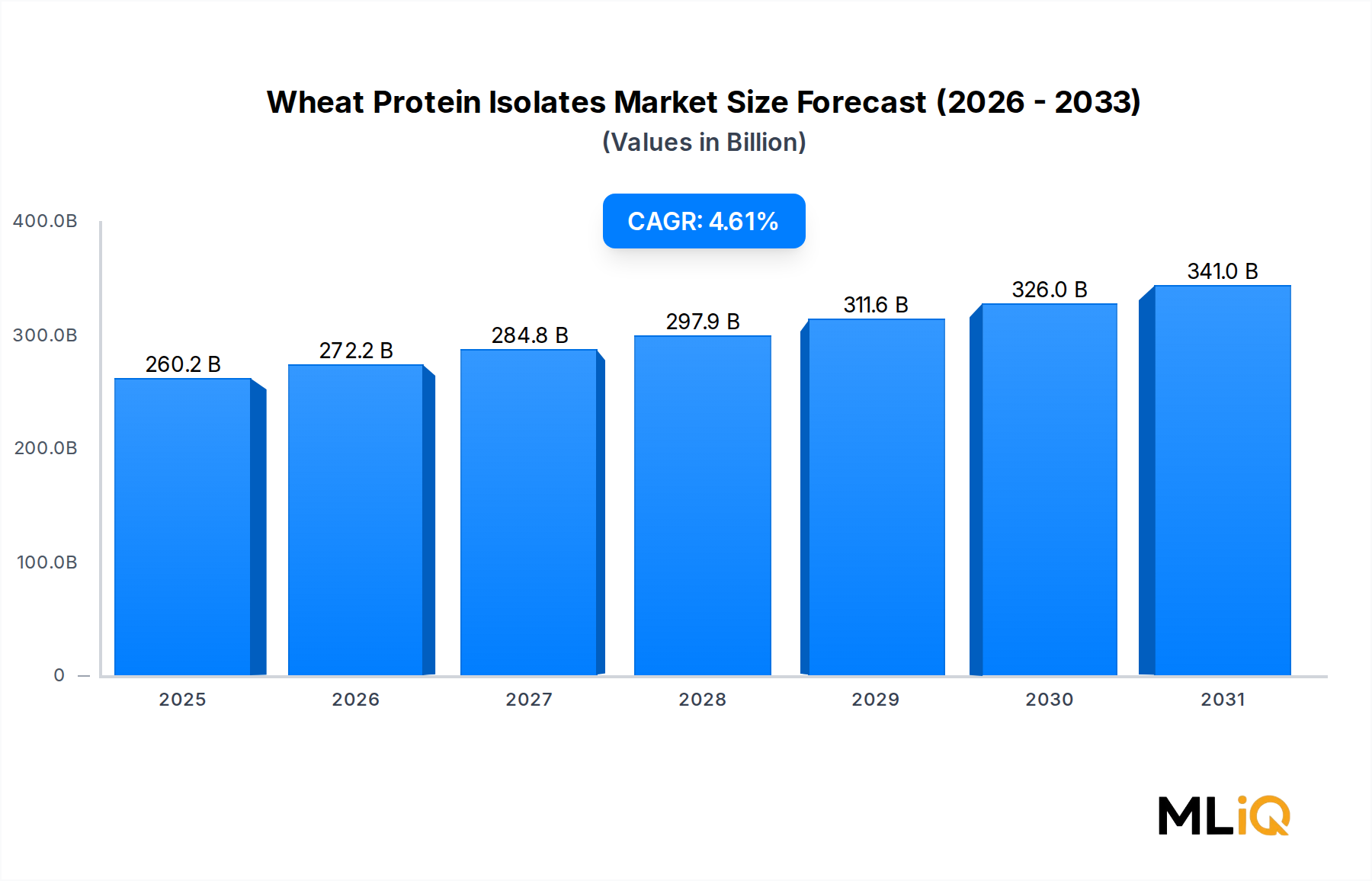

The global Wheat Protein Isolates Market was valued at $260.24 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 4.61% through the forecast period of 2025–2033. This sustained growth trajectory reflects a confluence of structural demand signals across food manufacturing, nutraceuticals, and animal nutrition segments, underpinned by the broader global shift toward high-protein, plant-derived ingredient systems.

Wheat protein isolates—characterized by protein concentrations of 75%, 85%, and 90% and above—serve as functionally versatile ingredients in applications ranging from starch-based foods and processed meat analogues to minced seafood products and aquaculture feed binders. Their unique viscoelastic properties, cost competitiveness relative to animal-derived proteins, and scalability of production from existing wheat milling infrastructure position them as preferred choices among large-scale food manufacturers.

Key demand drivers include the global rise in vegetarian and flexitarian dietary patterns, accelerating penetration of high-protein bakery and snack categories in North America and Europe, and growing utilization in processed seafood and meat applications across Asia Pacific. Rising consumer awareness around satiety, muscle recovery, and functional nutrition is catalyzing uptake across both retail and food service channels.

Macro tailwinds reinforcing market expansion include favorable agricultural policies in the European Union supporting wheat-derived ingredient production, investment in precision fermentation and extraction technologies that improve protein purity yields, and increasing regulatory acceptance of wheat protein concentrates and isolates in infant nutrition and clinical food formulations across several emerging economies.

From a regional standpoint, Europe and North America collectively account for the majority of current revenue, driven by mature food processing ecosystems and established regulatory frameworks. However, Asia Pacific is emerging as the fastest-growing regional market, propelled by urbanization, rising disposable incomes, and accelerating industrialization of food processing in China and India.

Competitive intensity remains high, with globally integrated ingredient players such as Cargill, Archer Daniels Midland, and Roquette maintaining multi-geography production footprints. Simultaneously, specialized European producers including CRESPEL & DEITERS GMBH AND CO. KG and Kroener Staerke are reinforcing positions through application-specific product portfolios.

Looking forward, the market's growth will be increasingly shaped by the pace of innovation in extraction efficiency, sustainability credentials of wheat protein supply chains, and the competitive dynamics of the broader Plant-Based Protein Market, which continues to attract significant venture and corporate R&D capital globally.

Among the product concentration tiers within the Wheat Protein Isolates Market, the 85% protein grade represents the dominant revenue-generating segment, capturing the largest share of global demand across both developed and emerging market applications. This dominance is attributable to an optimal balance between functional performance, cost efficiency, and technical compatibility with the widest array of food formulation requirements.

The 85% protein isolate grade delivers superior water absorption, dough rheology improvement, and texturizing capability compared to lower-grade concentrates, while remaining more cost-accessible than ultra-high purity 90% protein fractions that require additional processing steps, energy expenditure, and yield trade-offs. For large-volume customers in the processed meat, bakery, and seafood binding segments, the 85% grade represents the sweet spot of cost-per-functional-unit optimization.

In the processed meat products sub-segment—one of the most significant end-use categories—85% wheat protein isolates are deployed extensively as fat replacers, moisture retention agents, and texture modifiers in sausages, emulsified meat products, and hybrid meat-plant formulations. This application alone accounts for a substantial portion of global demand, as manufacturers seek to extend meat content while maintaining consumer-acceptable mouthfeel and slice integrity.

Within the starch-based food category, 85% isolates are used to enhance protein fortification of noodles, pasta, and flatbreads, particularly in markets such as China, India, and Japan, where wheat-based staple foods constitute a high-frequency consumption category. Regional manufacturers in these markets are increasingly adopting wheat protein isolates as a cost-effective means of meeting nutritional labeling and protein content claims without reformulating base ingredient matrices.

Key players actively serving the 85% protein segment include MGP Ingredients, which has established a strong commercial presence in North American high-purity wheat protein supply, and Roquette, whose integrated wheat processing platform in France supports large-volume supply of this grade to European food manufacturers. Manildra Group in Australia also serves as a major regional supplier to Asia Pacific accounts, leveraging its vertically integrated wheat milling and protein extraction operations.

The share of the 85% protein segment within the overall Wheat Protein Isolates Market is showing modest consolidation rather than aggressive expansion, as some premium food brands and sports nutrition manufacturers migrate toward the 90% and above tier to differentiate on protein density per serving. Nevertheless, the volume economics strongly favor continued dominance of the 85% grade through 2033, particularly in price-sensitive, high-volume industrial food manufacturing contexts.

The competitive structure within this segment is moderately concentrated, with the top five global suppliers accounting for a significant majority of production capacity. Capacity expansion announcements from Crop Energies AG and AB Amilina signal that supply growth in the 85% tier will be managed carefully to avoid price erosion, supporting margin stability for established producers over the medium term.

The Wheat Protein Isolates Market is propelled by a set of quantifiable demand and supply-side forces, each carrying distinct implications for growth velocity and competitive positioning.

Rising plant-based protein demand: Global retail sales of plant-based food products grew at double-digit rates through the early 2020s, and while growth has moderated, the category continues to expand at approximately 6–8% annually in core Western markets. Wheat protein isolates, as a key texturizing and binding agent in plant-based meat analogues, are direct beneficiaries of this structural dietary shift.

Processed meat reformulation: Increasing regulatory and consumer pressure to reduce saturated fat content in processed meats has prompted reformulation activity across the European Union and North America. Wheat protein isolates serve as functional fat replacers in emulsified meat systems, with some formulations substituting up to 20–25% of fat content without compromising textural attributes.

Aquaculture and feed binder expansion: Global aquaculture output surpassed 90 million metric tons in 2023, creating sustained demand for high-binding, digestible protein sources in pelletized feeds. Wheat protein isolates, particularly in the 75–85% concentration range, are gaining traction as partial substitutes for fish meal in finfish and shrimp feed, with trials demonstrating inclusion rates of 5–15% without adverse growth performance impacts.

Key constraints include raw material price volatility: Global wheat prices experienced extreme fluctuations between 2021 and 2023, driven by geopolitical disruption and climate-related harvest variability, compressing margins for wheat protein isolate producers whose feedstock costs are directly linked to soft wheat commodity pricing.

Allergen regulatory barriers: Wheat is classified as a major food allergen in the United States, European Union, and several other jurisdictions, necessitating mandatory labeling. This limits market penetration in allergen-free and pediatric nutrition segments, constraining addressable market scope by an estimated 10–15% of premium food categories.

The competitive landscape of the Wheat Protein Isolates Market is characterized by a mix of large integrated agro-processing conglomerates and specialized regional ingredient manufacturers. The following profiles outline the strategic positioning of key participants:

CRESPEL & DEITERS GMBH AND CO. KG: A Germany-based specialty wheat protein manufacturer with deep expertise in vital wheat gluten and high-purity isolate production. The company holds strong relationships with European bakery and meat processing customers, and its proprietary wet fractionation technology supports consistent protein quality across seasonal wheat crop variations.

MGP INGREDIENTS: A leading U.S.-based producer of wheat protein isolates with a vertically integrated model encompassing grain procurement, wet milling, and ingredient packaging. MGP has strategically expanded its specialty protein portfolio targeting sports nutrition, plant-based meat, and premium baking segments.

AGRIDIENT: A U.S. distribution and processing company specializing in plant-derived proteins including wheat-based fractions. Agridient serves as a key intermediary linking large-scale wheat protein producers with North American food manufacturers requiring custom specification products.

AB AMILINA: A Lithuanian starch and protein processor with growing export capabilities across the European Union. AB Amilina has invested in expanding its wheat protein isolate capacity to serve Eastern and Central European food manufacturers, capitalizing on regional wheat surplus conditions.

ROQUETTE: A globally integrated plant-based ingredient leader headquartered in France. Roquette's wheat protein portfolio benefits from its large-scale wet milling infrastructure and significant R&D investment in texture innovation, targeting applications in meat analogues, dairy alternatives, and clinical nutrition.

ARCHER DANEILS MIDLAND: One of the world's largest agricultural processors, with a diversified wheat protein portfolio spanning concentrates to high-purity isolates. The company leverages its global origination network and customer co-development capabilities to maintain leading positions across major end-use verticals.

CROP ENERGIES AG: A European bioethanol and co-product specialist that produces wheat protein isolates as a value-added byproduct of fermentation operations. The company's cost structure benefits from integrated processing efficiencies, supporting competitive pricing in bulk protein markets.

CARGILL INC.: A global agribusiness and food ingredient major with wheat protein capabilities embedded within its broader starch and sweetener operations. Cargill's commercial reach across Asia Pacific, North America, and Europe enables broad customer coverage and supply chain redundancy.

KROENER STAERKE: A German starch and protein producer with established capabilities in vital wheat gluten and wheat protein isolate manufacturing. Kroener Staerke serves European food manufacturers with consistent, food-grade protein inputs, maintaining quality certifications aligned with EU food safety directives.

MANILDRA GROUP: Australia's largest wheat processor and a major supplier of wheat protein isolates to the Asia Pacific region. Manildra's vertically integrated operations from grain receivals to finished ingredient dispatch provide supply security for regional customers in Japan, South Korea, and ASEAN markets.

January 2024: MGP Ingredients announced a capacity expansion initiative at its Atchison, Kansas facility, targeting increased production of high-purity wheat protein isolates to serve growing demand from plant-based food manufacturers in North America.

March 2024: Roquette completed the commissioning of an upgraded protein fractionation line at its Lestrem, France production campus, enabling higher throughput of 85% and 90% wheat protein isolate grades with improved protein purity consistency.

June 2024: The European Food Safety Authority (EFSA) published updated guidance on the use of wheat-derived protein concentrates in infant and follow-on formulae, creating a more clearly defined regulatory pathway for manufacturers seeking to expand into pediatric nutrition applications.

September 2024: Cargill Inc. entered a long-term supply agreement with a major European plant-based meat producer for the provision of textured wheat protein ingredients, representing one of the largest volume commitments in the segment recorded that year.

November 2024: AB Amilina announced an investment of approximately €15 million in its Panevezys, Lithuania facility to expand wheat starch and co-product protein extraction capacity, with phased commissioning targeted for completion by Q3 2025.

February 2025: Manildra Group secured a new export contract for wheat protein isolate supply to a South Korean aquaculture feed manufacturer, reflecting growing regional adoption of wheat protein in fish meal substitution applications.

The global revenue distribution across regions within the Wheat Protein Isolates Market reflects a well-established bifurcation between mature, high-consumption Western markets and dynamic, rapidly industrializing Asia Pacific economies.

Europe: Europe represents the largest single regional market, accounting for an estimated 35–38% of global revenue in 2024. Germany, France, the United Kingdom, and the Benelux countries are primary consumption centers, driven by robust food processing industries and long-standing incorporation of vital wheat gluten and protein isolates in bakery, meat, and confectionery manufacturing. The region's stringent food quality standards and sustainability mandates are accelerating premiumization toward higher-purity protein grades. Regional CAGR is estimated at approximately 3.8–4.2% through 2033.

North America: North America holds the second-largest revenue share, approximately 28–30% of the global total in 2024. The United States is the dominant national market, propelled by high consumer awareness of plant-based nutrition and the widespread adoption of wheat protein isolates in sports nutrition and processed food reformulation. Canada and Mexico represent smaller but growing consumption bases. Regional CAGR is estimated at 4.0–4.5%.

Asia Pacific: Asia Pacific is unequivocally the fastest-growing region, with an estimated CAGR of 5.8–6.2% through the forecast horizon. China and India are the primary growth engines, driven by urbanization, expanding middle-class dietary aspirations, and industrialization of food processing. Japan and South Korea maintain sophisticated demand for premium protein isolate grades in functional food and aquaculture applications. The region is expected to substantially close its revenue share gap with Europe by 2033.

South America: South America, led by Brazil and Argentina, represents an emerging but volume-significant market, with demand anchored in processed meat and feed binder applications. Regional CAGR is estimated at 4.1%, supported by growth in integrated protein production driven by expanding agricultural processing sectors.

Middle East & Africa: This region accounts for the smallest revenue share currently but is demonstrating above-average growth potential, particularly in Turkey, the GCC countries, and South Africa, where food processing investment and protein fortification mandates are rising. Regional CAGR is projected at approximately 4.5–5.0%.

Technological transformation is reshaping production economics, protein quality benchmarks, and application boundaries within the Wheat Protein Isolates Market, with three core innovation domains attracting the most concentrated R&D investment.

Advanced wet fractionation and membrane filtration: Next-generation ultrafiltration and nanofiltration membrane technologies are enabling producers to achieve higher protein purity thresholds—consistently above 90%—at lower energy inputs compared to conventional centrifugation-based separation. Companies including Roquette and CRESPEL & DEITERS GMBH AND CO. KG have integrated membrane separation modules into existing wet milling lines, reducing water and energy consumption per kilogram of protein isolate produced by an estimated 15–20%. Adoption timelines for full-scale commercial deployment of these systems are concentrated in the 2025–2028 window, with early movers expected to achieve meaningful cost advantages.

Enzymatic hydrolysis for bioactive peptide production: Controlled enzymatic processing of wheat protein isolates to produce bioactive peptide fractions—targeting antihypertensive, antioxidant, and immunomodulatory functional claims—represents a high-value product extension strategy. R&D investment in this area is accelerating among specialty ingredient firms, with several patent filings recorded in 2023 and 2024 relating to optimized hydrolysis protocols. This technology pathway directly reinforces competitive differentiation within the broader Food Protein Ingredients Market and Functional Food Ingredients Market, where value-added protein derivatives command significant price premiums.

Precision fermentation integration: Although nascent, the integration of wheat protein isolates with precision fermentation-derived proteins to create hybrid ingredient matrices is being explored by several ingredient innovators. This approach aims to combine the functional texturizing properties of wheat gluten fractions with the nutritional completeness and allergen-mitigation potential of fermentation-derived proteins. Commercial timelines extend toward 2028–2030, and

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.61% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Wheat Protein Isolates Market market expansion.

Key companies in the market include CRESPEL & DEITERS GMBH AND CO. KG, MGP INGREDIENTS, AGRIDIENT, AB AMILINA, ROQUETTE, ARCHER DANEILS MIDLAND, CROP ENERGIES AG, CARGILL INC., KROENER STAERKE, MANILDRA GROUP.

The market segments include PRODUCT, END USER.

The market size is estimated to be USD 260.24 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Wheat Protein Isolates Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Wheat Protein Isolates Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.