1. What are the major growth drivers for the Thailand Fertilizers Market market?

Factors such as Easy Usage and Application Procedures Suitable for European Land are projected to boost the Thailand Fertilizers Market market expansion.

+1 2315155523

Thailand Fertilizers Market

Thailand Fertilizers Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

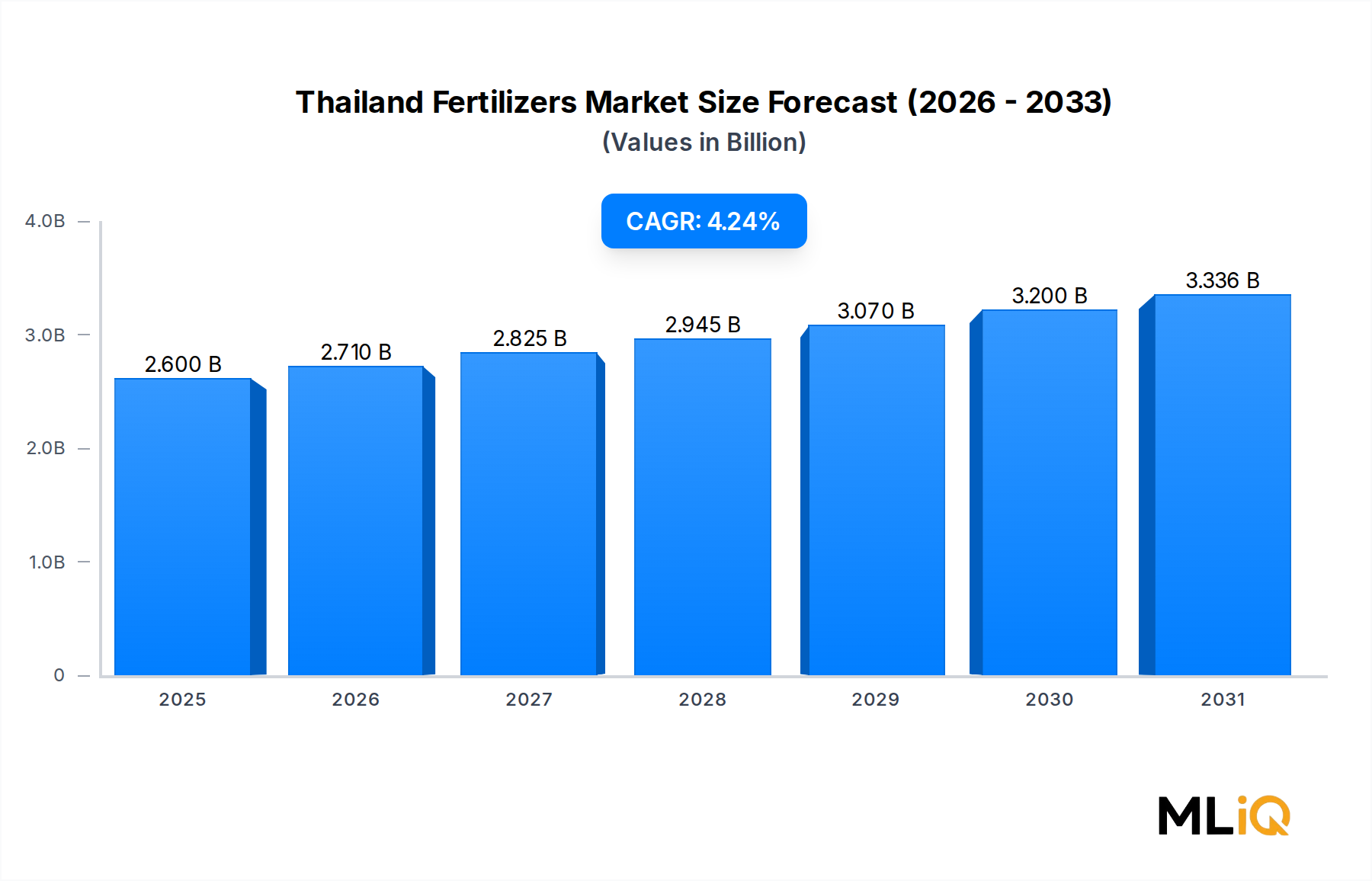

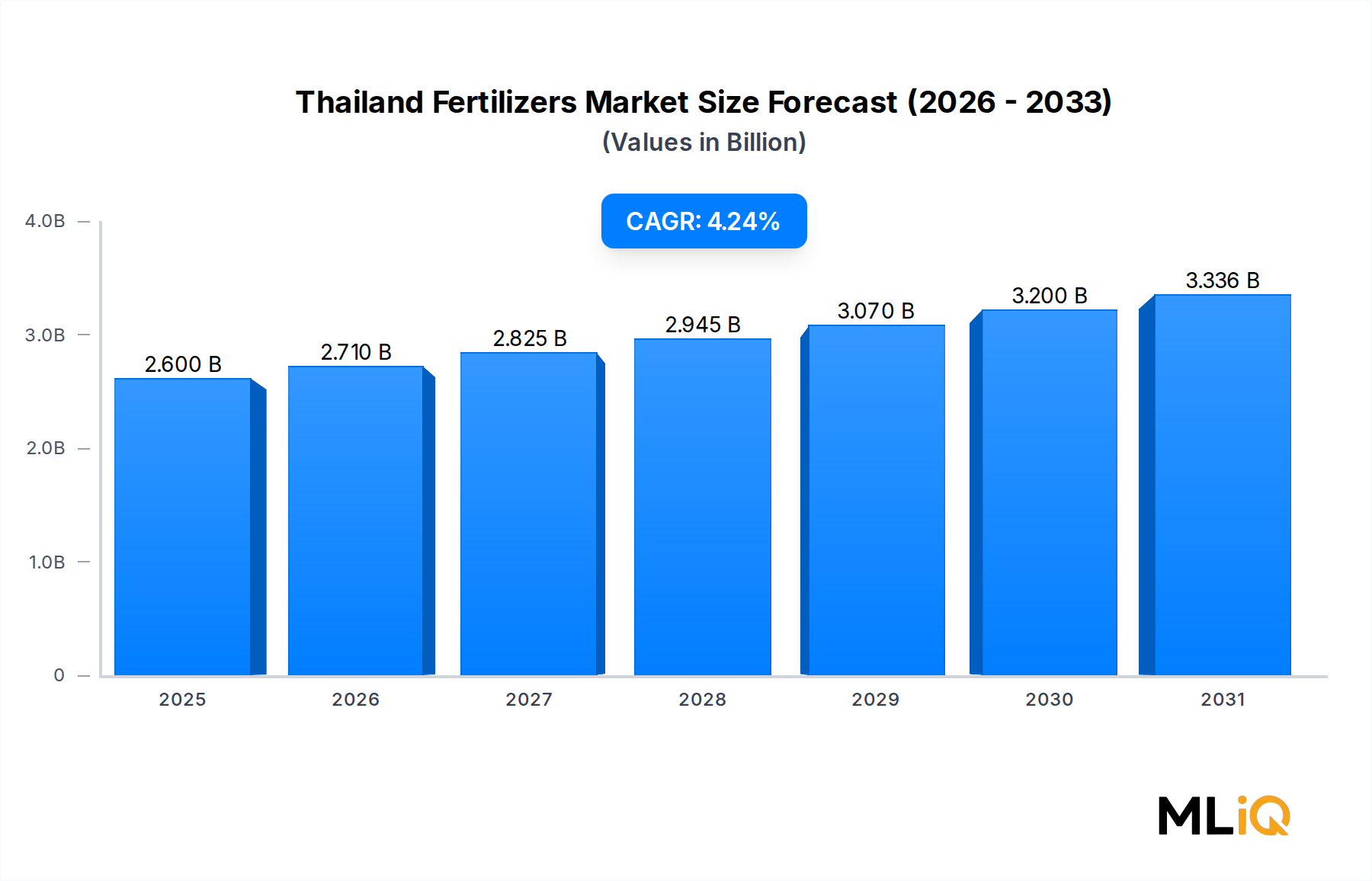

The Thailand Fertilizers Market is valued at $2.6 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 4.24% through the forecast period, reflecting sustained agricultural intensification across Thailand's diverse cropping systems. Thailand remains one of Southeast Asia's most significant agricultural economies, with fertilizers serving as a critical input across rice paddies, sugarcane plantations, rubber estates, fruit orchards, and vegetable farms. The market's forward trajectory is anchored by the government's strategic commitment to food security, export competitiveness in global commodity markets, and the broader modernization of smallholder farming practices.

Key demand drivers include rising pressure on arable land productivity, adoption of high-yield seed varieties that require optimized nutrient management, and increasing integration of soil-testing advisory services by both public agricultural extension bodies and private agrochemical distributors. Thailand's export-oriented agricultural sector—particularly in cassava, sugarcane, and fresh fruits—creates consistent commercial demand for balanced fertilizer programs. The country's rice sector alone accounts for millions of hectares under cultivation annually, establishing a structural baseline for nitrogen and phosphorus consumption.

Macro tailwinds reinforcing market growth include favorable government subsidy frameworks for smallholder farmers, expansion of modern irrigation infrastructure under the national water management plan, and growing foreign direct investment in contract farming arrangements that standardize input usage. Additionally, the shift toward specialty crop production—including durian, mango, and dragon fruit for export—is elevating demand for high-purity, slow-release, and foliar nutrient formulations.

From a forward-looking perspective, the market is expected to benefit from digitalization of supply chains, enabling more precise last-mile distribution in rural provinces. The emergence of fertigation systems in commercial horticulture and the gradual adoption of controlled-release fertilizer technologies are anticipated to add incremental value to average selling prices, thereby supporting revenue growth even amid volume stabilization pressures in traditional paddy segments. Regulatory scrutiny on synthetic inputs is a headwind that market participants are navigating through product reformulation and the development of bio-stimulant blended fertilizer lines. Overall, the Thailand Fertilizers Market presents a moderately growing, structurally resilient opportunity underpinned by both conventional staple-crop demand and the premiumization of specialty agricultural segments through 2030 and beyond.

Within the Thailand Fertilizers Market, the nitrogenous fertilizers segment commands the largest revenue share, driven by the foundational role of nitrogen in crop physiology and the enormous scale of nitrogen-intensive crops cultivated across Thai agricultural landscapes. Nitrogen is indispensable for vegetative growth, chlorophyll synthesis, and protein formation, making nitrogenous products the first-choice input for rice, maize, sugarcane, and cassava—all of which constitute core components of Thailand's agricultural output and export portfolio.

Urea remains the dominant nitrogenous fertilizer product by volume, owing to its high nitrogen content (46% N), relatively low cost per unit of nutrient, and versatile application compatibility across broadcast, side-dress, and fertigation methods. Ammonium sulfate and ammonium nitrate also hold meaningful market positions, particularly in acidic soil correction scenarios and in crops sensitive to sulfur nutrition. The Nitrogenous Fertilizers Market is thus a critical anchor segment that shapes procurement strategies across the entire fertilizer value chain in Thailand.

The segment's dominance is reinforced by the sheer scale of paddy rice cultivation, which spans approximately 10 million hectares across Thailand's central plains, northern highlands, and northeastern plateau regions. Rice requires multiple nitrogen applications across its growth cycle—at tillering, panicle initiation, and heading—creating a recurring, high-frequency demand pattern that sustains distributor throughput and manufacturer offtake volumes throughout the cropping calendar.

Key players operating within this segment include Yara (Thailand) Company Limited, which leverages its global nitrogen production and formulation expertise to supply premium urea and UAN (urea ammonium nitrate) solutions to commercial farms and cooperatives. Thai Central Chemical Public Company Limited (TCCC) maintains a dominant domestic position through its integrated blending and distribution infrastructure, offering a broad portfolio that covers urea-based NPK compounds calibrated to Thai soil profiles. NFC Public Company Limited operates as one of the country's largest domestic blenders, sourcing imported nitrogen raw materials and processing them into customized compound formulations for retail and institutional customers.

The nitrogenous sub-segment is also witnessing a gradual transition toward enhanced efficiency fertilizers (EEFs), including urease inhibitor-coated urea and polymer-coated slow-release nitrogen products. These innovations address regulatory pressure to reduce nitrogen volatilization and leaching losses, particularly in flood-irrigated paddy systems where conventional urea can lose up to 30–40% of applied nitrogen through ammonia volatilization and denitrification. While EEFs command a price premium, their adoption is accelerating among commercial growers and contract farming operators who can quantify productivity gains per baht of input expenditure.

The segment's revenue share is assessed as consolidating rather than rapidly expanding in volume terms, as fertilizer use efficiency improvements and precision nutrient management reduce per-hectare application rates in some commercial settings. However, the shift toward higher-value nitrogenous specialty formulations is sustaining per-unit revenue growth. Companies with proprietary inhibitor technologies or controlled-release coatings are strategically positioned to capture margin expansion even as commoditized urea faces pricing compression from global supply dynamics linked to natural gas feedstock costs and Chinese export policy fluctuations.

The Thailand Fertilizers Market is shaped by a defined set of quantifiable drivers and measurable constraints that jointly determine the pace and direction of growth across product segments and application categories.

One primary driver is the ease of application and compatibility of modern granular and liquid fertilizer formulations with Thai farming practices. Blended NPK granules, for instance, allow single-pass application covering multiple nutrient requirements, reducing labor costs in a market where agricultural wage inflation has averaged 3–5% annually in recent years. The streamlined logistics and application of these products are particularly relevant for smallholder farmers who operate with limited mechanization and rely on manual broadcasting or small tractor-mounted spreaders.

Agricultural productivity pressure constitutes a structural growth driver. Thailand's arable land per capita has been declining as urbanization expands, meaning that yield intensification through optimized fertilizer use is the primary lever for maintaining aggregate output. The Thai government's national agricultural development plan targets yield improvements of 15–20% in key staple and export crops over the medium term, directly increasing demand for balanced and specialty nutrient products.

The Phosphatic Fertilizers Market and Potash Fertilizers Market are also being driven by soil health campaigns that have revealed widespread macronutrient deficiencies in Thailand's intensively cropped soils, compelling agronomists and extension officers to recommend multi-nutrient programs beyond urea alone.

On the constraint side, environmental concerns regarding synthetic fertilizer use represent the most significant market headwind. Thailand's Department of Agriculture has tightened monitoring of nitrogen and phosphorus runoff into water systems, particularly in the Chao Phraya and Mekong river basins. Regulatory frameworks incentivizing organic fertilizer adoption and penalizing over-application are beginning to exert pressure on conventional synthetic fertilizer volumes. Additionally, global ammonia and phosphate rock price volatility—driven by geopolitical disruptions and energy market fluctuations—has introduced input cost unpredictability for domestic blenders, compressing margins and creating demand uncertainty among price-sensitive smallholders who delay purchases during price spikes.

The competitive landscape of the Thailand Fertilizers Market is characterized by a mix of global multinational corporations, regional agribusiness conglomerates, and domestic Thai manufacturers. The following profiles summarize the strategic positioning of key market participants:

Yara (Thailand) Company Limited: A subsidiary of Yara International, one of the world's largest nitrogen fertilizer producers, Yara Thailand focuses on premium crop nutrition solutions including YaraVita foliar products and YaraMila compound fertilizers, targeting commercial horticulture and export crop producers.

NFC Public Company Limited: One of Thailand's largest domestically listed fertilizer companies, NFC operates extensive blending facilities and a nationwide distribution network, supplying NPK compound fertilizers to rice, sugarcane, and cassava farmers across all major agricultural regions.

Chai Thai Co Ltd: A well-established Thai fertilizer trader and distributor, Chai Thai leverages deep relationships with regional agricultural cooperatives and provincial dealers to distribute imported and locally blended fertilizer products to smallholder farmer segments.

Thai Central Chemical Public Company Limited: Known as TCCC, this company holds a prominent position in the Thai market through its broad product portfolio spanning nitrogenous, phosphatic, and compound fertilizers, with strong brand recognition among both commercial and subsistence farmers.

Haifa Group: An Israeli specialty fertilizer multinational with regional presence in Southeast Asia, Haifa Group supplies water-soluble fertilizers, potassium nitrate, and controlled-release products primarily to the Thai horticulture, fruit, and greenhouse vegetable sectors.

SAKSIAM GROUP: A Thai agribusiness group engaged in fertilizer blending and distribution, SAKSIAM serves agricultural cooperatives and provincial markets with competitively priced compound fertilizer products tailored to regional soil and crop requirements.

ICL Fertilizers (Ranthai Agro Co Ltd): The Thai affiliate of ICL Group, a global specialty minerals and fertilizer company, Ranthai Agro distributes ICL's polysulfate and specialty potassium and phosphate products to premium and export-oriented crop growers in Thailand.

Rayong Fertilizer Trading Company Limited (UBE Group): Backed by Japan's UBE Industries, this company specializes in high-quality blended fertilizers and has established logistics infrastructure in eastern Thailand to serve industrial farming operations and commercial plantations.

COMPO Expert: A European specialty plant nutrition company, COMPO Expert markets controlled-release and stabilized fertilizer technologies in Thailand, targeting high-value crops where input efficiency justifies premium pricing.

ICP FERTILIZER COMPANY: A domestic Thai fertilizer manufacturer and distributor, ICP competes primarily on price and accessibility in the bulk commodity fertilizer segment, maintaining distribution reach in rural provinces where cost sensitivity is the primary purchasing criterion.

January 2024: The Thai Ministry of Agriculture and Cooperatives announced an expanded fertilizer subsidy program targeting 2.8 million smallholder rice farmers, allocating budgetary support for subsidized NPK compound fertilizers to mitigate the impact of global price volatility on farm-level input costs.

March 2024: Yara (Thailand) Company Limited launched a digital soil mapping initiative in partnership with a leading Thai agricultural university, covering over 50,000 hectares in the central plains region to enable precision nutrient recommendation services for commercial rice and corn growers.

June 2024: Thai Central Chemical Public Company Limited commissioned an upgraded granulation facility at its central Thailand plant, increasing domestic blending capacity by an estimated 15% to reduce dependence on imported finished fertilizer products.

September 2024: The Thai government's Department of Agriculture published revised guidelines on maximum application rates for synthetic nitrogen fertilizers in paddy cultivation zones adjacent to protected watershed areas, impacting formulation strategies for multiple market participants.

November 2024: Haifa Group expanded its regional distribution agreement with a major Thai agribusiness cooperative network, extending access to water-soluble fertilizer and fertigation product lines to an additional 12 provinces in northern and northeastern Thailand.

February 2025: COMPO Expert announced the introduction of its ENTEC stabilized nitrogen fertilizer line into the Thai market through a local distribution partnership, targeting commercial sugarcane and maize operations seeking to reduce nitrogen losses and comply with tightening environmental standards.

April 2025: NFC Public Company Limited reported strategic expansion of its logistics infrastructure, including new regional warehousing hubs in Chiang Mai and Khon Kaen provinces to reduce delivery lead times and seasonal stockout risks for cooperative and dealer customers.

The Thailand Fertilizers Market exhibits distinct regional demand patterns reflecting the diversity of crop systems, soil types, irrigation infrastructure, and commercial farming intensity across the country's major agricultural zones.

The Central Plains region is the most mature and highest-revenue market zone, accounting for an estimated 35–38% of total national fertilizer consumption. This area encompasses Thailand's iconic paddy rice belt, extensive sugarcane cultivation, and rapidly expanding commercial horticulture operations. Soil fertility management in the Central Plains is supported by well-developed extension services and dealer networks, and per-hectare fertilizer application rates are among the highest in the country. Regional CAGR is assessed at approximately 3.5–4.0%, reflecting a consolidating base demand with incremental growth from specialty and high-efficiency formulations.

The Northeastern region (Isan) represents the largest geographical agricultural zone and an increasingly important fertilizer consumption area, contributing approximately 28–30% of national volume. Cassava, rice, and sugarcane dominate the cropping landscape here. Historically characterized by lower input intensity due to smallholder scale and income constraints, the Northeast is now the fastest-growing regional segment, with an estimated CAGR of 4.8–5.2%, driven by contract farming expansion, cooperative consolidation, and government-backed input access programs.

The Northern region contributes approximately 18–20% of national demand, with a distinctive crop mix including corn, longan, lychee, and highland vegetables. The North is a significant growth pocket for micronutrient and specialty fertilizer products, with zinc, boron, and iron applications gaining traction among commercial fruit growers. Regional CAGR is estimated at 4.0–4.5%.

The Southern region, dominated by rubber and oil palm plantations alongside coastal aquaculture, accounts for approximately 12–15% of fertilizer demand. Fertilizer application patterns here are shaped by perennial crop nutrient cycles, with potassium and magnesium products holding particular importance for rubber latex quality and oil palm bunch production. Growth is steady at an estimated CAGR of 3.8–4.2%.

Across all regions, the Asia Pacific context remains critical, as Thailand's fertilizer import dependency—particularly for potash and phosphate raw materials—ties domestic pricing to regional trade dynamics involving China, Canada, Belarus, and Morocco as key supplier nations.

The Thailand Fertilizers Market is undergoing a technology-driven transformation that is reshaping product formulations, delivery mechanisms, and agronomic service models. Three disruptive technology vectors are particularly relevant to the medium-term competitive landscape.

The first is controlled-release and stabilized fertilizer technology. Polymer-coated urea and urease/nitrification inhibitor products are transitioning from niche premium products to mainstream adoption candidates as environmental regulations tighten and growers seek yield stability over multiple seasons. R&D investment in this category is concentrated among multinational players such as COMPO Expert and ICL Fertilizers, whose proprietary coating and inhibitor chemistries represent defensible intellectual property positions. Adoption timelines suggest meaningful commercial penetration in high-value horticultural and plantation segments by 2027, with broader commodity crop uptake contingent on price normalization.

The second technology vector is precision agriculture integration, which is directly relevant to the Precision Agriculture Market and is beginning to influence fertilizer recommendation and application practices in Thailand. Variable rate application (VRA) systems, drone-based nutrient sensing, and AI-driven soil-crop nutrient models are being piloted by commercial farm operators and agri-tech startups. The intersection of precision agriculture tools with fertilizer product selection is creating new service-bundling opportunities for manufacturers who can combine agronomic advisory with product supply. This convergence threatens purely transactional commodity fertilizer business models while reinforcing the value proposition of companies with technical agronomy capabilities.

The third technology area is biostimulant and bio-fertilizer integration. Microbial inoculants, humic acid formulations, and amino acid-based biostimulants are increasingly being co-formulated with conventional fertilizers to enhance nutrient use efficiency and root uptake. The Agricultural Inputs Market globally is witnessing R&D investment in this category exceed $500 million annually, and Thailand's regulatory framework is gradually creating pathways for registered bi

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.24% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as Easy Usage and Application Procedures Suitable for European Land are projected to boost the Thailand Fertilizers Market market expansion.

Key companies in the market include Yara (Thailand) Company Limited, NFC Public Company Limited, Chai Thai Co Ltd, Thai Central Chemical Public Company Limited, Haifa Group, SAKSIAM GROUP, ICL Fertilizers(Ranthai Agro Co Ltd), Rayong Fertilizer Trading Company Limited (UBE Group), COMPO Expert, ICP FERTILIZER COMPAN.

The market segments include Product, Other Nitrogenous Fertilizers, Other Phosphatic Fertilizers, Application.

The market size is estimated to be USD 2.6 billion as of 2022.

Easy Usage and Application Procedures Suitable for European Land.

Need for Increasing Agricultural Productivity.

Environmental Concerns Regarding Use of Synthetic Liquid Fertilizers.

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Thailand Fertilizers Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Thailand Fertilizers Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.