1. What are the major growth drivers for the Food Glazing Agents Market market?

Factors such as are projected to boost the Food Glazing Agents Market market expansion.

Food Glazing Agents Market

Food Glazing Agents Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

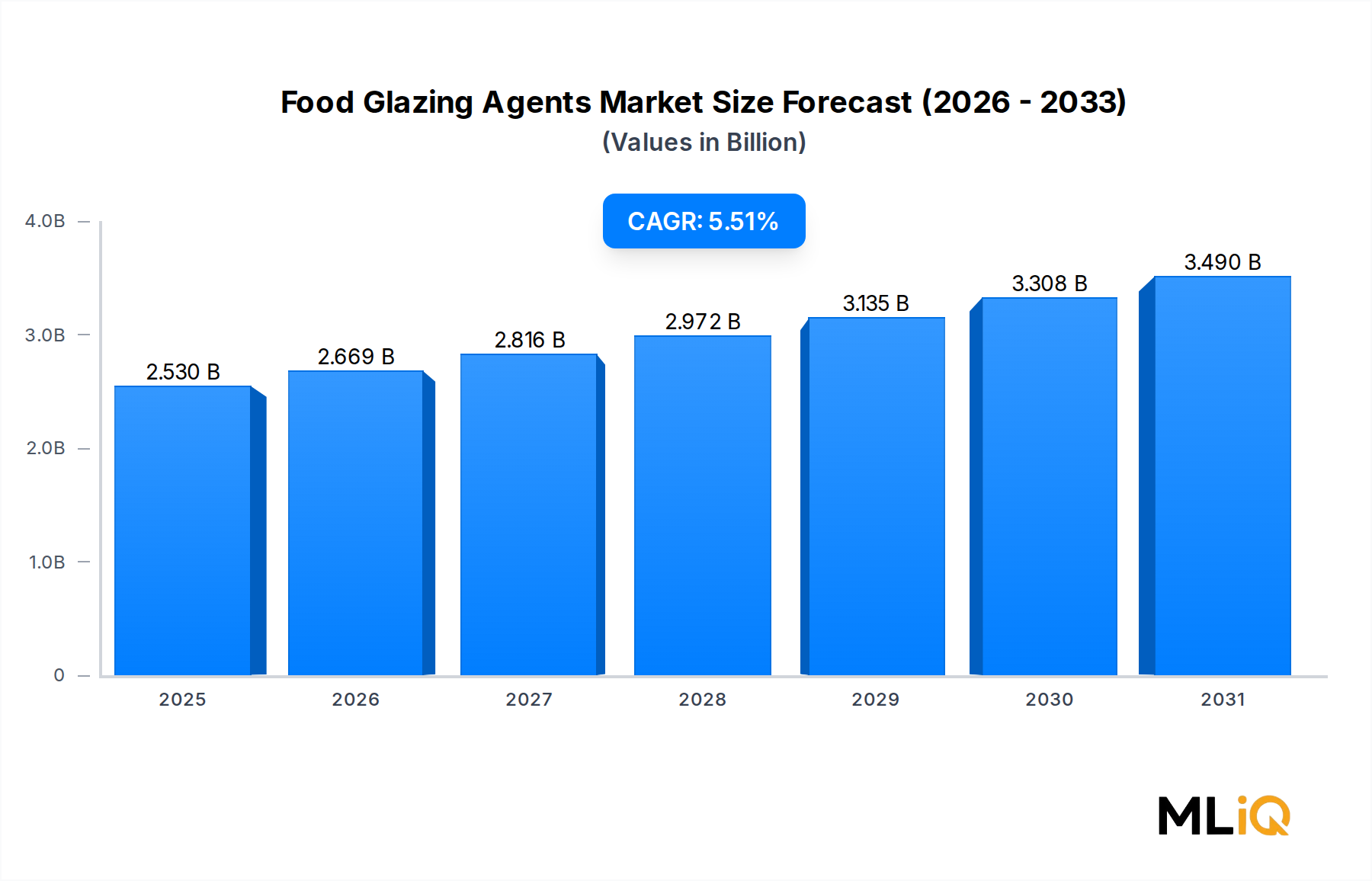

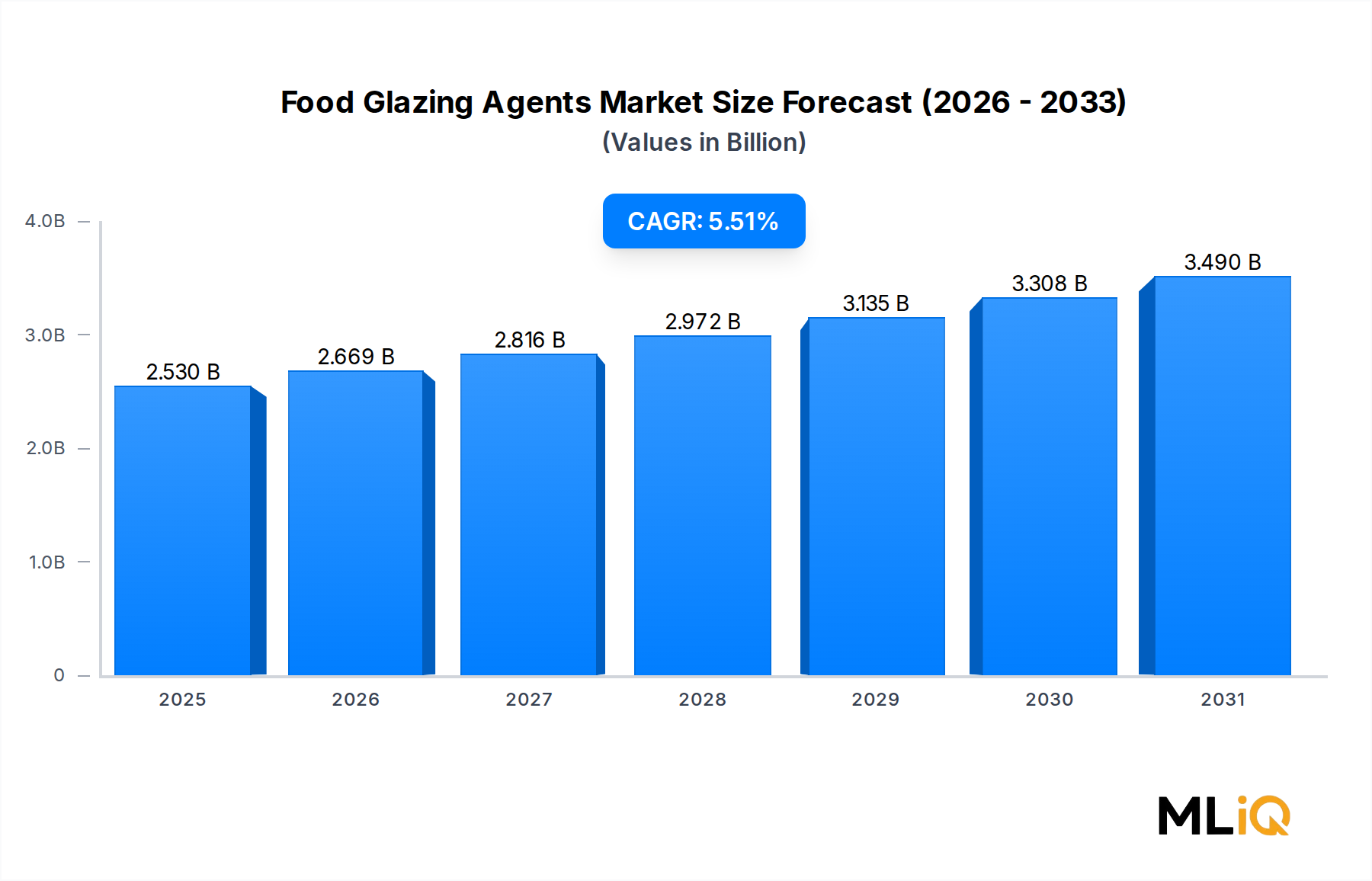

The global Food Glazing Agents Market is valued at $2.53 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 5.51% through 2033, reflecting robust demand across bakery, confectionery, fresh produce, and processed meat categories. Glazing agents — encompassing natural waxes, shellac, stearic acid, and synthetic alternatives — serve critical functional roles including moisture retention, surface sheen enhancement, shelf-life extension, and microbial barrier formation. These multifaceted properties place them at the intersection of aesthetics and food preservation technology.

Several macro tailwinds are accelerating market expansion. First, the global processed food industry continues to scale, with the broader Food Processing Ingredients Market registering sustained investment in surface-active and protective ingredient categories. Second, consumer preference for premium, visually appealing food products is intensifying, particularly in developed economies where retail presentation drives purchasing decisions. Third, the clean-label movement is prompting reformulation away from synthetic coatings toward naturally derived agents such as carnauba wax, beeswax, and candelilla wax, benefiting suppliers with certified organic and non-GMO portfolios.

From a segmentation perspective, the natural and organic sub-segment is outpacing conventional alternatives, driven by tightening regulatory scrutiny of petroleum-derived coatings in the European Union and parts of Asia Pacific. Bakery and confectionery applications collectively represent the largest end-use cluster, while fruits and vegetables constitute a rapidly growing secondary application as fresh-cut produce processors seek longer shelf life without synthetic preservatives.

Geographically, North America retains the largest revenue share owing to high per-capita processed food consumption and well-developed cold-chain infrastructure, while Asia Pacific is the fastest-growing region, propelled by urbanization, rising disposable incomes, and the expansion of organized retail. Europe remains a highly regulated but innovation-driven market, where stringent EU food contact material standards are catalyzing investment in bio-based coating solutions.

Looking ahead to 2033, the market is expected to benefit from technological advances in microencapsulation, edible film formulation, and nano-coating platforms, as manufacturers seek to differentiate products while meeting tightening global food safety standards. Strategic acquisitions, capacity expansions in emerging markets, and R&D investment in plant-derived wax alternatives will define the competitive frontier over the forecast horizon.

Among all product types within the Food Glazing Agents Market, carnauba wax holds the leading revenue share and continues to consolidate its position as the industry's benchmark glazing ingredient. Derived from the leaves of the Copernicia prunifera palm native to northeastern Brazil, carnauba wax offers an unmatched combination of high melting point (approximately 82–86°C), exceptional hardness, non-toxicity, and brilliant surface gloss — attributes that make it indispensable in confectionery panning, fruit coating, and pharmaceutical tablet finishing.

The segment's dominance is underpinned by several structural factors. From a regulatory standpoint, carnauba wax holds approval status under the U.S. Food and Drug Administration (FDA) as GRAS (Generally Recognized as Safe), is listed under EU Regulation (EC) No 1333/2008 as additive E903, and is accepted by Codex Alimentarius, granting manufacturers global market access without reformulation barriers. This universal regulatory clearance is a decisive competitive advantage over synthetic alternatives that face region-specific restrictions.

On the demand side, the global confectionery industry — a primary consumer segment feeding into the Confectionery Market — is valued in the hundreds of billions of dollars globally, and virtually all hard-panned candies, chocolate-coated nuts, and sugar-coated tablets utilize carnauba wax as a final polish coat. Leading confectionery producers demand consistent particle size distribution, low moisture content (below 1%), and verifiable traceability from certified sustainable Brazilian sources. These quality requirements have elevated barriers to entry and entrenched incumbent suppliers.

Key players dominating the carnauba wax sub-segment include CAPOL GMBH, which offers food-grade carnauba wax dispersions optimized for drum-coating processes; KOSTER KEUNEN, which maintains vertically integrated sourcing operations in Brazil; and STRAHL & PITSCH, INC., known for refined wax blends tailored to pharmaceutical and food dual-use applications. COLORCON® is also a significant participant, particularly in functional coating systems that combine carnauba wax with film-forming polymers for controlled-release confectionery and nutraceutical applications.

Market share within this segment is gradually consolidating as mid-tier suppliers struggle to meet increasingly stringent sustainability certification requirements, including Rainforest Alliance and Brazilian IBAMA environmental compliance standards. The trend toward certified sustainable sourcing is reshaping supplier relationships, with large food manufacturers requiring third-party chain-of-custody documentation that smaller wax processors cannot economically provide.

Price dynamics for carnauba wax are closely tied to Brazilian agricultural cycles, currency fluctuations in the Brazilian real, and seasonal harvest variability. The 2021–2023 period saw significant price volatility, with spot prices for Type-3 carnauba wax rising by approximately 25–35% due to drought conditions in Piauí and Ceará states combined with logistical bottlenecks during global shipping disruptions. This price sensitivity is encouraging some manufacturers to explore blended formulations incorporating candelilla wax or rice bran wax as partial substitutes, though full substitution remains technically challenging given carnauba's superior gloss index.

Overall, the carnauba wax segment is expected to maintain its dominant market position through 2033, supported by clean-label tailwinds, expanding confectionery markets in Asia Pacific, and the absence of a technically equivalent synthetic alternative that meets global regulatory standards.

The Food Glazing Agents Market is governed by a defined set of quantifiable growth drivers and structural constraints that investors and strategic planners must account for when modeling the sector's trajectory.

Primary Growth Drivers:

The first major driver is the expansion of the global bakery and confectionery sector. The Bakery Ingredients Market alone is projected to exceed $20 billion globally by 2030, and virtually all premium baked goods, chocolate products, and sugar confectionery incorporate glazing agents for sheen, moisture protection, and microbial control. Increased snacking frequency and premiumization trends in markets such as the United States, Germany, China, and India are directly translating into higher per-unit consumption of glazing agents.

The second driver is the global fresh produce trade. International fruit trade volumes have grown at approximately 3–4% annually over the past decade, and all commercially exported citrus fruits, apples, mangoes, and avocados receive wax coating treatments post-harvest to reduce transpiration losses by up to 30–40% and extend marketable shelf life by 1–3 weeks. This application creates a structurally recurring and volume-driven demand base for carnauba, beeswax, and shellac-based coating solutions.

A third driver is the clean-label shift, which is redirecting formulation investment toward the Natural Food Additives Market, of which food glazing agents are a key sub-component. Consumer surveys across North America and Europe consistently show that 60–70% of shoppers prefer products with recognizable, naturally derived ingredients, creating a commercial incentive for branded food manufacturers to reformulate with GRAS-certified waxes.

Primary Constraints:

The primary constraint is raw material supply concentration. Carnauba wax sourcing is geographically confined to Brazil, creating single-source geopolitical and climatic risk. Similarly, shellac production is concentrated in India and Thailand. Any disruption to these supply chains — whether through weather events, export restrictions, or labor disputes — can trigger price spikes of 20–40% within a single quarter, compressing processor margins.

A secondary constraint is the rising cost of certification and compliance. Achieving organic, kosher, halal, and sustainability certifications across multiple jurisdictions adds 8–15% to operational overhead for smaller suppliers, potentially limiting market participation and concentrating the competitive landscape.

The Food Glazing Agents Market features a moderately consolidated competitive landscape, with a mix of specialized wax processors, ingredient distributors, and diversified coating solution providers. The following profiles summarize the strategic positioning of key participants:

CAPOL GMBH: A leading European specialist in wax-based coating and glazing systems, CAPOL supplies food-grade carnauba, beeswax, and shellac-based coatings to confectionery and pharmaceutical manufacturers globally, with a strong technical service model centered on application-specific formulation support.

POTH HILLE & CO LTD: A UK-based wax supplier with over a century of industry experience, Poth Hille offers a broad portfolio of food-grade waxes including carnauba, candelilla, and microcrystalline variants, serving bakery, confectionery, and fresh produce markets across Europe and the Middle East.

STRAHL & PITSCH, INC.: Headquartered in the United States, Strahl & Pitsch specializes in the processing and distribution of natural waxes for food, cosmetic, and pharmaceutical applications, maintaining direct sourcing relationships with Brazilian carnauba wax producers and Indian shellac processors.

STÉARINERIE DUBOIS: A French oleochemical company with deep expertise in fatty acids and wax derivatives including stearic acid and food-grade wax blends, Stéarinerie Dubois serves European food manufacturers seeking traceable, sustainably sourced coating ingredients aligned with EU clean-label requirements.

MANTROSE-HAEUSER CO., INC.: Part of the RPM International group, Mantrose-Haeuser is a prominent North American supplier of edible coatings, shellac-based glazes, and wax emulsions, with established supply relationships across the confectionery, bakery, and fresh produce sectors.

MASTEROL FOODS: A specialist in food-grade release agents and glazing compounds, Masterol Foods serves industrial bakery and confectionery processors with customized wax-based and oil-based coating formulations, particularly for automated production lines.

KOSTER KEUNEN: One of the world's largest processors of natural waxes, Koster Keunen maintains vertically integrated sourcing from Brazil for carnauba wax and operates processing facilities in the United States and Europe, supplying food, cosmetic, and pharmaceutical industries with consistent, specification-grade materials.

COLORCON®: Recognized globally for functional coating systems, Colorcon offers food and nutraceutical glazing solutions that integrate carnauba wax and shellac with film-forming polymers, targeting high-performance applications in dietary supplements and confectionery.

BRITISH WAX REFINING COMPANY LTD: A UK-based refiner of natural and synthetic waxes, the British Wax Refining Company supplies food-grade wax blends to European food manufacturers, with a focus on quality consistency and regulatory compliance under UK and EU food contact standards.

PURATOS: A global ingredient group headquartered in Belgium, Puratos offers glazing and finishing solutions for artisan and industrial bakery applications, combining wax-based systems with enzyme and emulsifier technologies to deliver extended shelf life and visual appeal in premium bread and pastry categories.

March 2024: CAPOL GMBH announced the commercial launch of a new generation of water-dispersible carnauba wax emulsion designed for spray application in high-speed confectionery panning lines, reducing solvent usage by approximately 40% compared to conventional alcohol-based systems.

June 2024: The European Food Safety Authority (EFSA) published an updated safety re-evaluation of shellac (E904), confirming its continued approval for use as a glazing agent in confectionery and dietary supplement applications, providing regulatory certainty for shellac-dependent manufacturers across the EU.

September 2023: MANTROSE-HAEUSER CO., INC. expanded its New Jersey production facility to increase capacity for edible shellac and carnauba wax glaze production by approximately 20%, responding to growing demand from the North American nutraceutical coating segment.

January 2024: Koster Keunen introduced a new certified organic carnauba wax grade meeting USDA NOP and EU Organic Regulation 2018/848 standards, targeting the growing clean-label confectionery and fresh produce segments.

November 2023: PURATOS launched an expanded range of plant-based glazing solutions for artisan bakeries across Europe and North America, incorporating candelilla wax as a vegan alternative to shellac and beeswax-based finishing products.

April 2024: The U.S. FDA finalized guidance clarifying labeling requirements for wax coatings on fresh produce, mandating disclosure of carnauba wax, shellac, and lac-resin glazes on retail point-of-sale signage, affecting approximately 85% of commercially distributed fresh apples and citrus fruits in the U.S. market.

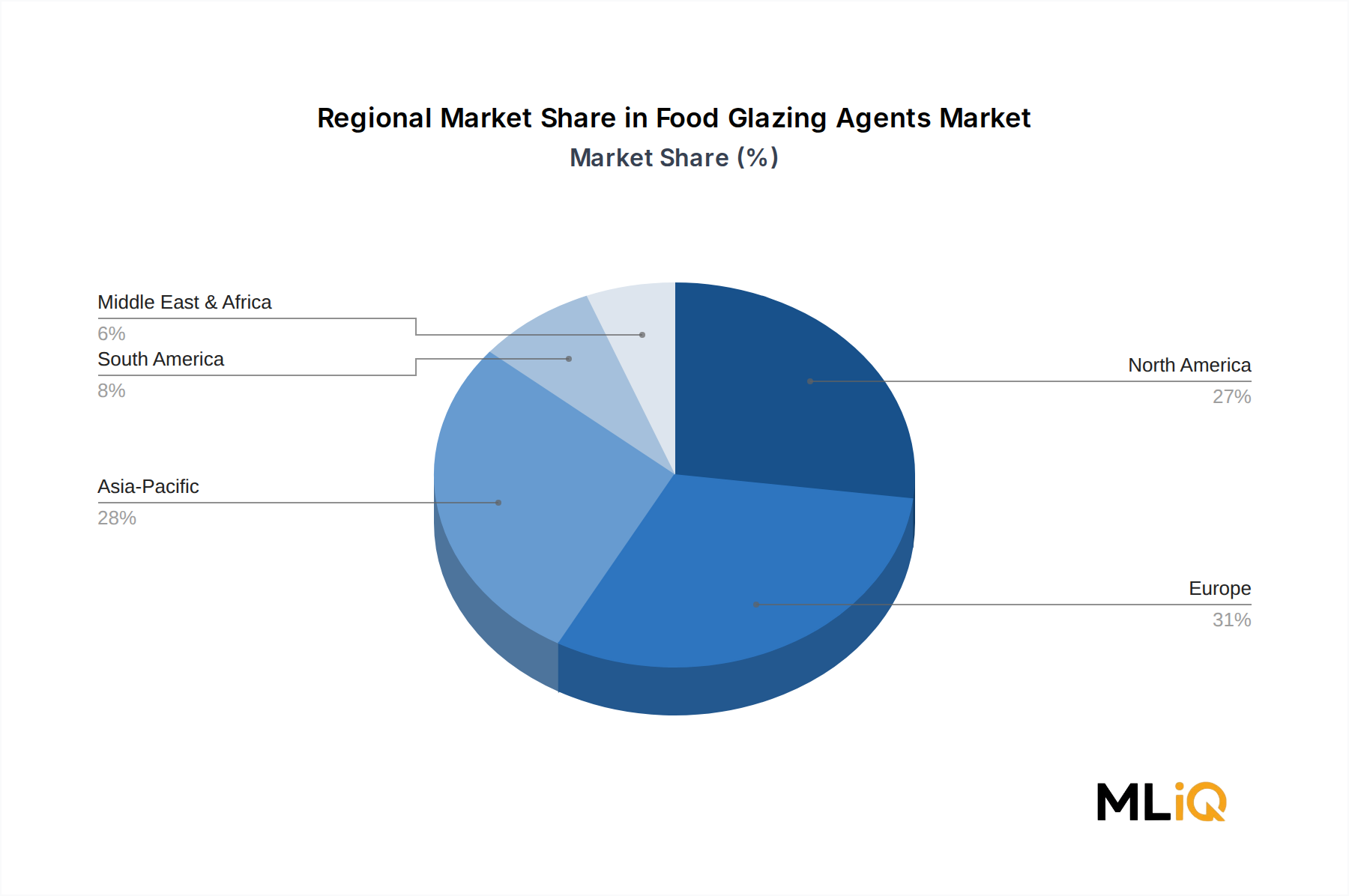

North America leads the Food Glazing Agents Market in absolute revenue terms, accounting for an estimated 32–35% of global market value in 2025. The United States is the dominant national market, driven by a large-scale processed food industry, significant fresh produce import and distribution network, and high penetration of confectionery and dietary supplement categories that rely heavily on shellac and carnauba wax coatings. The regional market is growing at a CAGR of approximately 4.8%, reflecting a mature but steadily expanding consumption base. Canada and Mexico contribute incrementally, with Mexico serving both as a consumer and a processing hub for certain wax coating applications targeting U.S. export markets.

Europe represents the second-largest regional market, with a combined revenue share of approximately 28–30%. Germany, the United Kingdom, France, and Italy are the leading national markets, underpinned by sophisticated confectionery industries and stringent food safety standards that favor certified natural glazing agents. European regulatory alignment under EU Regulation (EC) No 1333/2008 creates a harmonized approval framework that simplifies market entry for compliant suppliers. The regional CAGR is estimated at 4.5%, slightly below global average due to market maturity, though innovation in bio-based coatings is driving renewed investment.

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of 7.2–7.8% through 2033. China, India, Japan, South Korea, and ASEAN nations are all experiencing rapid growth in organized food retail, bakery chain expansion, and increasing fresh produce export activity — all of which drive demand for the Carnauba Wax Market and broader glazing agent categories. India is particularly notable as both a growing consumer market and a major producer of shellac, creating an integrated supply-demand dynamic. China's expanding confectionery and chocolate industries are generating substantial incremental demand.

South America, despite being the primary production region for carnauba wax, represents a relatively smaller consumption market, with a regional CAGR of approximately 5.0%. Brazil leads both production and domestic consumption, with growing demand from its expanding processed food sector.

The Middle East & Africa region is an emerging market for food glazing agents, growing at approximately 5.5–6.0% CAGR, driven by urbanization, food retail modernization, and increasing fresh produce trade flows through GCC distribution hubs. Halal certification compatibility is a key demand qualifier in this region.

The Food Glazing Agents Market operates within a supply chain characterized by pronounced geographic concentration of critical raw material inputs, creating systemic vulnerability to climatic, geopolitical, and logistical disruptions.

Carnauba wax, the market's dominant ingredient, is exclusively sourced from northeastern Brazil, primarily the states of Piauí, Ceará, and Rio Grande do Norte. Annual production volumes fluctuate significantly with rainfall patterns; drought years can reduce harvest yields by **20–

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.51% from 2020-2034 |

| Segmentation |

|

Factors such as are projected to boost the Food Glazing Agents Market market expansion.

Key companies in the market include CAPOL GMBH, POTH HILLE & CO LTD, STRAHL & PITSCH, INC., STÉARINERIE DUBOIS, MANTROSE-HAEUSER CO., INC., MASTEROL FOODS, KOSTER KEUNEN, COLORCON®, BRITISH WAX REFINING COMPANY LTD, PURATOS.

The market segments include Nature, Product Type, Application.

The market size is estimated to be USD 2.53 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3712, USD 5769, and USD 10663 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Food Glazing Agents Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Food Glazing Agents Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.