1. What are the major growth drivers for the U.S. and Europe polyphenol Market market?

Factors such as are projected to boost the U.S. and Europe polyphenol Market market expansion.

+1 2315155523

U.S. and Europe polyphenol Market

U.S. and Europe polyphenol Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

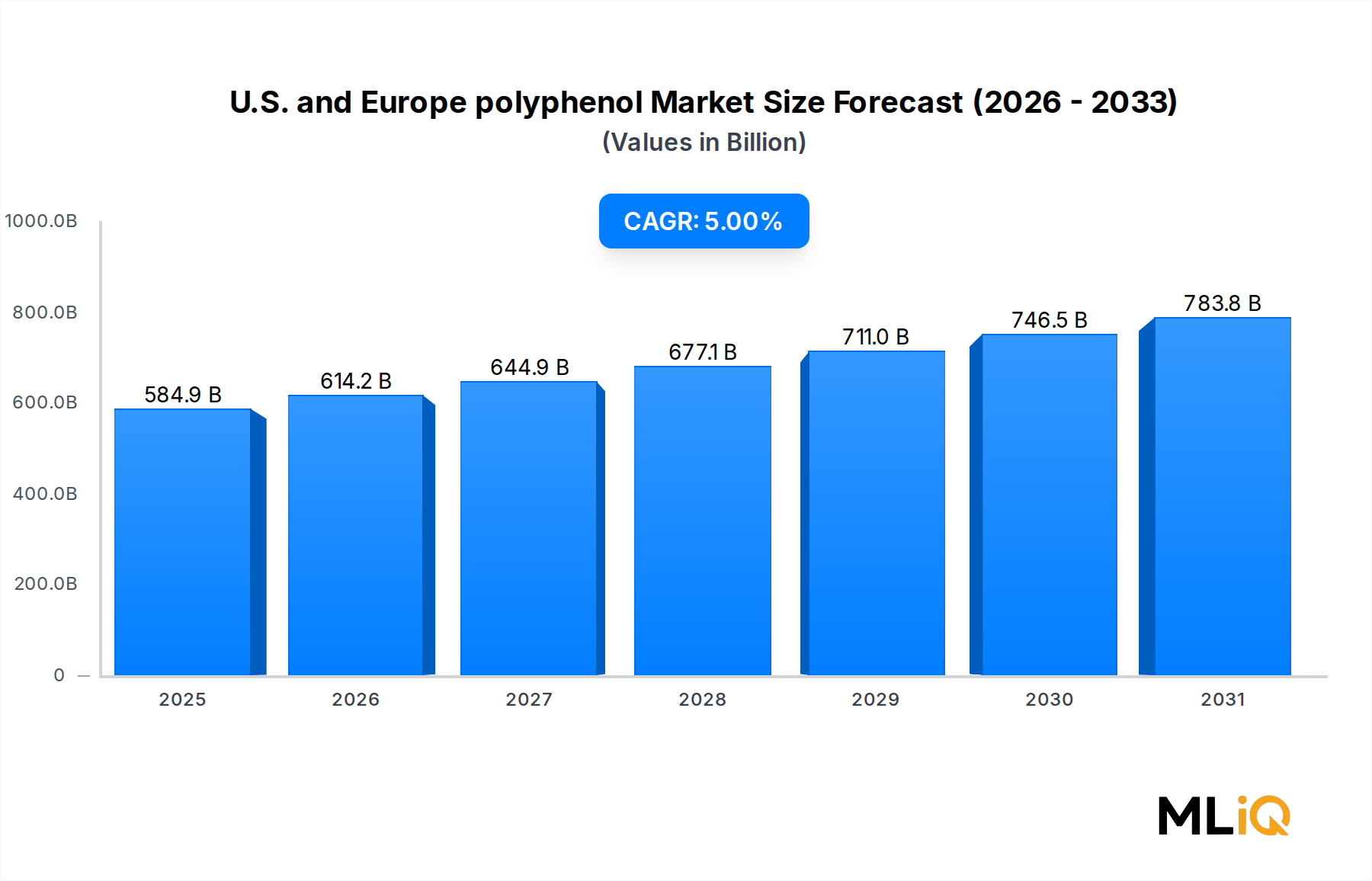

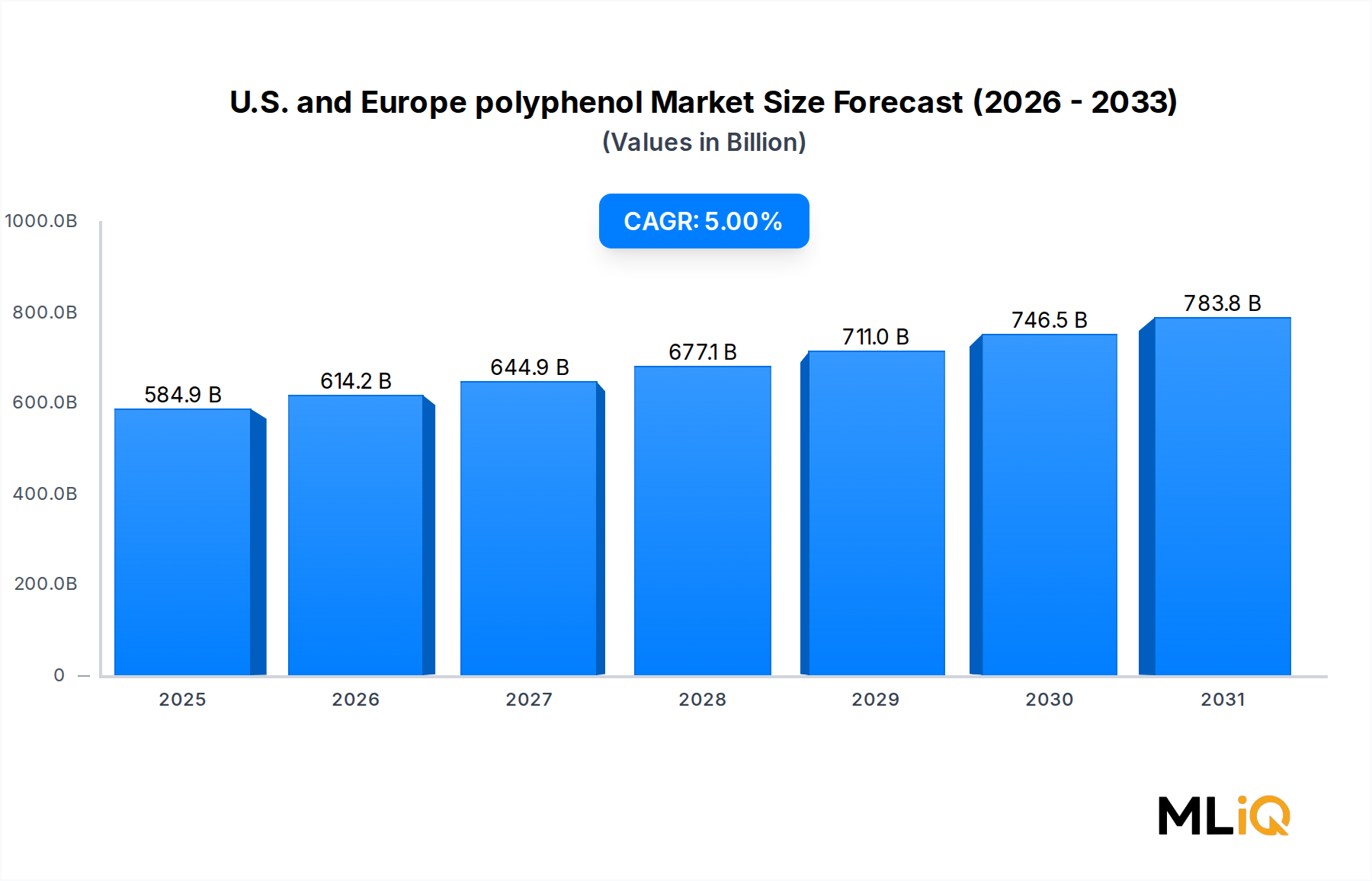

The U.S. and Europe polyphenol market is positioned at a pivotal inflection point, driven by accelerating consumer interest in preventive health, plant-derived nutrition, and clean-label formulation. As of the base year, the combined market valuation stands at approximately $584,907 million, reflecting a robust and expanding commercial landscape spanning dietary supplementation, functional food innovation, and bioactive ingredient manufacturing. The market is projected to advance at a compound annual growth rate (CAGR) of 5.0% through the forecast horizon, underscoring sustained demand momentum across both geographies.

Several macro-level tailwinds are reinforcing this trajectory. First, rising consumer awareness of the links between polyphenol intake and chronic disease prevention — including cardiovascular disorders, metabolic syndrome, and neurological decline — has elevated polyphenols from niche nutritional compounds to mainstream dietary constituents. Scientific literature continues to validate the antioxidant, anti-inflammatory, and chemopreventive properties of polyphenol classes including flavonoids, stilbenes, tannins, and phenolic acids, lending credibility to product claims and stimulating R&D investment.

In the United States, aging demographics are a structural demand driver. With over 54 million Americans aged 65 or older and this cohort projected to reach 80 million by 2040, the appetite for bioactive compounds that support healthy aging has become a long-term commercial force. In Europe, regulatory emphasis on substantiated health claims — combined with a well-established tradition of botanical medicine — has created a receptive environment for polyphenol-enriched product launches across Germany, France, the United Kingdom, and Italy.

From a supply-side perspective, advances in extraction technology — including supercritical CO2 extraction, ultrasound-assisted extraction, and membrane filtration — are improving yield efficiency and reducing production costs, enabling manufacturers to scale polyphenol ingredient supply without proportional cost escalation. These innovations are particularly significant for high-value polyphenol sources such as grape seed, green tea, and apple.

Application-wise, functional beverages and dietary supplements collectively account for the dominant revenue share, with nutraceutical innovation serving as the primary commercialization channel. The clean-label movement is encouraging formulators to replace synthetic antioxidants with polyphenol-based alternatives across a widening range of food and beverage categories.

Looking forward, the U.S. and Europe polyphenol market is expected to benefit from increased investment in bioavailability-enhancement technologies, personalized nutrition platforms, and sustainability-aligned sourcing strategies. Strategic partnerships between ingredient suppliers and branded consumer health companies are anticipated to intensify, further consolidating competitive positioning and accelerating market penetration across value-chain tiers.

Among all polyphenol source segments — including apple, green tea, grape seed, maracuya/passion fruit, and others — the grape seed segment commands the largest revenue share within the U.S. and Europe polyphenol market. This dominance reflects a confluence of scientific validation, established supply chain infrastructure, high bioavailability of oligomeric proanthocyanidins (OPCs), and broad applicability across functional food, beverage, and nutraceutical formulations.

Grape seed extract (GSE) is recognized as one of the most potent natural antioxidant compounds commercially available, with an oxygen radical absorbance capacity (ORAC) value substantially exceeding that of vitamin C and vitamin E on a per-gram basis. The high OPC concentration in GSE — typically ranging between 92% and 95% in standardized commercial-grade extracts — makes it the preferred polyphenol source for formulators targeting cardiovascular health, skin protection, and anti-aging applications.

From a supply perspective, Europe — particularly France, Italy, and Spain — benefits from proximity to major wine-producing regions where grape pomace (the primary raw material for GSE) is generated as a byproduct of winemaking. This geographic advantage reduces raw material logistics costs and supports the circular economy narrative that increasingly resonates with sustainability-oriented buyers. The Grape Seed Extract Market has expanded significantly over the past decade, with European extraction facilities scaling capacity in direct response to demand from U.S. importers and domestic nutraceutical manufacturers.

In the United States, GSE has achieved broad distribution across mass-market supplement retail, specialty health channels, and e-commerce platforms. Its inclusion in cardiovascular support formulas, beauty-from-within supplements, and sports recovery products has diversified demand beyond single-application positioning. Clinical research published in peer-reviewed journals — including studies demonstrating GSE's efficacy in reducing systolic blood pressure by 1.54 mmHg in controlled trials — continues to provide the evidence base needed for compliant health communication.

Key market participants active in the grape seed segment include Naturex S.A. (now part of Givaudan), Indena S.P.A., and Berkem, all of which maintain proprietary extraction platforms and standardized ingredient portfolios. These companies compete on standardization precision, traceability credentials, and the depth of clinical dossiers available to support customer formulation claims.

The segment's share is not merely holding steady — it is consolidating. As regulatory scrutiny over synthetic antioxidants intensifies in both the U.S. (under FDA guidance frameworks) and Europe (under EFSA regulations), formulators are systematically substituting GSE for butylated hydroxytoluene (BHT) and butylated hydroxyanisole (BHA) in lipid-containing food matrices. This substitution dynamic is structurally expanding the addressable market for grape seed polyphenols beyond supplement formats into food preservation and bakery applications.

Furthermore, emerging applications in cosmeceuticals — where GSE's skin-protective properties are leveraged in topical and ingestible beauty formats — are opening adjacent revenue streams for ingredient manufacturers. The convergence of nutricosmetics and functional nutrition is expected to reinforce grape seed's dominant position through the forecast period, with the segment projected to maintain a revenue share premium of approximately 8–12 percentage points above the nearest competing segment (green tea) throughout the forecast horizon.

The U.S. and Europe polyphenol market is governed by a defined set of quantifiable drivers and constraints that determine its growth velocity and structural direction.

Driver 1: Consumer Health Expenditure Expansion. U.S. consumer spending on dietary supplements exceeded $56 billion in 2023, according to industry trade data, with antioxidant and botanical categories among the fastest-growing subcategories. European nutraceutical expenditure similarly grew at 4.8% annually in recent years, with polyphenol-based products representing a disproportionately high share of new product launches — estimated at 18% of total botanical supplement introductions in 2023.

Driver 2: Functional Food Reformulation Trends. The global functional food reformulation wave, which has prompted more than 65% of large food manufacturers to audit their synthetic additive portfolios, is creating structured demand for natural antioxidant replacements. Polyphenol ingredients, particularly those derived from grape seed and green tea, are being adopted at scale as preservative and fortification agents, directly expanding the addressable market for ingredient suppliers.

Driver 3: Scientific Publication Volume. The cumulative body of peer-reviewed literature on polyphenol bioactivity has surpassed 25,000 indexed publications on PubMed as of 2024, providing a continuously replenishing evidence base that supports regulatory-compliant product claims and stimulates consumer confidence.

Constraint 1: Bioavailability Limitations. Despite proven antioxidant efficacy in vitro, the systemic bioavailability of many polyphenol classes in vivo remains constrained by rapid metabolism, protein binding, and poor intestinal absorption. This limits the clinical transferability of laboratory findings and creates a regulatory communication challenge for manufacturers, particularly under EFSA's stringent health claim authorization framework.

Constraint 2: Raw Material Price Volatility. Agricultural variability in grape, tea, and apple harvests — driven by climate change-related yield disruptions — introduces procurement cost uncertainty. A 15–20% price fluctuation in grape pomace pricing was observed during 2022–2023 drought conditions across Southern Europe, temporarily compressing margins for extraction-stage manufacturers.

These forces collectively define the market's 5.0% CAGR profile — a trajectory that reflects genuine demand strength moderated by supply and regulatory friction.

The competitive landscape of the U.S. and Europe polyphenol market is characterized by a mix of specialized ingredient suppliers, integrated nutrition companies, and global agri-food conglomerates. The following profiles summarize the strategic positioning of leading participants:

FUTURECEUTICALS: A U.S.-based specialty ingredient company focused on whole-food-derived polyphenol extracts, FUTURECEUTICALS maintains a strong clinical research platform and sources raw materials from traceable North American agricultural supply chains.

SWANSON HEALTH PRODUCTS, INC.: Operating primarily as a direct-to-consumer supplement brand, Swanson Health Products leverages an extensive polyphenol product portfolio — including resveratrol, quercetin, and OPC-based formulas — across e-commerce and catalog channels.

NATUREX S.A.: A globally recognized botanical extraction specialist (now integrated within Givaudan's active beauty and nutrition division), Naturex S.A. offers standardized polyphenol ingredients with deep regulatory compliance documentation for both U.S. and European markets.

INDENA S.P.A.: An Italian phytochemical company with over a century of botanical extraction expertise, Indena S.P.A. is a preferred supplier for pharmaceutical-grade polyphenol ingredients, particularly for applications requiring high-purity standardization and clinical validation.

CARGILL INC.: As a diversified agri-food giant, Cargill Inc. participates in the polyphenol market through its cocoa and botanical ingredient divisions, with a focus on scalable supply and integrated sourcing from cocoa, tea, and grape processing operations.

BERKEM: A French specialty chemicals and botanical extraction company, Berkem focuses on grape-derived polyphenol ingredients and maintains proprietary extraction technologies developed in partnership with French wine-industry raw material suppliers.

GLANBIA PLC. (GLANBIA NUTRITIONALS, INC.): An Irish nutrition company with significant U.S. operations, Glanbia Nutritionals provides polyphenol-containing ingredient blends primarily targeting sports nutrition and active health markets.

NOF AMERICA CORPORATION: Specializing in lipid-based delivery systems, NOF America Corporation contributes to the polyphenol market through encapsulation and bioavailability enhancement platforms that improve the commercial utility of polyphenol actives in finished formulations.

AMAX NUTRASOURCE, INC.: A nutraceutical ingredient distributor with a North American focus, Amax Nutrasource Inc. sources and commercializes a range of standardized polyphenol extracts for dietary supplement manufacturers.

KONINKLIJKE DSM N.V.: A global life sciences and nutrition company, Koninklijke DSM N.V. integrates polyphenol ingredients into its broader micronutrient and bioactive portfolio, targeting food fortification, premix, and supplement markets across Europe and North America.

January 2024: NATUREX S.A. announced the expansion of its grape polyphenol extraction capacity at its Avignon, France facility, adding 2,000 metric tons per year of additional processing throughput to meet rising European demand.

March 2024: KONINKLIJKE DSM N.V. completed integration of a polyphenol-based antioxidant line into its Human Nutrition premix portfolio, targeting functional food and clinical nutrition customers across 15 European markets.

June 2023: INDENA S.P.A. received a new GRAS (Generally Recognized as Safe) notification acknowledgment from the U.S. FDA for its proprietary green tea polyphenol extract, expanding its U.S. market access for food and beverage applications.

September 2023: CARGILL INC. launched a cocoa-derived flavanol ingredient under its CocoaWell platform, positioned specifically for the Functional Beverages Market, targeting cardiovascular health-focused product developers.

November 2023: FUTURECEUTICALS published Phase II clinical trial results demonstrating statistically significant improvements in vascular function biomarkers associated with its apple polyphenol extract, strengthening the clinical narrative for the segment.

February 2024: The European Food Safety Authority (EFSA) initiated a review of substantiation dossiers for resveratrol health claims, a development with potential implications for resveratrol-based product positioning across the EU market.

April 2024: GLANBIA PLC. announced a strategic supply agreement with a Spanish grape pomace processor to secure long-term raw material supply for its polyphenol-containing sports nutrition ingredient lines.

The U.S. and Europe polyphenol market exhibits distinct regional performance profiles, with the United States representing the largest single national market and Germany anchoring European demand.

United States: The U.S. constitutes the dominant revenue contributor within this bi-regional market, accounting for an estimated 42–45% of combined market value. Driven by a mature supplement retail infrastructure, high consumer health literacy, and robust e-commerce penetration, the U.S. market is growing at approximately 5.2% CAGR. The primary demand driver is the dietary supplement sector, particularly cardiovascular health, cognitive support, and anti-aging formulations. Regulatory clarity provided by the Dietary Supplement Health and Education Act (DSHEA) framework facilitates faster product commercialization compared to European equivalents.

Germany: Germany is the leading European market for polyphenol ingredients, supported by a strong tradition of phytomedicine, a sophisticated retail pharmacy (Apotheke) distribution channel, and significant domestic nutraceutical manufacturing capacity. Germany accounts for approximately 12–14% of the combined market and is growing at a CAGR of 4.8%, driven principally by functional food fortification and standardized botanical extract adoption.

France: France benefits from proximity to world-class grape polyphenol raw material sources and is home to several major extraction facilities. The French market is growing at approximately 4.5% CAGR, with domestic consumption concentrated in premium dietary supplement and cosmeceutical channels. France is also a major exporter of grape-derived polyphenol ingredients to other European markets and to the United States.

United Kingdom: Post-Brexit regulatory divergence has created some friction in U.K.-EU ingredient trade flows, but the U.K. polyphenol market remains robust, growing at approximately 4.6% CAGR, supported by strong consumer demand for functional beverages and evidence-based supplement formulations.

Italy and Spain: Both markets are significant in terms of raw material production (wine industry byproducts) and are growing at 4.3–4.7% CAGR, with domestic consumption increasingly oriented toward premium nutraceuticals and natural cosmetics. Spain is emerging as a fast-growing consumption market alongside its established role as a raw material exporter.

Overall, the United States represents the most mature demand market by revenue density, while Southern European markets — particularly Spain and Italy — represent the fastest-growing consumption segments relative to their base size, driven by rising disposable incomes and health-conscious lifestyle shifts.

The U.S. and Europe polyphenol market operates within a complex cross-Atlantic trade architecture, with significant bilateral ingredient flows underpinning commercial supply chains on both sides.

Europe is a net exporter of polyphenol raw materials and semi-processed extracts to the United States, with France, Spain, and Italy collectively supplying an estimated 60–65% of U.S.-imported grape seed and resveratrol ingredients by volume. This trade corridor is well-

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.0% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the U.S. and Europe polyphenol Market market expansion.

Key companies in the market include FUTURECEUTICALS, SWANSON HEALTH PRODUCTS, INC., NATUREX S.A., INDENA S.P.A., CARGILL INC., BERKEM, GLANBIA PLC. (GLANBIA NUTRITIONALS, INC.), NOF AMERICA CORPORATION, AMAX NUTRASOURCE, INC., KONINKLIJKE DSM N.V..

The market segments include Type, Application.

The market size is estimated to be USD 584907 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4290, and USD 8186 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "U.S. and Europe polyphenol Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the U.S. and Europe polyphenol Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.