1. What are the major growth drivers for the Indonesia Fungicide Market market?

Factors such as Demand For Landscaping Maintenance; Adoption of Green Spaces and Green Roofs are projected to boost the Indonesia Fungicide Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

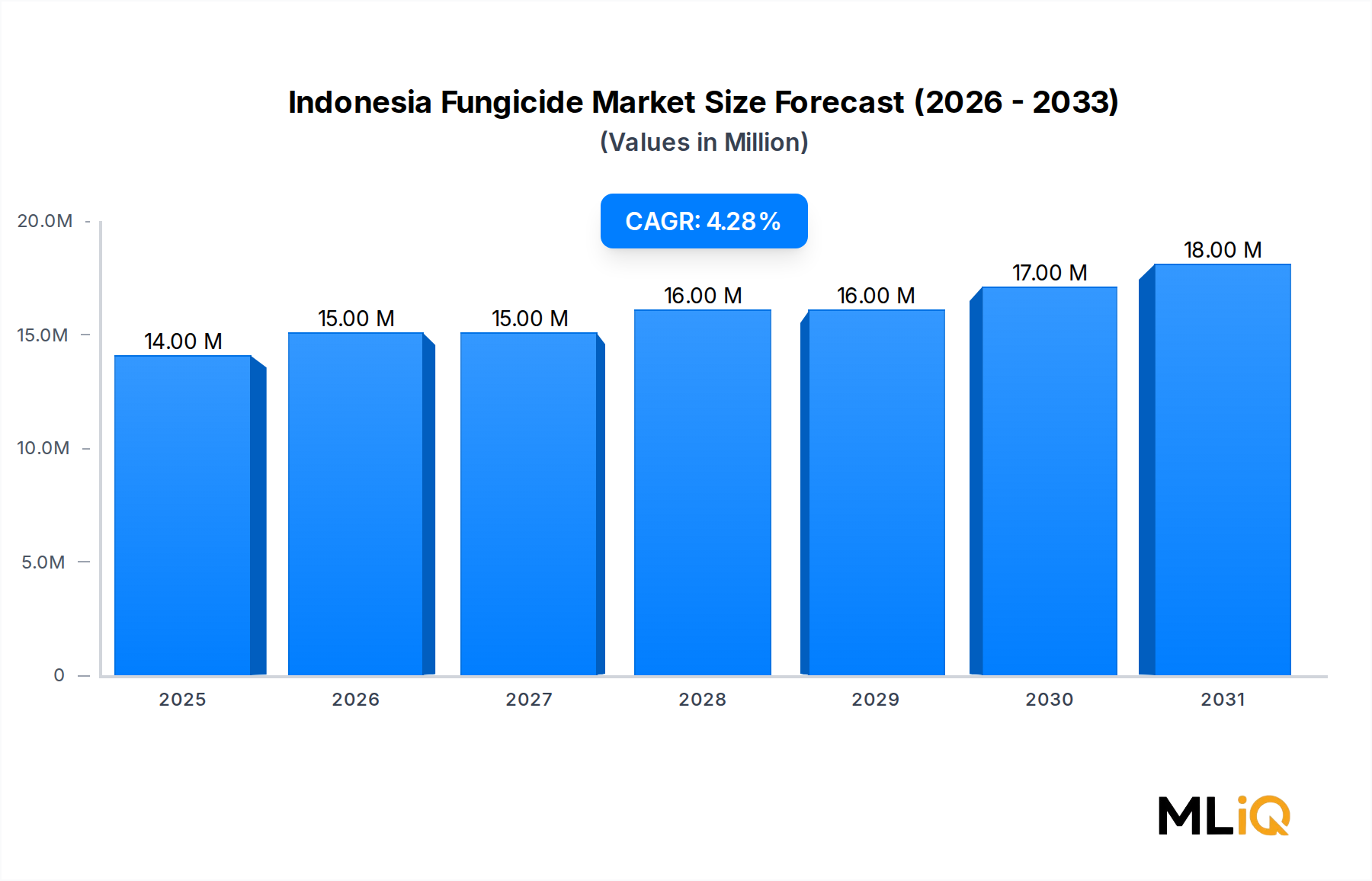

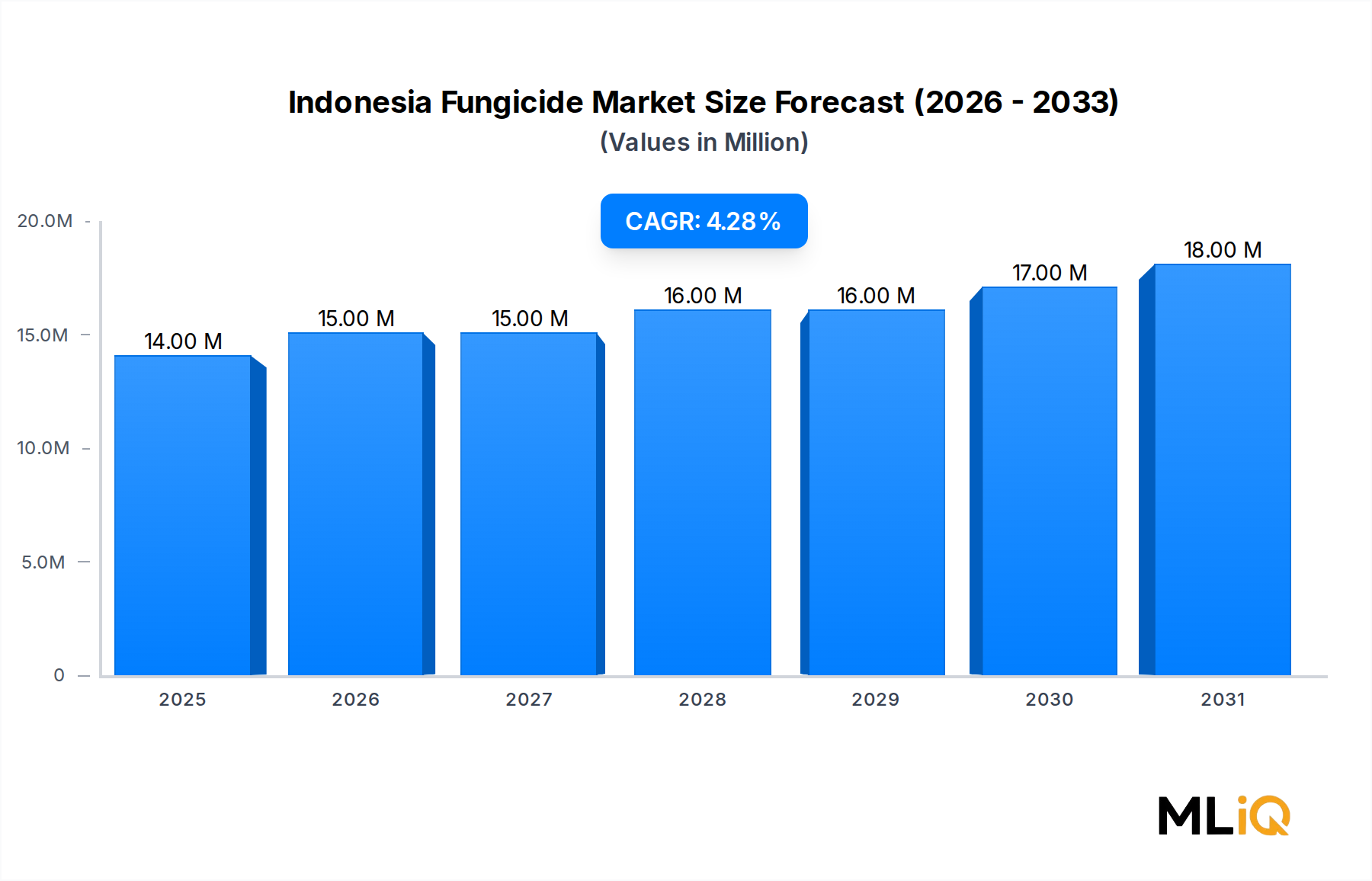

The Indonesia Fungicide Market is valued at $14.4 million as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 3.44% through 2033. This steady trajectory reflects a structural shift in Indonesian agricultural practices, where smallholder farmers and large plantation operators alike are intensifying fungicide deployment to safeguard crop yields against an increasingly volatile fungal disease landscape.

Indonesia's agricultural sector remains the backbone of its rural economy, employing over 40% of the national labor force and contributing significantly to GDP. Palm oil, rice, coffee, maize, and rubber collectively dominate land use across the archipelago, and each of these commodities faces mounting pressure from soil-borne pathogens, foliar blights, and seed-borne infections. The proliferation of fungal diseases — including Ganoderma boninense in oil palm plantations, rice blast caused by Magnaporthe oryzae, and coffee leaf rust driven by Hemileia vastatrix — has elevated fungicide adoption as a non-negotiable input cost rather than an optional agronomic supplement.

Macro tailwinds reinforcing this growth include government-backed food security initiatives under Indonesia's strategic agriculture development programs, rising export compliance standards for palm oil and coffee in the European Union, and expanded irrigation infrastructure that inadvertently creates humid microenvironments favorable to fungal proliferation. Furthermore, the growing preference for integrated pest management systems is driving demand for multi-mode-of-action fungicides that minimize resistance development.

On the supply side, multinational agrochemical corporations and regional distributors are channeling investment into product innovation, particularly systemic and contact fungicide combinations. The introduction of new active ingredients and co-formulated products has expanded the solution palette available to Indonesian growers. Companies such as BASF SE, Bayer AG, Syngenta Group, and FMC Corporation have all prioritized Indonesia as a key emerging market within their Asia Pacific commercial strategies.

Looking forward through 2033, the Indonesia Fungicide Market is poised to benefit from digitally enabled precision agriculture platforms that optimize fungicide application timing and dosage, reducing input waste while improving efficacy. The transition toward biological and biopesticide-integrated fungicide programs also represents a medium-term growth vector, particularly as sustainability certification requirements for Indonesian exports tighten. The convergence of regulatory pressure, agronomic necessity, and technological enablement positions the market for sustained, if measured, expansion across the forecast horizon.

Among the various application modes segmenting the Indonesia Fungicide Market, foliar application commands the largest revenue share. This dominance is rooted in the agronomic characteristics of Indonesia's primary crops, the infrastructure realities of its farming landscape, and the mode-of-action profiles of the most commercially significant fungicide chemistries currently registered in the country.

Foliar fungicide application involves the direct spray of liquid formulations onto plant leaf surfaces, stems, and exposed fruit bodies. This method delivers active ingredients to the site of infection or pre-emptive protection zones with high efficiency and is particularly well-suited to the high-humidity, high-rainfall conditions prevailing across Indonesia's equatorial agricultural zones. The wet season — which in Sumatra, Java, and Kalimantan can extend for six to eight months — creates near-continuous risk windows for fungal sporulation, making repeated foliar spray applications a standard agronomic protocol.

For rice cultivation, which spans millions of hectares across Java, Sumatra, Sulawesi, and Nusa Tenggara, foliar fungicide programs targeting rice blast, sheath blight, and brown spot are applied one to three times per growing season depending on disease pressure and varietal susceptibility. The sheer scale of Indonesian rice production — approximately 10.2 million hectares harvested annually — translates into enormous aggregate fungicide volumes delivered via foliar means. Propiconazole, tricyclazole, azoxystrobin, and hexaconazole are among the active ingredients most frequently applied through foliar routes in rice systems.

Palm oil represents another critical demand center for foliar fungicides. While Ganoderma basal stem rot is primarily managed through soil and stem treatments, foliar applications of copper-based compounds and triazole fungicides are used to manage leaf anthracnose and other foliar pathogens that reduce photosynthetic efficiency and overall bunch yield. Indonesia's position as the world's largest palm oil producer — with over 16 million hectares under cultivation — creates a structurally large and recurring demand base.

In the fruits and vegetables segment, which encompasses chili peppers, tomatoes, shallots, cucumbers, and tropical fruits, foliar fungicide application is the primary delivery mechanism. Disease complexes including downy mildew, powdery mildew, Botrytis gray mold, and Phytophthora late blight are managed predominantly through scheduled foliar spray programs. Indonesian horticulture has seen accelerated intensification over the past decade, driven by domestic consumption growth and expanding modern retail channels demanding visually uniform, disease-free produce.

Key players capturing share within the foliar segment include Syngenta Group with its Amistar and Score product lines, BASF SE with Cabrio and Signum formulations, and Bayer AG with its Folicur and Flint portfolio. FMC Corporation's recent introduction of Quintect 105 SC and Flint Pro 64.8 WG specifically targets foliar disease complexes in Indonesian horticulture, illustrating how multinational players are tailoring their commercial launches to the foliar-dominant application mode.

The foliar segment's share is consolidating rather than fragmenting, as newer chemistry classes — including SDHI fungicides and strobilurin-triazole premixes — are disproportionately formulated for foliar delivery. Generic manufacturers entering the Indonesian market, particularly those affiliated with Chinese agrochemical groups, are also primarily launching foliar-grade suspoemulsions and wettable granules, further reinforcing the segment's structural centrality within the Indonesia Fungicide Market.

Several quantifiable forces are simultaneously propelling and constraining growth within the Indonesia Fungicide Market, and understanding their relative magnitudes is critical for accurate demand forecasting.

Among the primary drivers, the increasing incidence and geographic spread of fungal diseases across Indonesia's commodity crop base is the most operationally significant. Ganoderma boninense, responsible for basal stem rot in oil palm, infects an estimated 50–80% of replanting areas in Sumatra and has no curative chemical solution, but prophylactic fungicide programs remain a revenue-generating practice. Rice blast, classified as the most destructive rice disease globally, results in average yield losses of 10–30% in severely affected Indonesian paddies, compelling farmers to allocate fungicide budgets even under tight input cost constraints. Coffee leaf rust, which spread aggressively across Sumatra's Arabica-growing regions following the 2013 epidemic, permanently elevated fungicide adoption rates among smallholder coffee farmers.

Government subsidy programs for pesticide inputs, while not uniformly applied to fungicides, have historically lowered the effective price barrier for smallholders. Indonesia's agricultural ministry has maintained subsidized distribution networks for strategic crop inputs, indirectly supporting fungicide market penetration in price-sensitive rural segments.

On the restraint side, high maintenance costs and limited technical advisory access represent structural barriers. Many Indonesian smallholders — who farm plots under 2 hectares on average — lack access to agronomic extension services capable of prescribing optimal fungicide programs. This leads to both under-application, where disease suppression is incomplete, and misapplication, which accelerates resistance development and reduces the cost-effectiveness of fungicide investments.

Labor availability constraints, particularly in post-harvest and spray application activities, compound this challenge. The rural-to-urban migration trend in Indonesia has reduced the agricultural labor pool, making tractor-mounted or drone-assisted fungicide application — which carries higher capital costs — a necessary but often unaffordable upgrade for smallholder operations.

Regulatory complexity surrounding fungicide registration, while improving, still imposes compliance timelines that delay new active ingredient introductions, giving generics a competitive window that compresses the revenue premium period for innovative chemistry within the Indonesia Fungicide Market.

The competitive structure of the Indonesia Fungicide Market is characterized by the dominance of multinational agrochemical corporations alongside a growing tier of generic and domestic players.

ADAMA Agricultural Solutions Ltd: A global generic agrochemical leader with a broad portfolio of off-patent fungicide active ingredients; ADAMA leverages its cost-competitive positioning to penetrate price-sensitive smallholder segments across Sumatra and Java.

BASF SE: One of the world's largest crop protection companies, BASF markets premium fungicide solutions including strobilurin and carboxamide chemistries specifically adapted for Indonesian rice, palm oil, and vegetable systems.

Bayer AG: A major force in Indonesian agriculture, Bayer's fungicide portfolio spans triazole, strobilurin, and multi-site contact actives, and its January 2023 partnership with Oerth Bio signals a strategic pivot toward biologically enhanced crop protection solutions.

Corteva Agriscience: The agricultural spinoff of DowDuPont, Corteva brings differentiated fungicide chemistry including SDHI actives and offers integrated crop protection programs aligned with precision agriculture platforms.

FMC Corporation: An active innovator in the Indonesian market, FMC launched Quintect 105 SC in January 2023 and Flint Pro 64.8 WG in July 2022, directly targeting high-value horticultural crops including potatoes and watermelons.

Nufarm Ltd: An Australian-headquartered agrochemical company with significant ASEAN distribution capabilities; Nufarm competes across the contact fungicide segment with copper-based and multi-site formulations suited to tropical disease complexes.

PT Biotis Agrindo: A domestic Indonesian player with a focus on biological and biopesticide-integrated solutions; PT Biotis Agrindo benefits from regulatory goodwill and local market knowledge in navigating smallholder distribution channels.

Syngenta Group: A leading multinational present across all major Indonesian crop systems; Syngenta's Amistar, Score, and Revus product families are among the most widely recognized fungicide brands among Indonesian extension officers and distributors.

UPL Limited: An India-headquartered global agrochemical company with a rapidly expanding ASEAN footprint; UPL competes on both price and product range, offering integrated solutions that bundle fungicides with herbicides and insecticides.

Wynca Group (Wynca Chemicals): A Chinese agrochemical manufacturer with growing export market ambitions; Wynca's cost-efficient production of triazole and strobilurin active ingredients positions it competitively within the generic tier of the Indonesia Fungicide Market.

January 2023: Bayer AG announced a new strategic partnership with Oerth Bio, a biotech firm specializing in RNA interference-based crop protection, with the collaboration aimed at developing eco-friendly alternatives and complements to conventional fungicide chemistry for deployment in key markets including Indonesia.

January 2023: FMC Corporation introduced Quintect 105 SC, a new fungicide product commercially launched for Indonesian farmers, specifically designed to provide broad-spectrum disease protection while securing both the quality and quantity of crop yields across rice and horticultural systems.

July 2022: FMC Corporation launched Flint Pro 64.8 WG, a wettable granule fungicide formulated to control Alternaria dry spot on potato plants and to manage leaf spot disease and stem rot in watermelon crops, directly addressing disease challenges in Indonesia's fast-growing vegetable production sector.

2022–2023: The Indonesian Ministry of Agriculture continued its enforcement of the regulation requiring all new fungicide active ingredients to undergo local efficacy trials in representative agro-ecological zones before receiving full commercial registration approval, a process that continued to affect launch timelines for several multinational entrants.

2023: Increased awareness campaigns by agrochemical associations in Indonesia, in coordination with international bodies, began promoting stewardship programs aimed at reducing fungicide resistance development, particularly in rice-growing provinces where azole fungicide use has intensified.

While the Indonesia Fungicide Market is analyzed as a single country-level market, its internal geography spans five major island groupings — Sumatra, Java, Kalimantan, Sulawesi, and Eastern Indonesia — each exhibiting distinct demand characteristics, crop compositions, and growth trajectories.

Sumatra is the single largest regional contributor to fungicide demand within Indonesia, driven primarily by its vast oil palm and rubber plantation base. Sumatra accounts for approximately 60% of Indonesia's total palm oil production, and the endemic pressure from Ganoderma boninense across replanting cycles sustains a large and relatively inelastic fungicide demand profile. Coffee cultivation in North Sumatra and Aceh further reinforces regional volumes, particularly for systemic fungicides targeting coffee leaf rust and berry disease. Sumatra's fungicide consumption growth rate tracks slightly above the national average, supported by expanding replanting programs and rising grower awareness of yield protection investments.

Java, despite being the most densely populated island, contributes significant fungicide volumes through its intensive horticultural and rice production systems. Vegetable farming in West Java, East Java, and Central Java generates high-frequency fungicide application cycles, with farmers applying fungicides four to eight times per crop cycle for chili pepper, tomato, and shallot systems. Java's market is the most mature in terms of product sophistication, with a higher proportion of premium and multi-site resistance-management products purchased relative to other islands.

Kalimantan's contribution to the Indonesia Fungicide Market is growing at the fastest sub-national rate, fueled by the rapid expansion of oil palm cultivation into newly developed agricultural frontier zones. Government transmigration programs and private plantation concessions have added hundreds of thousands of hectares of new palm area since 2015, creating incremental fungicide demand for both prophylactic and curative applications.

Sulawesi is a strategically important region for cocoa fungicide demand, as Indonesia is the world's third-largest cocoa producer and Sulawesi accounts for the majority of national cocoa output. Black pod disease (Phytophthora palmivora) and vascular streak dieback remain the most economically damaging fungal pathogens in Sulawesi's cocoa systems, driving sustained demand for copper-based and systemic fungicide products.

Eastern Indonesia, encompassing Maluku and Papua, represents the frontier growth zone with the lowest current penetration but the highest potential CAGR, contingent on infrastructure development and extension service expansion. At the broader geographic scale, the Asia Pacific Agrochemicals Market context significantly influences competitive dynamics, as pricing pressures, regulatory harmonization efforts under ASEAN frameworks, and raw material supply chains are coordinated at the regional level. Insights from the Crop Protection Chemicals Market and the Agricultural Fungicides Market indicate that Southeast Asian sub-markets, including Indonesia, are growing faster than the global average due to their underpenetrated smallholder segments and climate-driven fungal pressure intensification.

The supply chain underpinning the Indonesia Fungicide Market is structured across three principal tiers: active ingredient (AI) synthesis, formulation manufacturing, and in-country distribution. Each tier carries distinct sourcing risks and price volatility profiles that directly affect market pricing and product availability.

At the active ingredient level, Indonesia is almost entirely dependent on imports, with China and India supplying the vast majority of fungicide technical grades entering the country. Chinese manufacturers dominate the global supply of triazole active ingredients — including propiconazole, tebuconazole, and difenoconazole — as well as strobilurins such as azoxystrobin and pyraclostrobin. The concentration of AI synthesis capacity in Chinese chemical industrial parks creates significant supply chain fragility, as evidenced during the 2021–2022 period when Chinese energy rationing and factory curtailments caused spot shortages and price spikes of 15–30% for key triazole intermediates globally.\

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.44% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as Demand For Landscaping Maintenance; Adoption of Green Spaces and Green Roofs are projected to boost the Indonesia Fungicide Market market expansion.

Key companies in the market include ADAMA Agricultural Solutions Ltd, BASF SE, Bayer AG, Corteva Agriscience, FMC Corporation, Nufarm Ltd, PT Biotis Agrindo, Syngenta Group, UPL Limited, Wynca Group (Wynca Chemicals.

The market segments include Application Mode, Crop Type.

The market size is estimated to be USD 14.4 million as of 2022.

Demand For Landscaping Maintenance; Adoption of Green Spaces and Green Roofs.

Growing fungal diseases damages major crops. like palm oil. coffee. rice. and maize. increasing the fungicide adoption rate.

Shortage of Labor In Landscaping; High Maintenance Cost of Lawn Mowers.

January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.January 2023: Quintect 105 SC is a fungicide introduced by FMC for Indonesian farmers to provide protection and secure the quality and quantity of their crops.July 2022: FMC launched the fungicide Flint Pro 64.8 WG, which controls diseases including Alternaria dry spot on potato plants as well as leaf spot disease and stem rot in watermelon plants.

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Indonesia Fungicide Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Indonesia Fungicide Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.