1. What are the major growth drivers for the Spritzer Market market?

Factors such as are projected to boost the Spritzer Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

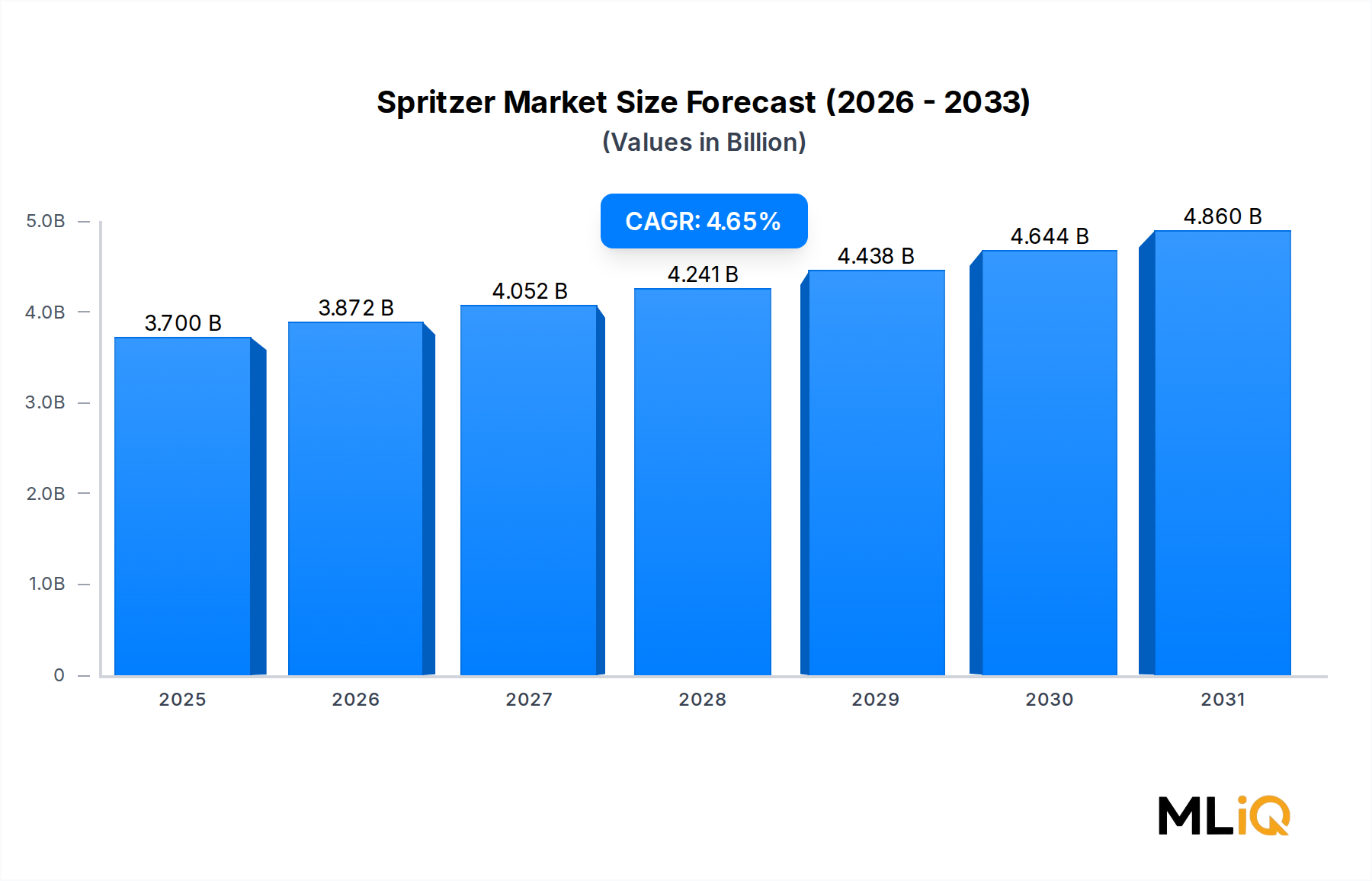

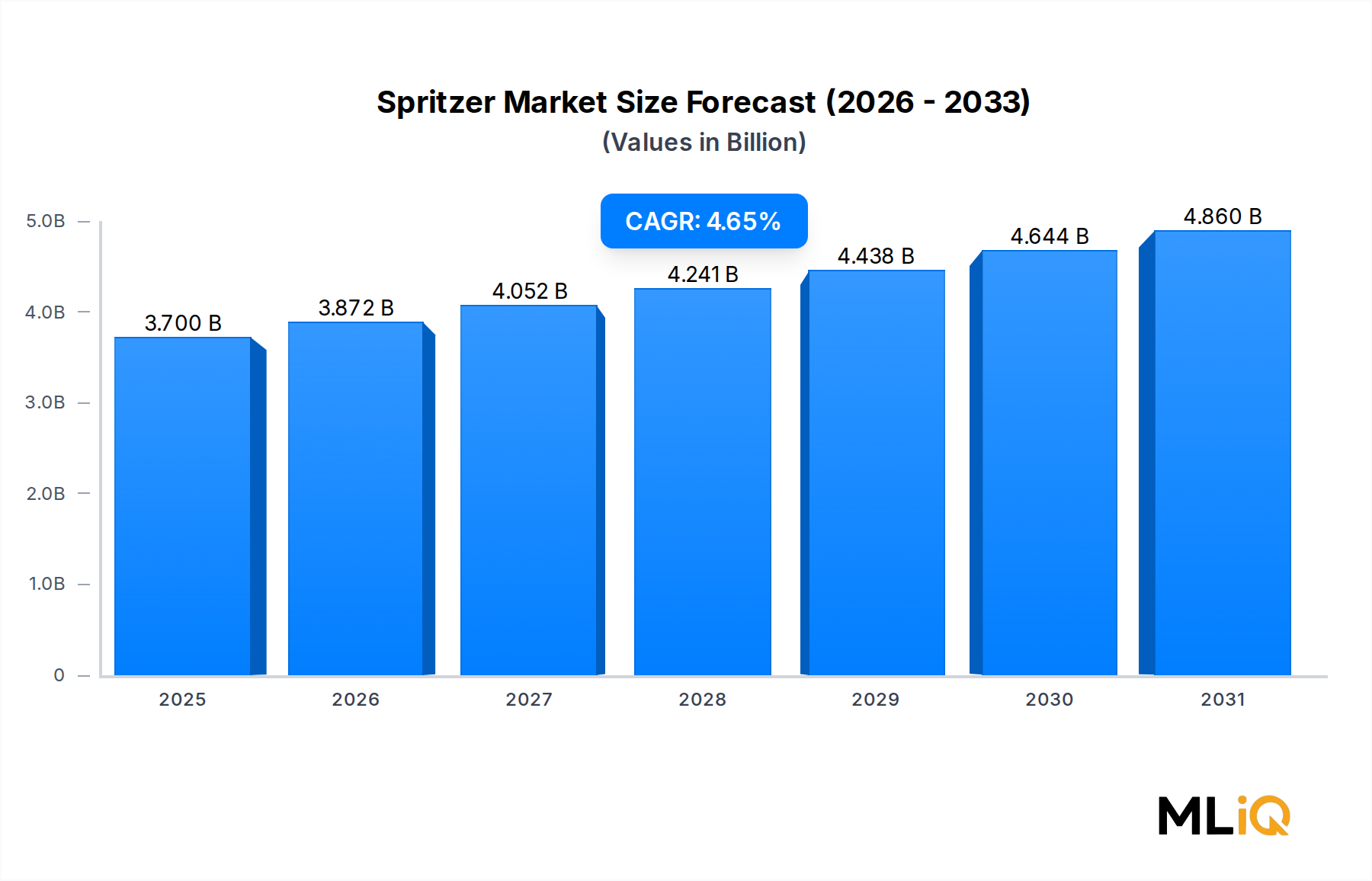

The global spritzer market is valued at $3.7 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 4.65% through the forecast period, driven by shifting consumer preferences toward lighter, lower-alcohol alternatives and the rapid premiumization of ready-to-drink beverage categories. As health-conscious consumption patterns become entrenched across demographics, spritzers—traditionally blends of wine and sparkling water or carbonated mixers—are gaining significant commercial traction beyond their European origins.

Key demand drivers include the mainstreaming of moderation-oriented drinking cultures, particularly among millennials and Gen Z consumers who seek social beverages with lower caloric and alcohol footprints. The proliferation of on-premise and off-premise distribution channels, including e-commerce platforms and specialty retail, has further democratized access to premium spritzer SKUs. Additionally, the alignment of spritzers with broader wellness trends—such as organic sourcing, natural flavor infusions, and low-sugar formulations—continues to attract investment from both established wine conglomerates and emerging beverage startups.

Macroeconomic tailwinds reinforcing growth include the expansion of the middle class in Asia Pacific and Latin American markets, where aspirational consumption of Western-style alcoholic beverages is rising. In parallel, favorable regulatory environments in several jurisdictions are easing the path for new market entrants to distribute flavored, low-ABV beverages through mainstream retail and digital channels.

The competitive landscape is fragmenting, with regional craft producers carving out meaningful share alongside multinational wine brands that have invested heavily in canned spritzer lines. Innovation in packaging—particularly slim-can and single-serve formats—is proving to be a decisive commercial lever, enabling impulse purchasing and outdoor consumption occasions that previously fell outside the category's reach.

Looking ahead, the spritzer market is well-positioned to benefit from continued crossover with adjacent categories. The convergence of the Hard Seltzer Market and wine-based RTD formats is blurring traditional category boundaries and creating hybrid SKUs that appeal to broader consumer cohorts. Simultaneously, growth in digital-first direct-to-consumer models is enabling smaller producers to achieve national and international scale without traditional distributor dependency. By the end of the forecast period, the market is expected to demonstrate robust volume gains across all key geographies, with particular acceleration in Asia Pacific and the Middle East, where premiumization is still in early stages.

Within the spritzer market's segmentation by nature, the organic sub-segment has emerged as the dominant revenue-generating category, commanding a disproportionately large share relative to its overall volume. This dominance is anchored in the intersection of two powerful market forces: the accelerating consumer preference for clean-label, sustainably produced beverages, and the willingness of premium-segment buyers to absorb higher price points for certified organic products.

Organic spritzers are typically produced using grapes or base wines sourced from certified organic vineyards, eliminating synthetic pesticides, herbicides, and chemical fertilizers from the supply chain. This production methodology resonates strongly with health-conscious consumers across North America, Western Europe, and increasingly in Australia and Japan—markets where organic food and beverage certifications carry significant purchase influence. Regulatory frameworks in the European Union and the United States have established clear certification pathways for organic wine-based beverages, providing brand owners with credible third-party validation that translates into shelf differentiation and consumer trust.

Key players driving organic segment growth include Hoxie Spritzer, which has built its entire brand identity around organic wine bases and natural botanical infusions, and Union Wine Company, which emphasizes sustainable vineyard sourcing and low-intervention winemaking as core brand pillars. The Grand Canyon Wine Co. has also made organic positioning a central element of its product narrative, targeting outdoor and adventure-oriented consumer demographics who place a premium on environmental responsibility.

The organic segment's share within the total spritzer market is not merely holding steady—it is actively expanding. Market data indicates that organic SKUs are gaining shelf space at the expense of conventional equivalents in premium retail formats, specialty grocery chains, and online platforms. Retailers such as Whole Foods Market, specialty wine shops, and health-oriented e-commerce platforms are disproportionately stocking organic spritzer lines, further reinforcing a virtuous cycle of visibility and trial.

Pricing dynamics within the organic segment are particularly favorable. Organic spritzers command price premiums ranging from 15% to 35% above conventional alternatives, depending on the market and format. This pricing power is sustainable because consumers in the target demographic exhibit relatively low price sensitivity for products that align with their wellness and sustainability values. As a result, organic spritzer lines deliver superior margin profiles for producers, incentivizing further investment in product development and marketing within this sub-segment.

Distribution channel alignment further reinforces the organic segment's dominance. Specialty stores and online platforms—both high-growth distribution vectors—are disproportionately oriented toward organic and natural product categories. This structural alignment means that as these channels gain share against traditional hypermarkets and supermarkets, the organic segment captures an outsized portion of incremental volume growth.

The conventional sub-segment retains scale advantages in volume terms, particularly in price-sensitive markets and mass-market retail environments. However, its revenue share trajectory is under pressure as consumer premiumization trends continue to favor organic alternatives. Producers operating primarily in the conventional tier are responding by introducing organic line extensions to protect revenue share rather than cede premium positioning entirely to specialist brands.

In aggregate, the organic nature segment is the clearest example of premiumization at work within the spritzer market, combining favorable margin economics, strong consumer tailwinds, and aligned distribution dynamics to sustain its leadership position through the forecast horizon.

The spritzer market's 4.65% CAGR trajectory is underpinned by a set of quantifiable drivers that create durable demand across geographies and demographic cohorts, while a parallel set of structural constraints introduces friction that producers must actively manage.

The primary growth driver is the documented shift toward low-ABV and moderate consumption behaviors. Surveys conducted across the United States, United Kingdom, and Germany consistently report that more than 40% of millennial and Gen Z respondents actively seek to reduce alcohol intake, creating a natural demand pull for beverages that deliver social occasion functionality at lower intoxication risk. Spritzers, typically ranging from 4% to 8% ABV, occupy an ideal positioning within this framework.

Health and wellness macro trends constitute a second driver of measurable impact. The global functional beverage sector—which increasingly overlaps with the Functional Beverage Market—is projected to sustain growth well above GDP rates in most developed economies. Spritzer producers that incorporate botanical extracts, natural fruit flavors, and low-sugar formulations are capturing crossover purchase intent from consumers who might otherwise gravitate toward kombucha or infused water alternatives.

Premiumization of the Alcoholic Beverages Market is a third structural driver. As consumers trade up from mass-market beer and spirits toward wine-based and craft-positioned RTD formats, spritzers benefit directly. The average unit selling price of premium canned spritzers has increased by approximately 12% to 18% over the past three years in North American retail, indicating genuine pricing power rather than volume-driven growth alone.

On the constraint side, raw material cost volatility presents a meaningful headwind. Wine base costs are subject to vintage variability, and disruptions from climate-related events—such as the frost damage to European vineyards in recent growing seasons—create input cost uncertainty that compresses margins for producers without diversified sourcing strategies.

Regulatory heterogeneity across markets is a further constraint. Alcohol classification rules, labeling requirements, and distribution licensing frameworks differ substantially across the United States, European Union, and Asia Pacific jurisdictions, increasing compliance costs for brands pursuing international scale.

Finally, category competition from the Sparkling Water Market and the Hard Seltzer Market creates substitution pressure, particularly in the on-trade channel where bartenders and consumers may opt for non-wine-based carbonated alternatives.

The competitive landscape of the spritzer market is characterized by a blend of established wine conglomerates, purpose-built RTD brands, and regional craft producers. The following profiles outline the strategic positioning of key participants:

Porch Pounder: A specialist canned wine and spritzer brand targeting casual outdoor occasions, Porch Pounder differentiates through value pricing and wide-format retail distribution, appealing to volume-oriented buyers in the North American mass market.

The Grand Canyon Wine Co.: Focused on adventure and outdoor lifestyle branding, The Grand Canyon Wine Co. has carved a niche in the premium canned spritzer segment by emphasizing sustainable sourcing and distinctive regional identity.

E. & J. Gallo Winery.: As one of the largest wine producers globally, E. & J. Gallo Winery. brings unmatched distribution infrastructure and brand investment capacity to the spritzer category, leveraging its portfolio breadth to cross-sell spritzer SKUs across retail channels.

Latitude Beverage Co.: Known for its 90+ Cellars and other value-premium wine brands, Latitude Beverage Co. has applied its sourcing expertise to spritzer formats, delivering competitive quality at accessible price points across specialty and mainstream retail.

Independent Liquor (NZ) Ltd.: A significant player in the Asia Pacific region, Independent Liquor (NZ) Ltd. holds strong distribution relationships across Oceania and Southeast Asia, enabling regional spritzer product launches to achieve rapid market penetration.

Union Wine Company: Pioneering the canned wine movement in the United States, Union Wine Company emphasizes organic sourcing and low-intervention production, positioning its spritzer offerings squarely within the premium wellness beverage tier.

Hoxie Spritzer: A digitally native brand built on organic wine bases and botanical flavor profiles, Hoxie Spritzer has achieved strong direct-to-consumer growth and is expanding into specialty retail, targeting health-conscious urban consumers.

Mancan Wine Llc.: Mancan Wine Llc. focuses on canned wine formats designed for convenience and portability, targeting male consumer demographics that have historically been underserved by traditional wine marketing, including spritzer-adjacent products.

Francis Ford Coppola Winery: Leveraging celebrity heritage and premium wine credentials, Francis Ford Coppola Winery has introduced spritzer-format products that command premium shelf positioning and benefit from strong brand equity in both on-premise and off-premise channels.

January 2024: Hoxie Spritzer secured a Series A funding round totaling $8 million, with proceeds earmarked for national retail expansion and new botanical flavor variant development targeting the wellness-oriented consumer segment.

March 2024: Union Wine Company launched a new line of organic spritzers in slim-can format across key US natural grocery retailers, citing consumer demand data showing 28% year-over-year growth in organic RTD wine searches on e-commerce platforms.

June 2024: E. & J. Gallo Winery. announced a strategic partnership with a major national convenience chain to distribute its canned spritzer SKUs across more than 6,000 US store locations, significantly expanding the brand's impulse-purchase footprint.

September 2024: Independent Liquor (NZ) Ltd. filed regulatory approvals for spritzer product distribution across three new Southeast Asian markets, aligning with the company's broader Asia Pacific growth strategy for the 2025–2027 period.

November 2024: Francis Ford Coppola Winery introduced a limited-edition holiday spritzer collection featuring tropical and chocolate flavor profiles, achieving sell-through rates reported at 40% above internal forecasts within the first six weeks of launch.

February 2025: The Grand Canyon Wine Co. announced a co-branding partnership with a leading outdoor apparel brand to develop co-marketed spritzer multi-packs targeting the adventure travel and festival consumption occasions for the 2025 summer season.

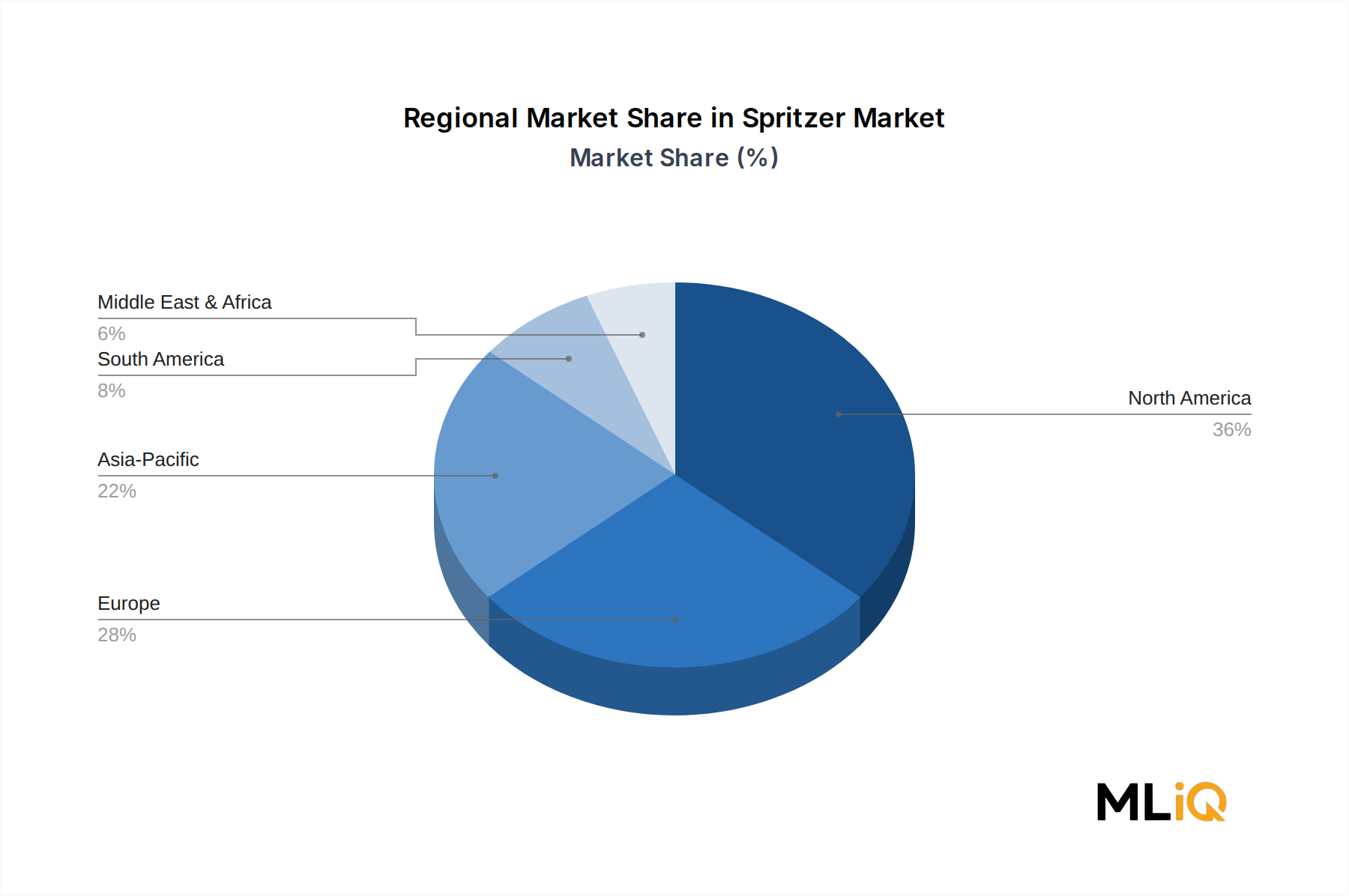

The spritzer market exhibits meaningful geographic heterogeneity, with distinct growth trajectories, maturity profiles, and demand drivers across five primary regions.

North America represents the largest single regional market, accounting for an estimated 38% of global spritzer revenue in 2025. The United States is the dominant contributor, driven by the rapid expansion of the canned wine and RTD beverage segment across mainstream and specialty retail. The regional CAGR is estimated at 4.8%, supported by premiumization trends, growing female and millennial buyer cohorts, and the maturation of direct-to-consumer wine commerce. Canada and Mexico contribute incremental volume, with Canada showing above-average growth in organic and natural product segments.

Europe is the most mature regional market and the historical birthplace of the spritzer category, particularly in Austria, Germany, and the United Kingdom. European consumers exhibit high brand loyalty to established regional producers, and regulatory frameworks for low-ABV wine-based beverages are well-developed. Regional CAGR is estimated at 3.2%, reflecting the market's maturity and high baseline penetration. However, premiumization and format innovation—particularly in single-serve and functional-infused variants—are generating above-average growth in the United Kingdom, France, and Scandinavia.

Asia Pacific is the fastest-growing region in the spritzer market, with a regional CAGR estimated at 7.1%. China, Japan, South Korea, and ASEAN markets are all experiencing accelerated demand for premium Western-style RTD alcoholic beverages. Rising disposable incomes, urbanization, and the influence of social media on beverage discovery are key demand catalysts. The wine-based spritzer format is gaining traction as an entry point for consumers new to wine culture, offering approachable flavor profiles and convenient packaging.

South America, led by Brazil and Argentina, is growing at an estimated CAGR of 4.3%. Argentina's established wine culture provides a natural foundation for domestic spritzer production, while Brazil's large and growing middle class represents a significant addressable market for imported and locally produced premium RTD formats.

The Middle East and Africa region is nascent but showing early-stage momentum, particularly in Israel, South Africa, and the GCC's non-prohibition jurisdictions. Growth is driven by expatriate consumer populations and tourism-related on-premise consumption, with a regional CAGR estimated at 3.8%.

Investment activity in the spritzer market has accelerated notably over the 2023–2025 period, reflecting investor confidence in the long-term durability of the low-ABV and premiumized RTD beverage trend. Venture capital and private equity flows have been particularly concentrated in three sub-segments: organic and wellness-positioned brands, digitally native direct-to-consumer platforms, and packaging innovation-focused producers.

The organic spritzer sub-segment has attracted the highest per-deal valuations, driven by demonstrated revenue growth and strong gross margin profiles. Brands positioned at the intersection of the Ready-to-Drink Cocktail Market and premium wine culture have been especially attractive to consumer-focused growth equity funds, which view the category as a sustainable alternative to the boom-and-bust cycles observed in the Hard Seltzer Market over the preceding cycle.

Strategic M&A has also been active. Large wine conglomerates with existing distribution infrastructure have pursued bolt-on acquisitions of emerging spritzer brands as a faster path to channel presence than organic brand building. This dynamic is consistent with broader consolidation trends observed across the Alcoholic Beverages Market, where scale and distribution efficiency are decisive competitive advantages.

Partnerships between spritzer brands and flavoring technology companies—participants in the Natural Flavors Market—have become a notable deal structure, enabling producers to accelerate new flavor development and differentiate on sensory profile without building in-house R&D infrastructure. These arrangements are typically structured as multi-year supply and co-development agreements rather than equity transactions.

The Wine Cooler Market and Flavored Alcoholic Beverage Market are the adjacent categories from which the most capital reallocation is occurring, as investors shift portfolio exposure from legacy categories toward higher-growth, premium-positioned formats. Spritzers, occupying the premium tier of both adjacencies, are the principal beneficiary of this reallocation trend.

The spritzer market's end-user base is structurally diverse, but three primary

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.65% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Spritzer Market market expansion.

Key companies in the market include Porch Pounder, The Grand Canyon Wine Co., E. & J. Gallo Winery., Latitude Beverage Co., Independent Liquor (NZ) Ltd., Union Wine Company, Hoxie Spritzer, Mancan Wine Llc., Francis Ford Coppola Winery.

The market segments include Nature, Flavor, Distribution Channel.

The market size is estimated to be USD 3.7 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Spritzer Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Spritzer Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.