Germany Fertilizer Market by Application Mode (Fertigation, Foliar, Soil), by Crop Type (Field Crops, Horticultural Crops, Turf & Ornamental), by Type (Complex, Straight), by Form (Conventional, Speciality), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

Updated On : May 28, 2026|Base Year : 2025|Pages : 197

About Market Lens IQ

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

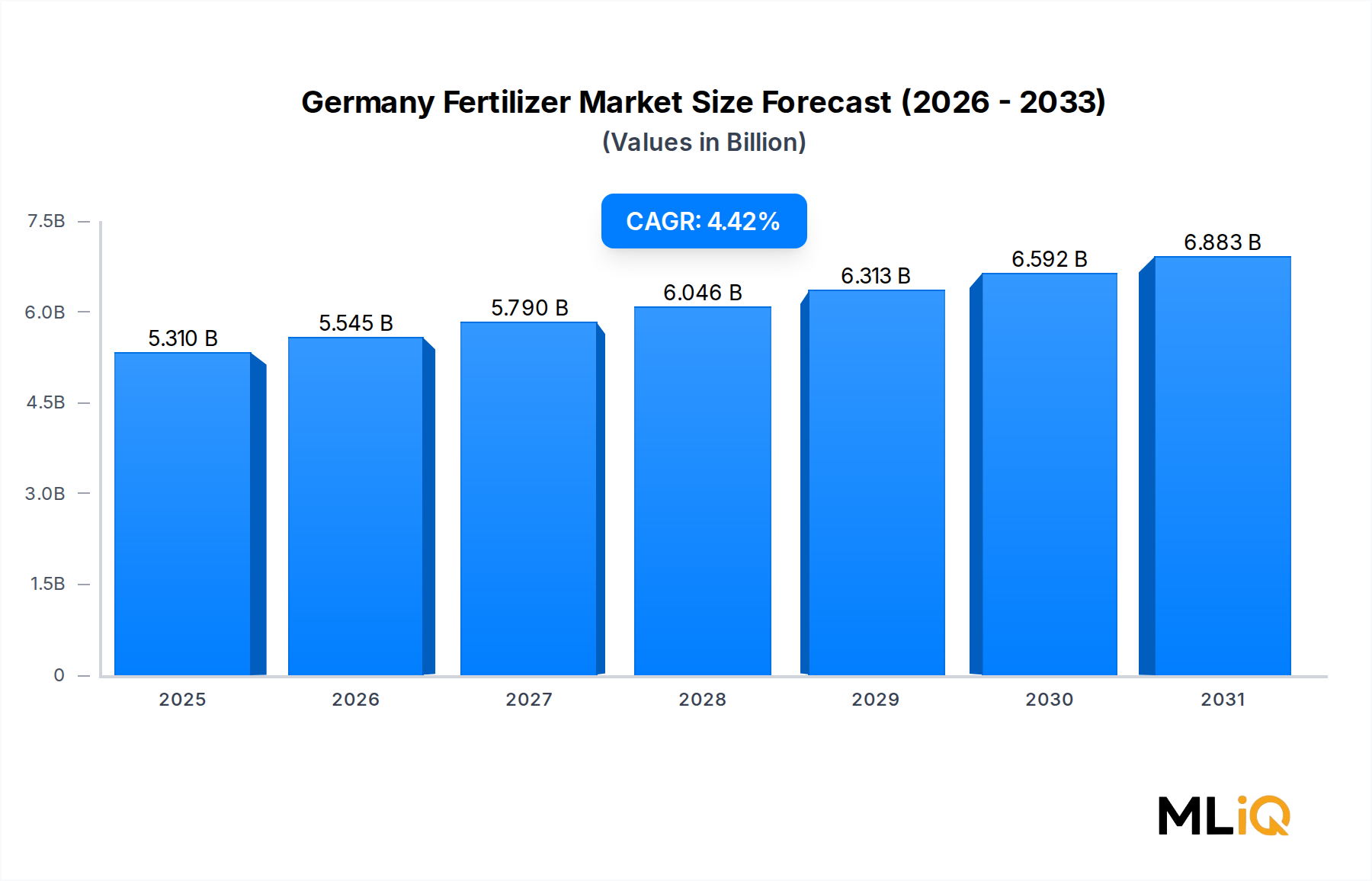

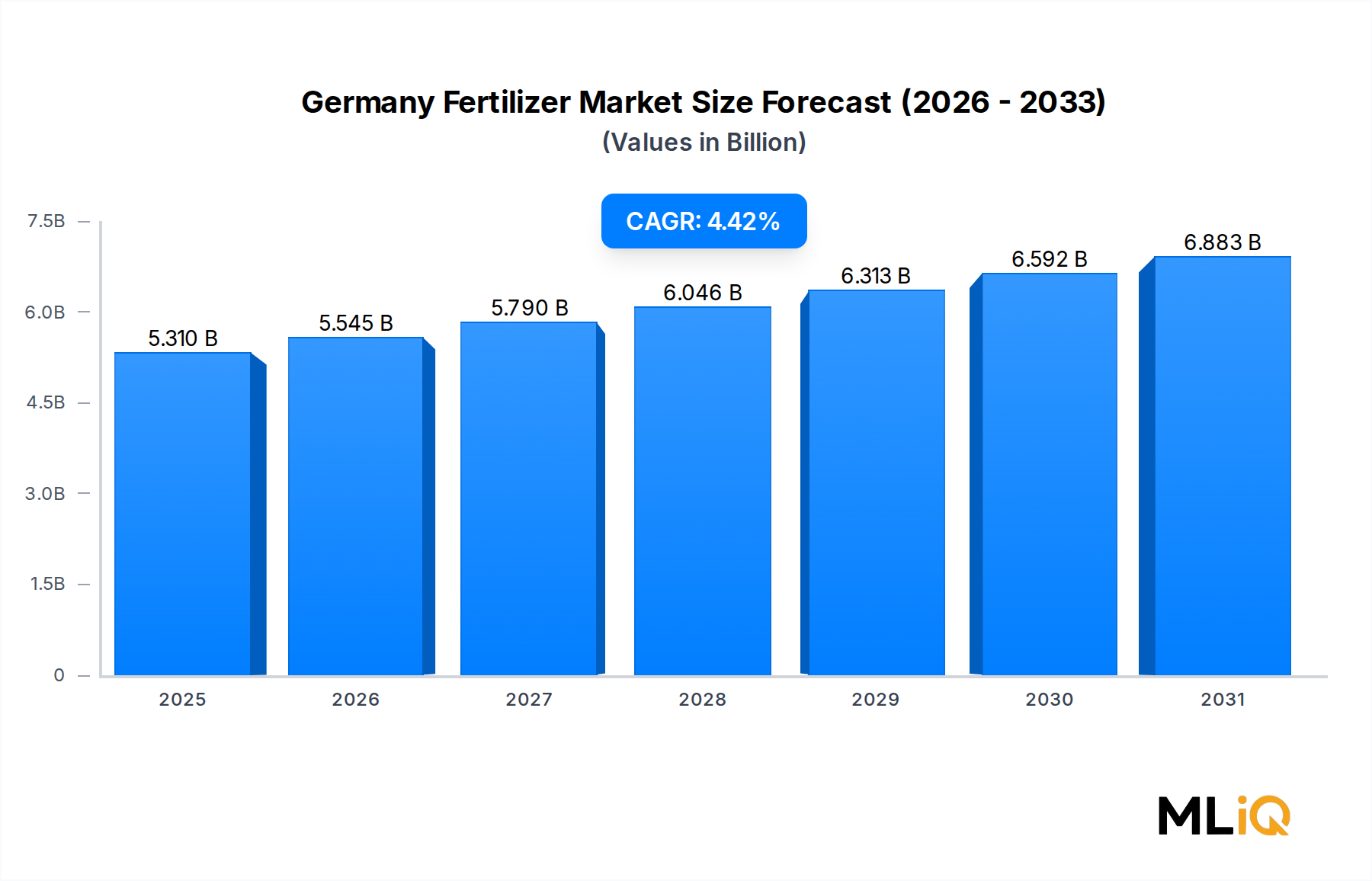

The Germany Fertilizer Market is currently valued at $5.31 billion and is projected to expand at a compound annual growth rate (CAGR) of 4.42% over the forecast period. Germany stands as one of the most significant agricultural economies in Europe, and its fertilizer sector reflects the country's dual commitment to high-yield crop production and increasingly stringent environmental stewardship. The market's growth trajectory is underpinned by the convergence of precision farming adoption, a robust horticultural sector, and ongoing policy-driven transitions toward sustainable nutrient management.

Germany Fertilizer Market Market Size (In Billion)

7.5B

6.0B

4.5B

3.0B

1.5B

0

5.310 B

2025

5.545 B

2026

5.790 B

2027

6.046 B

2028

6.313 B

2029

6.592 B

2030

6.883 B

2031

Key demand drivers include the intensification of greenhouse-based cultivation systems, particularly for high-value vegetables and ornamental crops, and the widespread adoption of fertigation technologies that allow for precise nutrient delivery directly through irrigation infrastructure. Germany's agricultural sector—responsible for cultivating over 16.7 million hectares of land—relies heavily on balanced nutrient programs, creating sustained demand across nitrogen, phosphorus, and potassium product categories.

Germany Fertilizer Market Company Market Share

Loading chart...

Macroeconomic tailwinds shaping this market include the European Union's Farm to Fork Strategy, which targets a 20% reduction in fertilizer use by 2030 while simultaneously pushing for more efficient, specialty-based formulations. This regulatory environment is, paradoxically, accelerating the shift from commodity bulk fertilizers toward higher-margin specialty and complex formulations, thereby supporting revenue growth even as volume metrics face pressure.

The market is further supported by Germany's position as a manufacturing hub for fertilizer inputs, with several globally recognized producers—including K+S Aktiengesellschaft and Yara International AS—maintaining significant production and distribution footprints in the country. This proximity to raw material processing and logistics infrastructure reinforces Germany's role not just as a consumer but as a strategic distribution center for fertilizer products across the broader European region.

Looking forward, the market outlook through 2030 remains constructive. The transition toward specialty formulations, the integration of digital agronomy platforms, and investments in slow-release and controlled-release nutrient technologies are expected to elevate average selling prices and support the overall CAGR of 4.42%. Companies that align their product portfolios with sustainability mandates—particularly those targeting reduced nitrogen runoff and improved nutrient use efficiency—are best positioned to capture incremental market share in this evolving competitive landscape.",

"## Dominant Segment Analysis: Soil Application Mode in the Germany Fertilizer Market

Among the application modes segmented in the Germany Fertilizer Market—fertigation, foliar, and soil—the soil application mode commands the dominant revenue share and represents the foundational channel through which the majority of macronutrients are delivered to German agricultural fields. This dominance is rooted in historical agronomic practice, infrastructure investment, and the scale requirements of Germany's field crop sector, which cultivates cereals, oilseeds, sugar beets, and root vegetables across expansive hectarage.

Soil application methods, which encompass broadcast spreading, incorporation, and banding of granular or liquid fertilizers, are preferred for their logistical scalability and compatibility with existing farm machinery. German farmers operating at scale—particularly in the northern plains regions of Lower Saxony, Mecklenburg-Vorpommern, and Brandenburg—rely on soil application as the primary delivery mechanism for nitrogen, phosphorus, and potassium inputs. The segment is also closely aligned with field crops, which remain the largest crop type sub-segment by cultivated area.

The soil segment's revenue dominance is reinforced by the prevalence of conventional form fertilizers, including granular urea, ammonium nitrate blends, and NPK compounds, which are cost-effectively distributed and applied using precision spreaders. However, the segment is undergoing structural transformation. Germany's Fertilizer Ordinance (Düngeverordnung), last substantially revised in 2020, has imposed tighter restrictions on nitrogen application rates and timing, compelling farmers to optimize application windows and invest in soil testing infrastructure. These regulatory pressures are accelerating the adoption of inhibitor-enhanced formulations—specifically urease and nitrification inhibitors—that improve nitrogen use efficiency while complying with leaching and runoff mandates.

Key players competing within the soil application segment include K+S Aktiengesellschaft, which maintains a vertically integrated model spanning potash mining to retail-ready NPK compounds; Yara International AS, which offers an extensive range of calcium ammonium nitrate and urea-based straight and complex fertilizers optimized for German soil profiles; and EuroChem Group, which has aggressively expanded its European distribution network to capture share in the bulk nitrogen and phosphate segments.

ICL Group Ltd is also a notable participant, leveraging its controlled-release polymer-coated technology platforms to bridge the conventional and specialty sub-segments within soil application. Grupa Azoty S.A. (Compo Expert) has similarly focused on premium NPK granular blends tailored to German soil and crop-specific requirements, particularly for cereal and oilseed rotations.

The soil application segment's share, while still dominant, is consolidating rather than growing at the expense of other modes. Fertigation is gaining traction in the horticultural and protected cultivation sectors, and foliar feeding is increasingly used as a supplemental micronutrient delivery mechanism. Nevertheless, soil application will retain its leading position through the forecast horizon given the structural inertia of field crop agriculture and the capital intensity required to transition to alternative delivery infrastructures. The segment is expected to remain the primary revenue contributor, supported by innovations in formulation chemistry that deliver better agronomic performance per unit of nutrient applied.",

"## Key Market Drivers and Constraints Shaping the Germany Fertilizer Market

The Germany Fertilizer Market is shaped by a well-defined set of demand drivers and structural constraints, each quantifiable and traceable to specific market events or regulatory developments.

On the driver side, the increasing demand for greenhouse-produced tomatoes and other high-value horticultural crops has been a notable catalyst. Germany's protected cultivation area has expanded steadily, with greenhouse vegetable production requiring precise, high-frequency fertigation programs that favor specialty liquid and chelated formulations over conventional bulk products. Tomato cultivation specifically—a crop with intensive calcium, potassium, and magnesium requirements—has driven demand for tailored fertigation solutions that command significant pricing premiums.

The adoption of precision agriculture technologies, including variable-rate application systems and soil sensor networks, has also underpinned market growth. Germany's high farm mechanization rate—with tractor density among the highest in Europe—facilitates the rapid integration of GPS-guided spreaders and drone-based foliar application systems, directly expanding the addressable market for specialty and controlled-release fertilizer products. The Precision Agriculture Market is increasingly intertwined with fertilizer demand patterns, as data-driven nutrient management platforms enable more targeted purchasing decisions.

Government support programs, including EU co-financing under the Common Agricultural Policy (CAP) and Germany's national Agrarinvestitionsförderungsprogramm (AFP), have supported capital investment in modern nutrient management infrastructure, reducing the cost barrier to adopting premium formulations.

On the constraint side, physiological disorders, pest and disease pressures—particularly in horticultural crops—have led to measurable crop losses that reduce net fertilizer pull-through. When yield certainty is impaired, farmers rationally reduce input expenditure, creating demand softness in high-value specialty segments.

Unfavorable climatic conditions, including the increasingly frequent drought periods documented in German agricultural statistics from 2018 to 2022, have disrupted crop development cycles, reducing fertilizer uptake efficiency and causing year-on-year volume volatility. Flooded conditions in northwest Germany have further disrupted application windows, compressing the effective selling season for spring nitrogen products. These climatic variables introduce revenue uncertainty that tempers the underlying growth trend.",

"## Competitive Ecosystem of the Germany Fertilizer Market

The Germany Fertilizer Market features a concentrated competitive landscape dominated by vertically integrated multinationals alongside specialized mid-tier players. The following profiles summarize each competitor's strategic positioning:

AGLUKON Spezialduenger GmbH & Co: A Germany-based specialty fertilizer manufacturer with deep expertise in chelated micronutrients and slow-release formulations tailored to high-value horticultural and professional turf applications. The company maintains strong domestic distribution relationships with agricultural cooperatives and garden center networks.

AGROFERT: A Czech-headquartered conglomerate with significant nitrogen fertilizer manufacturing assets in Central Europe. Following its May 2023 acquisition of Borealis' nitrogen business for approximately $871 million, AGROFERT substantially expanded its production footprint in Austria, Germany, and France, positioning it as a major supplier of nitrogen-based products to German distributors.

EuroChem Group: A globally integrated fertilizer producer with expanding European distribution capabilities. EuroChem competes on cost in the bulk nitrogen and phosphate segments while increasingly targeting the German specialty fertilizer channel through its product range of granular and solution-grade NPK compounds.

Grupa Azoty S A (Compo Expert): Operates the Compo Expert brand as a premium specialty fertilizer division, offering controlled-release, foliar, and fertigation solutions with strong traction in German viticulture, horticulture, and professional landscaping segments.

ICL Group Ltd: A global specialty minerals and fertilizer company competing in the polysulphate, potassium nitrate, and polymer-coated controlled-release segments. ICL's technology differentiation in the Specialty Fertilizer Market provides a competitive moat against commodity-grade competitors.

K+S Aktiengesellschaft: Germany's most prominent domestically headquartered fertilizer producer, with vertically integrated potash and salt mining operations. K+S expanded its global reach via the April 2023 acquisition of a 75% stake in Industrial Commodities Holdings' fertilizer business in South Africa, reinforcing its ambition to diversify beyond European markets.

Nouryon: Competes primarily in the chelated micronutrient and specialty crop nutrition segments. The April 2023 acquisition of ADOB, a Polish micronutrient specialist, materially broadened Nouryon's portfolio within the Micronutrient Fertilizer Market and enhanced its presence in the German professional agronomy channel.

PhosAgro Group of Companies: A Russian-origin phosphate and NPK producer with established European distribution channels. PhosAgro positions on price competitiveness in the phosphate and complex fertilizer segments, though geopolitical dynamics post-2022 have introduced supply reliability considerations for European buyers.

Sociedad Quimica y Minera de Chile SA: Known as SQM, this company competes in the potassium nitrate and specialty potash segments, serving high-value crops and greenhouse operators in Germany through its European distribution network.

Yara International AS: The market's leading nitrogen fertilizer supplier by brand recognition and distribution breadth in Germany. Yara competes across the full product spectrum from bulk calcium ammonium nitrate to premium digital agronomy-linked solutions, and its YaraVita micronutrient range has significant penetration in German arable and horticultural segments.",

"## Recent Developments & Milestones in the Germany Fertilizer Market

May 2023: AGROFERT completed the acquisition of Borealis' nitrogen business unit—encompassing fertilizers, melamine, and technical nitrogen products—for approximately $871 million. The transaction integrated Borealis production sites in Austria, Germany, and France into AGROFERT's operational network, along with a pan-European sales and distribution infrastructure, significantly elevating AGROFERT's competitive standing in the German fertilizer supply chain.

April 2023: K+S Aktiengesellschaft finalized the acquisition of a 75% equity stake in the fertilizer trading business of Industrial Commodities Holdings (Pty) Ltd (ICH), a South African trading company. The newly established joint venture, to operate under the FertiV Pty Ltd brand, extends K+S's market reach into southern and eastern Africa while reinforcing the company's diversification strategy beyond its core European potash business.

April 2023: Nouryon announced the completed acquisition of ADOB, a Poland-headquartered specialist in chelating micronutrients, foliar crop nutrition, and specialty farming solutions. The acquisition directly expanded Nouryon's innovative crop nutrition portfolio and strengthened its distribution capabilities within the European specialty fertilizer channel, with particular relevance to German precision agriculture customers.

2020: Germany implemented the revised Fertilizer Ordinance (Düngeverordnung), introducing stricter nitrogen application caps, mandatory soil testing requirements, and extended buffer zones near water bodies. This regulatory milestone has had a lasting structural impact on product mix dynamics, accelerating the transition from bulk nitrogen toward enhanced-efficiency and controlled-release formulations across the German market.",

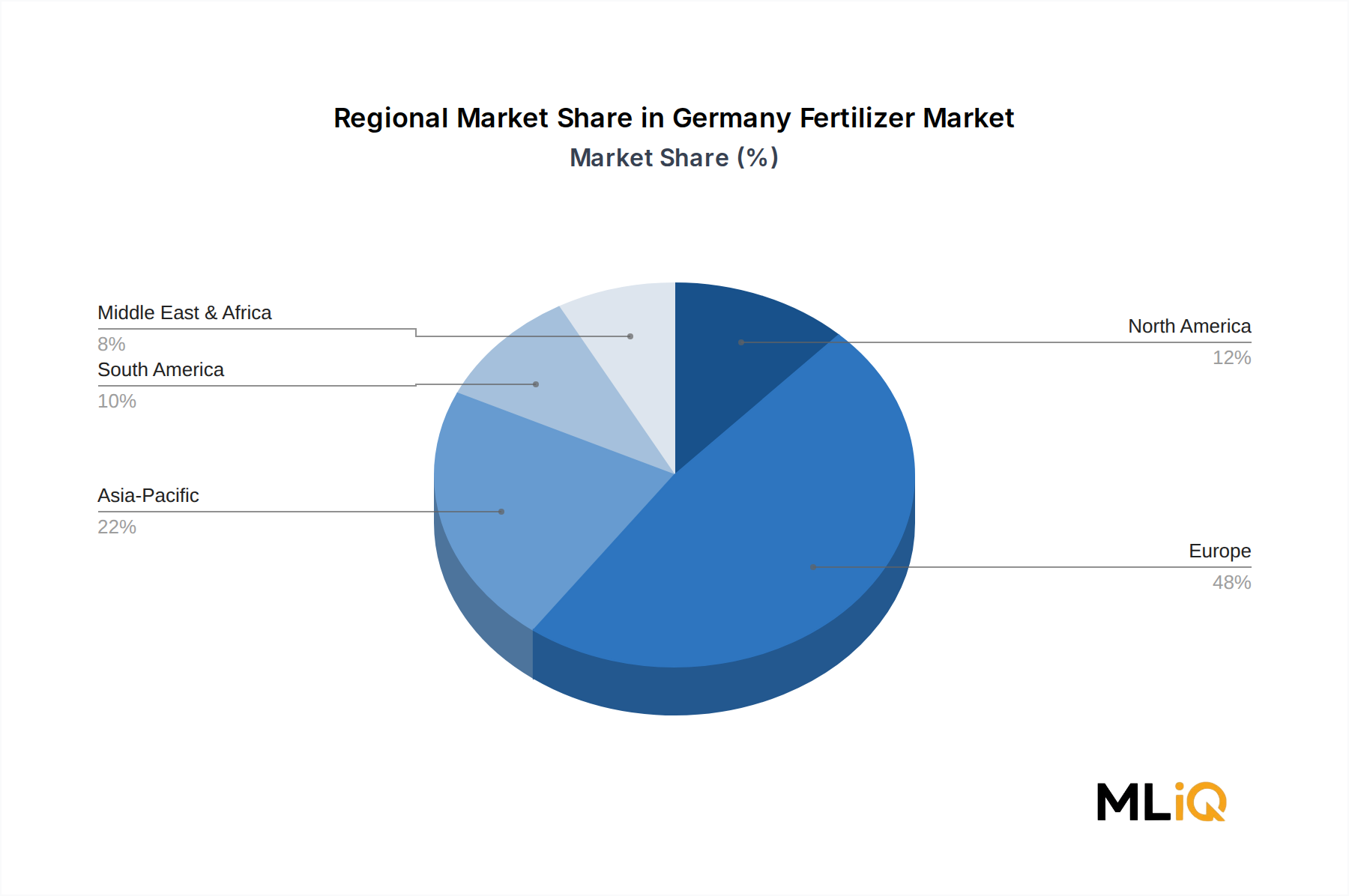

"## Regional Market Breakdown for the Germany Fertilizer Market

While the Germany Fertilizer Market is defined by its national boundaries, understanding Germany's positioning within the broader European and global fertilizer context—and the intra-national regional dynamics—provides critical strategic context for market participants.

Within Europe, Germany is among the top three fertilizer-consuming markets by value, alongside France and Poland. The European fertilizer segment as a whole is experiencing moderate growth, with intra-regional demand supported by the transition to specialty and enhanced-efficiency products. Germany's domestic market benefits from its centrality within European supply chains, positioning it as a redistribution hub for Eastern European producers targeting Western European buyers. The European Agrochemicals Market, of which Germany is a leading national component, is navigating the dual pressures of regulatory tightening and agronomic intensification.

North America represents a contrasting growth profile. The United States and Canada are characterized by large-scale commodity fertilizer consumption—particularly anhydrous ammonia and urea—with specialty product penetration growing rapidly in the horticulture and turf segments. The North American market is among the faster-growing globally, supported by precision agriculture investment and expanding row crop acreage.

Asia Pacific is the fastest-growing regional market for fertilizers globally, driven by food security imperatives in China, India, and Southeast Asia. The Crop Nutrition Market in Asia Pacific is expanding at a CAGR significantly above the global average, fueled by government subsidy programs and the expansion of irrigated agriculture. German manufacturers and distributors with export capabilities are actively targeting this region for volume growth.

South America, particularly Brazil and Argentina, represents a high-growth, high-volume fertilizer market anchored by soybean, corn, and sugarcane production. The Potash Market is particularly active in Brazil, where soil potassium deficiency is widespread and import dependency on Canadian and Belarusian producers remains structurally significant. K+S's expansion into southern Africa signals awareness of these emerging market dynamics.

The Middle East and Africa region is the most nascent in terms of current fertilizer market maturity, but represents significant forward growth potential given population growth trajectories, arable land availability, and increasing government investment in agricultural productivity. South Africa's fertilizer distribution sector—now partially served by K+S's newly established joint venture—exemplifies the incremental market development underway in this region.

Germany itself, as the primary market of focus, demonstrates the characteristics of a mature, high-value market: stable volume with upward price pressure driven by premiumization, regulatory-driven product mix shifts, and digital agronomy integration.",

"## Supply Chain & Raw Material Dynamics for the Germany Fertilizer Market

The Germany Fertilizer Market is critically dependent on a complex upstream supply chain that spans natural gas extraction, potash mining, phosphate rock processing, and sulfur production. Each of these raw material categories carries distinct price volatility and supply concentration risks that have materially affected market stability in recent years.

Natural gas is the primary feedstock for nitrogen fertilizer manufacturing, accounting for approximately 70–80% of the production cost of ammonia—the foundational nitrogen compound from which urea, ammonium nitrate, and calcium ammonium nitrate are derived. Germany's fertilizer industry was severely disrupted following the 2022 energy crisis triggered by the Russia-Ukraine conflict, which caused European natural gas prices to spike to unprecedented levels. Several European nitrogen fertilizer plants—including facilities supplying the German market—curtailed or halted production entirely, forcing increased reliance on imported nitrogen products and driving spot price volatility. The Nitrogen Fertilizer Market faced acute supply pressure during this period, with CAN and urea prices reaching multi-decade highs.

Potash supply chains are more geographically concentrated, with Belarus and Russia historically accounting for approximately 40% of global exports. Sanctions and trade disruptions following 2022 created supply gaps that elevated European potash prices and redirected German buyers toward Canadian (Nutrien, Mosaic) and German domestic sources via K+S, which operates the world's

Germany Fertilizer Market Segmentation

1. Application Mode

1.1. Fertigation

1.2. Foliar

1.3. Soil

2. Crop Type

2.1. Field Crops

2.2. Horticultural Crops

2.3. Turf & Ornamental

3. Type

3.1. Complex

3.2. Straight

4. Form

4.1. Conventional

4.2. Speciality

Germany Fertilizer Market Regional Market Share

Loading chart...

Germany Fertilizer Market Segmentation By Geography

1. North America

1.1. United States

1.2. Canada

1.3. Mexico

2. South America

2.1. Brazil

2.2. Argentina

2.3. Rest of South America

3. Europe

3.1. United Kingdom

3.2. Germany

3.3. France

3.4. Italy

3.5. Spain

3.6. Russia

3.7. Benelux

3.8. Nordics

3.9. Rest of Europe

4. Middle East & Africa

4.1. Turkey

4.2. Israel

4.3. GCC

4.4. North Africa

4.5. South Africa

4.6. Rest of Middle East & Africa

5. Asia Pacific

5.1. China

5.2. India

5.3. Japan

5.4. South Korea

5.5. ASEAN

5.6. Oceania

5.7. Rest of Asia Pacific

Germany Fertilizer Market Regional Market Share

Higher Coverage

Lower Coverage

No Coverage

Germany Fertilizer Market REPORT HIGHLIGHTS

Aspects

Details

Study Period

2020-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2020-2025

Growth Rate

CAGR of 4.42% from 2020-2034

Segmentation

By Application Mode

Fertigation

Foliar

Soil

By Crop Type

Field Crops

Horticultural Crops

Turf & Ornamental

By Type

Complex

Straight

By Form

Conventional

Speciality

By Geography

North America

United States

Canada

Mexico

South America

Brazil

Argentina

Rest of South America

Europe

United Kingdom

Germany

France

Italy

Spain

Russia

Benelux

Nordics

Rest of Europe

Middle East & Africa

Turkey

Israel

GCC

North Africa

South Africa

Rest of Middle East & Africa

Asia Pacific

China

India

Japan

South Korea

ASEAN

Oceania

Rest of Asia Pacific

Table of Contents

1. Introduction

1.1. Research Scope

1.2. Market Segmentation

1.3. Research Objective

1.4. Definitions and Assumptions

2. Executive Summary

2.1. Market Snapshot

3. Market Dynamics

3.1. Market Drivers

3.2. Market Challenges

3.3. Market Trends

3.4. Market Opportunity

4. Market Factor Analysis

4.1. Porters Five Forces

4.1.1. Bargaining Power of Suppliers

4.1.2. Bargaining Power of Buyers

4.1.3. Threat of New Entrants

4.1.4. Threat of Substitutes

4.1.5. Competitive Rivalry

4.2. PESTEL analysis

4.3. BCG Analysis

4.3.1. Stars (High Growth, High Market Share)

4.3.2. Cash Cows (Low Growth, High Market Share)

4.3.3. Question Mark (High Growth, Low Market Share)

4.3.4. Dogs (Low Growth, Low Market Share)

4.4. Ansoff Matrix Analysis

4.5. Supply Chain Analysis

4.6. Regulatory Landscape

4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

4.8. MIQ Analyst Note

5. Market Analysis, Insights and Forecast, 2021-2033

5.1. Market Analysis, Insights and Forecast - by Application Mode

5.1.1. Fertigation

5.1.2. Foliar

5.1.3. Soil

5.2. Market Analysis, Insights and Forecast - by Crop Type

5.2.1. Field Crops

5.2.2. Horticultural Crops

5.2.3. Turf & Ornamental

5.3. Market Analysis, Insights and Forecast - by Type

5.3.1. Complex

5.3.2. Straight

5.4. Market Analysis, Insights and Forecast - by Form

5.4.1. Conventional

5.4.2. Speciality

5.5. Market Analysis, Insights and Forecast - by Region

5.5.1. North America

5.5.2. South America

5.5.3. Europe

5.5.4. Middle East & Africa

5.5.5. Asia Pacific

6. North America Market Analysis, Insights and Forecast, 2021-2033

6.1. Market Analysis, Insights and Forecast - by Application Mode

6.1.1. Fertigation

6.1.2. Foliar

6.1.3. Soil

6.2. Market Analysis, Insights and Forecast - by Crop Type

6.2.1. Field Crops

6.2.2. Horticultural Crops

6.2.3. Turf & Ornamental

6.3. Market Analysis, Insights and Forecast - by Type

6.3.1. Complex

6.3.2. Straight

6.4. Market Analysis, Insights and Forecast - by Form

6.4.1. Conventional

6.4.2. Speciality

7. South America Market Analysis, Insights and Forecast, 2021-2033

7.1. Market Analysis, Insights and Forecast - by Application Mode

7.1.1. Fertigation

7.1.2. Foliar

7.1.3. Soil

7.2. Market Analysis, Insights and Forecast - by Crop Type

7.2.1. Field Crops

7.2.2. Horticultural Crops

7.2.3. Turf & Ornamental

7.3. Market Analysis, Insights and Forecast - by Type

7.3.1. Complex

7.3.2. Straight

7.4. Market Analysis, Insights and Forecast - by Form

7.4.1. Conventional

7.4.2. Speciality

8. Europe Market Analysis, Insights and Forecast, 2021-2033

8.1. Market Analysis, Insights and Forecast - by Application Mode

8.1.1. Fertigation

8.1.2. Foliar

8.1.3. Soil

8.2. Market Analysis, Insights and Forecast - by Crop Type

8.2.1. Field Crops

8.2.2. Horticultural Crops

8.2.3. Turf & Ornamental

8.3. Market Analysis, Insights and Forecast - by Type

8.3.1. Complex

8.3.2. Straight

8.4. Market Analysis, Insights and Forecast - by Form

8.4.1. Conventional

8.4.2. Speciality

9. Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

9.1. Market Analysis, Insights and Forecast - by Application Mode

9.1.1. Fertigation

9.1.2. Foliar

9.1.3. Soil

9.2. Market Analysis, Insights and Forecast - by Crop Type

9.2.1. Field Crops

9.2.2. Horticultural Crops

9.2.3. Turf & Ornamental

9.3. Market Analysis, Insights and Forecast - by Type

9.3.1. Complex

9.3.2. Straight

9.4. Market Analysis, Insights and Forecast - by Form

9.4.1. Conventional

9.4.2. Speciality

10. Asia Pacific Market Analysis, Insights and Forecast, 2021-2033

10.1. Market Analysis, Insights and Forecast - by Application Mode

10.1.1. Fertigation

10.1.2. Foliar

10.1.3. Soil

10.2. Market Analysis, Insights and Forecast - by Crop Type

10.2.1. Field Crops

10.2.2. Horticultural Crops

10.2.3. Turf & Ornamental

10.3. Market Analysis, Insights and Forecast - by Type

10.3.1. Complex

10.3.2. Straight

10.4. Market Analysis, Insights and Forecast - by Form

Table 48: Revenue billion Forecast, by Crop Type 2020 & 2033

Table 49: Revenue billion Forecast, by Type 2020 & 2033

Table 50: Revenue billion Forecast, by Form 2020 & 2033

Table 51: Revenue billion Forecast, by Country 2020 & 2033

Table 52: Revenue (billion) Forecast, by Application 2020 & 2033

Table 53: Revenue (billion) Forecast, by Application 2020 & 2033

Table 54: Revenue (billion) Forecast, by Application 2020 & 2033

Table 55: Revenue (billion) Forecast, by Application 2020 & 2033

Table 56: Revenue (billion) Forecast, by Application 2020 & 2033

Table 57: Revenue (billion) Forecast, by Application 2020 & 2033

Table 58: Revenue (billion) Forecast, by Application 2020 & 2033

Methodology

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Quality Assurance Framework

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

Multi-source Verification

500+ data sources cross-validated

Expert Review

200+ industry specialists validation

Standards Compliance

NAICS, SIC, ISIC, TRBC standards

Real-Time Monitoring

Continuous market tracking updates

Frequently Asked Questions

1. What are the major growth drivers for the Germany Fertilizer Market market?

Factors such as Increasing Demand for Tomato; Adoption of Greenhouse Technology in Tomato Cultivation; Government support are projected to boost the Germany Fertilizer Market market expansion.

2. Which companies are prominent players in the Germany Fertilizer Market market?

Key companies in the market include AGLUKON Spezialduenger GmbH & Co, AGROFERT, EuroChem Group, Grupa Azoty S A (Compo Expert), ICL Group Ltd, K+S Aktiengesellschaft, Nouryon, PhosAgro Group of Companies, Sociedad Quimica y Minera de Chile SA, Yara International AS.

3. What are the main segments of the Germany Fertilizer Market market?

The market segments include Application Mode, Crop Type, Type, Form.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.31 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Tomato; Adoption of Greenhouse Technology in Tomato Cultivation; Government support.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Increasing Loses due to Physiological Disorder. Pest and Disease; Unfavourable Climatic Condition.

8. Can you provide examples of recent developments in the market?

May 2023: Agrofert acquired Borealis' nitrogen business, including fertilizers, melamine, and technical products, at USD 871 billion. This acquisition will enable AGROFERT to serve its customers in the area of fertilizers and technical nitrogen throughout Europe by integrating Borealis production facilities in Austria, Germany, and France, as well as a comprehensive sales and distribution network.April 2023: K+S acquired a 75% share of the fertilizer business of a South African trading company, Industrial Commodities Holdings (Pty) Ltd (ICH). In addition to expanding the core business, K+S is strengthening its operations in southern and eastern Africa as a result of this acquisition. The newly acquired fertilizer business in the future is to be operated in a joint venture under the name of FertivPty Ltd.April 2023: ADOB, a major provider of chelating micronutrients, foliar, and other specialty farming solutions based in Poland, has been purchased by Nouryon. Through the acquisition, the company has broadened its innovative crop nutrition portfolio.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in .

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Germany Fertilizer Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Germany Fertilizer Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Germany Fertilizer Market?

To stay informed about further developments, trends, and reports in the Germany Fertilizer Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.