1. What are the major growth drivers for the Kuwait Fish Market market?

Factors such as ; Increasing Food Security Concerns; Inclination Toward a Healthy Lifestyle are projected to boost the Kuwait Fish Market market expansion.

+1 2315155523

Kuwait Fish Market

Kuwait Fish Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

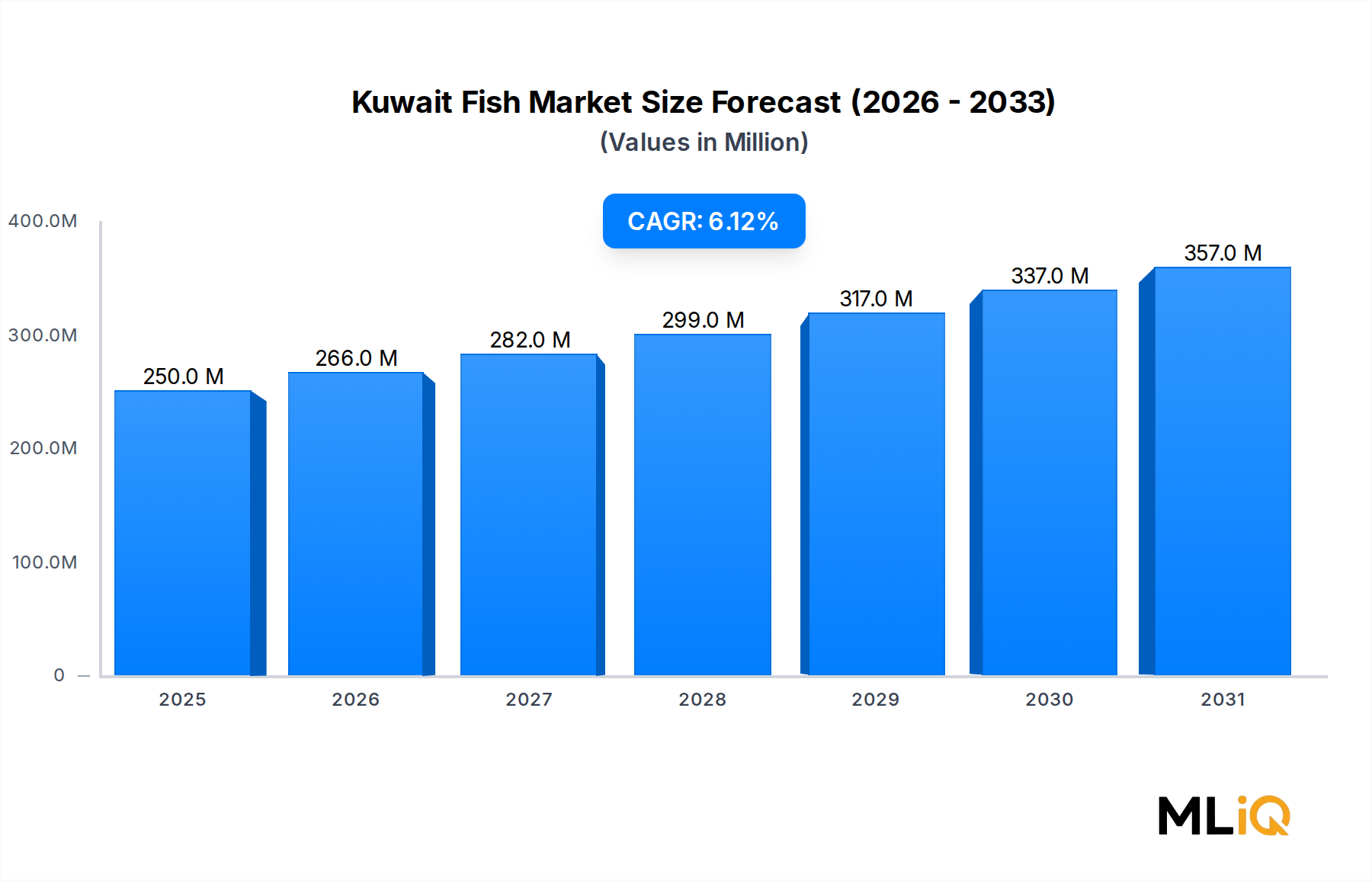

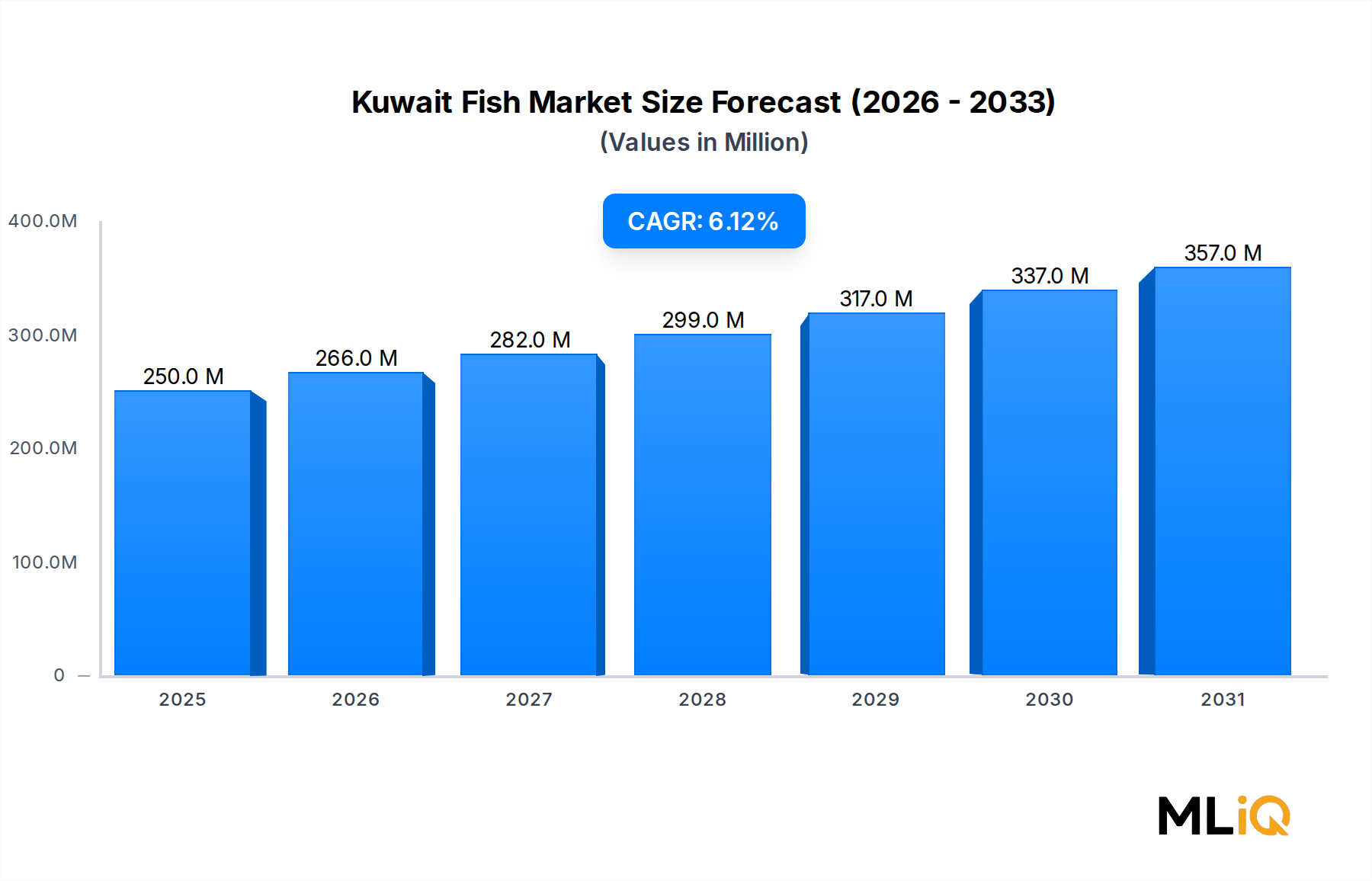

The Kuwait Fish Market is valued at $250.28 million as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 6.12% through the forecast horizon of 2025 to 2033. This sustained growth trajectory positions the market as one of the more dynamic segments within Kuwait's broader food and beverages sector, underpinned by converging macroeconomic, demographic, and lifestyle-driven forces.

Kuwait's strategic location along the Arabian Gulf provides natural access to rich marine ecosystems, supplying a diverse array of fresh water fishes, diadromous fishes, crustaceans, and premium marine species. Fish consumption per capita in Kuwait has risen consistently over the past decade, reflecting a broader regional pivot toward protein-rich, low-fat dietary choices. Government-backed initiatives to bolster domestic food security — in particular the Kuwait Institute for Scientific Research's aquaculture programs — have injected fresh capital and scientific rigor into the supply side of the market, reducing historical dependence on imports.

From a demand-side perspective, the increasing urban population in Kuwait, which exceeds 4.4 million residents including a substantial expatriate community, generates heterogeneous and robust seafood demand. Health-conscious consumers are gravitating toward omega-3-rich marine proteins, a trend that is expected to persist as lifestyle diseases including cardiovascular conditions remain prevalent in the Gulf Cooperation Council (GCC) region. The World Health Organization's recommendation of consuming at least two portions of fish per week is gaining traction among Kuwaiti consumers, providing a durable structural tailwind for market growth.

On the supply side, the emergence of technology-enabled e-commerce platforms is reshaping distribution channels, compressing the farm-to-table supply chain, and making premium seafood varieties accessible to a wider consumer base. The integration of cold chain infrastructure, robotics-based fulfillment, and last-mile delivery logistics is enhancing product freshness and consumer confidence.

Looking ahead through 2033, the Kuwait Fish Market is expected to benefit from regulatory support for sustainable fishing, expansion of aquaculture facilities into desert environments, and increased investment in fish processing infrastructure. The interplay of food security policy mandates, rising health awareness, and e-commerce-driven distribution modernization collectively underpin a bullish medium-to-long-term outlook. Market participants that align with these structural shifts — particularly in sustainable sourcing, digital retail, and value-added processing — are best positioned to capture disproportionate growth.

Within the Kuwait Fish Market, marine fishes constitute the dominant segment by both revenue share and consumer preference, a reflection of Kuwait's deep cultural affinity with Gulf seafood and the country's direct access to the Arabian Sea and Arabian Gulf. The marine fish category — encompassing species such as Zubaidi (silver pomfret), Hamour (grouper), Sobaity (spangled emperor), and Shari (red sea bream) — commands premium pricing and forms the centerpiece of traditional Kuwaiti cuisine.

The dominance of marine fishes is structural rather than cyclical. Kuwait's coastline and territorial waters provide access to native Gulf species that are deeply embedded in the national food culture. Premium native species such as Zubaidi and Hamour are not merely food commodities; they carry cultural and ceremonial significance, ensuring price-inelastic demand even during periods of economic contraction. This cultural moat insulates the segment from competition from cheaper imported alternatives.

From a supply perspective, marine fish sourcing involves a combination of domestic artisanal fishing fleets operating out of ports such as Shuwaikh and Ras Al-Ard, as well as a growing volume of imported marine fish from key suppliers including India, Oman, Iran, and Southeast Asian nations. Domestic catches, while subject to seasonal variation and environmental pressures, continue to supply high-value species that command significant premiums in local fish souqs (markets).

The segment's revenue share is estimated to exceed 45% of total Kuwait Fish Market revenues, reflecting both volume consumption and the relatively high average selling prices of premium marine species. This share has been consolidating rather than growing rapidly, as consumers diversify into crustaceans and diadromous species, but marine fishes retain their primary position.

Key institutional players within this segment include the state-affiliated Kuwait Fisheries Company, private import-export trading houses, and the growing network of organized retail chains such as Lulu Hypermarket and Sultan Center, which have invested in dedicated seafood counters with live tanks and chilled displays. The proliferation of organized retail in Kuwait is gradually eroding the market share of traditional fish souqs, though the latter remain important channels for premium and freshly caught local species.

The Kuwait Institute for Scientific Research (KISR) has also been conducting research into marine fish stock assessment and sustainable harvesting practices, which is critical given that overfishing pressures in the Arabian Gulf have historically constrained domestic supply. KISR's scientific work on marine ecosystem health is increasingly informing regulatory quotas and seasonal restrictions, ensuring long-term supply sustainability for this dominant segment.

Moreover, value-added marine fish products — including marinated fish, portion-cut fillets, and pre-seasoned fish — are gaining traction in Kuwait's retail environment, adding a processing dimension to the segment that is attracting investment from food manufacturing companies. This product diversification is expected to sustain the marine fish segment's revenue dominance through 2033, even as per-unit volumes may face ceiling effects from sustainable harvest limits.

The Kuwait Fish Market is propelled by a set of quantifiable drivers while simultaneously facing meaningful structural constraints that shape the pace and pattern of growth.

Increasing food security concerns represent the primary institutional driver. Kuwait imports approximately 90% of its food requirements, an exposure that has been highlighted by global supply chain disruptions during 2020–2022. In response, the government has elevated aquaculture and domestic food production to strategic national priorities. KISR's 2022 white leg shrimp farming project exemplifies this policy direction, aiming to reduce import dependency while boosting domestic seafood availability. Government capital allocation toward desert aquaculture and marine farming directly increases productive capacity within the market.

Inclination toward healthy lifestyles constitutes the second major driver. Kuwait's non-communicable disease burden — with obesity rates exceeding 37% and diabetes prevalence surpassing 23% among adults according to Gulf Health Council data — is prompting a measurable dietary shift toward lean proteins. Fish consumption is being actively promoted by healthcare institutions, nutritionists, and government health campaigns. This behavioral shift is quantifiable in rising seafood import volumes, with GCC seafood imports growing at approximately 5.8% annually over the 2018–2023 period.

On the constraint side, unfavorable climatic conditions represent a persistent challenge. Kuwait's extreme temperatures — summer highs exceeding 50°C — impose significant logistical costs on cold chain maintenance, accelerate perishability rates, and limit the viability of open-air fish souqs during peak summer months. These conditions elevate distribution costs and increase post-harvest losses, acting as a structural drag on margin expansion.

Higher market entry costs form the second key constraint. Establishing compliant cold storage, obtaining fishing licenses, and meeting Kuwait Municipality's food safety standards requires capital expenditure that deters smaller operators. Import tariffs and customs procedures add further friction to new entrant economics, concentrating the market among established incumbents.

The competitive landscape of the Kuwait Fish Market is characterized by a mix of state-linked enterprises, organized retail conglomerates, technology-driven e-commerce platforms, and traditional trading houses. Given that the source data does not provide specific URLs for named companies, all entities are rendered as plain text per disclosure standards.

Kuwait Fisheries Company: A state-affiliated enterprise with historical involvement in domestic fish sourcing, processing, and distribution; the company plays a pivotal role in supply-side stabilization and government food security initiatives.

Lulu Hypermarket Kuwait: A major organized retail operator with dedicated seafood sections featuring chilled marine fish, crustaceans, and frozen products; its large store footprint and supply chain scale make it a dominant retail channel for seafood consumers across Kuwait Governorate.

Sultan Center Food Products Company: A well-established Kuwaiti supermarket chain offering diversified fresh and processed seafood; the company has invested in in-store fish counters and is an important distribution partner for imported marine species.

Raha E-Commerce Platform: A technology-driven automated grocery platform launched in Kuwait in March 2022 featuring a chilled warehouse and robotics-based fulfillment; Raha distributes multiple fish varieties as part of a fully integrated last-mile delivery model, representing the vanguard of digital transformation in seafood retail.

Kuwait Institute for Scientific Research (KISR): While primarily a research and policy institution, KISR functions as a competitive force through its aquaculture programs, providing domestic supply alternatives and influencing regulatory frameworks that shape competitive dynamics.

Private Fish Import Trading Houses: A fragmented tier of privately owned trading companies sourcing marine fish and crustaceans from India, Oman, Iran, and Southeast Asia; these entities compete primarily on price and variety, servicing traditional souqs and restaurant trade.

September 2022: Kuwait Institute for Scientific Research (KISR) initiated a white leg shrimp farming project, marking a significant institutional step toward boosting domestic seafood production and food sustainability. The project also includes plans to farm fish in desert areas and improve aquaculture operations across Kuwait, directly addressing the country's high food import dependency.

March 2022: Raha, a technology-driven e-commerce platform, officially launched in Kuwait, announcing availability of its application on mobile devices. The platform operates Kuwait's first fully automated robotics fulfillment facility, which includes a chilled warehouse — one of the first of its kind globally. Raha incorporated multiple fish varieties into its product assortment as part of its end-to-end logistical cycle covering sourcing, storage, and last-mile delivery, fundamentally altering consumer access to fresh seafood.

2022–2023: Kuwait Municipality intensified enforcement of food safety and traceability standards for imported seafood, leading to increased compliance costs for importers but improving overall consumer confidence in fish product quality and freshness at organized retail outlets.

2023–2024: Regional aquaculture investment in the GCC accelerated, with Kuwait aligning its national aquaculture strategy to broader Gulf food security frameworks, attracting private sector co-investment into marine and freshwater fish farming infrastructure.

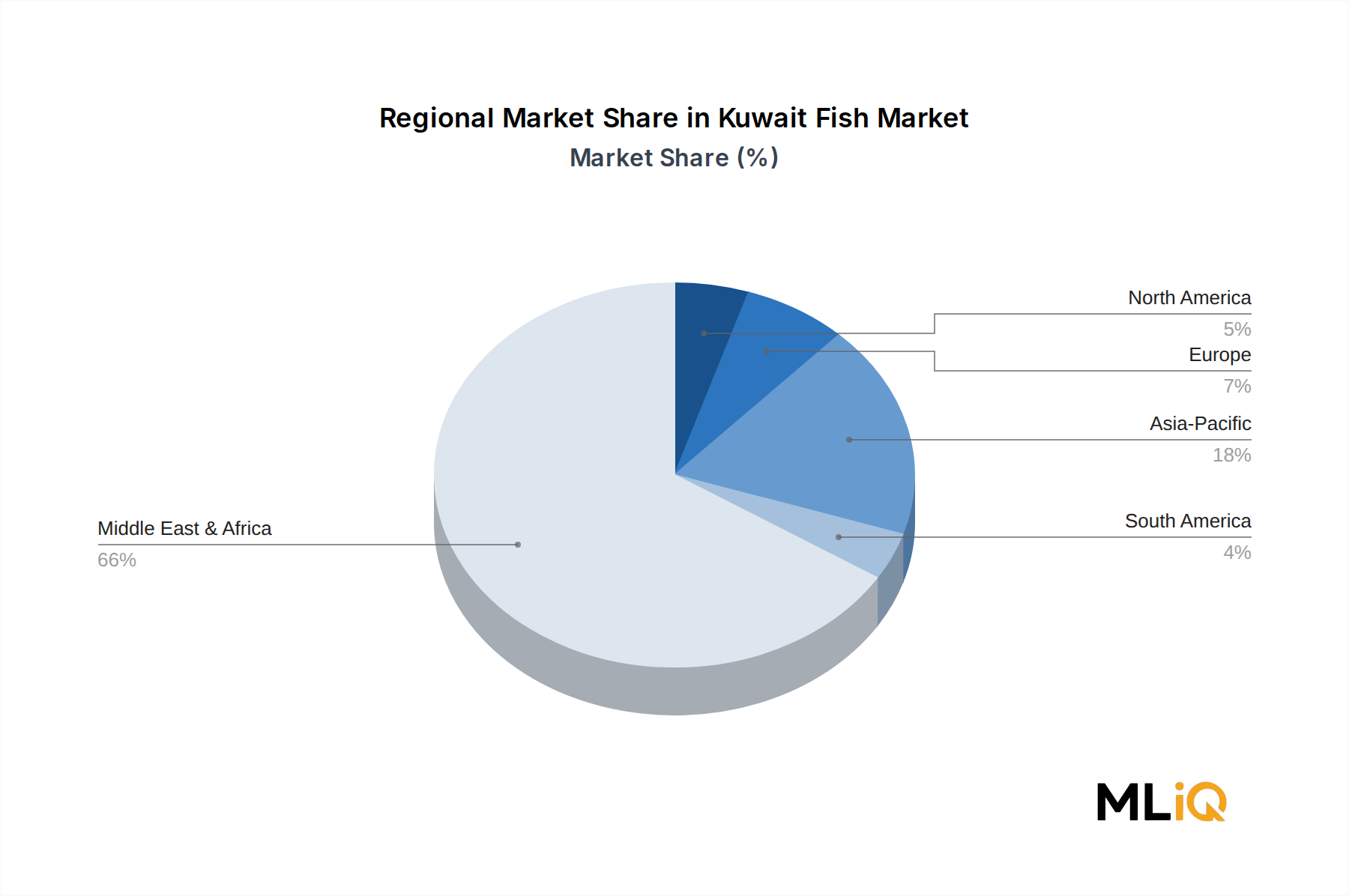

Although the Kuwait Fish Market is a single-country market, its supply chain, trade flows, and competitive dynamics are deeply embedded within a multi-regional global framework. Mapping regional dynamics is therefore essential to understanding sourcing, pricing, and growth vectors.

The Middle East & Africa region, of which Kuwait is a core constituent through the GCC grouping, represents the most immediate demand and competitive environment. GCC seafood consumption has been growing at an estimated 5.5–6.0% annually, with Kuwait tracking at the upper end of this range at 6.12% CAGR. The primary demand driver in this region is population growth combined with rising health consciousness and expanding organized retail penetration. Kuwait accounts for a meaningful sub-share of GCC seafood trade volume due to its elevated per capita income and consumer purchasing power.

Asia Pacific is the most critical supply region for the Kuwait Fish Market. Countries including India, Vietnam, Indonesia, Thailand, and China supply the majority of Kuwait's imported fish and crustacean volumes. India alone accounts for a significant share of frozen and chilled fish exports to Kuwait, with shrimp and pomfret being leading export species. The Asia Pacific Seafood Market and related processing industries are mature, operating at high volume with competitive pricing that sustains Kuwait's import model.

North America and Europe are relatively minor direct trade partners for Kuwait seafood but are influential in setting quality and sustainability standards — notably the Marine Stewardship Council (MSC) certifications — that are increasingly required by Kuwait's organized retail channels.

South America, particularly through Ecuadorian shrimp exports, has grown as a supplementary supply corridor for Kuwait's Shrimp Market demand, diversifying sourcing away from single-region dependency and providing price competition that benefits Kuwaiti importers and end consumers.

The fastest-growing regional supply corridor for Kuwait is South and Southeast Asia, driven by expanding aquaculture capacity and competitive logistics. The most mature supply relationship remains with neighboring GCC states and the broader Middle East, where intra-regional fish trade — particularly from Oman and Iran — has historically supplied fresh Gulf species to Kuwaiti fish souqs.

The Kuwait Fish Market is structurally import-dependent, with domestic production satisfying only a fraction of total consumption. This trade dependency creates specific vulnerability to global tariff regimes, freight cost fluctuations, and bilateral trade policy shifts.

Major import corridors include: India (frozen pomfret, shrimp, mackerel), Oman (fresh Gulf species via land/sea routes), Iran (historical but politically constrained supply of Gulf fish), Indonesia and Vietnam (processed and frozen fish products), and Ecuador (frozen shrimp). India ranks as the single largest supplier by volume, leveraging its extensive seafood processing industry and competitive aquaculture base.

Kuwait applies a standard GCC Unified Customs Tariff of 5% on most fish and seafood imports, with exemptions for select species critical to food security. Non-tariff barriers are a more significant constraint, including Kuwait Municipality's stringent halal certification requirements, phytosanitary inspections, and cold chain compliance mandates for all imported seafood. These compliance requirements add an estimated 3–7% to effective import costs for new-entrant suppliers unfamiliar with Kuwait's regulatory framework.

The broader Seafood Market trade flows are also influenced by sustainability certifications. Kuwaiti organized retailers are increasingly demanding MSC or Aquaculture Stewardship Council (ASC) certifications from suppliers, which effectively creates a non-tariff quality barrier that favors established, certified exporters from Europe and North America over smaller Asian suppliers.

Recent freight cost volatility — the Red Sea disruption of 2023–2024 that forced rerouting of Asian cargo shipments around the Cape of Good Hope — temporarily inflated seafood import costs by an estimated 15–25% for certain supply routes, compressing margins for Kuwaiti importers. This episode underscored Kuwait's vulnerability to geopolitical disruptions in key maritime corridors and accelerated interest in developing the domestic Aquaculture Market as a partial import substitution strategy.

Export activity from Kuwait is minimal, limited to re-export of processed or value-added seafood to neighboring GCC markets, and does not materially affect the market's financial profile.

The supply chain architecture of the Kuwait Fish Market is complex, spanning multiple upstream geographies, processing intermediaries, and cold chain logistics networks before reaching end consumers.

Upstream dependencies are centered on two key inputs: wild-caught fish stocks (sourced from the Arabian Gulf and imported marine species) and aquaculture inputs (including fish feed, fingerlings, and water treatment chemicals). The Fish Feed Market is a critical upstream dependency, particularly as Kuwait's aquaculture ambitions expand. Fish feed prices are closely correlated with global fishmeal prices, which have experienced significant volatility — fishmeal prices rose by approximately 30% between 2020 and 2023 due to El Niño-driven reductions in Peruvian anchovy harvests, the primary fishmeal feedstock. This price volatility directly impacts the cost economics of Kuwait's nascent aquaculture sector.

Cold chain infrastructure represents the most capital-intensive and operationally critical component of the Kuwait Fish Market supply chain. Given Kuwait's extreme ambient temperatures, refrigerated transport, cold storage warehousing, and point-of-sale chilled display systems are non-negotiable requirements. The Cold Chain Logistics Market in the GCC has been growing rapidly, but capacity constraints — particularly in specialized seafood cold storage — remain a bottleneck. The development of platforms such as Raha, with its chilled fulfillment warehouse, reflects private sector investment to address this gap.

The Fish Processing Market is a related upstream-midstream node that processes raw catch into consumer-ready formats (fillets, portions, marinated products, frozen blocks). Kuwait currently imports a significant volume of already-processed fish from Asian Fish Processing Market facilities, reducing the need for domestic processing capacity but increasing exposure to supply disruptions at source.

Key raw material price trends affecting the market include: rising packaging costs (

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.12% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as ; Increasing Food Security Concerns; Inclination Toward a Healthy Lifestyle are projected to boost the Kuwait Fish Market market expansion.

Key companies in the market include .

The market segments include Type, Shrimp.

The market size is estimated to be USD 250.28 million as of 2022.

; Increasing Food Security Concerns; Inclination Toward a Healthy Lifestyle.

Growing Consumption of seafood is Driving the market.

; Unfavorable Climatic Conditions; Higher Market Entry Cost.

September 2022: Kuwait Institute for Scientific Research (KISR) has initiated to farm white leg shrimp project as an important step to boost food production, availability, and sustainability and also aims to farm fish in desert areas and improve aquaculture operations.

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Kuwait Fish Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Kuwait Fish Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.