1. What are the major growth drivers for the Portable Projector Market market?

Factors such as are projected to boost the Portable Projector Market market expansion.

+1 2315155523

Portable Projector Market

Portable Projector Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

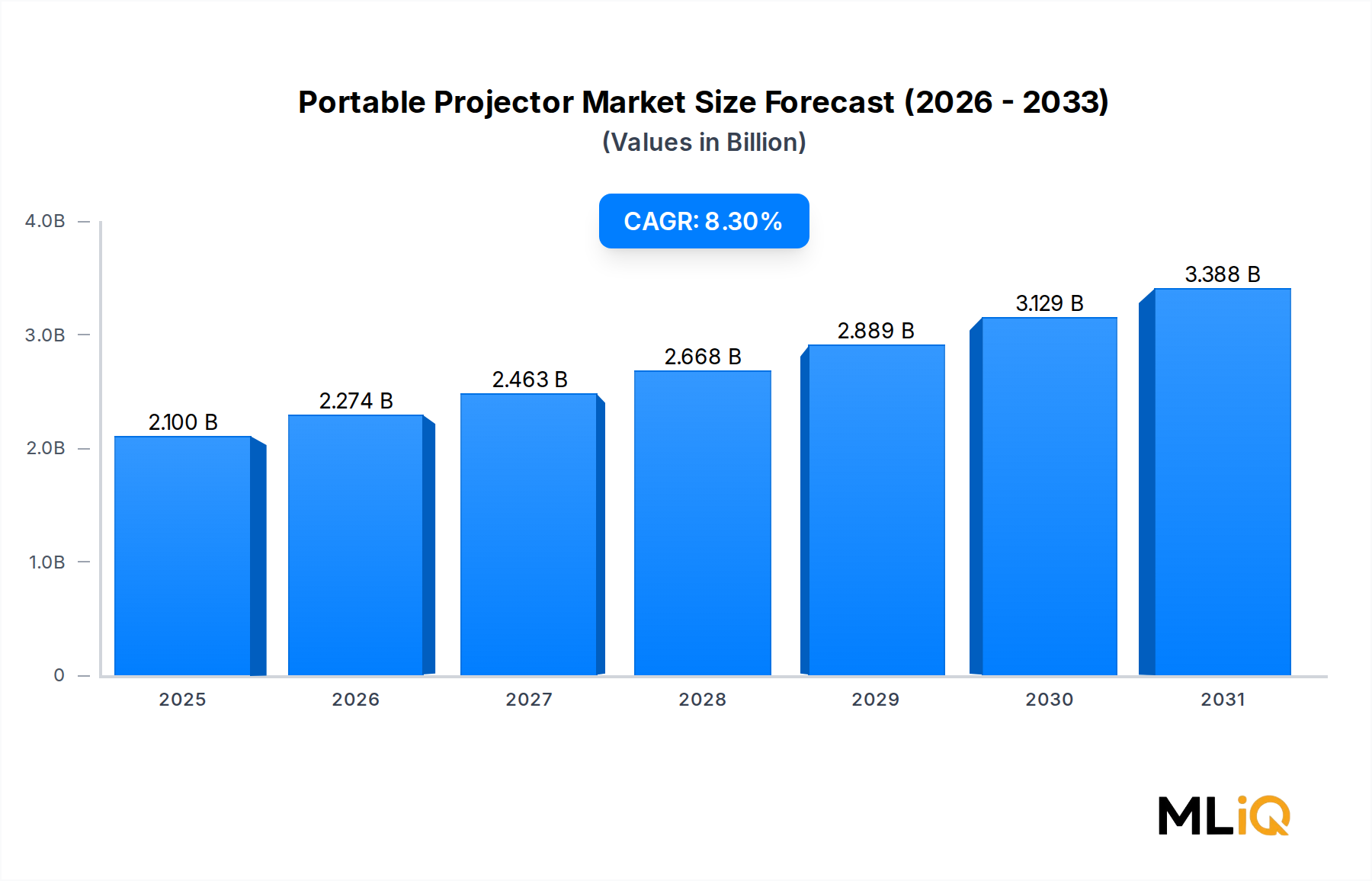

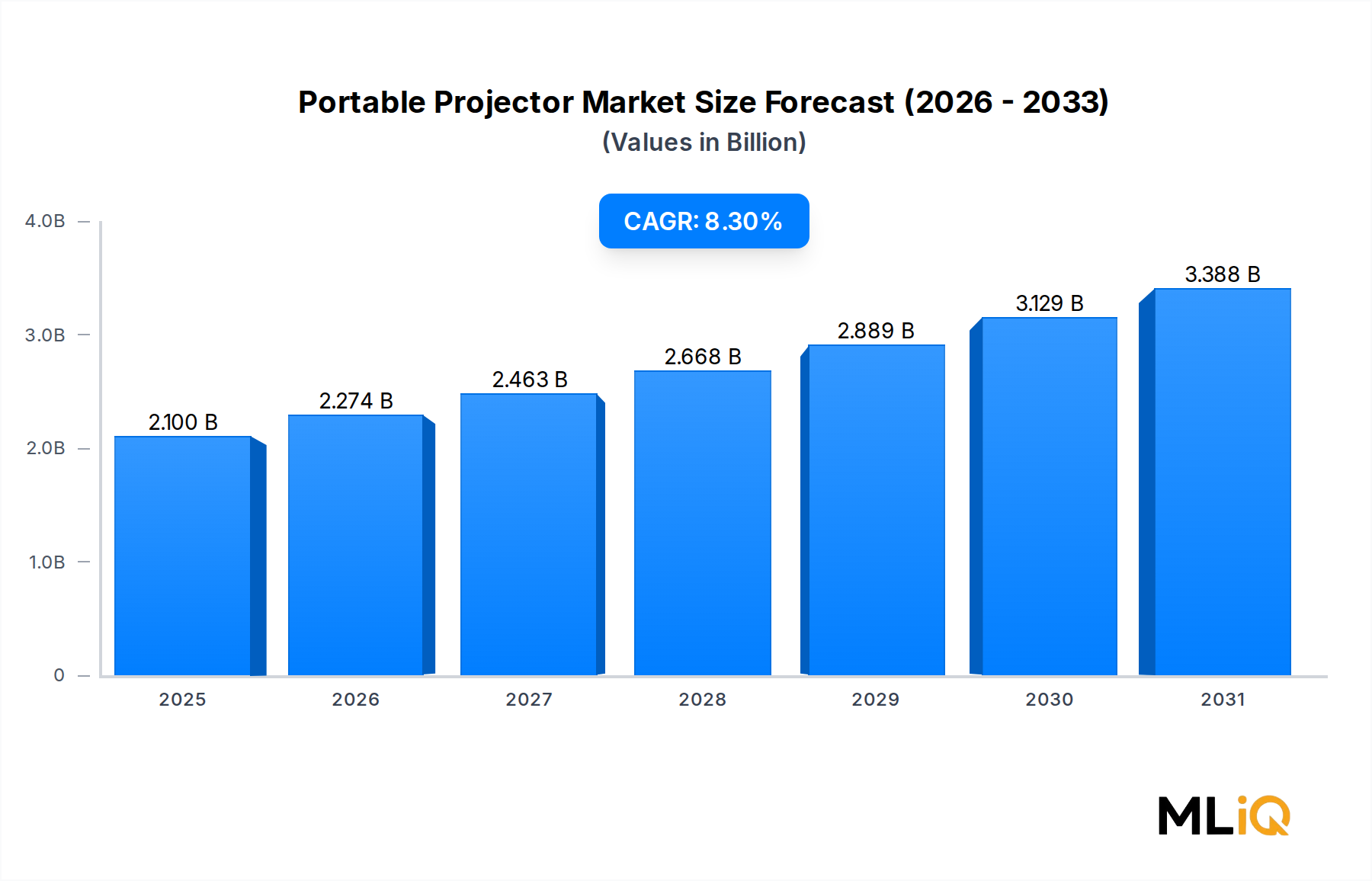

The global Portable Projector Market was valued at $2.1 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 8.3% through 2033, driven by accelerating consumer adoption of compact display solutions, the proliferation of remote and hybrid work environments, and rapid advances in miniaturized optical and semiconductor technologies. The market's trajectory reflects a structural shift in how individuals and enterprises consume and present visual content, moving decisively away from fixed, large-format installations toward agile, battery-powered alternatives.

Key demand drivers include the sustained expansion of the Consumer Electronics Market, in which portable projectors now occupy a distinct and growing sub-segment alongside smartphones, tablets, and wearables. Simultaneously, enterprise adoption of compact projection units for boardroom agility and field-based presentations has compressed sales cycles and broadened addressable buyer personas beyond traditional IT procurement. Educational institutions across Asia Pacific and Latin America are deploying portable projectors as cost-effective substitutes for interactive whiteboards and fixed ceiling-mounted systems, further diversifying end-market demand.

Macroeconomic tailwinds reinforcing this outlook include falling bill-of-materials costs for DLP chipsets and laser light engines, improvements in battery energy density that now support projection sessions exceeding three hours on a single charge, and the growing ubiquity of wireless display protocols such as Wi-Fi 6 and Miracast that eliminate cable dependency. The proliferation of streaming content platforms has also catalyzed demand for personal home cinema experiences without the spatial and financial burden of a fixed installation, a trend accelerating adoption among millennials and Gen Z consumers.

From a competitive standpoint, the market remains moderately fragmented, with the top ten vendors collectively holding an estimated share below 55% of global revenues in 2024. Innovation velocity is high, with product refresh cycles averaging 12 to 18 months across premium tiers. Looking forward to 2033, the market is expected to exceed $4.2 billion in absolute value, underpinned by the mainstream commercialization of holographic laser projection and the integration of AI-driven auto-keystone correction, ambient light sensing, and voice-assistant compatibility into entry-to-mid-range device tiers.

Among the four primary display technologies segmenting the Portable Projector Market — DLP (Digital Light Processing), LCD, LCoS (Liquid Crystal on Silicon), and Holographic Laser Projection — DLP commands the largest revenue share, estimated at approximately 48% of total market revenues in 2024. This dominance is rooted in DLP's unique combination of optical efficiency, compact chip architecture, and manufacturing scalability that aligns precisely with the size, weight, and brightness constraints intrinsic to portable form factors.

DLP technology, originally commercialized by Texas Instruments through its Digital Micromirror Device (DMD), enables projector OEMs to engineer units weighing under 500 grams while delivering luminous output in the 200 to 1,000 lumen range adequate for semi-darkened indoor environments. The single-chip DLP architecture eliminates the color filter arrays and polarizers required by LCD panels, reducing optical path length and allowing tighter chassis packaging. This mechanical advantage is irreplaceable for ultra-portable and pocket projector designs where internal volume is measured in cubic centimeters.

The DLP Projector Market benefits from a mature supplier ecosystem. Texas Instruments supplies DMD chipsets across multiple resolution tiers — from WVGA through Full HD — giving OEMs a modular design platform that compresses time-to-market. This explains why players such as Optoma Technology Corp and LG Electronics have concentrated their portable product lines on DLP architectures even as they maintain LCD and LCoS offerings in their fixed-installation ranges. The reliability profile of DLP — characterized by absence of burn-in risk and resistance to humidity-induced color degradation — further cements its preference in consumer and business segments alike.

LCD-based portable projectors occupy the second position with approximately 28% revenue share, competing primarily on price in the sub-$200 retail tier. LCD units generally deliver superior color saturation for static presentations and educational content but are disadvantaged by bulkier optics and shorter lamp lifespans relative to DLP LED hybrids. LCoS technology, represented commercially by Sony's SXRD platform and JVC's D-ILA derivatives, captures approximately 12% share in the portable segment, concentrated in premium prosumer and professional cinema-grade applications where pixel fill factor and contrast ratio outweigh portability trade-offs.

Holographic Laser Projection remains nascent in terms of commercial deployment, representing under 4% of total market revenues in 2024, though analyst consensus positions it as the highest-growth sub-technology through 2033. Companies such as MicroVision Inc are advancing MEMS-based laser beam scanning that eliminates the need for a focusing lens entirely, enabling projection from virtually any focal distance without mechanical adjustment. This architectural breakthrough is particularly relevant for integration into smartphones, wearables, and automotive head-up displays, suggesting that Holographic Laser Projection will progressively erode DLP's share in ultra-compact form factors post 2027.

The Lumen segmentation reveals that the 500 to 3,000 lumen band currently represents the commercial sweet spot for portable projectors, balancing brightness adequacy against battery consumption and thermal management constraints. Below 500 lumens, units serve niche personal viewing scenarios with significant image quality compromises. Above 3,000 lumens, thermal dissipation requirements push device weight and dimensions beyond convenient portability thresholds.

Resolution segmentation shows HD/FHD units gaining share rapidly, crossing 40% of unit volumes in 2024 as display panel cost deflation brought Full HD DLP chipsets into mid-range price bands. VGA and XGA resolutions are in structural decline, confined to price-sensitive education procurement in emerging economies.

Several quantifiable forces are simultaneously accelerating and moderating growth trajectories in the Portable Projector Market.

On the demand acceleration side, the global installed base of remote and hybrid workers surpassed 1.3 billion individuals as of 2024 according to multiple enterprise workforce surveys, creating sustained demand for portable presentation hardware that empowers professionals to conduct high-quality visual communications from client sites, co-working spaces, and home offices without depending on venue-provided display infrastructure. This structural shift in work modality directly expands the total addressable market for business-grade portable projectors.

The education sector represents a second powerful demand engine. UNESCO data indicates that over 300 million students in South and Southeast Asia attend schools without fixed projection or interactive display infrastructure. Government-funded technology-in-education programs across India, Indonesia, Vietnam, and the Philippines are channeling procurement budgets toward portable projectors as fiscally efficient alternatives, with per-unit costs ranging from $150 to $400 compared to $1,500 to $3,000 for comparable interactive flat panel installations.

On the supply side, the deflation of LED light source costs — LED arrays now accounting for approximately 18% of total bill-of-materials in mid-range portable projectors, down from 27% in 2020 — has enabled OEMs to improve gross margins or pass savings through to consumers, stimulating volume growth in the $200 to $500 retail tier that constitutes the highest-velocity price band.

Primary constraints include battery technology limitations. Lithium-ion energy density improvements have plateaued at approximately 2 to 3% annually, insufficient to simultaneously extend projection runtime and reduce chassis weight at the rate consumers demand. Thermal management remains a co-constraint: DLP and laser light engines operating at 100+ lumens generate localized heat densities that necessitate active cooling solutions incompatible with truly pocket-sized chassis designs, creating an engineering boundary that OEMs have not yet resolved through passive thermal materials alone.

Content rights and wireless connectivity fragmentation also constrain market penetration in premium entertainment use cases, as HDCP 2.2 compliance requirements and platform-specific streaming restrictions limit the projector's utility as a standalone home entertainment device without auxiliary streaming dongles.

The competitive landscape of the Portable Projector Market is characterized by a blend of diversified consumer electronics conglomerates, specialized projection OEMs, and technology-focused semiconductor-adjacent companies. The following profiles reflect the ten key players identified in the market dataset:

LG Electronics: A diversified consumer electronics leader headquartered in Seoul, LG has positioned its CineBeam product family as a premium lifestyle projector range, integrating webOS smart TV platforms and achieving brightness outputs up to 2,700 lumens in its portable Ultra Short Throw variants. The company leverages its OLED and display panel expertise to differentiate color accuracy benchmarks against DLP-dominant competitors.

Optoma Technology Corp: One of the highest-volume DLP projector specialists globally, Optoma competes aggressively across the $200 to $1,500 portable segment with a broad SKU portfolio spanning business, education, and home entertainment end-uses. The company's GT and ML series have established reference benchmarks for throw ratio flexibility and wireless connectivity feature sets.

Aaxa Technologies Inc.: A specialist in ultra-compact pico and micro projectors, Aaxa Technologies Inc. targets the budget-to-mid-range consumer and education segments with DLP LED projectors priced primarily below $300. The company's direct-to-consumer e-commerce distribution model enables competitive pricing without traditional retail margin stacking.

Miroir USA: Miroir USA focuses on ultra-miniaturized pocket projectors optimized for smartphone connectivity and personal entertainment use cases. Its product positioning emphasizes minimalist industrial design and sub-200 gram weight targets, appealing to frequent travelers and content creators.

Sony Corporation.: Sony competes in the premium and prosumer portable projection tier, deploying its proprietary LCoS (SXRD) technology to deliver class-leading contrast ratios and color volume metrics. The company's MP-CD1 and related compact cinema projectors target home theater enthusiasts and creative professionals willing to pay a premium for image fidelity.

Syndiant: Syndiant operates as a fabless semiconductor company supplying LCoS microdisplay panels to OEM projector manufacturers rather than competing in finished-goods markets. Its high-resolution panels are integrated into prosumer and professional portable projectors, making Syndiant a critical component supplier within the broader supply chain.

Celluon Inc: Celluon Inc is recognized for pioneering laser-based virtual keyboard and projection products, with its PicoPro and Epic laser projector platforms targeting ultra-portable business and personal productivity applications. The company's MEMS laser scanning architecture enables focus-free projection, differentiating it from lens-based DLP competitors.

ZTE Corporation: ZTE competes in the portable smart projector category primarily through its Spro series, integrating Android operating systems and LTE/5G connectivity to deliver standalone smart projector functionality without external source devices. The company's telco heritage provides distribution channel advantages through carrier partnerships in China and selected emerging markets.

Lenovo Group Ltd: Lenovo has entered the portable projector segment as an extension of its enterprise mobility ecosystem, targeting business professionals already within its ThinkPad and ThinkBook customer base. Its Go Portable Projector and related accessories are positioned as productivity companions optimized for USB-C bus-powered operation from laptops.

MicroVision Inc: MicroVision Inc is a semiconductor and photonics innovation company advancing MEMS-based laser beam scanning technology applicable to both automotive lidar and ultra-compact projection modules. Its PicoP scanning engine represents a platform technology licensed to OEM partners for integration into next-generation portable and wearable projection devices.

January 2025: LG Electronics unveiled the CineBeam Q portable laser projector at CES 2025, featuring a 500 lumen output in a 1.4 kg chassis with native 4K resolution support via LCoS optics, establishing a new performance benchmark for the premium portable segment.

March 2025: Optoma Technology Corp announced a strategic distribution partnership with a pan-European AV systems integrator network to expand portable projector accessibility across 18 European markets, targeting the education and SME business sectors with dedicated channel incentive programs.

June 2024: MicroVision Inc completed a technology licensing agreement with an undisclosed Tier-1 consumer electronics manufacturer for integration of its PicoP laser scanning engine into a forthcoming wearable display product category, marking a significant commercialization milestone for MEMS-based projection technology.

September 2024: Sony Corporation. launched the SRX-T615 compact reference projector targeting the professional events and high-end home cinema installation markets, incorporating updated SXRD panels with improved native contrast ratios exceeding 100,000:1.

November 2024: ZTE Corporation expanded its Spro Smart Projector lineup with a 5G-enabled variant featuring integrated Amazon Alexa voice control and HDR10+ content support, targeting smart home ecosystem integration in the Chinese domestic market.

February 2025: Aaxa Technologies Inc. introduced the M900 Pro, a 900 lumen portable DLP projector with a native 1080p resolution and a stated lamp-free LED lifespan of 30,000 hours, priced at $349, directly challenging mid-range offerings from larger OEM brands.

April 2025: Lenovo Group Ltd announced a corporate volume procurement agreement with a multinational professional services firm to supply 12,000 units of its Go Portable Projector over an 18-month deployment cycle, validating enterprise channel traction for sub-$400 business-class portable units.

Investment activity across the Portable Projector Market has intensified since 2022, driven by the convergence of miniaturized optics, AI-enabled image processing, and the broader consumer electronics supercycle associated with post-pandemic lifestyle hardware spending.

Mergers and acquisitions have been concentrated in the upstream semiconductor and optical component sub-segments. Fabless LCoS and DLP panel suppliers have attracted strategic investment from display conglomerates seeking vertical integration, as component supply constraints during 2021 to 2022 exposed supply chain vulnerabilities for projector OEMs dependent on single-source chipset suppliers. The Semiconductor Components Market has seen consolidation pressure from projector OEM procurement teams seeking long-term supply agreements and equity stakes in critical component manufacturers.

Venture capital deployment has been directed primarily toward software-differentiated portable projection platforms — specifically, companies developing AI-powered ambient correction algorithms, real-time geometric auto-adjustment systems, and embedded streaming OS platforms. Startups operating in the intersection of the Pico Projector Market and augmented reality display technology have attracted notable Series A and B rounds in the $15 million to $60 million range from strategic corporate venture funds affiliated with consumer electronics and automotive OEMs.

The Laser Projection Market sub-segment has attracted disproportionate institutional capital relative to its current revenue contribution, reflecting investor conviction in its long-term displacement of LED and lamp-based technologies. Strategic partnerships between laser diode manufacturers in Japan and South Korea and portable projector OEMs have structured multi-year supply commitments with embedded equity warrants, aligning technology roadmap incentives across the supply chain.

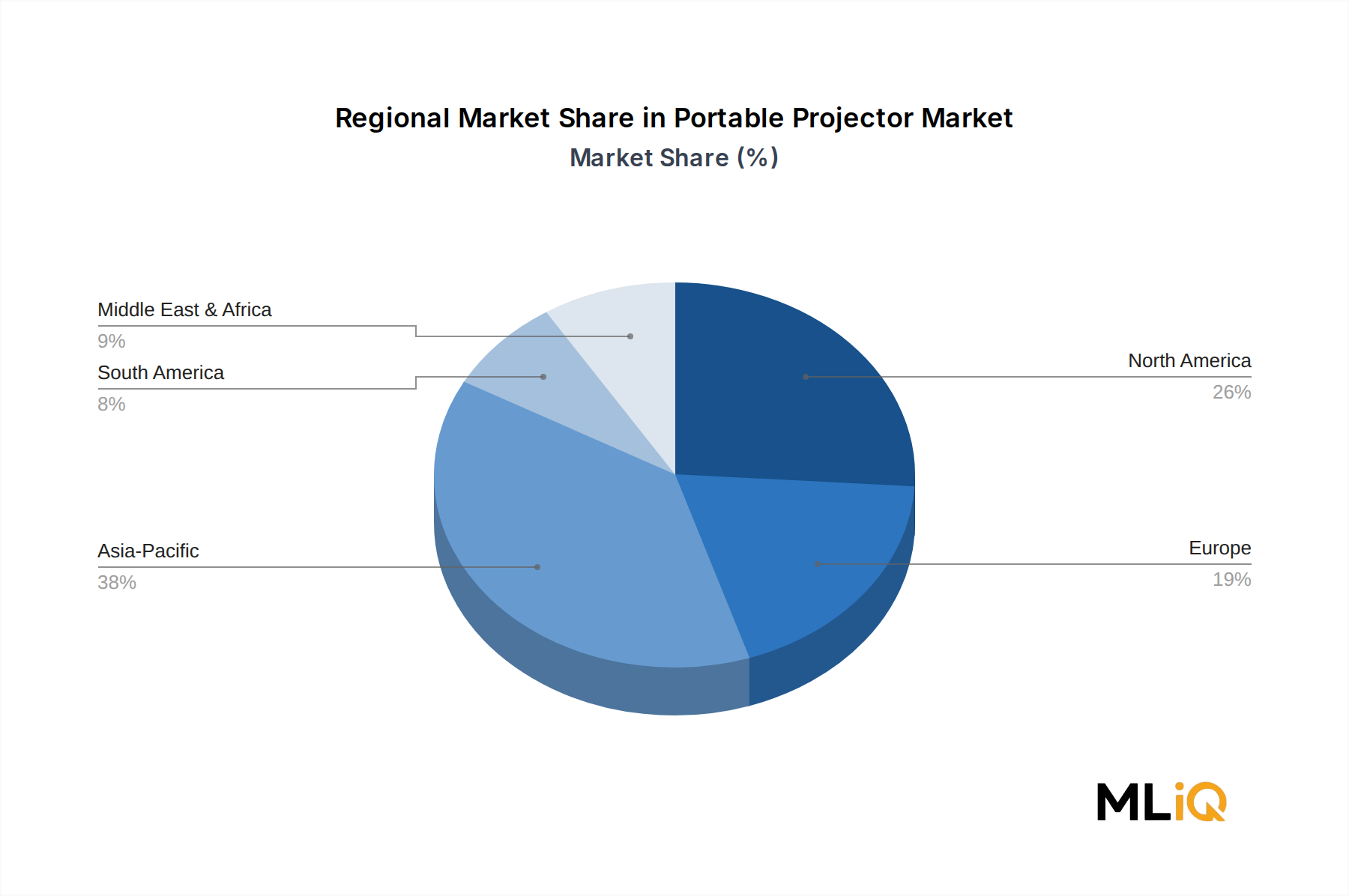

Geographically, China-based investment consortia have been most active in funding portable smart projector platforms that integrate 5G connectivity, cloud streaming, and AI content recommendation, targeting the domestic premium consumer market. Cross-border M&A involving Chinese acquirers targeting European and North American portable projector IP has faced heightened regulatory scrutiny under foreign direct investment review frameworks active since 2023.

The regulatory environment governing the Portable Projector Market spans product safety, electromagnetic compatibility, energy efficiency, laser safety classification, and environmental compliance frameworks across key geographies.

In the European Union, the Ecodesign for Sustainable Products Regulation (ESPR), which supersedes the original Ecodesign Directive, introduces mandatory energy efficiency minimum standards and repairability index requirements for electronic display products including projectors. Compliance timelines accelerating through 2025 to 2027 are compelling OEMs to redesign power management architectures and shift from legacy

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.3% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Portable Projector Market market expansion.

Key companies in the market include LG Electronics, Optoma Technology Corp, Aaxa Technologies Inc., Miroir USA, Sony Corporation., Syndiant, Celluon Inc, ZTE Corporation, Lenovo Group Ltd, MicroVision Inc.

The market segments include Technology, Dimensions, Lumen, Resolution, End-Use.

The market size is estimated to be USD 2.1 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Portable Projector Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Portable Projector Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.