1. What are the major growth drivers for the Flight Control Equipment Market market?

Factors such as are projected to boost the Flight Control Equipment Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

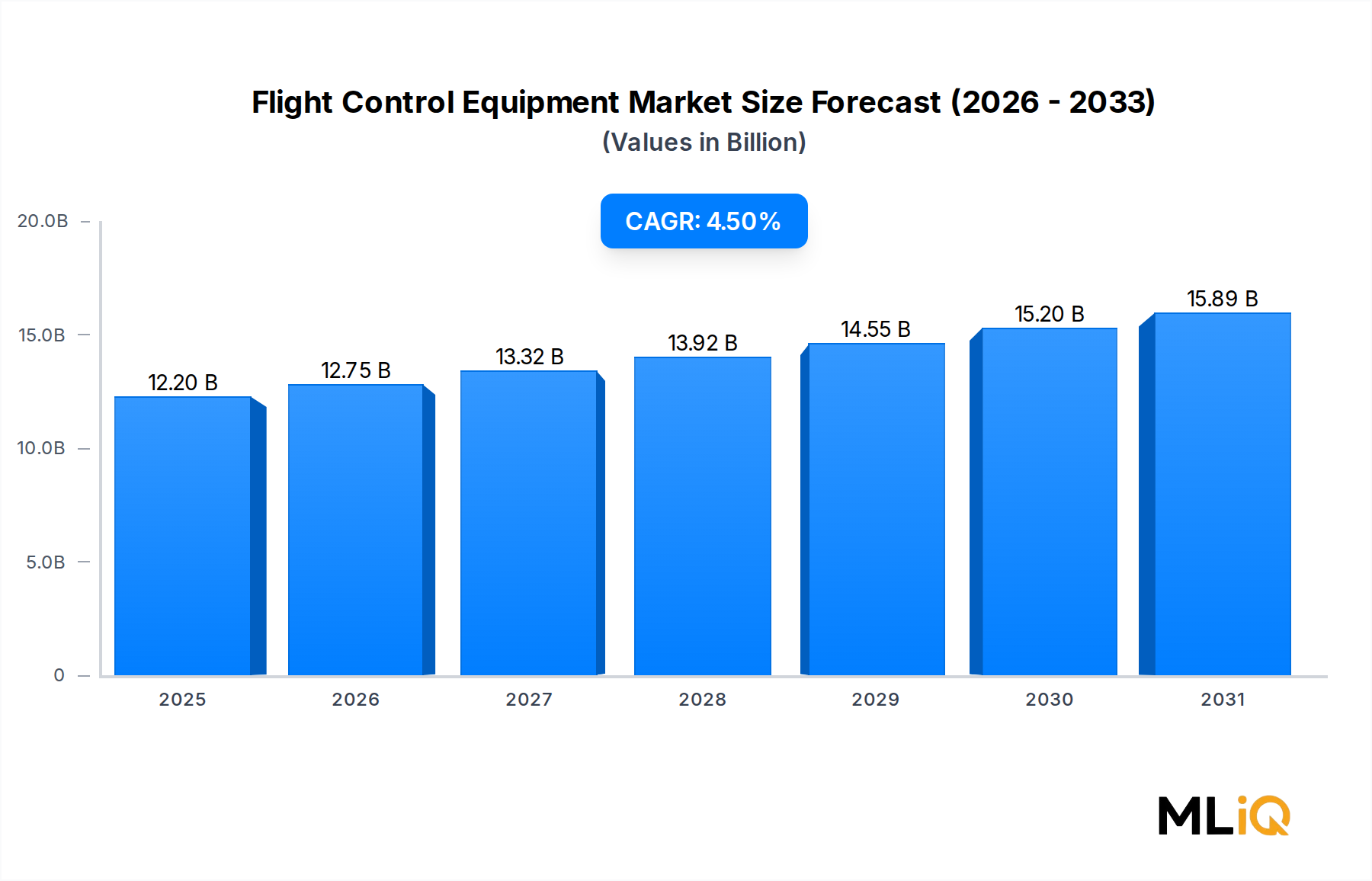

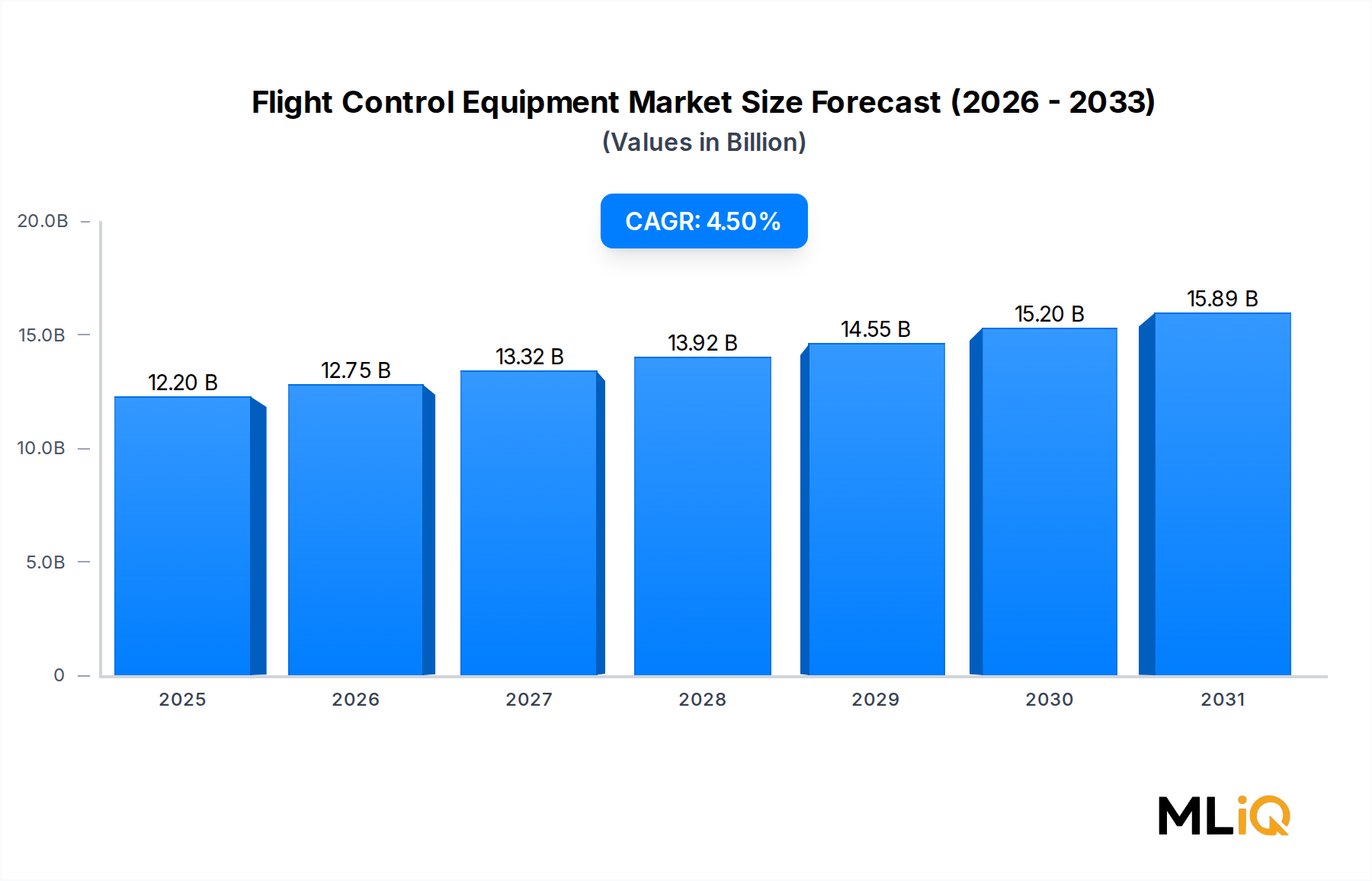

The global Flight Control Equipment Market is valued at $12.2 billion in 2025, reflecting sustained momentum driven by rising defense expenditures, accelerating commercial aviation recovery, and the rapid proliferation of next-generation aircraft platforms. Forecasts project the market to expand at a compound annual growth rate (CAGR) of 4.5% through the forecast horizon, underscoring robust long-term demand across both military and civil aviation segments.

Key demand drivers include the modernization of aging military fleets across NATO and Indo-Pacific nations, the surge in narrowbody and widebody aircraft orders from low-cost carriers, and the increasing adoption of fly-by-wire (FBW) and fly-by-light (FBL) architectures that require sophisticated electronic control hardware. The post-pandemic rebound in global air passenger traffic — which surpassed pre-2019 levels by 2024 — has prompted major original equipment manufacturers (OEMs) such as Airbus and Boeing to accelerate production ramp-ups, directly stimulating procurement of advanced flight control equipment.

Macro tailwinds further amplify this trajectory. Geopolitical tensions across Eastern Europe and the Asia-Pacific region have translated into elevated defense budgets; NATO members have collectively committed to spending 2% of GDP on defense, with avionics and flight control modernization forming a significant budget line. Simultaneously, urban air mobility (UAM) and autonomous aircraft initiatives are unlocking nascent demand vectors that extend well beyond traditional airframe programs.

On the technological frontier, the integration of artificial intelligence (AI) for adaptive control laws, the proliferation of modular open-system architectures (MOSA), and the maturation of electric flight control actuators are collectively redefining what constitutes a flight control system. These trends are compressing product development cycles and raising the bar for supplier certification compliance under FAA DO-178C and EASA CS-25 standards.

Supply-side consolidation — particularly among Tier 1 aerospace electronics integrators — is concentrating market share while simultaneously creating integration risk for platform primes. The entrance of defense-focused private equity into mid-tier avionics suppliers adds further competitive complexity.

Looking ahead, the Flight Control Equipment Market is positioned for consistent, quality-driven growth. The convergence of digital transformation, next-generation combat aircraft programs (including sixth-generation fighters), and the commercialization of electric vertical take-off and landing (eVTOL) platforms will collectively sustain capital investment in advanced flight control hardware and software well into the 2030s.

Among the end-user segments — commercial aircraft, defense aircraft, cargo military aircraft, and others — the defense aircraft segment commands the largest revenue share within the Flight Control Equipment Market, driven by the high unit value of military-grade flight control systems, the non-negotiable reliability and redundancy requirements embedded in defense procurement contracts, and the sheer breadth of active fleet modernization programs globally.

Defense aircraft flight control systems are engineered to operate across extreme environmental envelopes — supersonic speeds, high-g maneuver profiles, electronic warfare environments, and low-observable stealth configurations — demands that necessitate bespoke hardware, radiation-hardened electronics, and triple-redundant architectures. This engineering intensity translates directly into elevated per-unit revenues compared to commercial equivalents, anchoring the defense segment's top-line dominance.

The United States remains the single largest defense spender, with the Department of Defense's Fiscal Year 2025 budget allocating over $140 billion to procurement and research, development, test, and evaluation (RDT&E) — a meaningful portion of which flows into advanced aircraft programs including the F-35 Joint Strike Fighter, the B-21 Raider, and next-generation unmanned combat aerial vehicles (UCAVs). Each of these platforms represents a sustained multi-decade demand stream for flight control equipment subsystems.

European defense programs are also expanding. The Future Combat Air System (FCAS) — a Franco-German-Spanish initiative — and the Tempest program led by the United Kingdom represent multi-billion-euro commitments to sixth-generation fighter development, both of which will require novel flight control architectures. SAAB's Gripen E program, meanwhile, represents a mid-tier fighter export opportunity across Southeast Asia and Latin America that is actively generating flight control equipment orders.

Within the defense aircraft segment, fly-by-wire systems represent the dominant product sub-category, having entirely displaced mechanical and hydromechanical flight controls on frontline platforms. The shift toward fly-by-light — using fiber-optic data buses rather than copper wire for signal transmission — is progressing, particularly in classified programs where electromagnetic pulse (EMP) hardening is a design requirement.

Key players sustaining their position in the defense aircraft segment include BAE Systems, which holds deep integration contracts on the F-35's vehicle management computer; MOOG Inc., whose electrohydraulic and electromechanical actuators are specified on multiple USAF platforms; Parker Hannifin Corporation, a critical supplier of hydraulic flight control actuation on legacy and next-generation military aircraft; and Honeywell International Inc., whose inertial navigation and air data systems are deeply embedded in defense avionics suites.

The defense segment's share is consolidating rather than expanding as a proportion of the total Flight Control Equipment Market, owing to the accelerating growth of the commercial and UAM segments. However, in absolute dollar terms, defense aircraft investment continues to grow year-over-year, supported by multi-decade platform lifecycles, technology refresh cycles, and the growing importance of unmanned systems that require sophisticated autonomous flight control subsystems. The segment's structural dominance is therefore expected to persist through the forecast period, underpinned by long-term contracts and government-mandated domestic sourcing requirements.

The Flight Control Equipment Market is shaped by a well-defined set of quantifiable drivers and constraints that collectively determine investment velocity and competitive intensity.

Driver 1 — Military Modernization Programs: Global defense budgets reached approximately $2.2 trillion in 2023, per SIPRI data, marking the ninth consecutive year of increase. Modernization of aging fighter and transport fleets — notably the replacement of fourth-generation platforms with fifth- and sixth-generation aircraft — is generating sustained procurement demand for advanced flight control hardware across North America, Europe, and the Asia-Pacific.

Driver 2 — Commercial Aviation Fleet Expansion: IATA projects that global commercial aircraft fleets will nearly double to approximately 48,000 aircraft by 2043, implying delivery of over 40,000 new aircraft over the next two decades. Each new commercial airframe incorporates advanced fly-by-wire systems, generating compounding demand for flight control computers, actuators, and associated sensors.

Driver 3 — Fly-by-Wire Penetration: Fly-by-wire technology now commands over 70% of new commercial narrowbody deliveries, and its adoption on regional jets and next-generation turboprops is accelerating. This penetration rate structurally elevates average system complexity and per-unit value across the Flight Control Equipment Market.

Driver 4 — UAM and eVTOL Proliferation: Over 800 eVTOL designs are in various stages of development globally as of 2025, each requiring novel flight control architectures. This nascent segment is expected to contribute meaningfully to market volumes by 2028.

Constraint 1 — Certification Complexity: FAA and EASA certification timelines for new flight control software (DO-178C Level A) and hardware (DO-254) can exceed 5–7 years, creating substantial time-to-market delays and R&D cost overruns that disproportionately burden smaller Tier 2 and Tier 3 suppliers.

Constraint 2 — Supply Chain Fragility: Semiconductor shortages experienced during 2021–2023 disrupted avionics production schedules by 12–18 months at several major OEMs, exposing critical single-source dependencies in flight control computer assemblies.

Constraint 3 — Cybersecurity Requirements: Increasingly stringent DO-326A airworthiness security requirements add development cost and timeline burden, particularly for connected flight control systems interfacing with aircraft health management and communications infrastructure.

The competitive landscape of the Flight Control Equipment Market is characterized by a concentrated tier of global defense and aerospace primes alongside specialized mid-tier suppliers. The following profiles reflect each company's strategic positioning:

BAE Systems (U.K.): A leading integrator of vehicle management computers and fly-by-wire systems for military aircraft, BAE Systems holds deep integration roles on the F-35 program and is advancing autonomous flight control technologies for unmanned combat platforms.

UTC Aerospace Systems (U.S.): Now operating under Collins Aerospace (a Raytheon Technologies subsidiary), UTC Aerospace Systems contributed a broad portfolio of flight control actuation and sensing systems; the entity's capabilities have been consolidated into one of the most comprehensive avionics integration portfolios in the industry.

Rockwell Collins (U.S.): Absorbed into Collins Aerospace following the 2018 merger, Rockwell Collins built its reputation on advanced flight management systems and integrated modular avionics, and those product lines continue to anchor Collins Aerospace's commercial flight control business.

MOOG Inc. (U.S.): Specializes in precision electrohydraulic and electromechanical actuation systems for both military and commercial aircraft; MOOG's flight controls division is a primary supplier to virtually every major U.S. defense platform currently in production or development.

Honeywell International Inc. (U.S.): Offers a vertically integrated portfolio spanning flight control computers, inertial reference systems, and air data sensing; Honeywell is aggressively targeting the urban air mobility segment with adapted flight control architectures for eVTOL platforms.

Safran S.A. (France): A dominant supplier of flight control actuation and wiring harness systems for Airbus commercial programs; Safran is investing in more-electric aircraft technologies to reduce hydraulic system dependence in next-generation flight control architectures.

SAAB Ab (Sweden): Provides flight control systems for the Gripen fighter family and is expanding its export footprint across emerging market air forces; SAAB is also a technology partner in European next-generation combat aircraft feasibility studies.

Liebherr Group (Germany): Supplies high-reliability flight control actuation and hydraulic systems for both commercial and military platforms; Liebherr is notable for its dual-use capability across fixed-wing and rotary-wing aircraft.

Parker Hannifin Corporation (U.S.): A critical supplier of hydraulic and electromechanical flight control actuation; Parker Hannifin's Aerospace Systems segment serves all major commercial OEMs and is a key provider on U.S. Air Force tanker and bomber programs.

Raytheon Company (U.S.): Through its integration into RTX (Raytheon Technologies), the company contributes advanced sensor fusion and electronic warfare capabilities that interface with and enhance flight control system performance on military platforms.

January 2024: Honeywell International Inc. announced a strategic partnership with Joby Aviation to co-develop integrated fly-by-wire flight control systems for Joby's eVTOL air taxi, marking a significant technology crossover from traditional aviation into the urban air mobility segment.

March 2024: Parker Hannifin Corporation received a long-term contract extension from Boeing for electromechanical actuator supply on the 777X program, extending production commitments through 2035 and representing a multi-hundred-million-dollar revenue stream.

June 2024: Safran S.A. completed qualification testing of its next-generation electromechanical flight control actuator designed for more-electric aircraft architectures, targeting Airbus A320neo family retrofit and future narrowbody applications.

August 2024: MOOG Inc. was awarded a U.S. Air Force contract to supply advanced flight control actuation systems for the Next Generation Air Dominance (NGAD) technology maturation program, underscoring the company's continued relevance in classified combat aircraft development.

October 2024: BAE Systems announced a £200 million investment in its Rochester, U.K., facility to expand production capacity for military flight control computers, aligned with increased Tempest program design and development activity.

December 2024: Rockwell Collins-lineage products at Collins Aerospace received FAA STC approval for a digital flight control upgrade package applicable to Boeing 737NG retrofit, opening a significant aftermarket revenue pathway.

February 2025: The European Union Aviation Safety Agency (EASA) published updated airworthiness cybersecurity standards under ED-202A, directly impacting certification timelines for all new flight control system developments across the Flight Control Equipment Market.

North America represents the most mature and revenue-dominant region within the Flight Control Equipment Market, accounting for an estimated 38–40% of global market revenue in 2025. The United States' unparalleled defense procurement scale — anchored by F-35 production, NGAD development, and extensive legacy fleet sustainment — drives consistent high-value demand. Commercial aviation demand from major U.S. carriers, combined with the robust Boeing and Lockheed Martin OEM ecosystems, reinforces North America's leading position. The regional CAGR is estimated at approximately 3.8%, reflecting market maturity rather than stagnation.

Europe constitutes the second-largest regional market, holding approximately 25–28% revenue share. Growth is propelled by Airbus commercial ramp-ups at its Hamburg and Toulouse final assembly lines, the Eurofighter Typhoon sustainment program, and the emergence of the FCAS and Tempest sixth-generation fighter programs. The U.K., France, Germany, and Sweden are the dominant national markets. European regional CAGR is estimated at 4.1%, with defense modernization providing incremental upside above the baseline.

Asia-Pacific is the fastest-growing regional market, with an estimated CAGR of 6.2% over the forecast period. China's indigenous combat aircraft programs (J-20 upgrades, FC-31 derivatives) and its COMAC C919 commercial ramp-up are generating substantial domestic flight control equipment demand, while India's Tejas Mk2 and AMCA fighter programs — combined with Air India and IndiGo's massive aircraft orders — are expanding the Indian sub-market. South Korea's KF-21 Boramae fighter program and Japan's F-X next-generation fighter represent additional high-value program opportunities. The ASEAN region's airline capacity growth further contributes to commercial demand.

Middle East and Africa is an emerging growth corridor, driven by Gulf state military modernization and a sustained narrowbody aircraft procurement cycle by carriers including Emirates, Qatar Airways, and Riyadh Air. The regional CAGR is estimated at 5.1%, with defense spending in Saudi Arabia, the UAE, and Israel as primary demand anchors.

South America remains the smallest regional contributor, with a CAGR of approximately 3.2%, constrained by fiscal headwinds in Brazil and Argentina but supported by ongoing Embraer commercial aircraft production and modest military modernization budgets.

Environmental, social, and governance (ESG) considerations are increasingly shaping product development roadmaps, procurement decisions, and capital allocation strategies across the Flight Control Equipment Market. Three primary sustainability vectors are driving structural change.

First, the broader aviation industry's commitment to net-zero carbon emissions by 2050 — endorsed by IATA and reflected in ICAO's Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) — is accelerating investment in more-electric aircraft (MEA) architectures. MEA platforms progressively replace hydraulic and pneumatic flight control systems with electromechanical alternatives, reducing weight, eliminating hydraulic fluid (a hazardous material), and improving energy efficiency. This architectural shift is creating new product development mandates for suppliers across the Flight Control Equipment Market, requiring investment in brushless DC motors, high-power-density motor controllers, and solid-state power management.

Second, circular economy mandates — particularly within the European Union's Green Deal framework — are imposing end-of-life recyclability requirements on aerospace components. Flight control actuators and computers traditionally contain hazardous materials including lead-based

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Flight Control Equipment Market market expansion.

Key companies in the market include BAE Systems (U.K)9.1.1. Company Overview9.1.2. Key Executives9.1.3. Company Snapshot9.1.4. Operating Business Segments9.1.5. Product Portfolio9.1.6. Business Performance9.1.7. Key Strategic Moves and Developments9.2. UTC Aerospace Systems (U.S.)9.2.1. Company Overview9.2.2. Key Executives9.2.3. Company Snapshot9.2.4. Operating Business Segments9.2.5. Product Portfolio9.2.6. Business Performance9.2.7. Key Strategic Moves and Developments9.3. Rockwell Collins (U.S.)9.3.1. Company Overview9.3.2. Key Executives9.3.3. Company Snapshot9.3.4. Operating Business Segments9.3.5. Product Portfolio9.3.6. Business Performance9.3.7. Key Strategic Moves and Developments9.4. MOOG Inc. (U.S.)9.4.1. Company Overview9.4.2. Key Executives9.4.3. Company Snapshot9.4.4. Operating Business Segments9.4.5. Product Portfolio9.4.6. Business Performance9.4.7. Key Strategic Moves and Developments9.5. Honeywell International Inc. (U.S.)9.5.1. Company Overview9.5.2. Key Executives9.5.3. Company Snapshot9.5.4. Operating Business Segments9.5.5. Product Portfolio9.5.6. Business Performance9.5.7. Key Strategic Moves and Developments9.6. Safran S.A. (France)9.6.1. Company Overview9.6.2. Key Executives9.6.3. Company Snapshot9.6.4. Operating Business Segments9.6.5. Product Portfolio9.6.6. Business Performance9.6.7. Key Strategic Moves and Developments9.7. SAAB Ab (Sweden)9.7.1. Company Overview9.7.2. Key Executives9.7.3. Company Snapshot9.7.4. Operating Business Segments9.7.5. Product Portfolio9.7.6. Business Performance9.7.7. Key Strategic Moves and Developments9.8. Leibherr Group (Germany)9.8.1. Company Overview9.8.2. Key Executives9.8.3. Company Snapshot9.8.4. Operating Business Segments9.8.5. Product Portfolio9.8.6. Business Performance9.8.7. Key Strategic Moves and Developments9.9. Parker Hannifin Corporation (U.S)9.9.1. Company Overview9.9.2. Key Executives9.9.3. Company Snapshot9.9.4. Operating Business Segments9.9.5. Product Portfolio9.9.6. Business Performance9.9.7. Key Strategic Moves and Developments9.10. Raytheon Company (U.S).9.10.1. Company Overview9.10.2. Key Executives9.10.3. Company Snapshot9.10.4. Operating Business Segments9.10.5. Product Portfolio9.10.6. Business Performance9.10.7. Key Strategic Moves and Developments.

The market segments include Application, Device Type, End User.

The market size is estimated to be USD 12.2 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Flight Control Equipment Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Flight Control Equipment Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.