1. What are the major growth drivers for the 5G Small Cell Market market?

Factors such as are projected to boost the 5G Small Cell Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

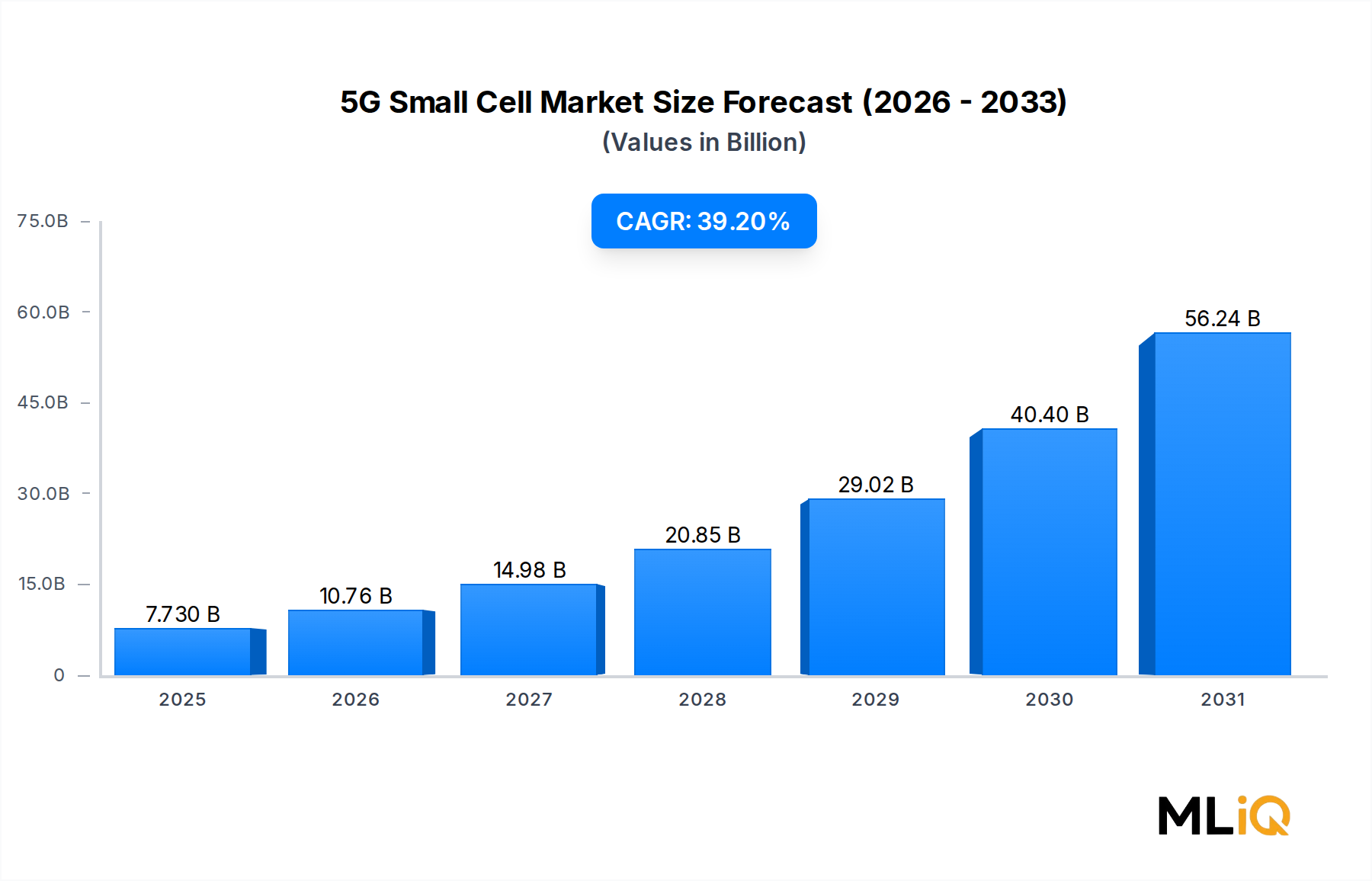

The global 5G Small Cell Market is poised for extraordinary expansion, with its valuation estimated at $7.73 billion in 2025 and projected to surge at a compound annual growth rate (CAGR) of 39.2% through 2033. This explosive trajectory reflects the accelerating global rollout of 5G networks, urbanization of mobile connectivity infrastructure, and the insatiable appetite for high-bandwidth, low-latency communications across enterprise and consumer segments.

Small cells — compact, low-power radio access points including picocells, femtocells, and microcells — are positioned as the architectural backbone of dense urban 5G deployments. Unlike macrocell towers, which cover broad geographic areas with high power, small cells are designed to fill coverage gaps, extend capacity in high-traffic zones, and deliver the millimeter-wave (mmWave) performance that next-generation applications demand. The convergence of smart city development, Industry 4.0 manufacturing automation, connected autonomous vehicles, and immersive augmented reality platforms is amplifying the demand signal for granular network densification.

From a macro-economic standpoint, government spectrum allocation programs, public-private partnerships, and national broadband initiatives across North America, Europe, and Asia Pacific are acting as powerful catalysts. The United States, China, South Korea, and members of the European Union have committed hundreds of billions of dollars to digital infrastructure modernization, with small cell deployments forming a critical component of urban connectivity strategies.

On the technology side, the transition from sub-6 GHz 5G to mmWave 5G is a structural tailwind. MmWave frequencies deliver multi-gigabit throughput but suffer from limited range and penetration, making dense small cell deployment a technical necessity rather than an option. Operators are deploying small cells across indoor venues — stadiums, airports, shopping malls, office complexes — as well as outdoor environments including street furniture, utility poles, and building facades.

The enterprise segment is increasingly adopting private 5G networks built on small cell architectures, enabling industrial automation, real-time asset tracking, and wireless process control in environments previously served by Wi-Fi or wired Ethernet. This enterprise adoption is expanding the total addressable market beyond traditional telecom operators.

Looking forward through 2033, the market will be defined by the maturation of Open RAN (O-RAN) standards, which are democratizing small cell hardware procurement and enabling multi-vendor interoperability. Simultaneously, energy efficiency imperatives are driving next-generation small cell designs toward lower power consumption per transmitted bit, reducing total cost of ownership for operators. The convergence of these trends positions the 5G Small Cell Market as one of the most dynamically growing segments within the broader Semiconductor and Electronics category.

Within the component-based segmentation of the 5G Small Cell Market, the hardware sub-segment commands the largest revenue share and is expected to maintain its leadership position through the forecast period. Hardware encompasses the physical radio units, baseband processing units, antennas, enclosures, power systems, and associated mounting infrastructure that form the tangible backbone of small cell deployments.

The hardware segment's dominance is grounded in the capital-intensive nature of network densification. Each small cell node requires purpose-built radio frequency (RF) hardware optimized for specific frequency bands — sub-6 GHz, mid-band, and mmWave — and the unit economics of large-scale deployments mean hardware procurement accounts for the majority of total project expenditure. Unlike software-defined elements that can be upgraded remotely, hardware must be physically manufactured, shipped, installed, and maintained, creating recurring revenue streams across the supply chain.

Key players driving the hardware segment include Nokia Corporation, Ericsson, Huawei Technologies Co. Ltd., Samsung Group, and NEC Corporation. Nokia's AirScale small cell portfolio has been widely deployed across European and North American networks, featuring integrated baseband and radio functions in compact form factors suitable for street-level and indoor deployment. Ericsson's Radio Dot System targets indoor enterprise applications, while Samsung Group has established strong footholds in the United States market through partnerships with major carriers including T-Mobile and Verizon.

Huawei Technologies Co. Ltd. remains a dominant hardware supplier in Asia Pacific markets, particularly China and Southeast Asia, where its LampSite and LampSite EE indoor small cell solutions have achieved widespread adoption across commercial buildings, transportation hubs, and stadiums. Despite geopolitical restrictions limiting Huawei's access to certain Western markets, the company continues to innovate aggressively in hardware miniaturization and energy efficiency.

Airspan Networks Inc. occupies an important niche in the hardware segment, specializing in Open RAN-compatible small cell hardware that enables operators to mix and match components from different vendors. This approach aligns with the broader industry shift toward disaggregated network architectures and is particularly relevant for Tier 2 and Tier 3 operators seeking cost-effective densification strategies.

The hardware segment is also benefiting from the maturation of application-specific integrated circuits (ASICs) and field-programmable gate arrays (FPGAs) designed specifically for 5G baseband processing. These purpose-built chips dramatically reduce power consumption and physical footprint compared to general-purpose processing architectures, enabling smaller, lighter, and more thermally efficient small cell units. The semiconductor innovation driving these improvements is closely linked to activity in the Semiconductor Chipset Market, where leading fabless designers and integrated device manufacturers are competing intensely on 5G modem and baseband processor performance.

The share of hardware in total small cell market revenue, while still dominant, faces gradual compression as managed services, software-defined networking capabilities, and network-as-a-service delivery models expand. However, this compression will be offset by volume growth: the absolute number of small cell units deployed globally is expected to grow by orders of magnitude as operators pursue the thousands of nodes per square kilometer density required for full mmWave coverage in urban cores. Industry analysts project that hardware procurement cycles will remain the primary revenue driver through at least 2029, after which services revenues may begin to close the gap.

The indoor deployment sub-segment — encompassing enterprise campuses, hospitals, transportation infrastructure, and retail environments — represents the fastest-growing application within hardware, driven by the surge in private 5G network deployments and venue-specific connectivity requirements that cannot be efficiently served by outdoor macrocell infrastructure.

The 5G Small Cell Market is shaped by a constellation of quantifiable drivers and structural constraints that collectively determine its growth trajectory.

Network densification requirements represent the primary demand driver. 5G mmWave signals operating above 24 GHz propagate only tens to hundreds of meters before significant attenuation, necessitating cell inter-site distances of 100–200 meters in dense urban deployments compared to 1–2 kilometers for sub-6 GHz macrocells. This geometric reality means operators must deploy 10 to 50 times more access nodes per unit area compared to 4G LTE networks, creating a structurally large and recurring hardware demand.

Spectrum allocation momentum is another measurable catalyst. In 2023 and 2024, regulatory bodies including the FCC, Ofcom, and national counterparts across Asia Pacific auctioned significant blocks of mid-band and mmWave spectrum. The C-band (3.7–3.98 GHz) auctions in the United States alone generated over $81 billion in proceeds, signaling operator commitment to 5G infrastructure investment at scale. Spectrum acquisition at these valuations creates a capital allocation imperative to deploy supporting infrastructure, including small cells, rapidly.

The expansion of private 5G networks is a powerful incremental driver. By 2024, over 1,500 private 5G networks had been deployed globally across manufacturing, logistics, mining, and healthcare sectors, with the figure expected to exceed 10,000 by 2028. Each private network deployment typically requires dedicated small cell infrastructure, expanding the addressable market beyond traditional telecom operator procurement.

On the constraint side, the primary challenge is site acquisition complexity and cost. Installing small cells on utility poles, building facades, and street furniture requires navigating complex permitting regimes, right-of-way agreements, and landlord negotiations. In dense urban environments, permitting timelines of 6–18 months per site can significantly delay deployment velocity. Regulatory streamlining efforts — such as the FCC's Shot Clock rules in the United States — have helped but have not fully resolved the bottleneck.

Power availability and grid connectivity at street-level sites present an additional constraint, as many candidate small cell locations lack convenient access to utility power, requiring costly trenching or solar power solutions. Supply chain disruptions affecting semiconductor components, particularly baseband processors, have intermittently extended hardware lead times by 8–16 weeks, constraining operators' ability to execute densification plans on schedule.

The competitive landscape of the 5G Small Cell Market is characterized by a blend of established telecom equipment giants, specialized small cell vendors, and emerging Open RAN ecosystem players. The following profiles capture the strategic positioning of the primary competitors:

ZTE Corporation: A leading Chinese telecom equipment manufacturer with a comprehensive small cell portfolio spanning indoor and outdoor deployments. ZTE has aggressively expanded its small cell presence across Asia Pacific and select emerging markets, leveraging its integrated R&D capabilities in baseband processing and RF design.

Cisco Systems Inc.: Positions its small cell strategy within a broader enterprise networking and private 5G narrative. Cisco integrates small cell capabilities with its enterprise Wi-Fi, switching, and security portfolio, targeting campus and industrial private network deployments where converged connectivity management is valued.

CommScope Inc.: A major provider of indoor connectivity solutions, including distributed antenna systems and small cells for enterprise and public venue environments. CommScope's RUCKUS small cell solutions are widely deployed in stadiums, airports, and convention centers across North America and Europe.

NEC Corporation: A Japanese technology conglomerate with strong small cell capabilities, particularly in the Open RAN ecosystem. NEC has partnered with Rakuten Mobile and other operators to deploy disaggregated small cell solutions, establishing a credible position in the O-RAN-compliant infrastructure segment.

Fujitsu Limited.: An early Open RAN proponent with commercial small cell deployments in Japan and expanding international partnerships. Fujitsu's small cell hardware is part of its broader telecom infrastructure business, with a focus on energy efficiency and compact form factors.

Nokia Corporation: One of the two largest global small cell vendors, Nokia offers the AirScale small cell family for outdoor macro-offload and indoor enterprise applications. Nokia's strength lies in its end-to-end network management software integration, making its small cells attractive to operators seeking unified radio access network operations.

Airspan Networks Inc.: A specialist small cell and Open RAN vendor with a differentiated portfolio of 5G outdoor and indoor nodes. Airspan has established partnerships with operators in the United States, Europe, and Asia Pacific, positioning itself as an agile alternative to the large incumbent vendors.

Samsung Group: A significant 5G small cell player, particularly in the United States and South Korea. Samsung's integrated approach — combining in-house chip design, radio hardware, and system software — has enabled competitive total cost of ownership propositions for major carrier customers.

Huawei Technologies Co. Ltd.: Despite geopolitical restrictions in certain markets, Huawei remains the dominant small cell vendor in China and maintains strong positions across Asia, Africa, and Latin America. Its LampSite portfolio is widely regarded as technically advanced in indoor coverage density.

Comba Telecom Systems Holdings Ltd.: A Hong Kong-based specialist in wireless coverage solutions, including distributed antenna systems and small cells. Comba serves both operator and enterprise customers across Asia Pacific and select international markets.

Telefonaktiebolaget LM Ericsson: The other of the two largest global small cell vendors, Ericsson's Radio Dot System and Street Macro solutions are deployed by major operators globally. Ericsson's software-centric approach to radio access network management differentiates its small cell offerings in enterprise and public network contexts.

January 2024: Nokia Corporation announced the commercial availability of its next-generation AirScale Indoor small cell, featuring a 40% reduction in power consumption compared to the prior generation, targeting enterprise and venue operators focused on total cost of ownership reduction.

March 2024: The U.S. Federal Communications Commission finalized updated rules streamlining small cell permitting on federal properties, reducing average approval timelines by an estimated 30% and accelerating outdoor urban densification plans for major operators.

May 2024: Samsung Group secured a multi-year small cell supply agreement with a major North American carrier for urban mmWave densification, covering the deployment of over 50,000 outdoor small cell units across 10 metropolitan areas through 2027.

July 2024: Ericsson and NEC Corporation announced a joint interoperability validation of their respective Open RAN small cell components on a Tier 1 European operator's live network, marking a milestone in multi-vendor O-RAN commercial readiness.

September 2024: Huawei Technologies Co. Ltd. unveiled its LampSite Ultra indoor small cell platform at MWC Shanghai, incorporating integrated AI-based interference management and claiming a 60% improvement in spectral efficiency for dense indoor environments.

November 2024: CommScope Inc. completed the acquisition of a specialized indoor positioning technology startup, integrating centimeter-level location accuracy capabilities into its small cell product line for logistics and healthcare enterprise applications.

February 2025: Airspan Networks Inc. announced a strategic partnership with a Southeast Asian national operator for the deployment of Open RAN-compliant outdoor small cells across 3 major urban markets, representing one of the largest O-RAN small cell contracts in the Asia Pacific region.

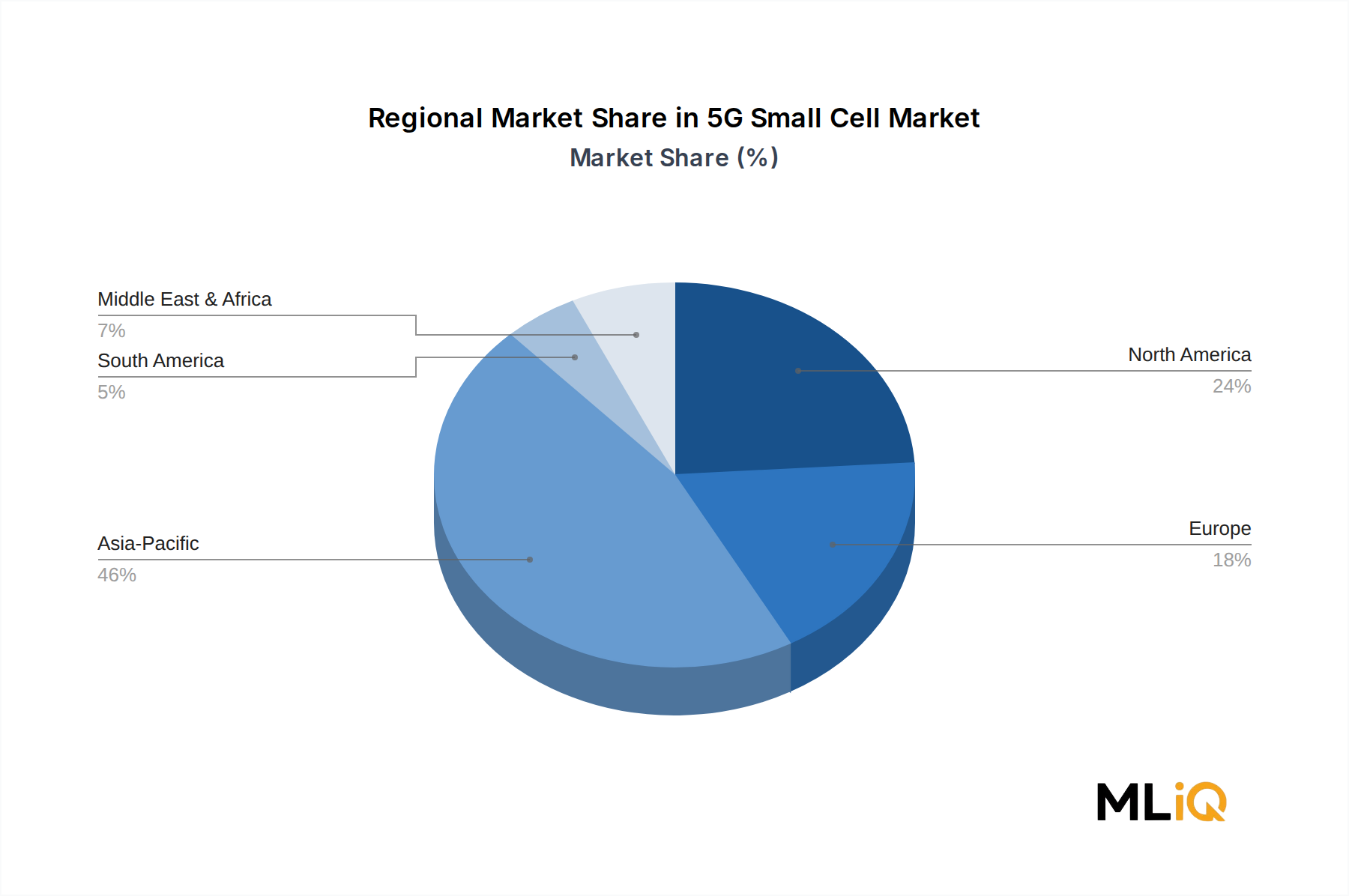

The 5G Small Cell Market exhibits significant regional variation in growth rates, maturity levels, and demand drivers, reflecting differences in spectrum policy, operator investment cycles, and urban infrastructure characteristics.

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR exceeding 42% through 2033, driven primarily by China's massive 5G infrastructure rollout and strong demand from India, South Korea, and Japan. China alone accounts for the largest national small cell deployment volume globally, with state-owned operators deploying millions of indoor and outdoor small cell nodes to support the country's smart city and digital economy initiatives. India represents the highest-growth opportunity within the region, with Reliance Jio and Airtel commencing 5G service rollouts and requiring aggressive densification to achieve coverage targets in the country's dense urban centers. South Korea and Japan, as early 5G adopters, are transitioning toward second-generation small cell upgrades focused on mmWave capacity and enterprise private network expansion.

North America is the most mature regional market, with the United States leading in mmWave small cell deployments supported by the FCC's spectrum auction outcomes and carrier capital expenditure commitments. The North American market is projected to grow at a CAGR of approximately 35%, somewhat below the global average, reflecting its relative maturity but still robust absolute investment volumes. Enterprise private 5G network deployments in manufacturing and logistics are a key secondary demand driver in this region.

Europe represents a mid-growth profile with a projected CAGR of approximately 33%, driven by smart city initiatives in Germany, the United Kingdom, France, and the Nordics. The European market is shaped by the EU's Digital Decade policy targets, which include 5G coverage of all populated areas by 2030, creating regulatory pressure for accelerated small cell deployments. Permitting complexity and fragmented national regulatory environments remain the primary constraint on deployment velocity.

Middle East and Africa is an emerging market with significant growth potential, particularly in the GCC countries where smart city mega-projects — such as NEOM in Saudi Arabia — are creating concentrated demand for dense 5G connectivity infrastructure. South Africa and Turkey represent additional active deployment markets within the region.

South America, led by Brazil and Argentina, represents the smallest but fastest-emerging regional segment, with operators beginning commercial 5G small cell deployments in major metropolitan areas. Infrastructure investment constraints and macroeconomic volatility temper near-term growth expectations relative to other regions.

Regulatory frameworks exert a profound influence on the deployment velocity, cost structure, and competitive dynamics of the 5G Small Cell Market. Across key geographies, policy evolution is generally trending toward facilitation of densification, though significant variation in implementation speed

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 39.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the 5G Small Cell Market market expansion.

Key companies in the market include ZTE Corporation, Cisco Systems Inc., CommScope Inc., NEC Corporation, Fujitsu Limited., Nokia Corporation, Airspan Networks Inc., Samsung Group, Huawei Technologies Co. Ltd., Comba Telecom Systems Holdings Ltd., Telefonaktiebolaget LM Ericsson.

The market segments include Component, Cell Type, End User.

The market size is estimated to be USD 7.73 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "5G Small Cell Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the 5G Small Cell Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.