1. What are the major growth drivers for the Automatic Test Equipment Market market?

Factors such as are projected to boost the Automatic Test Equipment Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

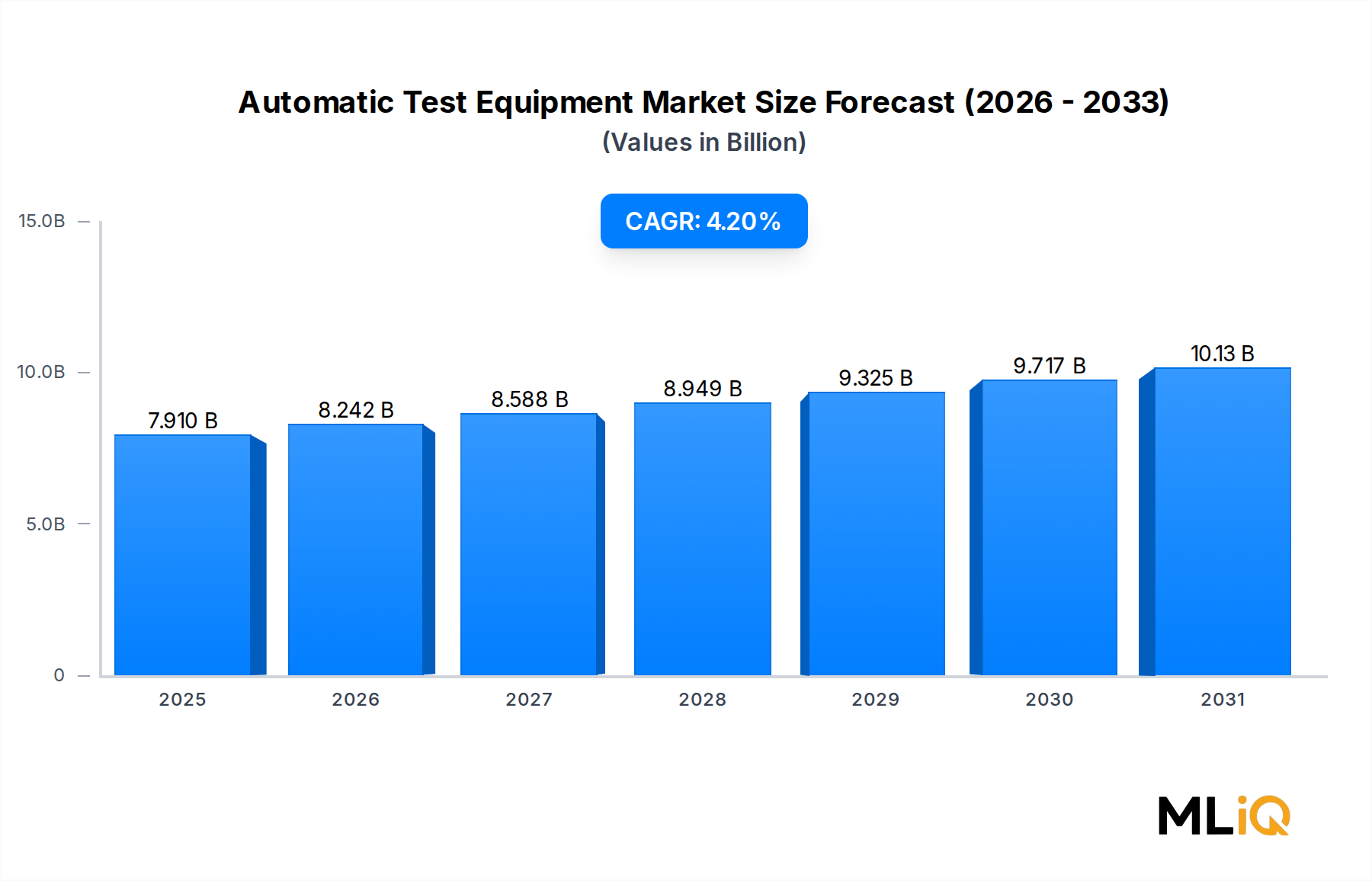

The global Automatic Test Equipment Market is valued at $7.91 billion as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 4.2% through 2033. This trajectory reflects sustained demand across semiconductor manufacturing, consumer electronics, aerospace, and automotive sectors, all of which require rigorous validation of electronic components prior to deployment. At the prevailing CAGR, the market is expected to surpass $11.5 billion by the end of the forecast window, underscoring the enduring strategic importance of test integrity in an era of complex, miniaturized electronics.

Several macro-level forces are simultaneously reinforcing demand. The accelerating proliferation of advanced node semiconductors — including 3nm and 5nm process geometries — demands progressively sophisticated test platforms capable of detecting sub-micron defects at scale. Concurrently, the global push toward vehicle electrification has elevated ATE requirements within automotive supply chains, where power electronics, battery management systems, and advanced driver-assistance system (ADAS) chipsets each demand dedicated, high-throughput test regimes. The expansion of 5G network infrastructure is a parallel catalyst, requiring millimeter-wave and radio-frequency test capabilities that legacy platforms cannot adequately address.

From a demand-side perspective, Asia Pacific — particularly China, South Korea, Taiwan, and Japan — remains the gravitational center of semiconductor fabrication and thus ATE consumption. However, significant policy-driven capacity investments in North America and Europe, spurred by the U.S. CHIPS and Science Act and the European Chips Act, are redistributing geographic demand in ways that will materially influence market structure through 2028 and beyond.

The competitive landscape is moderately concentrated, with Teradyne Inc. and Advantest Corporation together commanding a majority of global revenue share in the memory and digital test segments. However, mid-tier and specialty vendors are expanding into niche verticals — including medical device electronics, aerospace subsystems, and power semiconductor testing — creating a bifurcated market where scale advantages coexist with high-margin specialization opportunities.

Looking forward, the integration of artificial intelligence and machine learning into test analytics platforms represents the most transformative near-term trend. Predictive fault classification, adaptive test sequencing, and real-time yield optimization algorithms are shifting ATE from passive validation tools to active quality intelligence systems. This evolution is expected to increase average selling prices for premium ATE platforms while simultaneously applying cost pressure to commoditized legacy testers, reshaping margin structures across the value chain through the forecast horizon.

Among the type-based segments — Memory, Mixed Signal, Digital, and Others — the Memory segment commands the largest revenue share within the Automatic Test Equipment Market. This dominance is not incidental; it is structurally anchored in the volume economics of DRAM and NAND flash production, where test yield directly translates into margin outcomes for some of the world's largest semiconductor manufacturers.

Memory semiconductors are among the most test-intensive products in the electronics supply chain. Each DRAM module must undergo functional verification, parametric testing, and burn-in screening across thousands of individual cells. For NAND flash, the challenge is compounded by multi-level cell (MLC), triple-level cell (TLC), and quad-level cell (QLC) architectures, which require nuanced read-write endurance validation that pushes tester throughput and pin count requirements to their limits. As memory densities increase — driven by AI inference workloads demanding high-bandwidth memory (HBM) and enterprise SSD proliferation — the complexity and cost of memory ATE platforms continue to escalate.

Teradyne Inc.'s Magnum platform and Advantest Corporation's T5503 series are the dominant memory test solutions in this segment, collectively serving major integrated device manufacturers (IDMs) and fabless-to-foundry supply chains in South Korea, Japan, Taiwan, and China. These platforms support parallel test architectures capable of simultaneously testing hundreds of devices, a prerequisite for economic viability at high-volume manufacturing scale.

The memory segment's share consolidation is further reinforced by the cyclical nature of memory markets. During upswings in the DRAM pricing cycle — such as those observed in 2021 and again in 2023 driven by AI server memory demand — memory manufacturers aggressively invest in capacity and, consequently, in ATE capital expenditure. This cyclicality creates demand spikes that temporarily inflate the segment's revenue contribution, a pattern expected to recur as HBM3 and HBM4 adoption ramps through 2025 to 2027.

The rise of compute-in-memory architectures and processing-in-memory (PIM) technologies introduces a new layer of test complexity. These hybrid designs blur the boundary between logic and memory testing, requiring ATE platforms that can simultaneously validate both functional memory arrays and embedded logic cores. This convergence is creating a new sub-segment within memory ATE, one that commands a meaningful premium over conventional DRAM or NAND test equipment.

Geographically, South Korea — home to Samsung Electronics and SK Hynix — is the single largest national market for memory ATE procurement. Japan and Taiwan follow, driven by Kioxia, Micron's local operations, and supply chain integrators. China's domestic memory industry, centered on YMTC and CXMT, represents an emerging and increasingly constrained demand node due to export control dynamics affecting U.S.-origin ATE suppliers.

The memory segment's dominance shows no near-term signs of reversal. As AI training and inference hardware demands escalate memory bandwidth requirements, the capital intensity of memory fabrication — and by extension, memory ATE investment — will remain among the highest in the semiconductor ecosystem. Analysts anticipate the memory ATE sub-segment to maintain a revenue share above 35% of total ATE spending through 2033, with episodic spikes correlated to HBM capacity expansion cycles.

The Automatic Test Equipment Market is shaped by a tightly interlocking set of structural drivers and counterbalancing constraints that collectively determine capital allocation patterns across the semiconductor and electronics industries.

The most quantitatively significant driver is the global surge in semiconductor content per electronic device. The average automotive vehicle in 2024 contains between 1,400 and 3,000 discrete semiconductors — a figure that rises to over 4,000 in battery electric vehicles (BEVs) with full ADAS capability. Each semiconductor requires test coverage, and as vehicles incorporate more chips, ATE demand from automotive supply chains scales proportionally. This dynamic is estimated to have contributed approximately $480 million in incremental ATE demand between 2021 and 2024.

5G infrastructure rollout is a second computable driver. Global 5G base station deployments exceeded 3.5 million units by 2023, each containing radiofrequency front-end modules, power amplifiers, and baseband processors that require specialized high-frequency ATE. The transition to sub-6 GHz and mmWave 5G creates test requirement divergences that legacy RF testers cannot bridge, driving replacement and upgrade cycles estimated to generate $600 million in cumulative ATE spending through 2026.

On the constraint side, the capital expenditure cyclicality of semiconductor manufacturers represents the most disruptive risk factor. During the industry downcycle of 2022–2023, global semiconductor capex contracted by approximately 18% year-over-year, directly compressing ATE order books. Teradyne reported a 23% revenue decline in its semiconductor test segment during this period, illustrating how tightly ATE revenues track fab investment cycles.

Export control regulations constitute a growing structural constraint. U.S. Bureau of Industry and Security (BIS) restrictions on advanced semiconductor equipment exports to China — expanded in October 2023 — have created procurement uncertainty for Chinese IDMs and fabless companies, reducing addressable market access for U.S.-headquartered ATE vendors by an estimated 8–12% of their previously accessible China revenue base.

Component supply chain constraints, particularly for high-performance analog front-end ICs and precision timing components used within ATE platforms, added 12–16 weeks to equipment lead times during 2021–2022, delaying revenue recognition and compressing margin.

The competitive structure of the Automatic Test Equipment Market features a blend of dominant global incumbents and specialized regional players. Below is a profile of key participants:

Teradyne Inc.: The global revenue leader in semiconductor ATE, Teradyne holds an estimated 40–45% share of the memory and SoC test segments. Its UltraFLEX and Magnum platforms serve leading-edge foundries and IDMs across Asia Pacific and North America, and the company has aggressively invested in robotics and industrial automation as a strategic diversification vector.

Advantest Corporation.: Japan-based Advantest is the primary global competitor to Teradyne in memory and logic test, with a particularly strong position in DRAM test via its T5500 and T5800 series. The company benefits from deep integration with Japanese and South Korean memory manufacturers and has expanded into system-level test (SLT) to capture post-packaging validation demand.

Chroma ATE Inc.: A Taiwan-headquartered specialist, Chroma ATE focuses on power electronics, battery, and photovoltaic test systems. The company has carved a defensible niche in EV battery testing and renewable energy component validation, segments growing at rates exceeding the broader ATE market average.

National Instruments Corp.: Now operating under the Emerson umbrella following its 2023 acquisition, National Instruments Corp. offers modular, software-defined test platforms that appeal to defense electronics, telecommunications, and aerospace customers requiring highly configurable test architectures over standardized high-throughput solutions.

SPEA S.p.A.: An Italian ATE manufacturer specializing in flying probe testers and in-circuit test systems, SPEA S.p.A. holds significant market share in European automotive and industrial electronics testing, particularly among Tier 1 automotive suppliers operating in Germany, Italy, and France.

Marvin Test Solutions, Inc. (Marvin Engineering Co., Inc): A U.S. defense-sector specialist, Marvin Test Solutions focuses on military-grade ATE for avionics, radar, and electronic warfare systems, leveraging its PXI-based platforms to address complex multi-domain test requirements within the U.S. Department of Defense supply chain.

Roos Instruments, Inc.: Roos Instruments specializes in RF and mixed-signal semiconductor test, with a particular emphasis on wafer-level test solutions for wireless chipsets. Its Cassini platform addresses the high-parallelism requirements of Wi-Fi 6E and 5G RF component manufacturers.

Cal-Bay Systems, Inc. (Averna): Averna provides functional test and measurement solutions for telecommunications, automotive, and consumer electronics manufacturers. The company differentiates on integration services and test software customization rather than proprietary hardware platforms.

LTX-Credence (Cohu, Inc.): Cohu acquired LTX-Credence to consolidate its position in handler and contactor solutions alongside semiconductor test. The combined entity serves a broad base of analog, mixed-signal, and power device manufacturers, with particular strength in automotive-grade component test.

January 2023: Teradyne Inc. announced its UltraFLEXplus platform update targeting advanced packaging test, including 2.5D and 3D IC configurations, directly addressing the HBM3 test requirement emerging from AI GPU supply chains.

March 2023: Emerson Electric completed its $8.2 billion acquisition of National Instruments Corp., reshaping the modular ATE segment and creating a large industrial test conglomerate with combined revenues exceeding $18 billion.

June 2023: Advantest Corporation. unveiled the T2000 system-level test platform, designed for post-package validation of AI accelerator chips, reflecting the growing demand for SLT capacity driven by hyperscaler chip procurement.

October 2023: The U.S. Department of Commerce issued expanded export control rules under BIS, significantly restricting the sale of advanced semiconductor manufacturing and test equipment to Chinese entities, accelerating domestic Chinese ATE development initiatives.

February 2024: Chroma ATE Inc. launched a next-generation EV battery formation and test system capable of handling 800V battery architectures, targeting the premium BEV segment's expanding power electronics validation requirements.

May 2024: Cohu, Inc. reported a strategic partnership with a leading OSAT provider in Malaysia to co-develop advanced handler solutions optimized for fan-out wafer-level packaging (FO-WLP) test throughput.

September 2024: SPEA S.p.A. received a multi-unit contract from a Tier 1 European automotive supplier for flying probe test systems targeting ADAS sensor module production, valued at approximately €45 million.

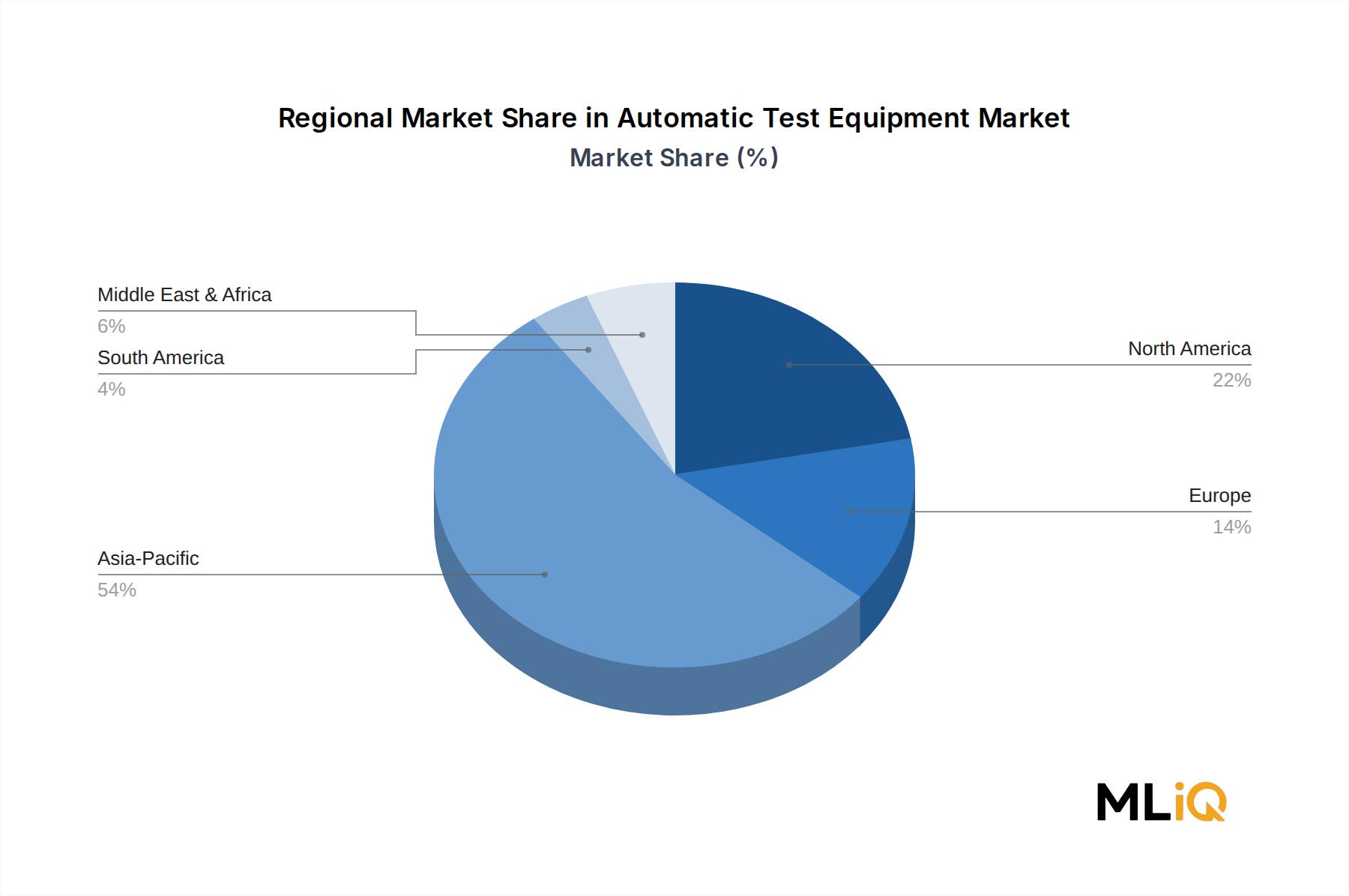

The Automatic Test Equipment Market exhibits pronounced regional concentration, with Asia Pacific serving as the dominant demand hub while North America and Europe demonstrate differentiated growth profiles driven by policy-backed onshoring initiatives.

Asia Pacific accounts for approximately 55–60% of global ATE revenue, driven by the density of semiconductor fabrication, OSAT, and electronics manufacturing in China, South Korea, Taiwan, Japan, and increasingly India and Southeast Asia. China alone represents roughly 20% of global ATE demand, though export control restrictions are beginning to bifurcate this market between permitted and restricted technology tiers. South Korea's dominance in memory manufacturing and Taiwan's foundry ecosystem sustain elevated per-capita ATE investment intensity. The Asia Pacific region is expected to grow at a CAGR of approximately 5.1% through 2033, making it both the largest and fastest-growing major region.

North America holds approximately 20–22% of global ATE revenue, underpinned by the defense and aerospace electronics sectors, fabless semiconductor design houses, and a rapidly expanding domestic fabrication capacity. The U.S. CHIPS and Science Act has committed over $52 billion in domestic semiconductor investment, with ATE procurement implications expected to materialize progressively between 2025 and 2028 as greenfield fabs come online. The North American market is projected to grow at a CAGR of 4.5%, slightly above the global average, driven by defense electronics and advanced packaging test demand.

Europe represents approximately 12–15% of global ATE revenue, with Germany, France, and the Netherlands serving as primary demand centers aligned with automotive electronics, industrial automation, and semiconductor equipment manufacturing. The European Chips Act's ambition to double Europe's global semiconductor market share to 20% by 2030 is creating forward demand signals for ATE investment, though near-term demand remains more modest than North America. Europe's ATE market is expected to grow at a CAGR of approximately 3.8% through 2033.

The Middle East and Africa region, while representing less than 3% of current ATE revenue, is emerging as an area of interest due to defense electronics modernization programs in GCC nations and Israel's established semiconductor R&D base. South America, led by Brazil, remains a marginal participant at below 2% global share, constrained by limited domestic semiconductor manufacturing infrastructure. Both regions are projected to grow at below-average CAGRs of 2.5–3.2%, primarily driven by defense procurement and technology service sector expansion rather than volume semiconductor manufacturing.

Environmental, social, and governance (ESG) imperatives are reshaping product development priorities, procurement criteria, and supply chain governance within the Automatic Test Equipment Market in ways that are accelerating beyond voluntary commitments into regulatory mandate territory.

Energy consumption is among the most scrutinized operational metrics. High-throughput ATE platforms — particularly memory test systems operating parallel test configurations — can consume between 20 kW and 150 kW per system. As semiconductor manufacturers face Science Based Targets initiative (SBTi) commitments and Scope 2 carbon reduction mandates, ATE energy efficiency has become a procurement criterion rather than merely a cost consideration. Teradyne and Advantest have both published roadmaps targeting double-digit percentage reductions in per-device-tested energy consumption through architectural optimization and dynamic power scaling.

Circular economy mandates in the European Union — particularly the Ecodes

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Automatic Test Equipment Market market expansion.

Key companies in the market include Teradyne Inc., Chroma ATE Inc., SPEA S.p.A., National Instruments Corp., Marvin Test Solutions, Inc. (Marvin Engineering Co., Inc, Roos Instruments, Inc., Cal-Bay Systems, Inc. (Averna), Advantest Corporation., LTX-Credence (Cohu, Inc.), .Shinbashi Inc..

The market segments include Type, Component, Industry Vertical.

The market size is estimated to be USD 7.91 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3707, USD 5760, and USD 10648 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Automatic Test Equipment Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automatic Test Equipment Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.