1. What are the major growth drivers for the Multi-Axis Sensor Market market?

Factors such as are projected to boost the Multi-Axis Sensor Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

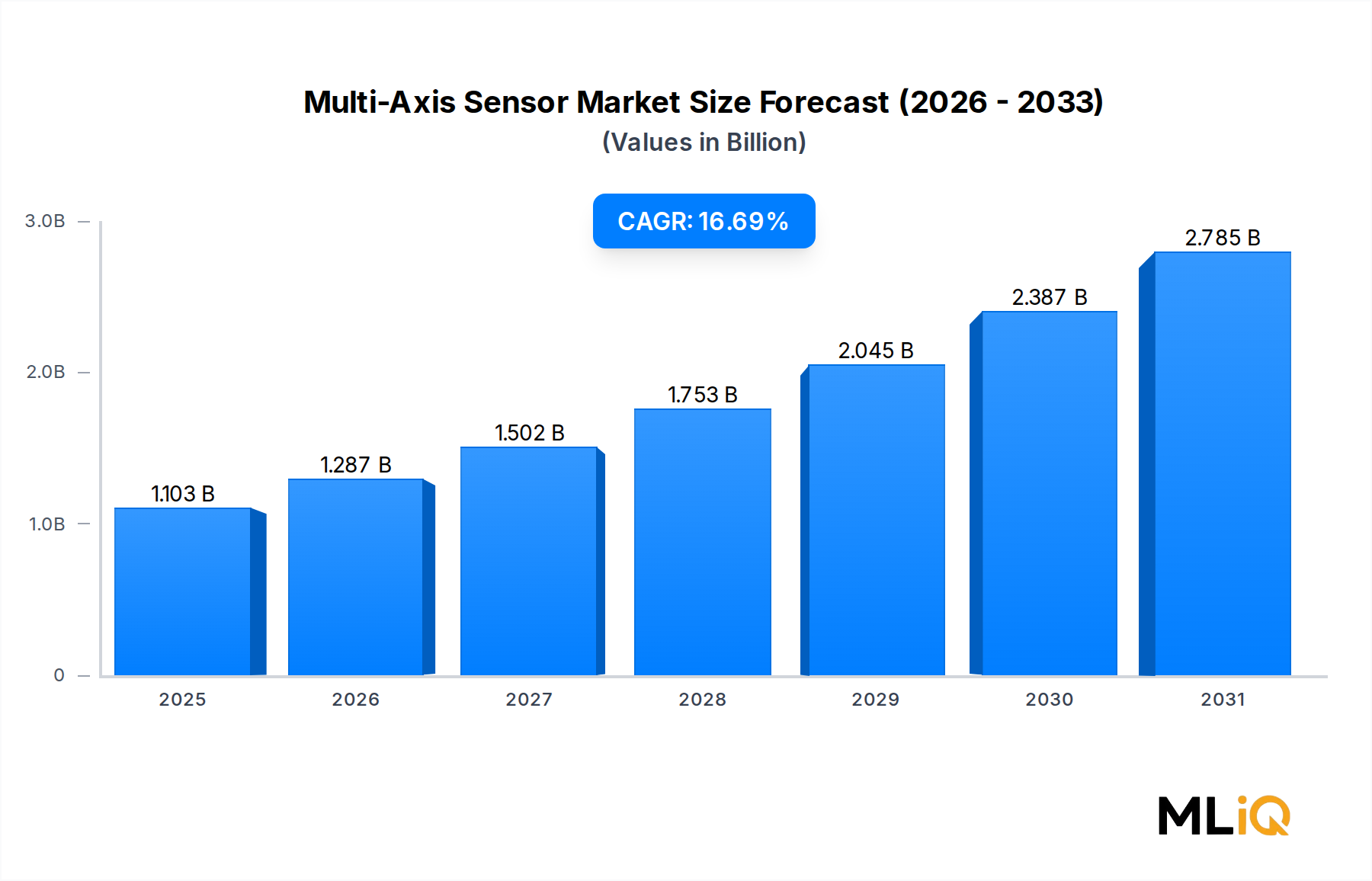

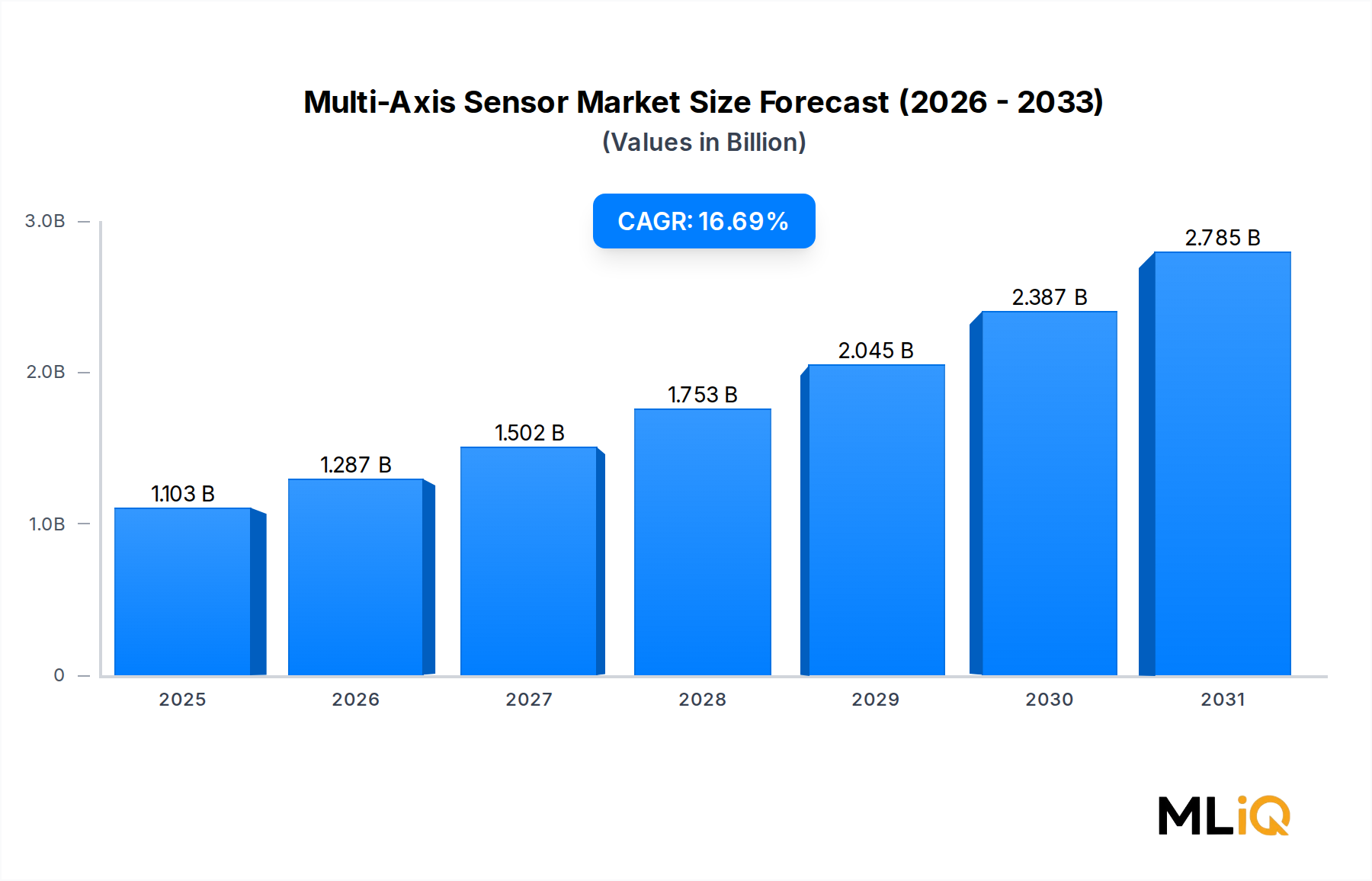

The global Multi-Axis Sensor Market is valued at $1,102.67 million as of the base assessment period and is forecast to expand at a compound annual growth rate of 16.7% through 2033, driven by the accelerating convergence of sensing, computing, and connectivity technologies across industrial, automotive, and consumer verticals. This trajectory places the market on a high-growth path, with cumulative investment and deployment activity expected to more than quadruple in absolute value terms by the end of the forecast window.

At the macro level, the proliferation of autonomous systems—ranging from self-driving vehicles and unmanned aerial vehicles to collaborative industrial robots—is fundamentally reshaping the demand profile for multi-axis sensing solutions. These platforms require precise, real-time measurement of force, torque, acceleration, angular velocity, and magnetic field orientation along multiple spatial axes simultaneously, a capability that single-axis architectures cannot deliver at the required resolution or latency. The integration of MEMS-based multi-axis sensors into edge-AI nodes further amplifies this demand, as on-device inferencing requires high-fidelity motion and orientation data streams.

Additionally, the continued miniaturization of sensor packages, driven by advances in wafer-level chip scale packaging and through-silicon via interconnects, is reducing bill-of-material costs and enabling deployment in form-factor-constrained applications such as hearables, smart patches, and sub-gram drones. The cost-per-axis metric has declined substantially over the past five years, opening previously price-sensitive consumer and medical wearable segments to multi-axis adoption.

From a demand-driver standpoint, the automotive sector's shift toward ADAS Level 2+ and Level 4 autonomy is particularly consequential. Regulatory mandates in the European Union and North America requiring electronic stability control, lane-keeping assist, and automatic emergency braking all necessitate robust multi-axis inertial sensing. Similarly, Industry 4.0 deployments are embedding multi-axis force-torque sensors into robotic end-effectors and CNC machine tool spindles to enable real-time process control and predictive maintenance.

Geopolitically, reshoring initiatives in North America and Europe are catalyzing domestic semiconductor fabrication investments that will indirectly benefit the multi-axis sensor supply chain by reducing lead times and single-source dependencies. Meanwhile, Asia Pacific remains the dominant volume market, with China, Japan, and South Korea collectively accounting for the majority of MEMS sensor fabrication capacity globally.

Looking forward to 2033, the market is expected to achieve strong double-digit growth in every major region, with the fastest expansion anticipated in Asia Pacific and the Middle East and Africa corridors, where smart city infrastructure and defense modernization programs are accelerating sensor adoption. North America and Europe will sustain premium revenue positions driven by high-value aerospace, defense, and industrial automation deployments.

Among all product types within the multi-axis sensing landscape, MEMS Accelerometers represent the single largest revenue-generating segment, commanding a dominant share of the overall market at the base year valuation of $1,102.67 million. This dominance stems from a combination of mature manufacturing economics, broad application versatility, and deeply embedded design wins across consumer electronics, automotive, and industrial verticals.

MEMS accelerometers measure acceleration forces along multiple axes—typically two or three—by detecting the displacement of a proof mass suspended on micro-fabricated springs within a silicon substrate. Their ability to measure both dynamic acceleration (vibration, shock) and static acceleration (gravitational orientation) in a single package makes them uniquely suited for applications spanning tilt sensing, gesture recognition, vehicle crash detection, and structural health monitoring.

In the consumer electronics vertical, MEMS accelerometers are ubiquitous components in smartphones, tablets, gaming controllers, and wearable fitness devices. Every major smartphone platform embeds at least a three-axis accelerometer to enable screen rotation, step counting, and motion-triggered wake functions. The global smartphone shipment volume—exceeding one billion units annually—ensures sustained baseline demand that provides market stability even as unit ASPs face downward pressure from commoditization.

In the automotive vertical, MEMS accelerometers are deployed in airbag deployment systems, electronic stability control modules, tire pressure monitoring systems, and increasingly in ADAS sensor fusion stacks. Modern vehicles incorporate anywhere from six to more than twenty discrete accelerometer channels, depending on the level of autonomous functionality. The transition toward electric vehicles is additive rather than substitutive for multi-axis accelerometer content, as battery management systems and regenerative braking controllers rely on high-precision inertial data.

In the industrial vertical, MEMS accelerometers are embedded in condition monitoring nodes attached to rotating machinery, conveyor systems, and structural beams. Predictive maintenance platforms aggregate vibration signatures from multi-axis accelerometers to detect bearing faults, misalignment, and imbalance conditions weeks before catastrophic failure, delivering substantial operational cost savings. The Industrial Internet of Things buildout is driving wireless, battery-powered accelerometer node deployments at scale, with the addressable installation base for industrial vibration monitoring sensors measured in the tens of millions of endpoints globally.

Key players active in this segment include STMicroelectronics, Texas Instruments Inc., and Honeywell International Inc., each of which maintains vertically integrated MEMS fabrication capabilities. STMicroelectronics holds particularly strong design-win depth in consumer and automotive accelerometer platforms, benefiting from its dual-fab model across Agrate Brianza and Crolles. Texas Instruments competes on signal conditioning integration, offering accelerometers with embedded digital interfaces that reduce system-level BOM complexity.

The segment's share is consolidating around a smaller number of Tier 1 MEMS foundry-integrated suppliers, as the capital intensity of sub-micron MEMS process nodes creates meaningful barriers to new entrants. However, niche differentiation opportunities persist in high-g shock sensing (above 50,000 g), cryogenic temperature operation, and radiation-hardened variants for aerospace applications, where specialized players such as Jewell Instruments and Interface Inc. maintain defensible positions.

Overall, MEMS accelerometers are expected to sustain their dominant revenue position through 2033, with their share potentially expanding as three-axis combo sensors increasingly displace two-axis and single-axis architectures across all major verticals.

The Multi-Axis Sensor Market is propelled by a set of structurally durable demand drivers while simultaneously navigating a distinct set of supply-side and regulatory constraints that modulate its growth trajectory.

The primary driver is the accelerating adoption of autonomous and semi-autonomous systems across automotive and industrial verticals. Global ADAS sensor content per vehicle is projected to grow at rates exceeding 20% annually through the mid-2030s, with multi-axis inertial sensors serving as the backbone of sensor fusion architectures in Level 2 through Level 4 autonomous driving platforms. Regulatory mandates in the EU requiring automatic emergency braking systems in all new passenger vehicles from 2024 onward have created a structural, non-discretionary demand floor for automotive multi-axis sensors.

The second major driver is the expansion of consumer wearables and hearables, a segment in which global unit shipments surpassed 500 million devices annually and continue to grow. Each device typically incorporates a six-axis or nine-axis inertial measurement unit combining accelerometer, gyroscope, and magnetometer functionality, driving MEMS multi-axis sensor demand in high volumes at competitive price points.

Industrial robotics represents a third structural driver. The global installed base of industrial robots exceeded 3.9 million units by the early 2020s, with annual installation rates growing at approximately 10% per year according to the International Federation of Robotics. Collaborative robots in particular require high-bandwidth, multi-axis force-torque sensing at their wrist joints to enable safe human-robot interaction, a capability that ATI Industrial Automation and Interface Inc. actively address.

On the constraint side, the primary challenge is supply chain concentration. A significant proportion of MEMS fabrication capacity is geographically concentrated in Asia Pacific, particularly in China, Taiwan, and Japan. Geopolitical tensions and export control regulations—including U.S. Bureau of Industry and Security restrictions on advanced semiconductor technology transfers—introduce procurement risk for end customers in defense and aerospace applications, compelling a bifurcation of supply chains that adds cost and complexity. Additionally, the technical complexity of calibrating and compensating multi-axis sensors for cross-axis sensitivity, temperature drift, and vibration rectification error imposes non-trivial NRE costs on system integrators.

The competitive landscape of the Multi-Axis Sensor Market is characterized by a mix of vertically integrated MEMS specialists, diversified electronics conglomerates, and precision instrumentation niche players. The following profiles capture the strategic positioning of the primary participants identified in the market data:

ATI Industrial Automation, Inc.: A leading supplier of robotic force-torque sensors and multi-axis tool changers, ATI commands a strong position in collaborative and industrial robot end-effector sensing, with products designed for real-time torque feedback in assembly and machining applications.

Parker Hannifin: A diversified motion and control conglomerate, Parker Hannifin integrates multi-axis sensing into its broader fluid power and electromechanical systems portfolio, serving aerospace, industrial, and mobile equipment markets with high-reliability sensing solutions.

Trimble Navigation Limited: Specializing in precision positioning and geospatial technologies, Trimble deploys multi-axis inertial sensors within its GNSS-augmented navigation and machine control platforms, targeting surveying, agriculture, and construction verticals.

L3Harris Technologies, Inc.: A premier defense electronics integrator, L3Harris develops ruggedized multi-axis inertial sensing systems for guided munitions, aircraft navigation, and unmanned system applications under stringent MIL-SPEC performance requirements.

STMicroelectronics: A global MEMS foundry and fabless-integrated supplier, STMicroelectronics maintains one of the broadest portfolios of multi-axis MEMS inertial sensors in the industry, with design wins across consumer, automotive, and industrial customers on every inhabited continent.

Texas Instruments Inc.: Leveraging its analog signal chain expertise, Texas Instruments provides multi-axis inertial sensors with integrated digital interfaces and onboard processing, reducing system complexity for industrial and automotive customers.

Aeron Systems Private Limited: An Indian aerospace-focused sensor manufacturer, Aeron Systems develops multi-axis inertial measurement and navigation systems for UAVs, guided projectiles, and aerospace platforms under domestic defense procurement programs.

Jewell Instruments: A precision inclinometer and inertial sensor specialist, Jewell Instruments serves niche high-accuracy applications in seismic monitoring, precision leveling, and aerospace testing where conventional MEMS solutions lack sufficient resolution.

Interface Inc.: A force measurement technology leader, Interface Inc. designs multi-axis load cells and force-torque sensors used in aerospace structural testing, automotive durability evaluation, and robotic calibration facilities.

Honeywell International Inc.: A major aerospace and industrial conglomerate, Honeywell supplies radiation-hardened and high-reliability multi-axis inertial reference units for commercial aviation, defense navigation, and space vehicle guidance applications.

January 2024: STMicroelectronics announced a new generation of six-axis IMU devices featuring an onboard machine learning core capable of executing gesture recognition algorithms at under 0.5 mA active current, targeting smartwatch and hearable applications.

March 2024: Honeywell International Inc. disclosed a multi-year contract with a North American defense prime contractor to supply radiation-hardened, nine-axis inertial measurement units for next-generation tactical missile guidance systems.

May 2024: Texas Instruments Inc. released an updated family of multi-axis vibration sensors with integrated analog front-end signal conditioning optimized for industrial condition monitoring nodes operating in environments up to 125°C.

August 2024: ATI Industrial Automation, Inc. unveiled a new compact six-axis force-torque sensor series with an integrated Ethernet/IP interface, designed specifically for collaborative robot wrist mounting at payload capacities below 10 kg.

October 2024: Parker Hannifin completed a strategic technology partnership with a European automotive Tier 1 supplier to co-develop multi-axis inertial sensing modules compliant with ASIL-D functional safety requirements under ISO 26262.

December 2024: L3Harris Technologies, Inc. received FAA certification for an upgraded multi-axis attitude and heading reference system deployed across a major regional commercial aviation platform, marking a key milestone in avionics sensing modernization.

February 2025: Trimble Navigation Limited integrated a new nine-axis MEMS inertial sensing module into its flagship machine control platform, reducing position update latency by 40% in GNSS-denied urban canyon environments.

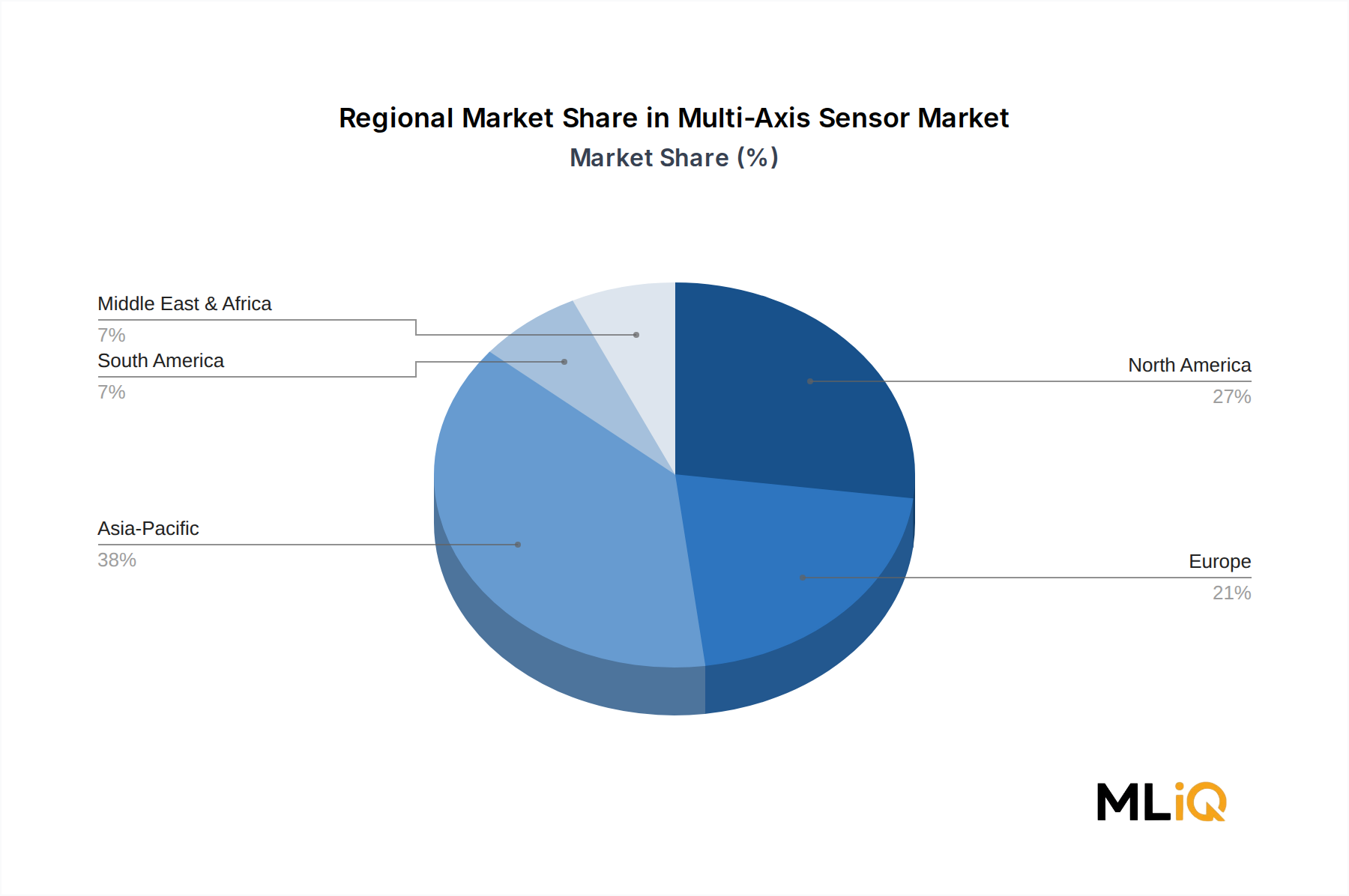

The Multi-Axis Sensor Market exhibits distinct regional growth dynamics shaped by industrial base composition, regulatory environments, defense spending levels, and consumer electronics production capacity.

Asia Pacific is the dominant region by revenue share, capturing an estimated 38–42% of global market value at the base year, underpinned by China's massive consumer electronics manufacturing ecosystem, Japan's precision industrial robotics sector, South Korea's semiconductor and display supply chain, and ASEAN's emerging automotive production base. China alone hosts the largest concentration of MEMS sensor fabrication fabs globally, enabling tight integration between sensor manufacture and downstream electronics assembly. The region is forecast to sustain a CAGR of approximately 18–19% through 2033, driven by EV adoption, smart factory investment under Made in China 2025 successor programs, and defense modernization spending across India and Southeast Asia.

North America holds the second-largest revenue share at approximately 28–30% of the global total, with the United States dominating on the strength of its aerospace and defense procurement programs, advanced robotics sector, and automotive R&D investment concentrated in Michigan, California, and Texas. The U.S. Department of Defense's sustained investment in autonomous systems and precision-guided munitions is a structural demand anchor. North America is forecast to grow at a CAGR near 14–15%, slightly below the global average, reflecting its relative market maturity.

Europe accounts for approximately 20–22% of global revenues, led by Germany's automotive and industrial machinery sectors, France's aerospace and defense ecosystem, and the United Kingdom's advanced defense electronics base. EU regulatory mandates around vehicle safety and industrial workplace automation are compelling OEM sensor content upgrades across the board. Europe is projected to expand at a CAGR of approximately 13–15% through 2033.

The Middle East and Africa region, while currently the smallest market at approximately 4–6% of global revenue, is positioned as the fastest-emerging growth corridor after Asia Pacific. GCC nations' smart city investments and expanding defense procurement budgets—particularly in the UAE, Saudi Arabia, and Israel—are driving multi-axis sensor adoption in surveillance drones, autonomous ground vehicles, and precision agriculture systems. CAGR estimates for MEA range from 17–21% through 2033.

South America contributes approximately 4–5% of global revenues, with Brazil as the primary market driven by automotive production and agri-tech sensor deployments. Regional growth is forecast at approximately 12–14%, constrained by macroeconomic volatility and lower defense spending relative to GDP.

Global trade flows in the Multi-Axis Sensor Market are heavily shaped by the geographic concentration of MEMS semiconductor fabrication and the downstream distribution networks that route finished sensor modules to OEM customers worldwide. The primary export corridors run from Asia Pacific manufacturing hubs—principally China, Taiwan, Japan, and South Korea—toward North America and Europe, where the largest high-value end-use industries in automotive, aerospace, and industrial automation are concentrated.

China is simultaneously the world's largest exporter of low-to-mid tier MEMS sensor components and a significant importer of high-precision, defense-grade multi-axis inertial modules from the United States and Europe, a bifurcation driven by export control regimes. The U.S. Bureau of Industry and Security's Entity List restrictions and Export Administration Regulations impose

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.7% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Multi-Axis Sensor Market market expansion.

Key companies in the market include ATI Industrial Automation, Inc., Parker Hannifin, Trimble Navigation Limited, L3Harris Technologies, Inc., STMicroelectronics, Texas Instruments Inc., Aeron Systems Private Limited, Jewell Instruments, Interface Inc., Honeywell International Inc..

The market segments include Type, Vertical.

The market size is estimated to be USD 1102.67 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Multi-Axis Sensor Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Multi-Axis Sensor Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.