Dominance of Cleaners Segment in the Seed Processing Machines Market

Among all equipment types in the seed processing machines market, the Cleaners segment consistently commands the largest share of revenues, a position rooted in the fundamental agronomic and commercial necessity of removing impurities from seed lots before any downstream processing can take place. Cleaners occupy the earliest and most indispensable stage of any seed processing workflow, making their procurement effectively non-discretionary for seed companies, agricultural cooperatives, and government seed certification agencies alike.

Seed cleaning encompasses the separation of seeds from chaff, weed seeds, broken kernels, dust, stones, and other foreign matter using a combination of air classification, oscillating screens, and gravity separation principles. The universality of this requirement across all crop categories — cereals, oilseeds, pulses, vegetables, and turf grasses — ensures that cleaners are installed in virtually every seed processing facility globally, regardless of scale or geographic location. This broad applicability creates a demand base that is both wide and relatively inelastic compared to more specialized equipment categories such as coaters or polishers.

The segment's dominance is further reinforced by replacement and upgrade cycles. Cleaning machines, particularly high-throughput air-screen cleaners, are subject to significant wear from continuous operation and abrasive seed materials. Consumable components including screens, brushes, and air intake filters require periodic replacement, generating recurring aftermarket revenue streams that complement initial equipment sales. This installed-base dynamic incentivizes manufacturers to prioritize cleaners in their product portfolios as a platform for building long-term customer relationships.

Key players competing for leadership within the Cleaners segment include Cimbria A/S, PETKUS Technologie, Westrup, and Alvan Blanch Development Company. Cimbria A/S, headquartered in Denmark, has established particularly strong positioning through its modular CIMBRIA HEID range, which allows customers to configure cleaning capacity to specific throughput requirements. PETKUS Technologie leverages decades of German engineering heritage to offer high-precision, multi-stage cleaning lines favored by large commercial seed producers in Europe and North America. Westrup, another Danish manufacturer, has built significant market share in Asia Pacific and the Middle East through competitive pricing and robust distributor networks.

The Cleaners segment is also benefiting from a wave of technology upgrades driven by the broader digitalization of seed processing. Modern cleaner platforms increasingly incorporate real-time sensors that monitor output purity levels and automatically adjust air velocity and screen oscillation parameters to maintain target separation efficiency. This capability reduces dependence on skilled operators — directly addressing one of the market's key structural pain points — and enables remote diagnostics that lower maintenance costs. As a result, the segment is not merely maintaining its dominance but is actively expanding its value proposition and revenue per unit.

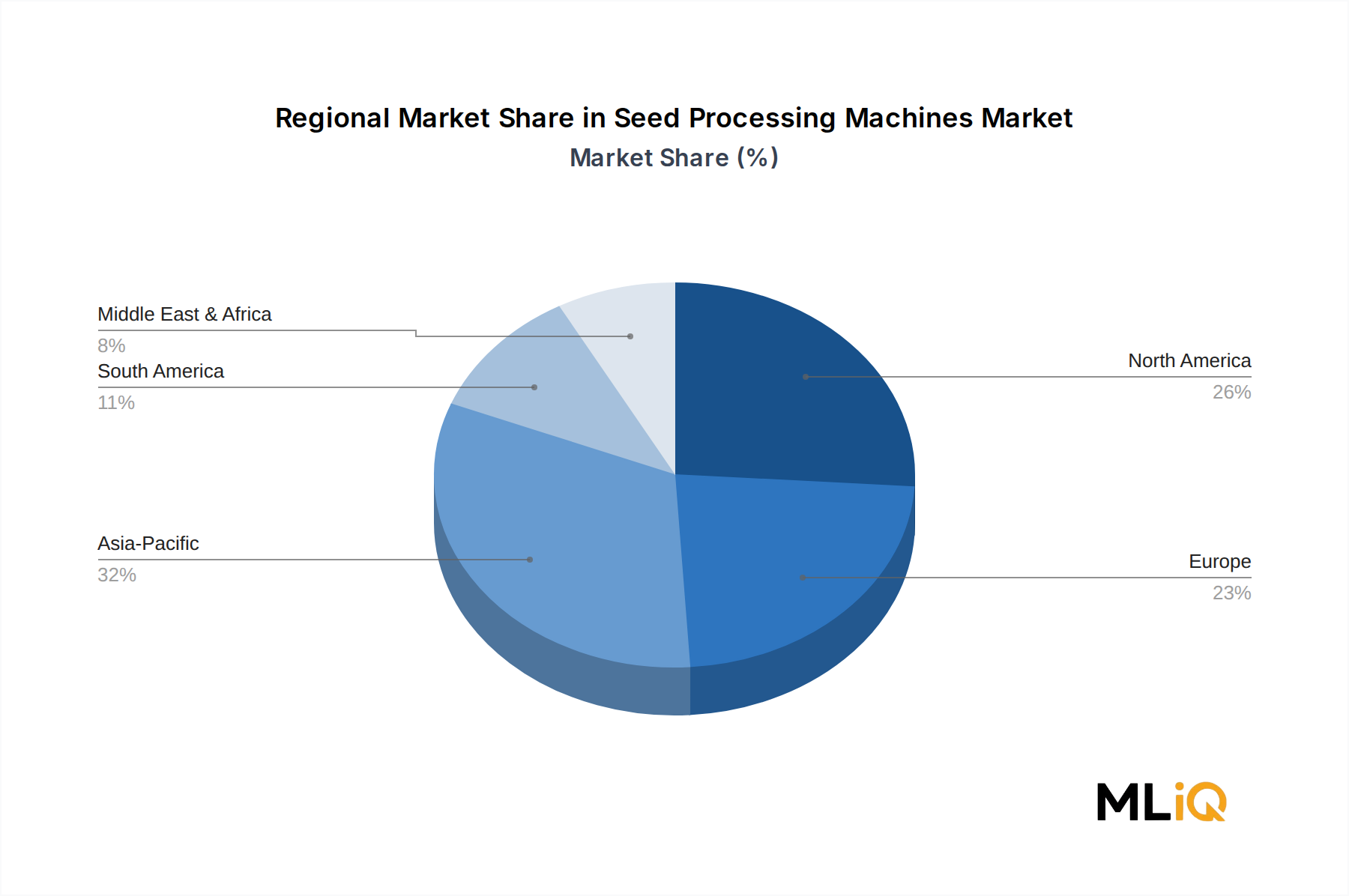

Geographically, the strongest demand for cleaners is concentrated in Asia Pacific, where the combination of large cultivated area, diverse crop mix, and government-driven seed certification programs creates a particularly favorable demand environment. India's national seed policy and China's ongoing seed industry consolidation have both generated large procurement orders for industrial-scale cleaning equipment in recent years. North America and Europe represent mature but high-value markets where the emphasis is shifting toward high-precision, automation-integrated cleaner systems rather than volume-driven replacement purchases.

The segment's share is consolidating rather than fragmenting, as leading manufacturers increasingly differentiate through software platforms, IoT connectivity, and service contracts rather than through hardware specifications alone. Smaller regional manufacturers face mounting competitive pressure to either specialize in niche crop applications or form distribution partnerships with global equipment groups to remain commercially viable.