1. What are the major growth drivers for the Satellite Market market?

Factors such as are projected to boost the Satellite Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

Satellite Market

Satellite Market+1 2315155523

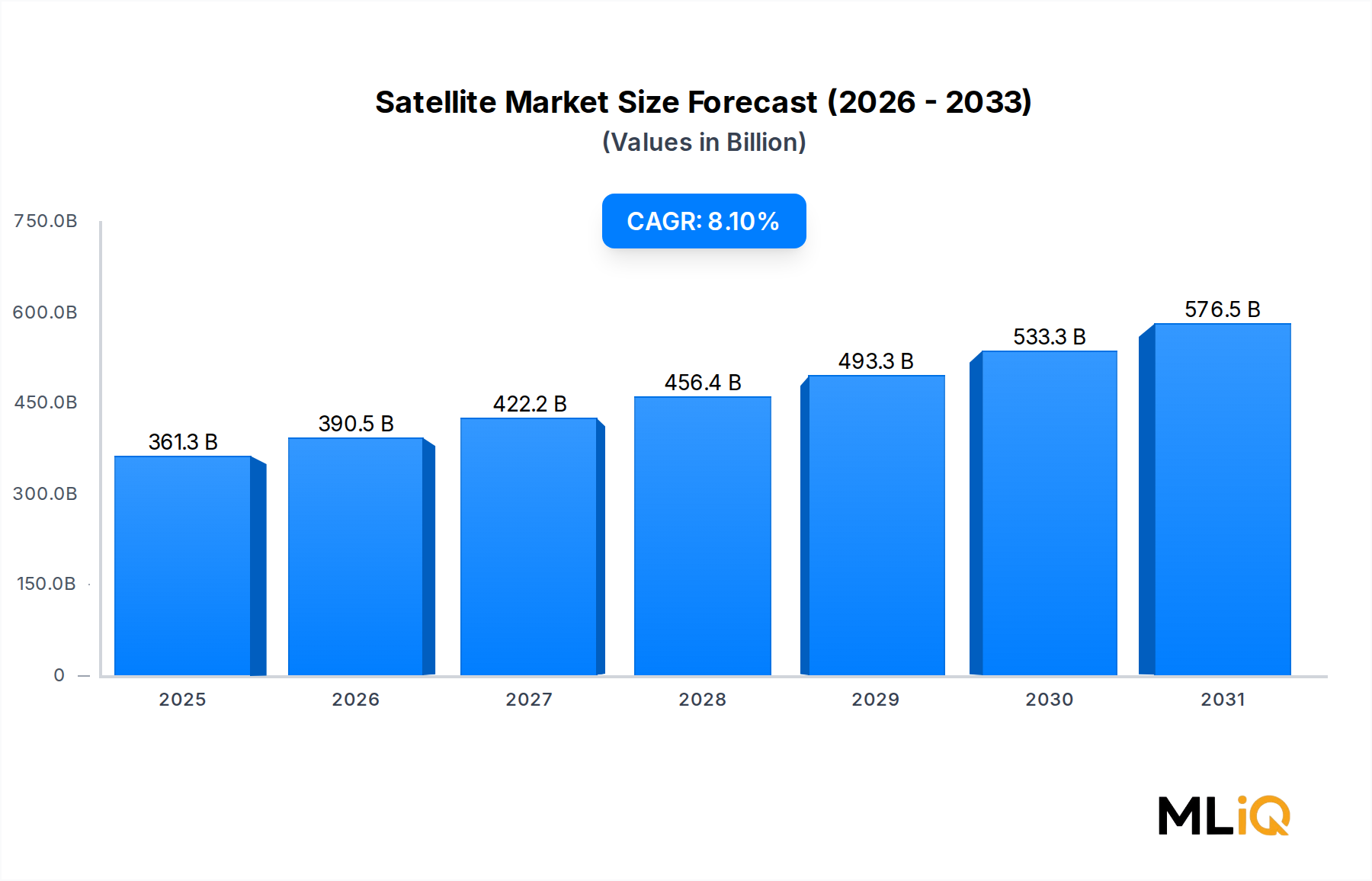

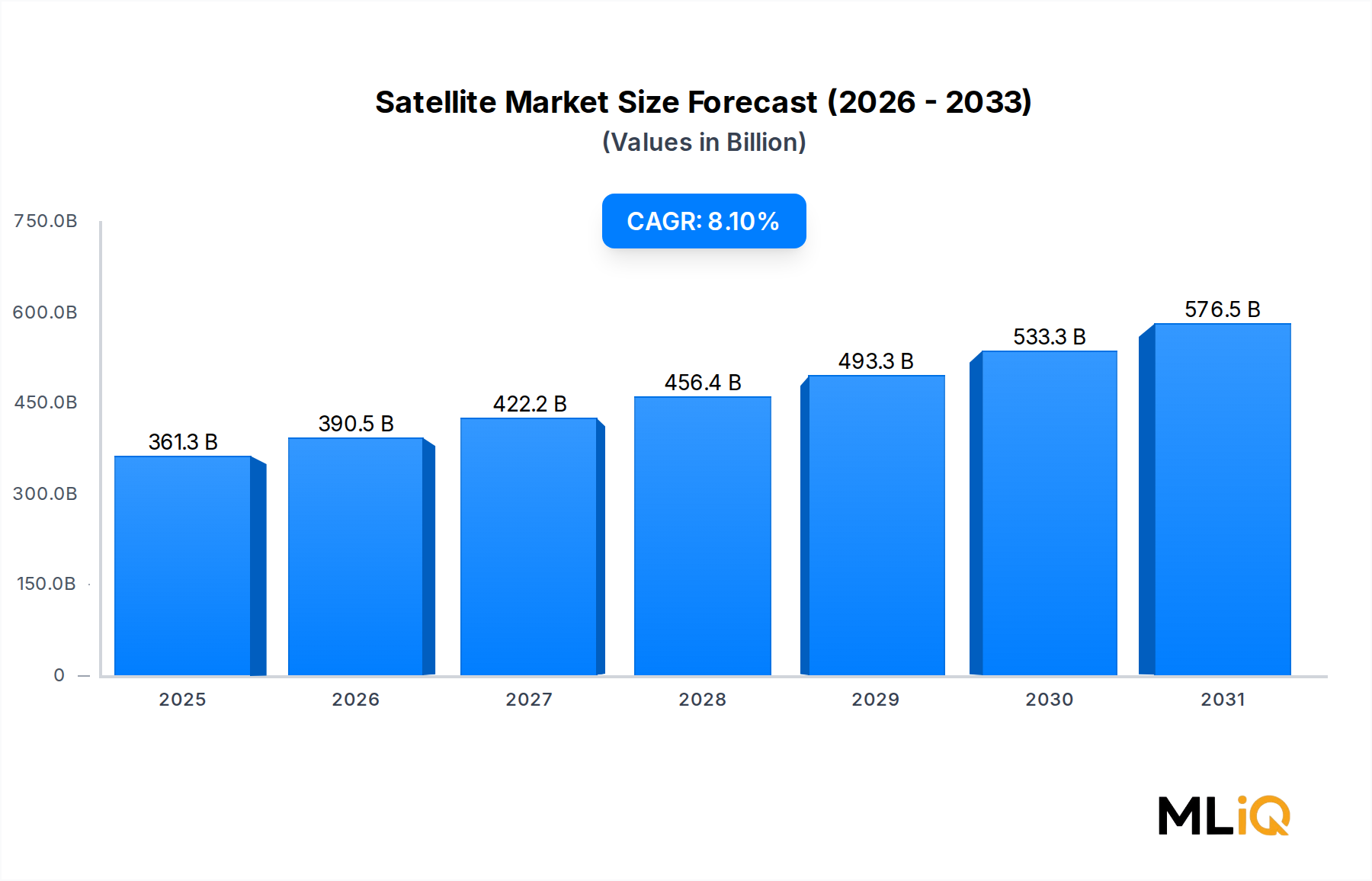

The global Satellite Market is valued at $361.28 billion as of the base year and is projected to expand at a compound annual growth rate (CAGR) of 8.1% through the forecast period of 2025 to 2033. This trajectory reflects a sustained elevation in demand across commercial, governmental, and military end-use verticals, underpinned by accelerating digitalization, geopolitical imperatives, and the democratization of space access driven by reusable launch technologies.

At its core, the market is being reshaped by three macro tailwinds. First, the proliferation of low Earth orbit (LEO) mega-constellations has fundamentally altered the economics of satellite deployment, compressing per-unit manufacturing costs and enabling broadband connectivity for previously underserved geographies. Second, government-led initiatives across North America, Europe, and Asia Pacific are directing significant capital toward sovereign satellite infrastructure, spanning Earth observation, navigation, and secure military communications. Third, the commercialization of space has opened entirely new revenue streams, including space tourism logistics, on-orbit servicing, and in-space manufacturing, all of which depend on satellite infrastructure as a backbone.

Demand drivers span a broad spectrum. The accelerating adoption of Internet of Things (IoT) devices requiring real-time data transmission, the expansion of autonomous vehicle ecosystems dependent on precision satellite navigation, and the surge in remote-sensing applications for climate monitoring and precision agriculture are all channeling investment into satellite infrastructure. The growing need for resilient, unjammable communications in defense contexts — particularly in light of recent conflicts that have highlighted the strategic value of satellite communications — has further elevated military procurement budgets globally.

From a forward-looking perspective, the Satellite Market is entering a phase of structural transformation. The convergence of artificial intelligence with satellite data analytics, the maturation of software-defined satellite platforms, and the emergence of on-orbit servicing and refueling capabilities are expected to extend satellite operational lifecycles and reduce total cost of ownership. Meanwhile, the small satellite segment is democratizing access for emerging market governments and private enterprises alike, diversifying the customer base well beyond traditional defense and telecommunications primes. By 2033, the market is expected to represent a substantially larger share of global aerospace expenditure, cementing its position as one of the most dynamic verticals within the broader Aerospace and Defense Market.

Within the functional segmentation of the Satellite Market — spanning satellite services, ground equipment, satellite manufacturing, and satellite launch — the satellite services segment commands the largest revenue share. This dominance is not incidental but structurally entrenched, reflecting the recurring, subscription-based revenue model that distinguishes services from the capital-intensive, project-driven economics of manufacturing and launch.

Satellite services encompass a wide array of offerings: fixed satellite services (FSS), mobile satellite services (MSS), direct-to-home (DTH) broadcasting, broadband internet via satellite, and managed network services for enterprise and government clients. The recurring nature of these revenues — typically delivered under multi-year contracts — provides a level of revenue visibility that is unmatched by hardware-oriented segments, making it the preferred investment target for institutional capital and the highest-margin contributor to integrated satellite operators.

The shift toward LEO-based broadband services has catalyzed a significant expansion of the total addressable market for satellite services. Operators including SPACEX, through its Starlink constellation, have demonstrated that consumer-grade broadband delivered via LEO satellites can achieve latency profiles comparable to terrestrial fiber in many use cases, unlocking demand from maritime, aviation, enterprise mobility, and rural connectivity segments. This has pressured legacy geostationary (GEO) operators to reposition their service portfolios, invest in high-throughput satellite (HTS) capacity, and form strategic partnerships with LEO operators to offer hybrid solutions.

SES S.A. exemplifies this transition, having committed to its O3b mPOWER medium Earth orbit (MEO) constellation to deliver high-throughput, low-latency services to maritime and enterprise clients. Intelsat has similarly pivoted, leveraging its legacy GEO fleet while pursuing next-generation capacity investments. Inmarsat Global Limited continues to hold a differentiated position in mobile satellite services for aviation and maritime verticals, where its L-band spectrum assets provide unmatched global coverage reliability.

The communication application sub-segment underpins the majority of satellite services revenue. Broadband connectivity for underserved regions, voice and data services for maritime and aviation, and government-grade secure communications collectively represent the demand engine for this segment. Earth observation-as-a-service models are also gaining ground, enabling commercial entities and government agencies to procure imagery and analytics on a subscription basis rather than commissioning dedicated satellites, further expanding the services revenue pool.

The market share held by the satellite services segment is not merely maintaining its position — it is consolidating. As LEO constellations scale their subscriber bases and enterprise clients migrate toward managed satellite network services, the proportion of total Satellite Market revenue attributable to services is projected to increase through 2033. This consolidation is being reinforced by vertical integration strategies, wherein operators such as SPACEX own the entire stack from manufacturing through launch to service delivery, capturing margin at every layer and creating formidable competitive barriers for standalone service providers.

Key players within this segment — including SES S.A., Intelsat, Inmarsat Global Limited, and emerging LEO operators — are competing not merely on coverage but on service quality, latency, reliability, and integration with terrestrial network infrastructure. The segment's dominance is therefore both a reflection of current market structure and a forward indicator of where incremental value creation will concentrate over the forecast horizon.

The Satellite Market's projected 8.1% CAGR through 2033 is driven by a constellation of quantifiable forces, balanced against structural and regulatory constraints that merit rigorous assessment.

Primary drivers include the exponential growth of LEO constellation deployments. As of recent tallies, over 7,000 active satellites orbit Earth, with LEO constellations accounting for the majority of new deployments. SPACEX's Starlink alone has launched over 5,000 satellites and continues to expand capacity, directly stimulating demand across satellite manufacturing, ground equipment, and launch services sub-segments.

Defense spending is a second high-magnitude driver. NATO members have pledged to increase defense budgets to at least 2% of GDP, with satellite communications and space situational awareness receiving disproportionate allocation. The United States Space Force budget exceeded $30 billion in fiscal year 2024, a significant portion of which is directed toward satellite procurement, launch, and ground segment modernization. This creates durable, long-cycle demand that insulates the Satellite Market from short-term commercial demand fluctuations.

The proliferation of IoT devices — projected to surpass 30 billion connected units globally by 2030 — is driving demand for satellite-based connectivity in geographies where terrestrial networks are economically unviable. Direct-to-device satellite connectivity, enabled by non-terrestrial network (NTN) standards within 3GPP Release 17 and beyond, is poised to expand the addressable market substantially.

On the constraint side, orbital congestion and radio frequency (RF) spectrum scarcity represent material limitations. The International Telecommunication Union (ITU) filing backlog and inter-operator coordination requirements introduce multi-year delays in constellation deployment timelines. Space debris poses an escalating collision risk: the European Space Agency estimates over 36,500 debris objects larger than 10 cm currently in orbit, necessitating active debris removal investments that add cost without direct revenue generation. Regulatory fragmentation across jurisdictions further complicates spectrum licensing, foreign ownership restrictions, and launch approval processes for globally operating operators.

The competitive landscape of the Satellite Market is characterized by a blend of vertically integrated space primes, specialist operators, and emerging new-space challengers:

SPACEX: The undisputed disruptor of the Satellite Market, SPACEX combines reusable Falcon 9 and Falcon Heavy launch vehicles with its Starlink LEO broadband constellation, creating a vertically integrated model that has compressed launch costs and accelerated satellite deployment timelines industry-wide.

Northrop Grumman Corporation: A leading defense-oriented satellite manufacturer and on-orbit servicing pioneer, Northrop Grumman Corporation operates the Mission Extension Vehicle (MEV) program, enabling life extension for aging GEO satellites and opening a new service category within the market.

Inmarsat Global Limited: A specialist in mobile satellite services for aviation and maritime verticals, Inmarsat Global Limited holds valuable L-band and Ka-band spectrum assets and has been integrated into Viasat's portfolio, enhancing hybrid GEO-LEO service capabilities.

Boeing: A diversified aerospace and defense prime, Boeing delivers advanced military and commercial satellites including the GPS III ground control segment and proprietary GEO communication platforms for government clients.

Intelsat: One of the largest GEO satellite fleet operators globally, Intelsat has navigated financial restructuring and is investing in C-band spectrum clearing proceeds to fund next-generation satellite capacity and hybrid orbit service architectures.

Airbus: Through its Airbus Defence and Space division, Airbus designs and manufactures communication, Earth observation, and navigation satellites, including the European Galileo navigation constellation, positioning it as a cornerstone of European sovereign space capability.

SES S.A.: A dual-orbit operator with both GEO and MEO assets, SES S.A. is executing a growth strategy anchored on its O3b mPOWER MEO constellation targeting enterprise and government broadband applications with high-throughput, low-latency performance.

Lockheed Martin Corporation: A major U.S. defense prime, Lockheed Martin Corporation produces advanced military satellite systems including GPS III satellites and protected military satellite communications (MILSATCOM) platforms for the U.S. government.

Safran SA: Contributing critical satellite propulsion and navigation components, Safran SA occupies a strategic position in the supply chain for both European and international satellite programs.

L3Harris Technologies, Inc.: Specializing in intelligence, surveillance, and reconnaissance (ISR) satellite payloads and ground systems, L3Harris Technologies, Inc. serves as a key supplier to U.S. government and allied defense satellite programs.

January 2024: SPACEX surpassed 5,000 active Starlink satellites in orbit, achieving a milestone that enabled global broadband coverage including polar regions, significantly expanding its commercial and government subscriber base.

March 2024: The European Union formally adopted the IRIS² satellite constellation program, committing over 6 billion euros toward a sovereign European LEO broadband infrastructure designed to reduce dependence on non-European operators for secure government communications.

May 2024: Northrop Grumman Corporation successfully completed its second Mission Extension Vehicle docking with a Intelsat GEO satellite, demonstrating commercial on-orbit servicing viability and signaling a shift toward satellite life-extension as a mainstream service offering.

July 2024: SES S.A. completed the acquisition of Intelsat, creating one of the world's largest satellite fleet operators with combined assets spanning GEO and MEO orbits, generating significant regulatory and strategic attention across the Satellite Market.

September 2024: India's ISRO successfully launched its NVS-02 navigation satellite aboard the GSLV Mk II rocket, advancing the NavIC regional satellite navigation system and marking a key milestone in India's push for satellite navigation sovereignty.

November 2024: L3Harris Technologies, Inc. was awarded a multi-year contract by the U.S. Space Force valued at over $1.2 billion for next-generation protected satellite communication payload development, underscoring the continued elevation of military satellite budgets.

February 2025: Amazon's Project Kuiper successfully deployed its first batch of 27 production satellites, signaling the entry of a formidable new competitor into the LEO broadband segment with over 3,200 satellites planned for full constellation deployment.

The Satellite Market exhibits pronounced regional differentiation, with maturity levels, growth rates, and demand drivers varying significantly across geographies.

North America represents the largest regional market by revenue share, accounting for an estimated 38% of global Satellite Market revenue. The United States anchors this dominance through its unparalleled private-sector innovation ecosystem — led by SPACEX, Boeing, Lockheed Martin Corporation, and Northrop Grumman Corporation — combined with the world's largest defense satellite procurement budget. The U.S. Space Force and National Reconnaissance Office sustain consistent demand for advanced military satellite systems. North America is expected to maintain a CAGR of approximately 7.5% through 2033, reflecting market maturity tempered by sustained defense investment and commercial LEO expansion.

Asia Pacific is the fastest-growing regional segment, projected at a CAGR exceeding 10% through 2033. China's state-led space program is aggressively expanding its Beidou navigation constellation, remote sensing capabilities, and a planned LEO broadband constellation targeting over 13,000 satellites. India's commercial space liberalization — including the establishment of IN-SPACe to facilitate private sector participation — is catalyzing domestic satellite manufacturing and launch investment. Japan and South Korea are similarly advancing sovereign satellite programs, particularly in Earth observation and military communications.

Europe holds the second-largest revenue share, driven by institutional demand from the European Space Agency (ESA), European Union flagship programs including Galileo and Copernicus, and strong commercial operators including Airbus, SES S.A., and Eutelsat. Europe's regional CAGR is estimated at 7.8%, supported by the IRIS² initiative and increasing defense satellite budgets among NATO members responding to the evolving geopolitical environment.

Middle East and Africa represent an emerging growth frontier, with Gulf Cooperation Council (GCC) nations investing in sovereign satellite programs as part of national diversification strategies. The UAE's Mohammed Bin Rashid Space Centre and Saudi Arabia's space authority have committed significant capital to satellite development partnerships, supporting a regional CAGR of approximately 9.2%. South America, led by Brazil's expanding remote sensing and communication satellite requirements, contributes modestly but is growing as commercial LEO broadband reaches economically viable penetration levels.

Three disruptive technology trajectories are poised to fundamentally reshape the Satellite Market architecture through the forecast period.

First, software-defined satellites (SDS) represent perhaps the most transformative near-term innovation. Unlike traditional hardware-defined payloads locked to specific frequency bands and coverage patterns at manufacturing time, SDS platforms enable in-orbit reconfiguration of power allocation, beam shaping, and frequency assignment via software updates. This dramatically reduces time-to-revenue for capacity deployment and allows operators to respond dynamically to shifting demand geographies. Airbus, through its OneSat program, and Boeing's 702X platform are commercially deploying SDS architectures, with adoption expected to reach mainstream GEO procurement by 2027.

Second, optical inter-satellite links (OISLs) are enabling the construction of space-based mesh networks that reduce dependence on ground station infrastructure and dramatically lower data latency. SPACEX's Starlink v2 satellites incorporate laser inter-satellite links, enabling trans-oceanic routing of traffic entirely through the satellite constellation. R&D investment in OISL technology has accelerated significantly, with the market for optical satellite communication components projected to grow at double-digit rates. This technology reinforces the competitive moat of vertically integrated operators while threatening traditional ground-station-centric business models, directly impacting the Satellite Ground Station Market.

Third, on-orbit servicing, assembly, and manufacturing (OSAM) technologies represent a longer-horizon disruption with transformative potential. The ability to refuel, repair, and upgrade satellites in orbit — demonstrated commercially by Northrop Grumman Corporation's MEV program — fundamentally alters satellite economic lifecycles. If OSAM scales commercially by the late 2020s, it could suppress demand for replacement satellite manufacturing while expanding the total services addressable market. NASA and DARPA are investing hundreds of millions of dollars in OSAM capability development, validating its strategic importance despite remaining technical and regulatory hurdles.

Environmental, social, and governance (ESG) considerations are increasingly influencing procurement, investment, and product development decisions within the Satellite Market, moving from peripheral concern to strategic imperative.\

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.1% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Satellite Market market expansion.

Key companies in the market include SPACEX, Northrop Grumman Corporation, Inmarsat Global Limited, Boeing, Intelsat, Airbus, SES S.A., Lockheed Martin Corporation, Safran SA, L3Harris Technologies, Inc..

The market segments include Function, Orbit Type, Application, End Use.

The market size is estimated to be USD 361.28 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Satellite Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Satellite Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.