1. What are the major growth drivers for the Land-based Military EOIR Systems Market market?

Factors such as are projected to boost the Land-based Military EOIR Systems Market market expansion.

+1 2315155523

Land-based Military EOIR Systems Market

Land-based Military EOIR Systems Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

The Land-based Military EOIR Systems Market was valued at $1.66 billion in the base year and is projected to grow at a compound annual growth rate of 3.05% through the forecast period. Electro-optical and infrared (EOIR) systems deployed on land-based military platforms represent a critical segment of modern ground-force capabilities, enabling persistent surveillance, target acquisition, threat detection, and fire control across all weather and lighting conditions. As geopolitical instability intensifies across multiple regions—from Eastern Europe to the Indo-Pacific—defense budgets have responded with elevated procurement allocations directed toward advanced sensor and surveillance technologies.

Several macro tailwinds are reinforcing this market's moderate but steady expansion. First, NATO member states have renewed commitments to increase defense spending to 2% or more of GDP, channeling billions into ground-based sensor modernization programs. Second, the Russia-Ukraine conflict has served as a real-world testbed that underscored the operational indispensability of EOIR systems for situational awareness on contested terrain. Third, emerging economies across Asia Pacific and the Middle East are rapidly modernizing their ground forces, representing a meaningful incremental demand source.

The market is underpinned by two principal product typologies: vehicle-mounted systems and man-portable systems. Vehicle-mounted configurations currently command a dominant revenue share owing to their higher unit value, integration complexity, and prevalence in armored fighting vehicle (AFV) modernization contracts. Man-portable systems, meanwhile, are gaining traction among special operations forces and light infantry units requiring dismounted ISR (intelligence, surveillance, and reconnaissance) capability.

From a technology standpoint, ongoing advancements in uncooled detector arrays, quantum dot infrared photodetectors, and AI-assisted target recognition algorithms are expanding the operational envelope of EOIR systems while simultaneously reducing lifecycle costs—a dynamic that is expected to accelerate adoption among second-tier defense buyers. The forward-looking outlook for the Land-based Military EOIR Systems Market remains constructive, with sustained investment in multi-spectral sensor fusion, networked battlefield architectures, and autonomous ground vehicle integration expected to provide incremental revenue uplift beyond the base growth trajectory.

The vehicle-mounted segment represents the single largest revenue-generating category within the Land-based Military EOIR Systems Market and is projected to maintain and extend its lead throughout the forecast period. This dominance is attributable to a confluence of platform-level procurement economics, operational doctrinal preferences, and integration requirements that collectively favor high-value, platform-embedded sensor suites over dismounted alternatives.

From a procurement economics standpoint, vehicle-mounted EOIR systems carry substantially higher average selling prices—often ranging from several hundred thousand to multiple millions of dollars per unit depending on system complexity—compared to man-portable configurations. Major armored vehicle modernization programs, including upgrades to Leopard 2, M1A2 Abrams, Challenger 3, and K2 Black Panther platforms, routinely incorporate integrated EOIR turrets with thermal imagers, day cameras, laser rangefinders, and fire control computers as standard equipment. These high-value bundled procurements inflate the segment's revenue share disproportionately relative to unit volume.

Operational doctrine further reinforces vehicle-mounted system primacy. Modern combined-arms maneuver warfare doctrine requires armored and mechanized units to conduct 24-hour operations across degraded visibility environments, making high-performance thermal imaging and low-light optical sensors not optional enhancements but core operational necessities. The integration of EOIR payloads into remote weapon stations (RWS) and panoramic commander's sights has become a de facto standard for new armored vehicle designs submitted to NATO-aligned customers.

Key players active in the vehicle-mounted segment include BAE Systems plc, which integrates EOIR solutions into its CV90 infantry fighting vehicle family and provides sensor systems for British Army programs. Elbit Systems Ltd has developed the COAPS (Commander's Open Architecture Panoramic Sight) and multiple multi-spectral turret solutions deployed across numerous armored platforms globally. HENSOLDT AG offers the PERI RTWL-B panoramic sight for the Leopard 2A7 and is a primary sensor supplier for German Bundeswehr vehicle programs. Leonardo S p A provides integrated thermal observation systems for European armored vehicle fleets, while Rheinmetall AG integrates EOIR sensors into its Lynx and Puma IFV platforms.

The vehicle-mounted segment's revenue share is not merely stable—it is actively consolidating as defense programs shift from incremental sensor upgrades to comprehensive platform overhauls that embed next-generation EOIR architectures at the design stage. The proliferation of active protection systems (APS) that rely on EOIR sensors for threat detection and tracking is creating additional demand vectors within this segment. Furthermore, the emergence of optionally manned and unmanned ground vehicle programs—where EOIR serves as the primary perception modality in the absence of a human crew—is opening a structurally new demand source that is expected to reach meaningful procurement volumes in the latter half of the forecast period. The vehicle-mounted segment's combination of high unit values, long program lifetimes, and expanding platform diversity positions it as the market's primary growth engine.

The Land-based Military EOIR Systems Market is shaped by a well-defined set of quantifiable drivers and counterbalancing constraints that collectively determine its 3.05% CAGR trajectory.

The most significant driver is the sustained increase in global defense budgets. NATO members have collectively committed to defense spending floors of 2% of GDP, with several nations—including Poland (4% of GDP allocated to defense in 2023) and the Baltic states—exceeding this threshold materially. These elevated budgets translate directly into armored vehicle acquisition and sensor modernization contracts that constitute the primary revenue pipeline for EOIR system suppliers.

Geopolitical conflict is a secondary but highly catalytic driver. The ongoing conflict in Ukraine has generated verified operational data confirming that thermal imaging systems are essential for armored and infantry units operating in contested environments. This empirical validation has accelerated procurement decisions among European NATO allies who observed capability gaps in peer-competitor ground engagements, driving near-term contract awards that bolster market revenue.

Technology pull represents a third driver. The transition from cooled to advanced uncooled infrared detector technologies—which have achieved sensitivity thresholds within 15–20% of cooled alternatives at significantly lower system cost—is expanding the addressable market to budget-constrained defense buyers. Additionally, AI-enabled automatic target recognition (ATR) capabilities embedded within modern EOIR systems are elevating their operational value proposition, justifying premium pricing.

On the constraint side, budget sequestration risks in key markets—particularly the United States, where Continuing Resolutions and debt ceiling negotiations have historically delayed program starts—represent a meaningful procurement timing risk. Export control regulations under the International Traffic in Arms Regulations (ITAR) and comparable frameworks in Europe also limit addressable market expansion in regions with ambiguous geopolitical alignments. Finally, the high technical complexity and long qualification cycles—typically 3–5 years for new EOIR systems to achieve full military qualification—constrain the rate at which new entrants or innovative products can capture market share.

The competitive landscape of the Land-based Military EOIR Systems Market is characterized by a concentrated group of established defense electronics and optics primes competing across platform integration, detector technology, and system-level performance dimensions.

BAE Systems plc: A leading UK-headquartered defense prime with deep capabilities in thermal imaging, fire control, and vehicle-integrated sensor systems; its EOIR portfolio supports multiple NATO armored vehicle programs including CV90 and AMPV derivatives.

Elbit Systems Ltd: An Israeli systems integrator and EOIR technology developer with a broad product range including thermal weapon sights, multi-spectral turrets, and panoramic commander's sights deployed across more than 30 countries; a major beneficiary of Israeli and export armored vehicle modernization programs.

Teledyne Technologies Incorporated: A US-based provider of high-performance infrared detectors and imaging modules that supply both military-grade cooled and uncooled sensor components to EOIR system integrators globally; particularly strong in focal plane array development.

Israel Aerospace Industries Ltd: An Israeli defense conglomerate offering advanced EOIR payloads for ground and vehicle-mounted surveillance applications, with significant export market penetration across Asia Pacific, Eastern Europe, and the Middle East.

Rheinmetall AG: A German defense and automotive technology group that integrates proprietary EOIR sensors into its Lynx, Puma, and Boxer vehicle platforms while also supplying standalone sensor systems to NATO partners.

Saab AB: A Swedish defense company offering the CROWS RWS and integrated situational awareness systems with EOIR components for ground vehicles; active in Nordic, European, and select export markets.

THALES: A French multinational providing advanced optronics and integrated battlefield management systems including the CATHERINE thermal imager family, widely deployed across European and export armored vehicles.

HENSOLDT AG: A German sensor solutions specialist with strong positions in panoramic sights, thermal imaging, and multi-function electro-optical systems for German Bundeswehr and allied armored platforms.

L3Harris Technologies Inc: A US-headquartered defense technology company offering thermal imaging systems, weapon sights, and integrated EOIR solutions under the AN/PAS and AN/TAS product families for US Army and allied customers.

Leonardo S p A: An Italian defense and aerospace prime offering the LOTHAR thermal observation and targeting system and integrated EOIR turrets for European armored vehicle programs.

March 2024: Elbit Systems Ltd announced the delivery of an initial batch of integrated multi-spectral EOIR turrets for a NATO European ally's armored vehicle upgrade program, valued at approximately $120 million, marking one of the largest European EOIR contracts awarded in the prior 12 months.

January 2024: HENSOLDT AG secured a follow-on contract from the German Bundeswehr for the supply of PERI RTWL-B panoramic sights incorporating upgraded thermal imaging channels for the Leopard 2A8 modernization program, reinforcing the company's position as the primary EOIR sensor supplier for Germany's armored fleet.

September 2023: L3Harris Technologies Inc unveiled a next-generation uncooled thermal imaging module featuring a 12-micron pitch detector array with enhanced sensitivity, targeting integration into vehicle-mounted and man-portable EOIR applications across US Army and export customers.

June 2023: Teledyne Technologies Incorporated completed qualification testing of an advanced cooled focal plane array with 1280×1024 resolution for integration into high-performance military EOIR systems, representing a significant detector technology milestone.

February 2023: BAE Systems plc received a contract modification from the US Army for EOIR sensor system upgrades on the M1A2 SEPv3 Abrams platform, extending the scope of its existing fire control sensor integration work by an estimated $85 million.

November 2022: Saab AB completed the integration of an upgraded EOIR package into its next-generation CROWS RWS platform demonstrated to multiple European customers at the Eurosatory defense exhibition, generating confirmed letters of intent from three NATO member states.

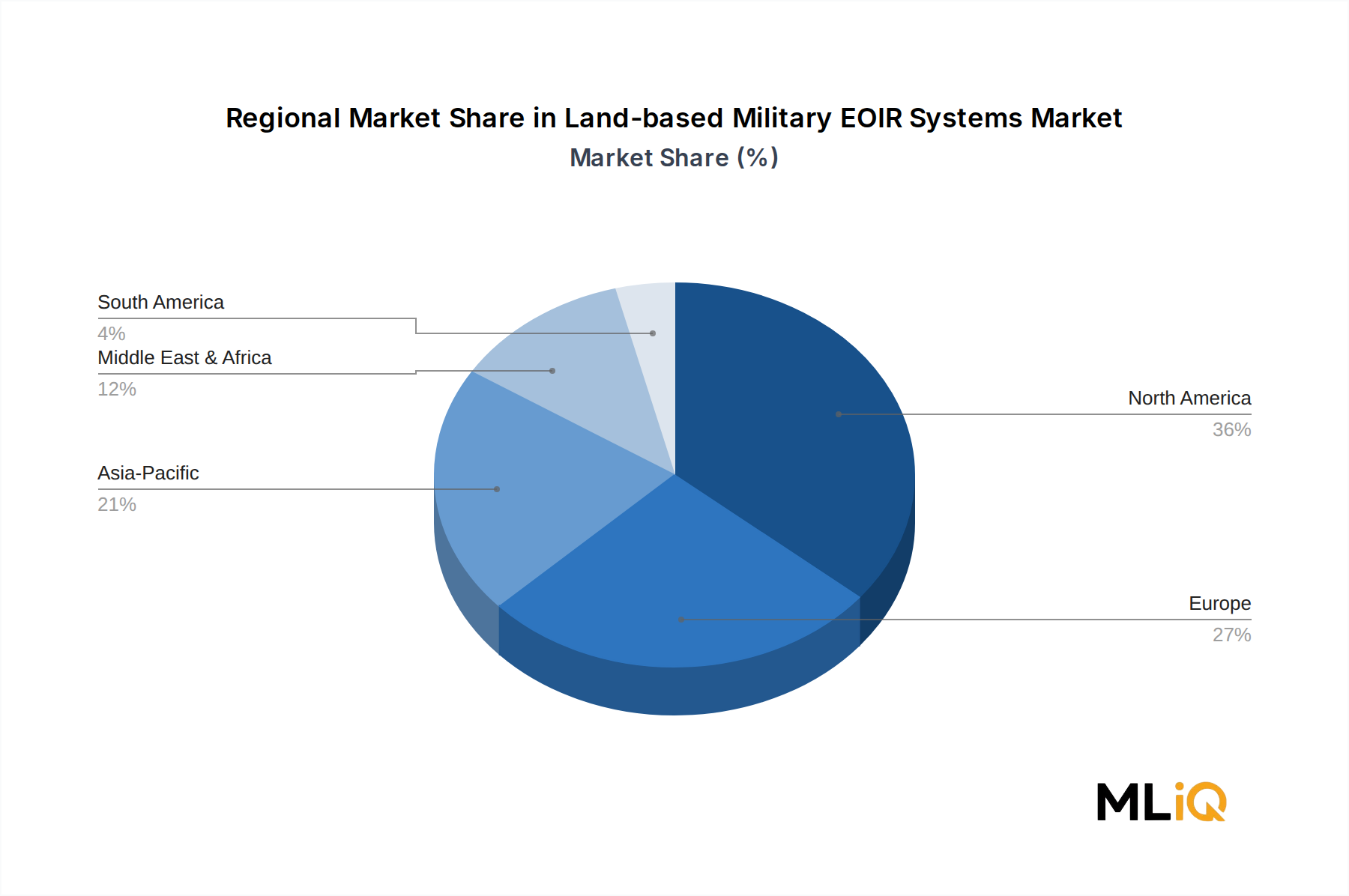

The Land-based Military EOIR Systems Market exhibits distinct regional demand profiles driven by defense budget trajectories, threat environments, and platform modernization timelines.

North America, led by the United States, represents the most mature and highest-revenue regional market, accounting for an estimated 35–38% of global market revenue. The US Army's ongoing Next Generation Combat Vehicle (NGCV) programs and continuous upgrades to the Abrams, Bradley, and Stryker fleets generate predictable, high-value EOIR procurement. Canada and Mexico contribute marginally at this stage. The regional CAGR is estimated at approximately 2.5–2.8%, reflecting a mature base with steady but not accelerating demand.

Europe is the fastest-growing region within the Land-based Military EOIR Systems Market, driven by an unprecedented defense reinvestment cycle triggered by Russia's invasion of Ukraine. Countries including Germany, Poland, France, and the Nordic states are executing multi-year armored vehicle procurement and upgrade programs that embed EOIR sensors as core requirements. European regional CAGR is estimated at 3.8–4.2%, above the global average, with Poland's $4+ billion armored vehicle acquisition program among the most significant near-term demand catalysts.

Asia Pacific represents the most dynamic long-term growth region, with China, India, South Korea, and Japan each executing substantial ground force modernization programs. India's Futuristic Infantry Combat Vehicle (FICV) program and South Korea's K2 and K21 fleet expansions are generating meaningful EOIR demand. Regional CAGR is estimated at 3.5–4.0%, supported by rising indigenous defense industrial capabilities that are increasingly competing with Western suppliers.

The Middle East and Africa region is characterized by episodic but high-value procurement, particularly from GCC states and Israel. Israeli domestic EOIR demand is structurally high given the country's operational environment and its role as a global EOIR technology exporter. Regional CAGR is estimated at 2.8–3.2%.

South America remains a minor revenue contributor at present, constrained by fiscal pressures in Brazil and Argentina, though targeted modernization programs in Brazil's armored fleet are expected to generate incremental demand over the forecast period.

The regulatory and policy environment governing the Land-based Military EOIR Systems Market is complex, multilayered, and materially consequential for both market access and competitive dynamics.

In the United States, the International Traffic in Arms Regulations (ITAR) administered by the Directorate of Defense Trade Controls (DDTC) govern the export of EOIR systems, subsystems, and components—including focal plane arrays, thermal imaging cameras, and associated software. ITAR classification of infrared detectors and advanced optics severely constrains the ability of US-based manufacturers to supply certain technologies to non-allied nations without lengthy licensing processes, effectively bifurcating global demand into ITAR-unrestricted and ITAR-restricted customer pools. Amendments to the Export Administration Regulations (EAR) and the Commerce Control List (CCL) periodically realign which EOIR technologies fall under Commerce versus State Department jurisdiction, creating compliance uncertainty for exporters.

In Europe, the EU's Common Military List and individual member-state export licensing regimes govern EOIR system transfers. Post-Brexit, the UK operates under its own Strategic Export Licensing framework administered by the Export Control Joint Unit (ECJU), creating parallel compliance obligations for companies like BAE Systems plc operating across multiple jurisdictions. The EU's European Defence Fund (EDF)—with a €8 billion budget over 2021–2027—actively incentivizes collaborative EOIR R&D among European partners through co-funding mechanisms, reinforcing European industrial consolidation around shared technology roadmaps.

NATO's STANAG (Standardization Agreement) framework—particularly STANAG 4568 governing thermal imaging performance parameters—provides a harmonized technical baseline that simplifies multi-nation procurement programs and shapes product development priorities across suppliers. Compliance with NATO STANAGs has become a de facto market access requirement for any supplier targeting European alliance customers, effectively raising technical entry barriers.

Recent policy developments include the US National Defense Authorization Act (NDAA) provisions restricting procurement of EOIR components sourced from Chinese manufacturers, notably affecting focal plane array supply chains and creating significant sourcing restructuring obligations for US-based EOIR integrators. This onshoring imperative is driving capital investment in domestic detector manufacturing capacity.

While defense markets have historically been insulated from ESG pressures relative to civilian industries, the Land-based Military EOIR Systems Market is increasingly subject to sustainability considerations that are reshaping procurement criteria, product development priorities, and investor relations strategies across the sector.

On the environmental dimension, the transition away from certain detector cooling technologies that rely on high-global-

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.05% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Land-based Military EOIR Systems Market market expansion.

Key companies in the market include BAE Systems plc, Elbit Systems Ltd, Teledyne Technologies Incorporated, Israel Aerospace Industries Ltd, Rheinmetall AG, Saab AB, THALES, HENSOLDT AG, L3Harris Technologies Inc, Leonardo S p A.

The market segments include Type.

The market size is estimated to be USD 1.66 billionusdbillion as of 2022.

N/A

Vehicle-mounted Segment is Projected to Showcase Highest Growth During the Forecast Period.

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

The market size is provided in terms of value, measured in billionusdbillion and volume, measured in .

Yes, the market keyword associated with the report is "Land-based Military EOIR Systems Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Land-based Military EOIR Systems Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.