1. What are the major growth drivers for the Air Cargo Screening Systems Market market?

Factors such as are projected to boost the Air Cargo Screening Systems Market market expansion.

Air Cargo Screening Systems Market

Air Cargo Screening Systems Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

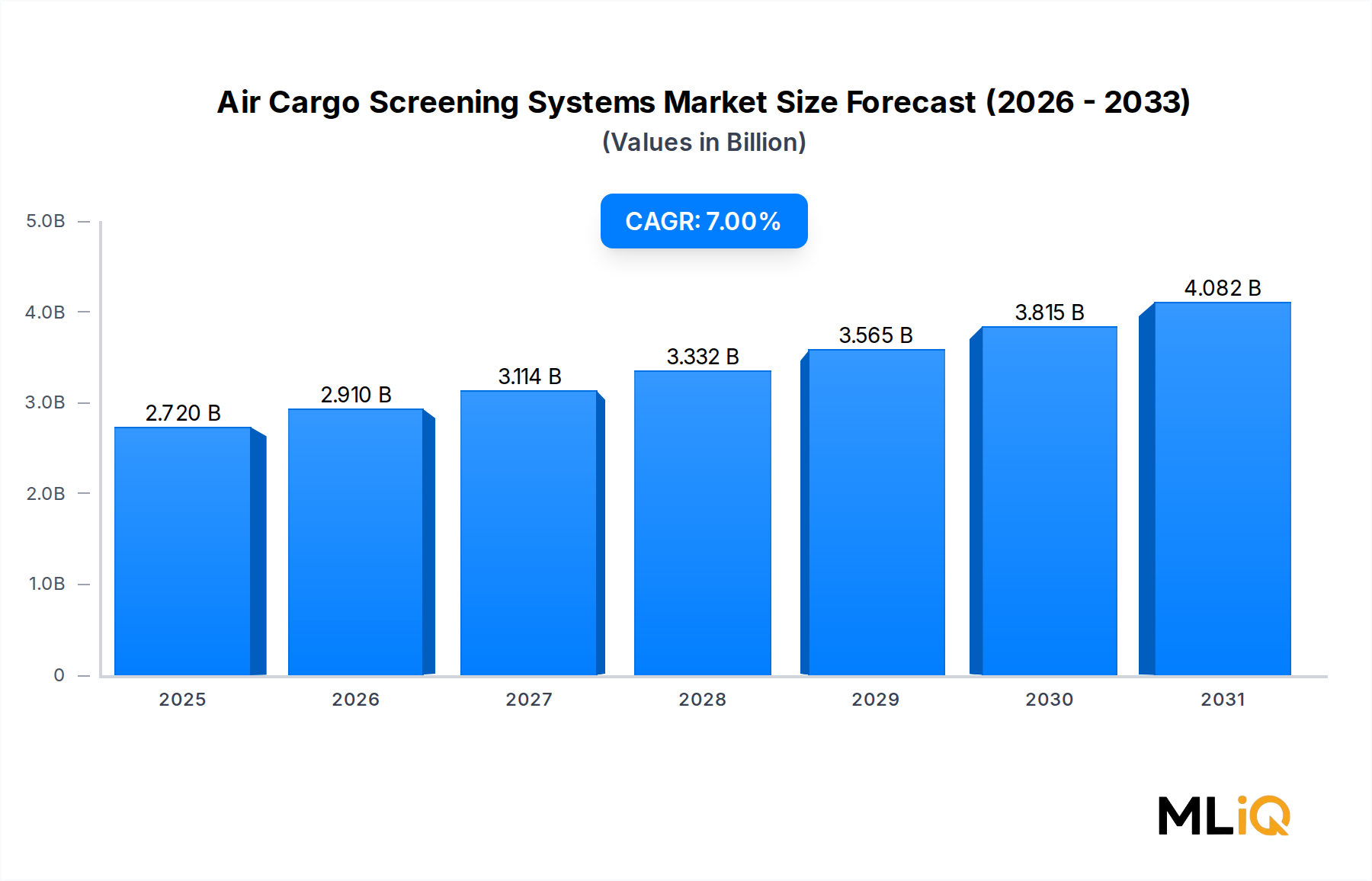

The global Air Cargo Screening Systems Market was valued at $2.72 billion in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 7% through the forecast period of 2025–2033. At this growth trajectory, the market is expected to surpass $4.8 billion by 2033, reflecting robust and sustained investment in aviation security infrastructure worldwide. This upward momentum is underpinned by a confluence of macroeconomic forces, escalating global trade volumes, and tightening regulatory mandates that compel airports and freight operators to upgrade screening capabilities.

A primary macro tailwind is the exponential growth of e-commerce, which has dramatically increased the volume of air freight consignments requiring inspection. Global air cargo volumes have rebounded strongly post-pandemic, with the International Air Transport Association (IATA) reporting multi-year record freight tonne kilometres (FTKs) in recent cycles. This surge directly translates into heightened demand for high-throughput, automated screening infrastructure. Airlines, freight forwarders, and airport operators are under intensifying pressure to process larger consignment volumes without sacrificing security integrity.

Heightened geopolitical tensions and the persistent threat of terrorism targeting aviation supply chains have also prompted governments across North America, Europe, and Asia Pacific to mandate more stringent cargo screening protocols. Regulatory bodies such as the U.S. Transportation Security Administration (TSA), the European Union Aviation Safety Agency (EASA), and the International Civil Aviation Organization (ICAO) have introduced increasingly prescriptive standards for 100% cargo screening, compelling airports to invest in next-generation detection platforms.

Technological evolution is a significant demand catalyst. The transition from legacy X-ray systems toward computed tomography (CT)-based platforms, artificial intelligence (AI)-augmented threat recognition, and multi-energy detection systems is reshaping procurement cycles. These advanced platforms offer superior threat discrimination, reduced false-alarm rates, and greater throughput — characteristics particularly valued by major international hub airports processing high cargo densities.

The market also benefits from government-funded modernization programs in emerging economies across Asia Pacific, the Middle East, and Africa, where airport infrastructure investment is accelerating. Simultaneously, rising adoption of automated hold baggage and cargo screening solutions in domestic airports — historically underserved relative to international terminals — is opening a new demand frontier.

From a competitive perspective, the market is moderately consolidated, with a handful of technologically sophisticated players commanding substantial share alongside a growing tier of regional specialists. The integration of machine learning, robotics, and data analytics into screening workflows represents the most consequential near-term technological frontier, with leading vendors racing to embed these capabilities into product roadmaps. Looking ahead, the Air Cargo Screening Systems Market is poised for durable, technology-driven expansion supported by inescapable regulatory tailwinds and structural growth in global air freight.

Within the Air Cargo Screening Systems Market, the Explosives Detection Systems (EDS) sub-segment commands the largest revenue share, driven by its critical role in addressing the most severe and consequential threat category in aviation security. EDS platforms are deployed at the primary checkpoint for all inbound and outbound cargo at international airports, making them the foundational layer of any cargo security architecture. Their dominance is structural rather than cyclical: regulatory mandates from ICAO, the TSA, and equivalent European authorities specifically require certified explosive detection capabilities for 100% cargo screening programs, ensuring a captive and recurring demand base.

The EDS segment encompasses a spectrum of detection technologies including X-ray diffraction (XRD), CT-based volumetric scanning, trace detection via ion mobility spectrometry (IMS), and multi-view X-ray imaging. Among these, CT-based EDS platforms have emerged as the technology of choice for large-volume cargo screening at major international hubs. CT systems generate three-dimensional reconstructions of cargo contents, enabling automated threat libraries to flag suspicious density profiles, shapes, and material compositions with far greater precision than conventional two-dimensional X-ray imaging. This superiority in threat discrimination is a key reason airports are allocating the largest share of capital expenditure to CT-based EDS upgrades.

Key players capturing significant share within this sub-segment include Rapiscan System Inc., which has developed a broad portfolio of EDS platforms spanning cabin baggage, checked luggage, and cargo applications. Smith's Detection Inc. offers a comprehensive range of CT and trace detection solutions and has a particularly strong installed base in European and Asia Pacific airports. Leidos, Inc. has leveraged its deep government contracting relationships to secure large-scale EDS deployment contracts, particularly in the United States where TSA procurement programs represent a consistently large order book. L3 Security & Detection Systems maintains a strong competitive position through its ProVision and ClearScan product families, targeting both airport and critical infrastructure clients.

The EDS segment's dominance is further reinforced by the substantial installed base of legacy systems now reaching end-of-life, generating a sizeable replacement cycle. Airports that deployed first-generation EDS platforms in the early 2000s following the September 11-driven security overhaul are now investing in third-generation CT systems with AI-assisted automated threat recognition (ATR) capabilities. This upgrade cycle is expected to sustain elevated capital expenditure throughout the 2025–2028 period, particularly in North America and Western Europe.

From a revenue concentration standpoint, EDS is estimated to account for approximately 38–42% of total Air Cargo Screening Systems Market revenue in 2023, with its share anticipated to remain stable or marginally expand through 2033 as CT adoption deepens in emerging market airports. The segment is also benefiting from dual-use procurement trends, where security agencies procure EDS platforms capable of serving both passenger terminal and cargo warehouse environments, broadening the addressable market for established vendors.

Growth within the EDS segment is also being propelled by advances in automated threat recognition software. Modern EDS platforms increasingly embed machine learning models trained on vast libraries of threat and benign object signatures, enabling operator-independent threat detection and significantly reducing the cognitive burden on security personnel. This automation premium justifies higher per-unit pricing, supporting favorable revenue mix dynamics for vendors with advanced AI capabilities.

The segment faces some consolidation pressure as the technological barrier to entry for CT-based systems remains high, favoring established players with proprietary algorithm libraries and regulatory certifications. Smaller vendors are increasingly targeting niche applications such as small parcel screening for e-commerce fulfillment centers, where cost sensitivity and throughput requirements differ from traditional airport deployments.

The Air Cargo Screening Systems Market is shaped by a defined set of quantifiable drivers and measurable constraints that collectively determine investment velocity and technology adoption cycles.

Driver 1 — Regulatory Mandates for 100% Cargo Screening: The TSA's Known Shipper Program and its subsequent evolution into the Air Cargo Security Program mandate that all cargo transported on passenger aircraft undergo certified screening. In the European Union, EC Regulation 300/2008 and its implementing rules require equivalent standards. These mandates create a non-discretionary spending floor estimated to account for over 60% of annual procurement in mature markets, ensuring base-level demand irrespective of macroeconomic conditions.

Driver 2 — Global Air Freight Volume Growth: IATA data indicates that air freight demand grew by approximately 7.6% year-over-year in 2023 in FTK terms, directly expanding the volume of consignments requiring screening. Each percentage point increase in global FTKs is estimated to generate proportional incremental demand for high-throughput screening capacity additions at major hub airports.

Driver 3 — Technological Obsolescence and Replacement Cycles: A significant share of screening systems installed globally are more than 10–15 years old and no longer meet updated certification standards. The TSA's Certification Test & Evaluation (CT&E) program has progressively withdrawn certifications from legacy two-dimensional X-ray systems that cannot meet contemporary explosive detection thresholds, forcing accelerated replacement procurement.

Driver 4 — E-Commerce Freight Expansion: Cross-border e-commerce shipments, projected to exceed $1 trillion in annual value by 2027, are generating disproportionate growth in small-parcel air cargo volumes. This trend is driving demand for high-speed, automated screening solutions optimized for small-parcel throughput.

Constraint 1 — High Capital and Operational Expenditure: Next-generation CT-based EDS platforms carry unit prices ranging from $500,000 to over $2 million, creating significant procurement barriers for smaller airports in emerging economies with constrained capital budgets.

Constraint 2 — Skilled Operator Shortage: Despite advances in ATR automation, regulatory requirements still mandate certified human operators for threat resolution, creating operational bottlenecks. Workforce training and retention costs add to total cost of ownership and constrain deployment velocity in labor-scarce markets.

The competitive landscape of the Air Cargo Screening Systems Market is characterized by a blend of established defense and security conglomerates, specialized detection technology companies, and emerging regional players.

Teledyne UK Limited: A subsidiary of Teledyne Technologies, this company provides advanced X-ray detection and imaging solutions for cargo and baggage screening, leveraging its expertise in high-resolution detector arrays and proprietary image processing algorithms to serve major international airport clients.

L3 Security & Detection Systems: A business unit of L3Harris Technologies, L3 Security & Detection Systems is a leading provider of CT-based and conventional X-ray screening systems for cargo, baggage, and checkpoint applications, with a particularly strong presence in North American and European airport security programs.

Gilardoni S.p.A.: An Italian manufacturer specializing in X-ray inspection systems for industrial, security, and medical applications, Gilardoni serves European airport and customs authorities with a range of cargo and parcel screening solutions.

Astrophysics Inc.: A California-based developer of X-ray security inspection systems, Astrophysics Inc. has built a significant installed base across airports, border crossings, and government facilities in over 130 countries, competing primarily on price-performance and compact form factor.

Smith's Detection Inc.: One of the most globally diversified players in the detection technology space, Smith's Detection Inc. offers a comprehensive portfolio spanning CT cargo scanners, trace detection, and chemical agent identification, with strong market penetration in Asia Pacific and the Middle East.

Autoclear, LLC: A U.S.-based manufacturer of X-ray screening systems and related security equipment, Autoclear serves domestic and international airport security programs with a focus on cost-effective solutions for mid-tier and regional airports.

Leidos, Inc.: A major U.S. defense and government services contractor, Leidos, Inc. has expanded its security technology portfolio through acquisition and organic development, holding significant TSA contract positions for screening system supply, maintenance, and operator support services.

Rapiscan System Inc.: A global leader in security inspection technology, Rapiscan System Inc. manufactures a broad array of X-ray, CT, and multi-energy screening systems for cargo, baggage, and vehicle inspection, with a strong footprint in both government and commercial aviation markets.

ICTS S.A: A European aviation and travel security services company, ICTS S.A combines physical security operations with technology integration services, offering consultative deployment of screening systems across European airports.

VOTI Detection Inc.: A Canadian developer of high-resolution X-ray inspection systems, VOTI Detection Inc. differentiates through its proprietary image quality enhancement technology and has been expanding its international commercial airport footprint.

January 2023: The U.S. Transportation Security Administration announced expanded funding under its Next Generation Screening initiative, committing over $100 million toward CT-based cargo screening upgrades at major international hub airports, accelerating the retirement of legacy two-dimensional X-ray platforms.

March 2023: Smith's Detection Inc. unveiled its HI-SCAN 10080 XCT cargo CT screening system, designed for high-throughput palletized cargo, incorporating an updated AI-driven automated threat recognition engine capable of sub-30-second scan cycle times.

June 2023: The European Union Aviation Safety Agency published updated certification standards for cargo screening equipment under its revised security regulation framework, mandating compliance with enhanced explosive detection performance criteria by 2025 for all passenger aircraft cargo holds.

September 2023: Rapiscan System Inc. secured a multi-year contract with a major Asia Pacific hub airport operator for the deployment of its RTT 110 CT cargo screening platform, representing one of the largest single-country cargo screening procurements recorded in the region that year.

November 2023: Leidos, Inc. announced a strategic partnership with a leading AI software developer to integrate advanced object recognition models into its cargo screening decision support systems, targeting a 40% reduction in false alarm rates.

February 2024: VOTI Detection Inc. received Transport Canada certification for its XR3D-6 high-resolution X-ray system, enabling deployment at Canadian domestic and international cargo facilities under the new Canadian Air Transport Security Authority framework.

April 2024: ICAO issued updated guidance material for the implementation of Chapter 7 cargo security standards, recommending member states transition to CT-based primary screening for all international cargo by 2027.

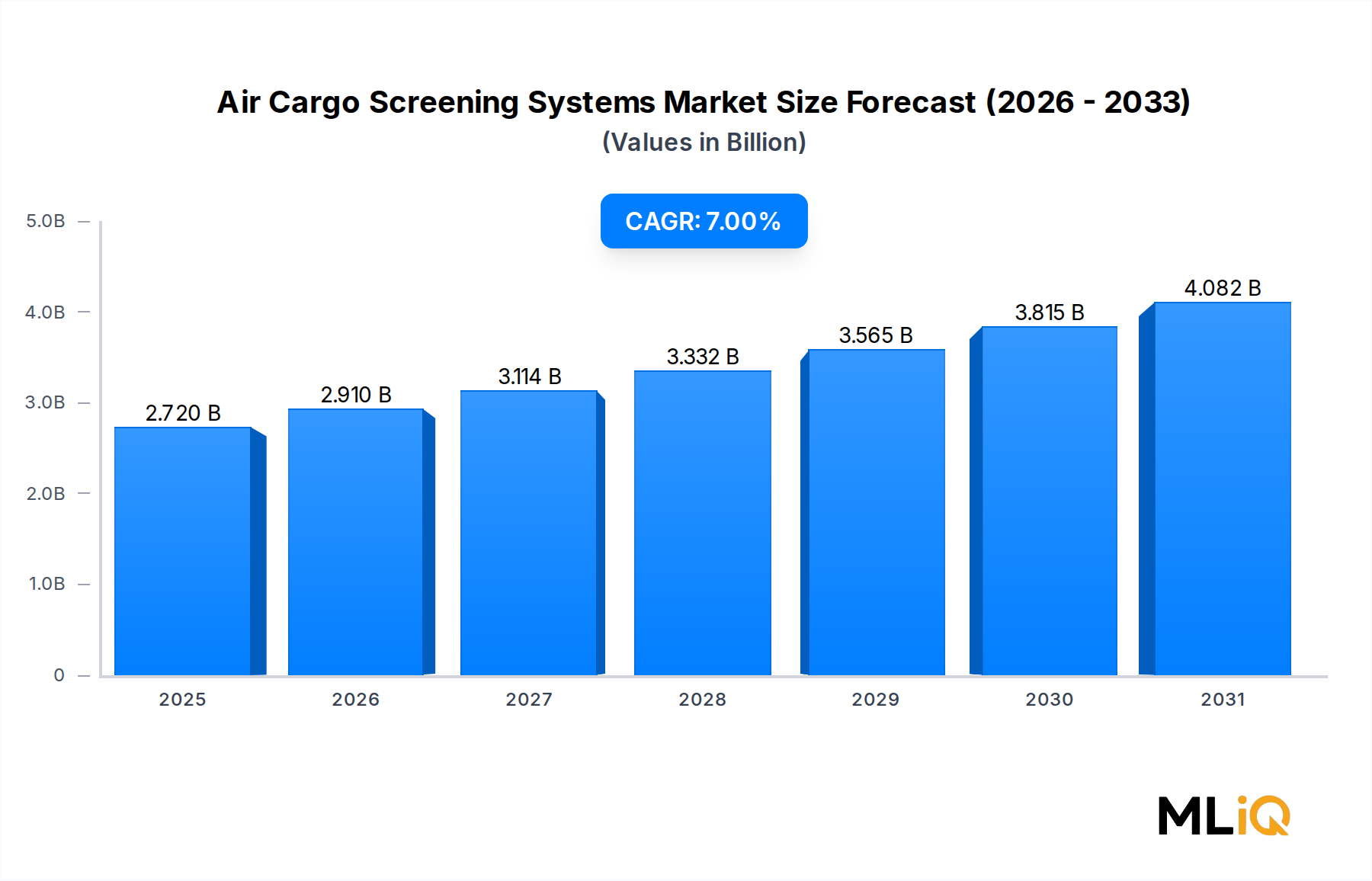

The Air Cargo Screening Systems Market exhibits significant regional variation in both growth velocity and demand maturity, reflecting differences in regulatory stringency, infrastructure investment capacity, and air freight volume concentration.

North America remains the most mature and largest revenue-generating region, accounting for an estimated 34–36% of global market revenue in 2023. The United States is the dominant contributor, underpinned by TSA-mandated 100% cargo screening requirements and substantial federal procurement budgets. The region is growing at approximately 5.5–6.0% CAGR, reflecting a market transitioning from initial compliance-driven build-out to technology refresh and CT upgrade cycles. Canada and Mexico contribute incrementally, with growing cross-border e-commerce trade driving additional screening infrastructure investment.

Europe represents the second largest regional market, capturing approximately 28–30% of global revenue. Stringent EU regulatory frameworks and the high density of major international hub airports drive consistent procurement. The United Kingdom, Germany, France, and the Benelux region are the leading national markets. The European market is growing at a CAGR of approximately 6.0–6.5%, with growth accelerating as airports upgrade to meet revised EU certification standards mandated through 2025.

Asia Pacific is the fastest-growing region, projected to expand at a CAGR of 8.5–9.5% through 2033. China, India, Japan, South Korea, and the ASEAN bloc are the primary growth engines. The Chinese government's continued investment in airport infrastructure expansion — with dozens of new international airports commissioned or under construction — is creating substantial greenfield demand for cargo screening systems. India's rapidly expanding domestic air freight market, supported by the government's UDAN regional connectivity scheme and dedicated freight corridor development, is similarly driving procurement.

The Middle East & Africa region is growing at a CAGR of approximately 7.5–8.0%, with Gulf Cooperation Council (GCC) states — particularly the UAE, Saudi Arabia, and Qatar — representing the highest-value national markets. Major hub airports including Dubai International, Hamad International, and Abu Dhabi International are investing heavily in cargo security infrastructure to support their strategic positioning as global air freight transshipment hubs.

South America remains a smaller but steadily growing market, with Brazil and Argentina leading regional demand. Growth is estimated at 5.0–5.5% CAGR, constrained by fiscal pressures but supported by increasing international air cargo volumes tied to agricultural commodity exports.

The Air Cargo Screening Systems Market is exposed to a complex upstream supply chain encompassing specialized electronic components, precision-engineered mechanical assemblies, advanced detector materials, and proprietary software platforms. Understanding these dependencies is critical for assessing vendor resilience and pricing dynamics.

X-ray detector arrays — the core sensing element in conventional screening systems — rely heavily on cadmium tungstate (CdWO4) and cesium iodide (CsI) scintillator crystals, which are subject to constrained global supply. Rare earth elements used in detector manufacturing, including gadolinium and lutetium

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Air Cargo Screening Systems Market market expansion.

Key companies in the market include Teledyne UK Limited, L3 Security & Detection Systems, Gilardoni S.p.A., Astrophysics Inc., Smith’s Detection Inc., Autoclear, LLC, Leidos, Inc., Rapiscan System Inc., ICTS S.A, VOTI Detection Inc..

The market segments include Type, Size, Airport Type.

The market size is estimated to be USD 2.72 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Air Cargo Screening Systems Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Air Cargo Screening Systems Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.