1. What are the major growth drivers for the Guided Rocket Market market?

Factors such as are projected to boost the Guided Rocket Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

Guided Rocket Market

Guided Rocket Market+1 2315155523

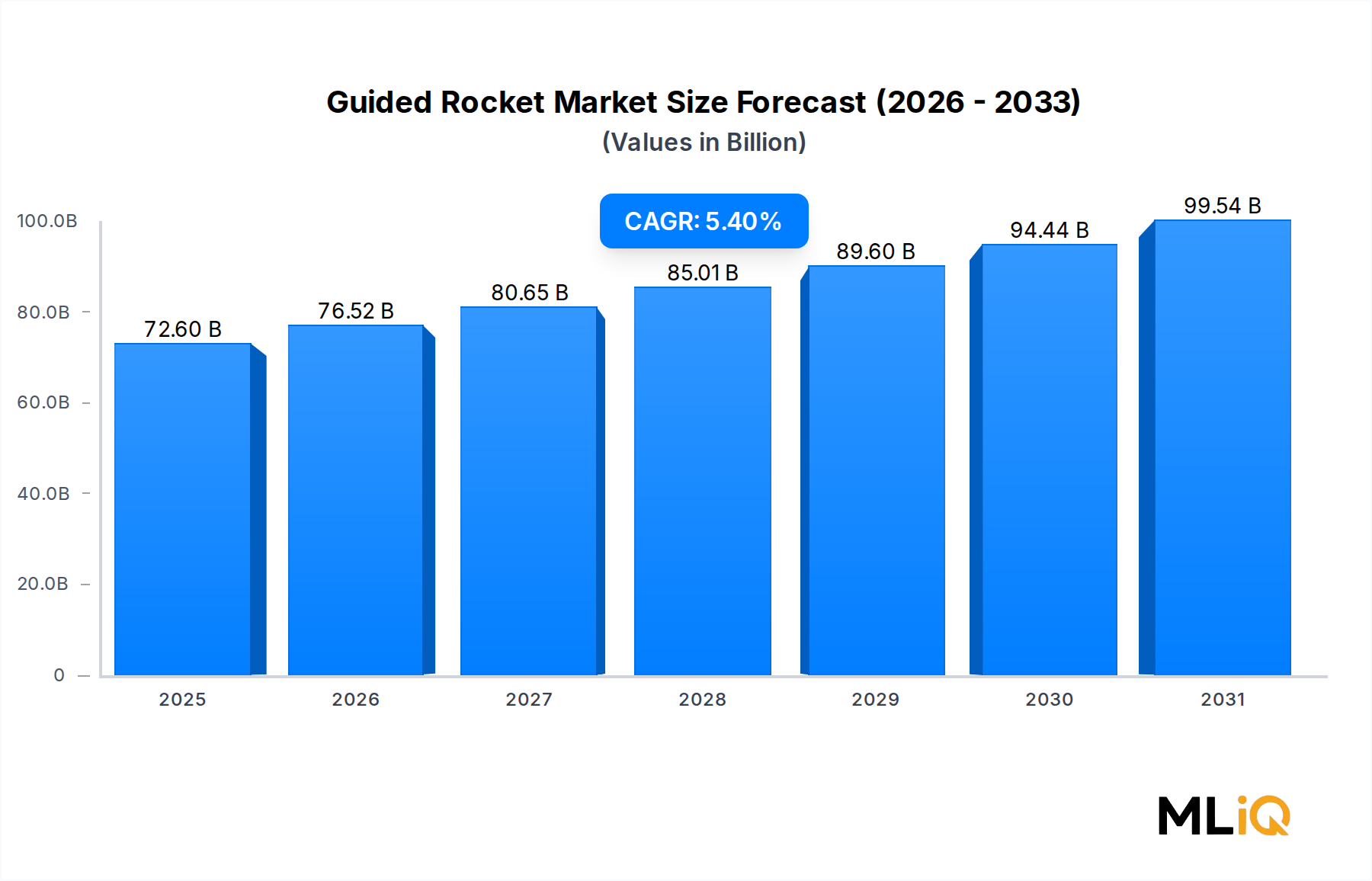

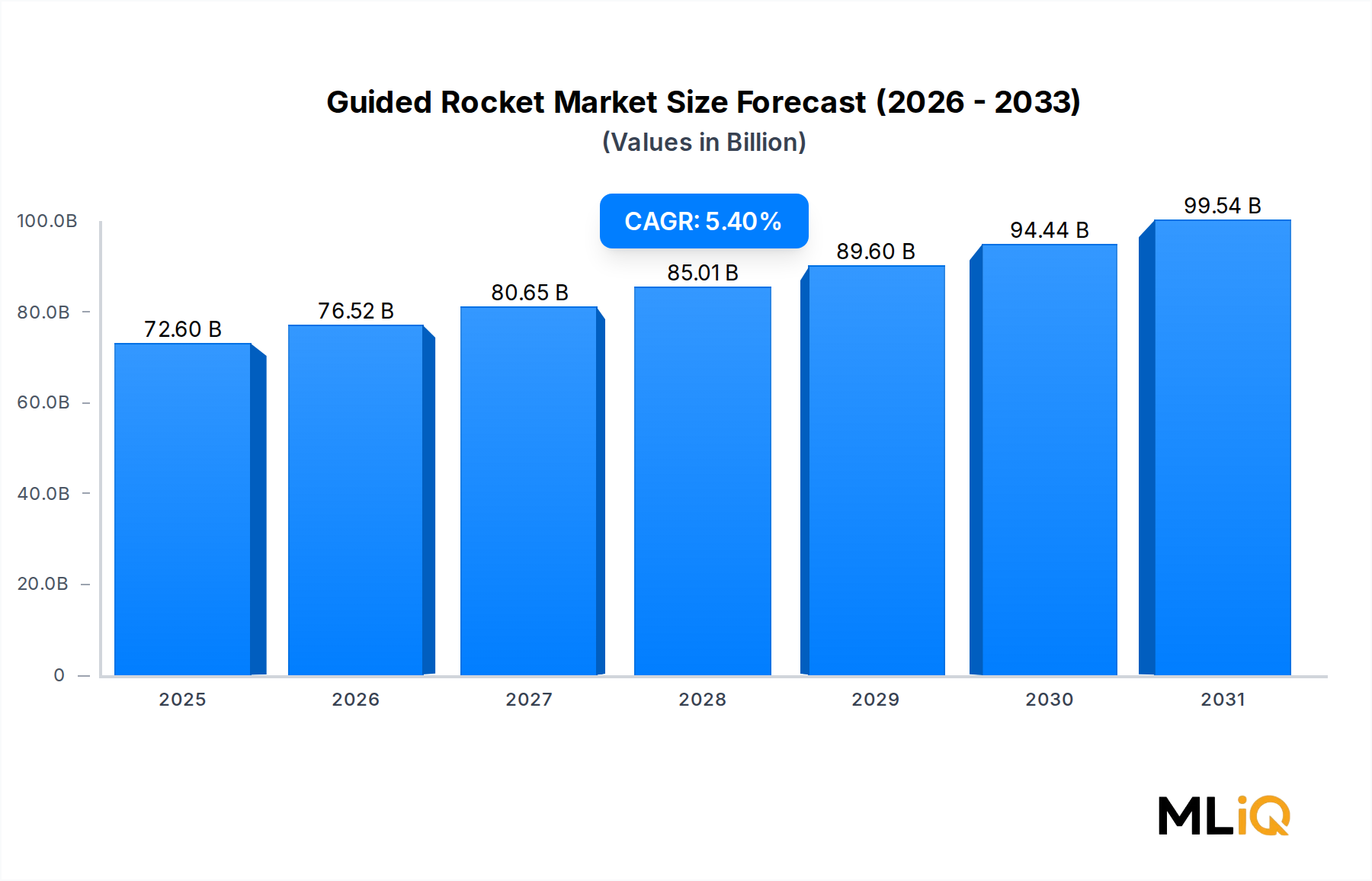

The global Guided Rocket Market is valued at $72.6 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 5.4% through 2033, underscoring its critical role within the broader Aerospace and Defense Market. This growth trajectory reflects sustained and accelerating investment by nation-states and allied defense coalitions in precision-strike capabilities, force modernization programs, and next-generation battlefield deterrence systems.

Several macro-level tailwinds are converging to reinforce demand. First, geopolitical tensions across Eastern Europe, the Indo-Pacific, and the Middle East have prompted governments to accelerate procurement cycles and refresh aging inventories of precision munitions. NATO member states have committed to expanding defense budgets beyond 2% of GDP, and this fiscal commitment directly translates into elevated procurement of guided rocket systems across air, land, and sea platforms. Second, the proliferation of near-peer adversary capabilities — including advanced air-defense networks and electronic warfare systems — has intensified the requirement for longer-range, higher-accuracy guided rockets that can defeat sophisticated countermeasures.

On the demand side, the convergence of digital warfare, autonomous targeting, and AI-assisted fire control is reshaping the operational requirements placed on guided rockets. Platform integration with unmanned aerial vehicles, next-generation fighter aircraft, and multi-domain command-and-control architectures is creating new procurement pathways. The intersection of guided rockets with the Military Drone Market is particularly noteworthy, as drone-launched precision rockets represent one of the fastest-growing sub-segments within the broader category.

From a product perspective, anti-tank and tactical rockets continue to account for a substantial share of total market revenue, driven by land-based conflict scenarios and persistent asymmetric warfare environments. Anti-satellite weapons (ASAT) programs, while representing a smaller absolute share, are growing at above-average rates due to escalating competition in the space domain among major powers.

Forward-looking outlook: Between 2025 and 2033, cumulative market investment is expected to surpass several hundred billion dollars across all product lines and launch modes. The integration of hypersonic glide vehicles, AI-enabled guidance systems, and miniaturized seeker technologies will further differentiate next-generation guided rockets from legacy platforms. Suppliers that invest early in software-defined guidance architectures and modular warhead systems are expected to capture disproportionate market share through long-term government framework contracts and allied foreign military sales programs.

Within the Guided Rocket Market, the anti-tank and tactical rockets sub-segment commands the largest revenue share, driven by persistent global demand from land-warfare programs, mechanized infantry modernization, and asymmetric conflict environments. This dominance is structural rather than cyclical, reflecting the enduring relevance of armored vehicle threats across multiple theaters of operation.

Anti-tank guided rockets — including man-portable, vehicle-launched, and air-delivered variants — are procured by virtually every tier-one and tier-two defense force globally. The proliferation of main battle tanks, infantry fighting vehicles, and armored personnel carriers among state and non-state actors has sustained procurement volumes at elevated levels for over two decades. More recently, the intensification of conventional land warfare in Eastern Europe has accelerated emergency procurements and long-term replenishment contracts across NATO and partner nations, further consolidating this segment's dominance.

Tactical rockets, which encompass unguided and guided variants for suppression of enemy air defenses (SEAD), close air support, and direct-fire artillery supplementation, have seen rising demand as militaries seek cost-effective precision fires that complement expensive standoff cruise missiles. The unit economics of tactical guided rockets — significantly lower per-round cost relative to cruise missiles — make them the preferred option for high-volume, time-sensitive engagement scenarios.

Key players within this segment include Lockheed Martin Corporation, which produces the Hellfire and Joint Air-to-Ground Missile (JAGM) families widely used across US and allied platforms. Raytheon Company contributes TOW and other anti-armor systems. MBDA Inc. delivers the Brimstone and MILAN ER systems, which are central to European land-force modernization programs. Roketsan A.S. has emerged as a significant regional player in anti-tank and tactical rocket production, securing contracts across the Middle East and Central Asian markets. Rafael Advanced Defense Systems Ltd supplies the Spike family of anti-tank guided missiles, which has achieved exceptional export penetration across more than 40 countries.

The segment's market share is not merely holding steady — it is actively consolidating. As procurement agencies shift from purely reactive replenishment to proactive capability enhancement, contract structures are evolving toward multi-year, multi-lot agreements with embedded technology refresh provisions. This shift locks in incumbent manufacturers while raising barriers to new entrants due to the stringent qualification, certification, and supply-chain requirements imposed by defense ministries.

A critical growth vector within this segment is the integration of anti-tank rockets with loitering munition platforms and rotary-wing unmanned systems. Helicopter-launched anti-tank rockets such as the Hellfire and Brimstone are increasingly being adapted for deployment from medium-altitude long-endurance UAVs, expanding the total addressable engagement envelope. This platform convergence is expected to drive double-digit revenue growth in air-delivered anti-tank rocket variants through 2028.

The Precision Guided Munitions Market is closely intertwined with this segment, as advances in seeker technology, dual-mode guidance (semi-active laser combined with millimeter-wave radar), and network-enabled targeting are being applied first to high-volume anti-tank platforms before cascading to other product lines. Manufacturers investing in these guidance upgrades are securing both modernization retrofits on legacy platforms and design-win positions on next-generation systems, creating durable revenue streams across the forecast horizon.

The Guided Rocket Market is propelled by a well-defined set of quantifiable drivers, each underpinned by verifiable procurement and policy data.

Rising global defense expenditure is the primary macroeconomic driver. NATO member nations collectively increased defense spending by approximately 11% year-over-year in 2023, the largest single-year increase since the Cold War, according to alliance reporting. This surge directly elevated procurement budgets for precision munitions, with guided rockets receiving a disproportionate share due to their versatility across multi-domain operations. The United States alone allocated over $30 billion to missile and munitions procurement within its FY2024 defense budget, a significant portion of which applies to guided rocket systems.

Inventory depletion from active conflict zones represents a second, urgent driver. Sustained combat operations have drawn down stockpiles of guided rockets at rates that far exceed pre-conflict replenishment planning assumptions. Defense ministries across Europe and North America have responded by issuing multi-year urgent operational requirement (UOR) contracts, compressing typical procurement timelines from five to seven years down to eighteen to twenty-four months.

Technology-driven demand for precision and reduced collateral damage is a third structural driver. Rules of engagement in urban and asymmetric conflict environments increasingly mandate low-yield, high-precision engagement solutions. This policy imperative is directly expanding the addressable market for miniaturized guided rockets with advanced fuzing and guidance systems.

Constraining the market, however, are several significant challenges. Defense supply chains for critical components — including rare earth elements used in guidance electronics and solid-fuel propellants sourced from limited geographic producers — remain vulnerable to disruption. The Rocket Motor Market faces production bottleneck risks, particularly for high-demand solid-propellant motors, where manufacturing scale-up timelines are measured in years rather than months. Additionally, export control regimes such as the US International Traffic in Arms Regulations (ITAR) and the EU's Common Position on arms exports create friction in international sales cycles, constraining revenue expansion in otherwise high-growth markets.

The competitive landscape of the Guided Rocket Market is defined by a small number of large prime contractors with deep integration across guidance, propulsion, and warhead subsystems, alongside a growing cohort of regional manufacturers leveraging government-supported industrial programs.

Lockheed Martin Corporation: The world's largest defense contractor by revenue, Lockheed Martin maintains dominant positions in air-to-ground and anti-armor guided rocket segments through the Hellfire, JAGM, and ATACMS product families, supported by long-cycle US Army and allied procurement contracts.

MBDA Inc.: A pan-European missile consortium jointly owned by Airbus, BAE Systems, and Leonardo, MBDA is the primary supplier of guided rockets to French, British, Italian, and German armed forces, with the Brimstone and MMP systems as flagship products.

Leonardo: The Italian defense and aerospace conglomerate contributes guidance systems, electro-optical seekers, and complete guided rocket assemblies, serving as both a prime contractor for Italian national programs and a Tier-1 supplier within MBDA.

Raytheon Company: A subsidiary of RTX Corporation, Raytheon is a leading producer of anti-armor and air-to-ground guided rockets, operating production facilities that supply both US military requirements and extensive foreign military sales programs across the Middle East and Indo-Pacific.

Roketsan A.S.: Turkey's national missile and rocket manufacturer has achieved rapid capability growth under government-supported domestic defense industrialization, now exporting systems including the CIRIT laser-guided rocket and the UMTAS anti-tank guided missile to multiple international customers.

General Dynamics Corporation: Through its Ordnance and Tactical Systems division, General Dynamics provides rocket propulsion systems, warheads, and complete guided rocket assemblies to US and allied military customers.

Northrop Grumman Corporation: A major supplier of rocket motor systems, guidance electronics, and complete guided rocket platforms, Northrop Grumman serves both prime contract roles and critical Tier-1 subcontract positions across multiple US and international programs.

Thales Group: The French defense and electronics major contributes advanced seekers, navigation systems, and complete guided rocket products, particularly within European joint programs and export markets across Africa and the Middle East.

Boeing: Through its Defense, Space & Security division, Boeing develops and produces air-launched guided rockets including the Small Diameter Bomb family and contributes to next-generation precision strike programs as both prime and integrating contractor.

Rafael Advanced Defense Systems Ltd: The Israeli state-owned defense technology company is globally recognized for the Spike family of anti-tank guided missiles and the SPICE precision guidance kit, with export penetration spanning more than 40 countries across five continents.

January 2024: The US Department of Defense announced a $1.8 billion multi-year procurement contract with Lockheed Martin for Joint Air-to-Ground Missile (JAGM) systems, covering deliveries through 2028 for US Army and Navy aviation platforms.

March 2024: MBDA completed the first operational deployment of the Brimstone 3 variant by Royal Air Force Typhoon aircraft, marking a significant capability milestone with enhanced dual-mode seeker and extended standoff range for the Guided Rocket Market.

May 2024: Roketsan A.S. signed export framework agreements with three undisclosed Middle Eastern nations for the supply of CIRIT 2.75-inch laser-guided rockets, valued collectively at approximately $400 million.

August 2024: Raytheon Company received a $950 million contract modification for TOW 2B Aero guided rockets under an existing US Army foreign military sales program, with deliveries scheduled for allied customers in Europe and Southeast Asia.

October 2024: Rafael Advanced Defense Systems unveiled the Spike NLOS Block 5 variant at the Euronaval exhibition, featuring AI-assisted target recognition and a man-in-the-loop guidance capability upgrade relevant to the Anti-Tank Missile Market.

December 2024: The European Defence Agency (EDA) published a joint procurement roadmap for precision guided munitions among seven member states, with guided rockets identified as the highest-priority replenishment category, projecting combined demand exceeding $6 billion through 2030.

February 2025: Northrop Grumman announced a $220 million investment in expanded solid rocket motor production capacity at its Rocket Center, West Virginia facility, targeting increased throughput for guided tactical rocket programs.

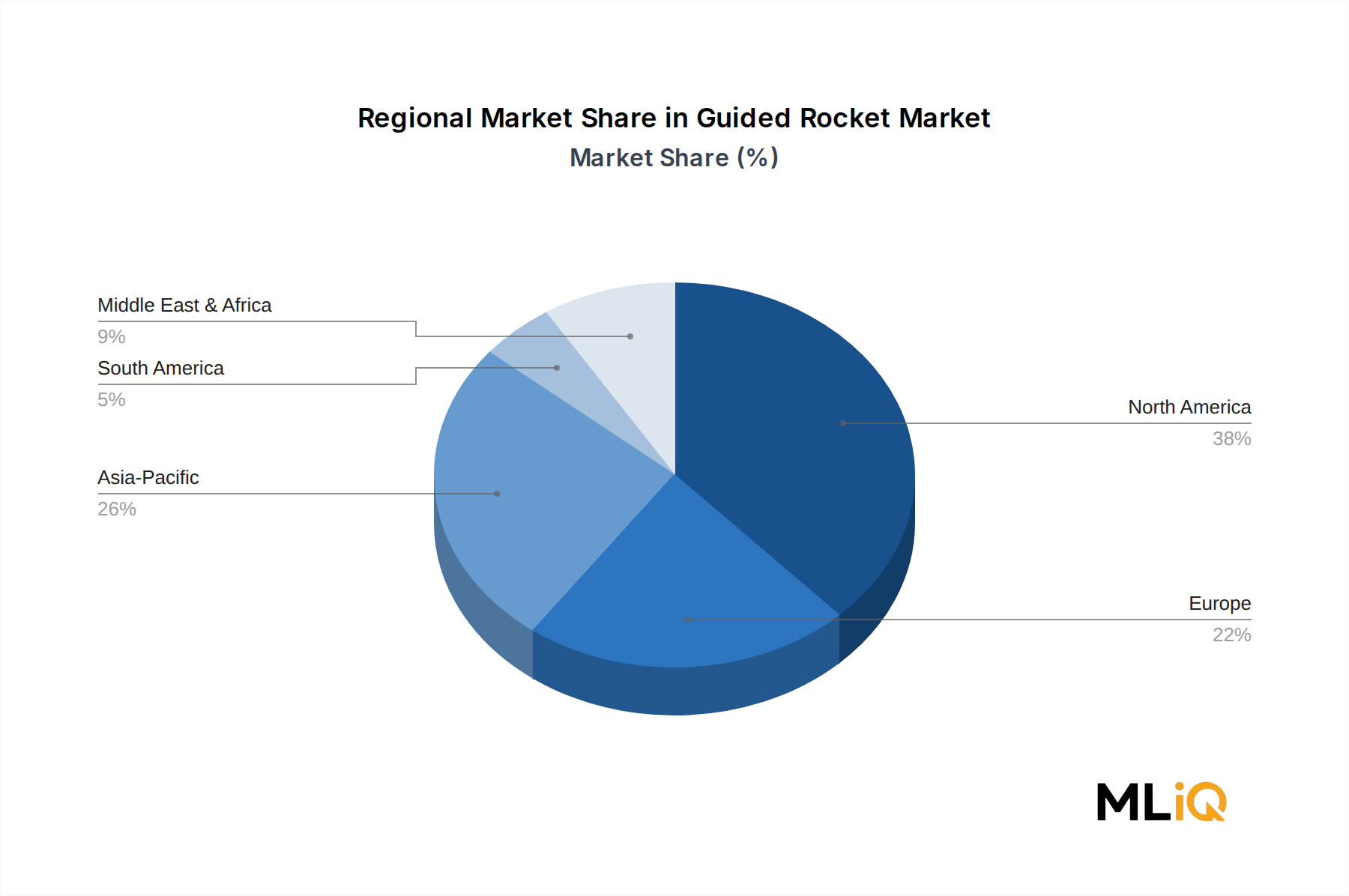

North America represents the largest and most mature regional segment of the Guided Rocket Market, accounting for an estimated 38% of global revenue in 2024. The United States drives virtually all of this share through sustained Department of Defense procurement, replenishment contracts, and foreign military sales administered by the Defense Security Cooperation Agency. The region is forecast to grow at a CAGR of approximately 4.8% through 2033, with growth moderated by the sheer scale of the existing base but sustained by continuous modernization requirements and multi-year programmatic contracts.

Europe is experiencing the fastest absolute growth acceleration of any established region, with a projected CAGR of 6.1% through 2033, driven by the post-2022 defense spending surge across NATO member states. Germany, France, the United Kingdom, and Poland are the primary demand centers, collectively committing to multi-year guided rocket procurement programs valued in the tens of billions of euros. The Air-to-Surface Missile Market is particularly active in Europe, as Typhoon and Rafale operators modernize their air-launched precision rocket inventories.

Asia Pacific is the fastest-growing regional market on a percentage basis, with a projected CAGR of 7.2% through 2033. China's continued military modernization, India's push toward indigenous defense production under the "Make in India" initiative, Japan's historic defense budget expansion to 2% of GDP, and South Korea's advanced domestic defense industrial base collectively underpin this trajectory. The Anti-Submarine Warfare Market is a key demand driver within this region, as maritime security concerns prompt investment in air- and ship-launched guided rockets for anti-submarine and anti-surface roles.

The Middle East and Africa region is projected to grow at a CAGR of 5.9% through 2033, with Israel, Saudi Arabia, the UAE, and Turkey serving as the primary demand centers. Israel's advanced domestic industry — anchored by Rafael and Elbit — contributes both supply and demand dynamics. GCC nations continue to execute large foreign military sales contracts for US and European guided rocket systems.

South America represents a smaller but stable segment, growing at approximately 3.8% CAGR, with Brazil leading regional procurement through its national defense modernization program.

Three disruptive technology vectors are reshaping the innovation trajectory of the Guided Rocket Market over the 2025–2033 forecast period.

First, hypersonic and extended-range glide technologies are transitioning from advanced development to early fielding. While full hypersonic capability (Mach 5+) remains the domain of larger strategic systems, hyper-velocity glide enhancements applied to tactical guided rockets — enabling Mach 3–4 terminal engagement speeds — are nearing production readiness at several prime contractors. The Defense Electronics Market is a critical enabler here, supplying the high-bandwidth, radiation-hardened electronics required to survive aerothermal loads at these velocities. R&D investment in this area across the US, France, and China exceeded an estimated $4 billion annually as of 2023.

Second, AI-assisted autonomous target recognition (ATR) and multi-mode seeker integration are fundamentally changing guidance architectures. Traditional semi-active laser guidance is being supplemented or replaced by dual-mode seekers combining millimeter-wave radar, infrared imaging, and GPS/INS navigation. AI-enabled ATR algorithms allow the rocket to autonomously classify, prioritize, and engage targets within a predefined engagement authority envelope. Adoption timelines suggest early operational fielding of AI-ATR systems on anti-tank guided rockets by 2026–2027, with broader fleet integration by 2030. This technology transition reinforces incumbent business models for large prime contractors while threatening smaller guidance-only suppliers who cannot integrate software-defined AI stacks.

Third, additive manufacturing and digital engineering are reducing development cycle times and enabling rapid configuration changes for warhead and structural components. The Missile Propulsion System Market is already seeing adoption of 3D-printed motor casing components,

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Guided Rocket Market market expansion.

Key companies in the market include Lockheed Martin Corporation, MBDA Inc., Leonardo, Raytheon Company, Roketsan A.S., General Dynamics Corporation, Northrop Grumman Corporation, Thales Group, Boeing, Rafael Advanced Defense Systems Ltd.

The market segments include Launch Mode, Product.

The market size is estimated to be USD 72.6 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Guided Rocket Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Guided Rocket Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.