1. What are the major growth drivers for the Military Software Market market?

Factors such as are projected to boost the Military Software Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

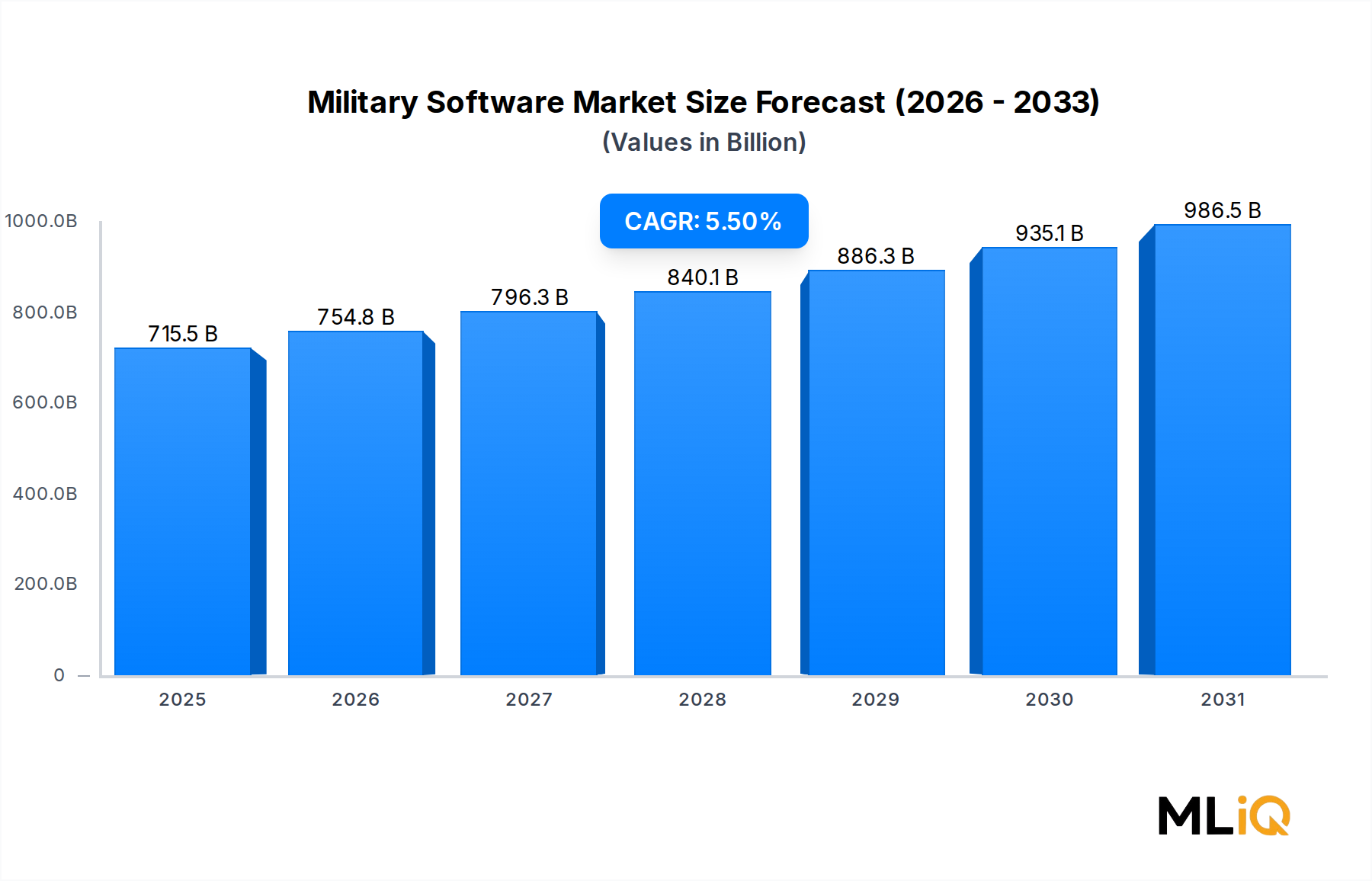

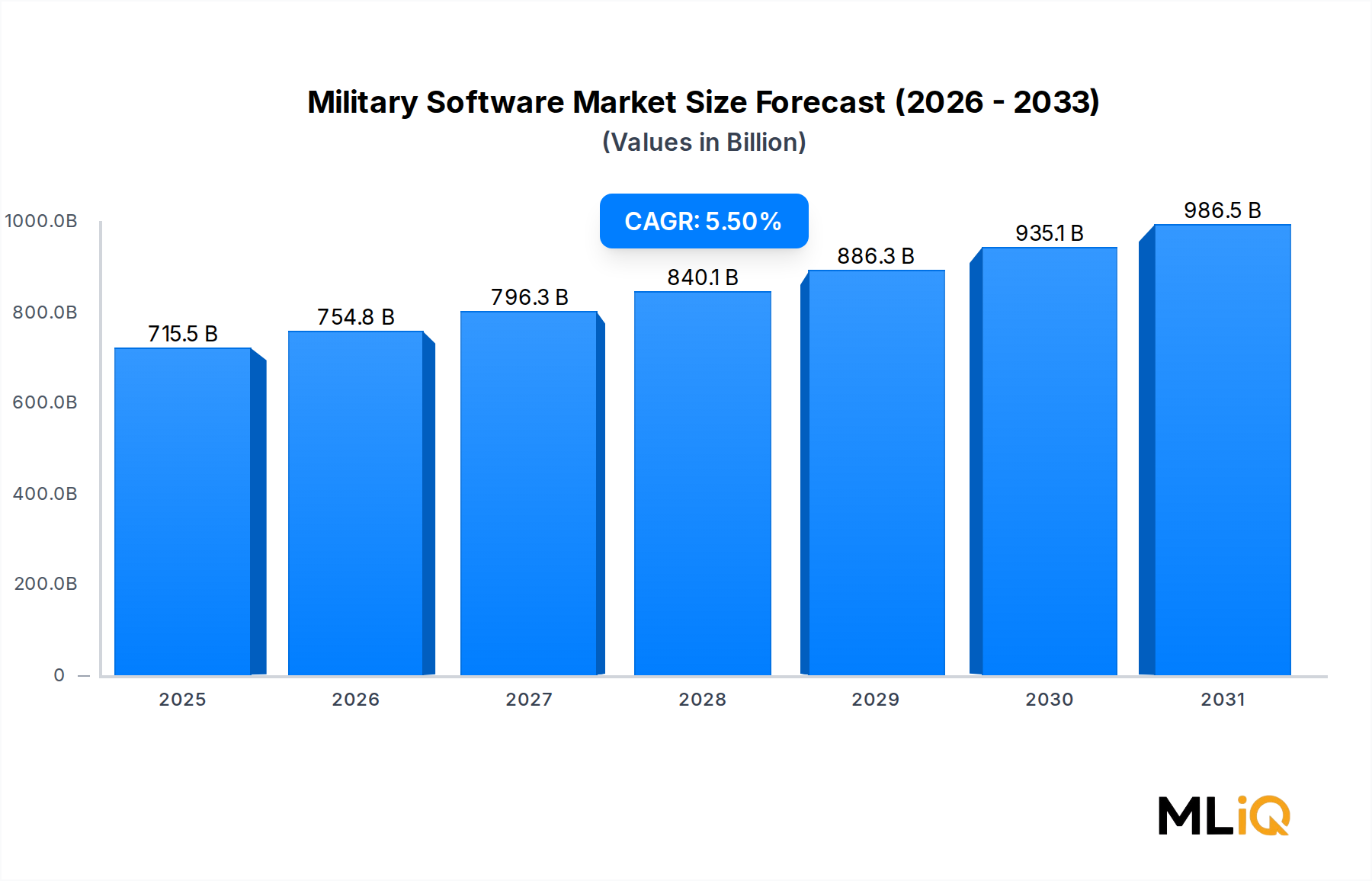

The global Military Software Market is poised for sustained expansion over the coming decade, underpinned by accelerating defense modernization programs, the proliferation of networked warfare platforms, and growing investment in autonomous and AI-driven systems. As of the base year, the market is valued at $715.45 billion, and projections indicate continued robust growth at a compound annual growth rate (CAGR) of 5.5% through 2033. This trajectory reflects an intensifying global security environment, rising geopolitical tensions across multiple theaters, and the structural shift from hardware-centric to software-defined defense architectures.

Demand drivers are multifaceted. Nations across North America, Europe, and the Asia Pacific are aggressively expanding their defense budgets, with software solutions capturing an increasingly large share of total procurement spending. The transition to multi-domain operations — integrating land, naval, air, space, and cyber capabilities — has created an urgent need for interoperable software platforms that can harmonize real-time data flows across heterogeneous systems. This directly elevates requirements for advanced computing, machine learning integration, and cybersecurity resilience within defense software stacks.

Macro tailwinds reinforcing market growth include NATO member commitments to exceed the 2% GDP defense spending threshold, the United States Department of Defense's sustained investment in software modernization under its Digital Modernization Strategy, and parallel initiatives by China, India, South Korea, and Israel to build sovereign defense software capabilities. The commercial technology sector's rapid advancement in cloud-native architectures, edge computing, and large language models is also diffusing into military software development cycles, compressing time-to-deployment and enabling adaptive, upgradeable systems.

From a segmentation perspective, cybersecurity and information processing applications are the two fastest-growing application categories, driven by the exponential rise in cyber threat vectors targeting military infrastructure. On the technology side, learning intelligence — encompassing machine learning, predictive analytics, and AI-assisted decision support — is emerging as a transformative force, supplementing traditional advanced computing approaches that have historically dominated procurement.

Looking forward through 2033, the Military Software Market is expected to consolidate around a smaller number of integrated platform providers who can deliver end-to-end software ecosystems rather than point solutions. The increasing adoption of open-architecture standards, such as the U.S. DoD's Open Mission Systems initiative, is lowering barriers for specialized software firms to compete alongside incumbent prime contractors. Strategic partnerships between defense primes and commercial technology companies are accelerating, further expanding the competitive landscape and injecting agile development methodologies into traditionally slow acquisition pipelines. The outlook remains strongly positive, with geopolitical imperatives ensuring that defense software budgets remain structurally elevated across all major economies.

Within the Military Software Market, the cybersecurity application segment commands the largest revenue share and is simultaneously one of the fastest-growing categories. This dual status — dominance and growth — distinguishes it from more mature segments such as basic information processing, which, while substantial, faces slower incremental expansion as foundational data management systems reach saturation in advanced military forces.

The primacy of cybersecurity within the market stems from a structural reality: every modernization initiative in defense — whether autonomous platforms, networked command systems, or AI-assisted logistics — expands the digital attack surface that adversaries can exploit. Nation-state cyber actors, particularly those affiliated with China, Russia, Iran, and North Korea, have demonstrated both the capability and intent to target military networks, critical infrastructure, and defense industrial base supply chains. High-profile incidents, including intrusions into defense contractor networks and persistent advanced persistent threat (APT) campaigns targeting operational technology in military installations, have elevated cybersecurity from a discretionary investment to a mandatory core capability.

Defense-specific cybersecurity software encompasses several sub-layers: endpoint protection for classified and unclassified networks, intrusion detection and response platforms, zero-trust architecture implementation tools, cryptographic key management systems, and software for securing operational technology and industrial control systems within military bases and naval vessels. Each of these sub-layers represents a distinct procurement category, and the aggregated spend across all of them positions cybersecurity as the dominant application segment.

Governments are institutionalizing cybersecurity software requirements through formal policy mandates. The United States Cybersecurity and Infrastructure Security Agency (CISA) and the DoD's Cybersecurity Maturity Model Certification (CMMC) framework compel defense contractors to meet stringent cybersecurity software standards as a condition of contract award. The European Union's NIS2 Directive similarly tightens requirements for defense-adjacent critical infrastructure operators. These regulatory compulsions create a captive, non-discretionary demand pool that insulates the cybersecurity software segment from budget volatility.

Leading players active in this segment include BAE Systems, which deploys integrated cyber defense platforms for military clients across the Five Eyes alliance, and General Dynamics Corporation, whose Gulfstream-derived secure communications infrastructure underpins classified government networks. IBM Corporation contributes AI-enhanced threat intelligence and security operations center (SOC) capabilities tailored for defense environments. Elbit Systems Ltd. has invested heavily in cyber-electronic warfare convergence platforms, recognizing that the boundary between electronic warfare and cyberattack is increasingly blurred in contested operational environments.

The segment's share is not merely holding steady — it is consolidating. Mid-tier cybersecurity software providers that lack classified clearances and the ability to integrate with legacy military systems are being absorbed through M&A or outcompeted by primes with established program-of-record relationships. The Defense Cyber Security Market broadly is converging with military software procurement, creating a feedback loop that further entrenches the cybersecurity segment's leadership position within the Military Software Market. Vendors that can demonstrate compliance with NIST SP 800-171, the Risk Management Framework (RMF), and international equivalents are capturing disproportionate contract volumes, reinforcing the segment's dominant status through 2033.

Several data-anchored forces are propelling and simultaneously constraining growth within the Military Software Market.

Primary Driver — Rising Defense Budgets and Software-Intensive Modernization: Global defense expenditure exceeded $2.2 trillion in 2023, according to SIPRI, with software and digital systems capturing a growing share of total procurement. The United States alone allocated over $145 billion to research, development, test, and evaluation (RDT&E) in its FY2024 defense budget, with a significant portion directed toward software-intensive programs including the Joint All-Domain Command and Control (JADC2) architecture.

Secondary Driver — AI and Machine Learning Integration: The convergence of the Military Software Market with the Artificial Intelligence in Defense Market is generating new procurement categories that did not exist five years ago. Autonomous target recognition, predictive maintenance algorithms, and AI-enabled logistics optimization are each spawning dedicated software procurement lines across NATO member states.

Tertiary Driver — Proliferation of Networked Platforms: The expansion of platforms tracked within the Unmanned Aerial Vehicle Market and the Military Sensors Market is creating cascading demand for software that can fuse sensor data, manage communications links, and execute decision loops within latency constraints measured in milliseconds. Each new platform deployment generates long-term software sustainment contracts that contribute recurring revenue to market participants.

Primary Constraint — Procurement Cycle Latency: Defense software acquisition cycles remain significantly longer than commercial equivalents, often spanning 5–10 years from requirement definition to operational deployment. This latency disadvantages smaller vendors and slows the pace at which cutting-edge commercial technologies — particularly those in cloud computing and generative AI — can be integrated into fielded military systems.

Secondary Constraint — Interoperability and Legacy Integration Complexity: A substantial share of military IT infrastructure runs on legacy systems, some dating to the 1980s and 1990s, that were never designed for software-defined modernization. Integrating contemporary military software with these systems imposes significant cost overruns and schedule delays, suppressing the addressable market for next-generation solutions in the near term.

The competitive landscape of the Military Software Market is characterized by a tiered structure of large defense primes, specialized software firms, and commercially-derived technology entrants.

BAE Systems: A global defense prime with deep software capabilities spanning cyber defense, electronic warfare signal processing, and battlefield management systems; the company's software division serves clients across the United States, United Kingdom, Australia, and Saudi Arabia under long-term program-of-record contracts.

IBM Corporation: Leverages its hybrid cloud, AI, and cybersecurity portfolio — including IBM Security QRadar — to address defense data analytics and secure operations requirements; the company has pursued multiple partnerships with classified government agencies to deliver AI-enhanced intelligence processing.

Honeywell International, Inc.: Provides avionics software, mission computing platforms, and secure communications systems for military aircraft and rotorcraft; Honeywell's Connected Enterprise platform is being adapted for defense logistics and predictive maintenance applications.

Aselsan A.S.: Turkey's leading defense electronics company, with significant software capabilities in communication systems, electronic warfare, and radar signal processing; Aselsan has expanded its software exports to Middle Eastern and Central Asian markets in recent years.

Elbit Systems Ltd.: An Israel-based defense technology group delivering software for unmanned systems, battlefield digitization, and cyber-electronic warfare convergence; Elbit's Iron Vision helmet-mounted display system exemplifies software-hardware integration for dismounted soldiers.

General Dynamics Corporation: Operates one of the largest defense IT and software businesses in the United States through its Mission Systems and Information Technology divisions; the company is a primary integrator for classified government networks and tactical communications.

Rohde & Schwarz: A German-based technology group specializing in secure military communications software, electronic warfare systems, and software-defined radio platforms; the company serves NATO members with encrypted voice, data, and tactical networking solutions.

Rolta India Limited: Provides geospatial intelligence software, command and control applications, and defense analytics solutions primarily for the Indian Armed Forces; the company holds significant domestic program relationships with the Indian Ministry of Defence.

RTX: Through its Raytheon Intelligence & Space division, RTX delivers advanced signal processing software, electronic warfare systems, and missile guidance software; the company is a major contributor to the U.S. DoD's JADC2 initiatives.

Teledyne FLIR LLC: Specializes in thermal imaging sensor software, autonomous vehicle perception algorithms, and surveillance analytics; Teledyne FLIR's software platforms are embedded in ground robotics, unmanned systems, and force protection applications across allied militaries.

January 2024: The U.S. Department of Defense released its updated Software Acquisition Pathway policy, formalizing agile and DevSecOps methodologies as the preferred approach for all new military software programs, directly reshaping procurement practices across the industry.

March 2024: General Dynamics Corporation was awarded a $2.8 billion contract extension for the development and sustainment of the Warfighter Information Network-Tactical (WIN-T) software infrastructure, underscoring continued U.S. Army investment in battlefield communications software.

May 2024: Elbit Systems Ltd. announced the successful integration of its Iron Fist active protection system software with a new generation of modular open systems architecture (MOSA)-compliant combat vehicle platforms, demonstrating interoperability across allied partners.

August 2024: NATO's Communications and Information Agency (NCIA) awarded a multi-year contract for the development of federated mission networking software to a consortium including BAE Systems and IBM Corporation, targeting interoperability across all 32 member states.

October 2024: Rohde & Schwarz unveiled its next-generation software-defined radio platform, the M3SR Series 4400, incorporating AI-assisted spectrum management capabilities designed to operate in heavily contested electromagnetic environments.

February 2025: RTX's Raytheon division completed the first operational deployment of its AI-enabled electronic warfare management software aboard a U.S. Navy EA-18G Growler aircraft, marking a milestone in software-driven airborne electronic attack capability.

April 2025: India's Ministry of Defence approved a $1.1 billion indigenization program for military software, with Rolta India Limited identified as a key domestic beneficiary, reinforcing the country's Atmanirbhar Bharat (self-reliant India) defense policy.

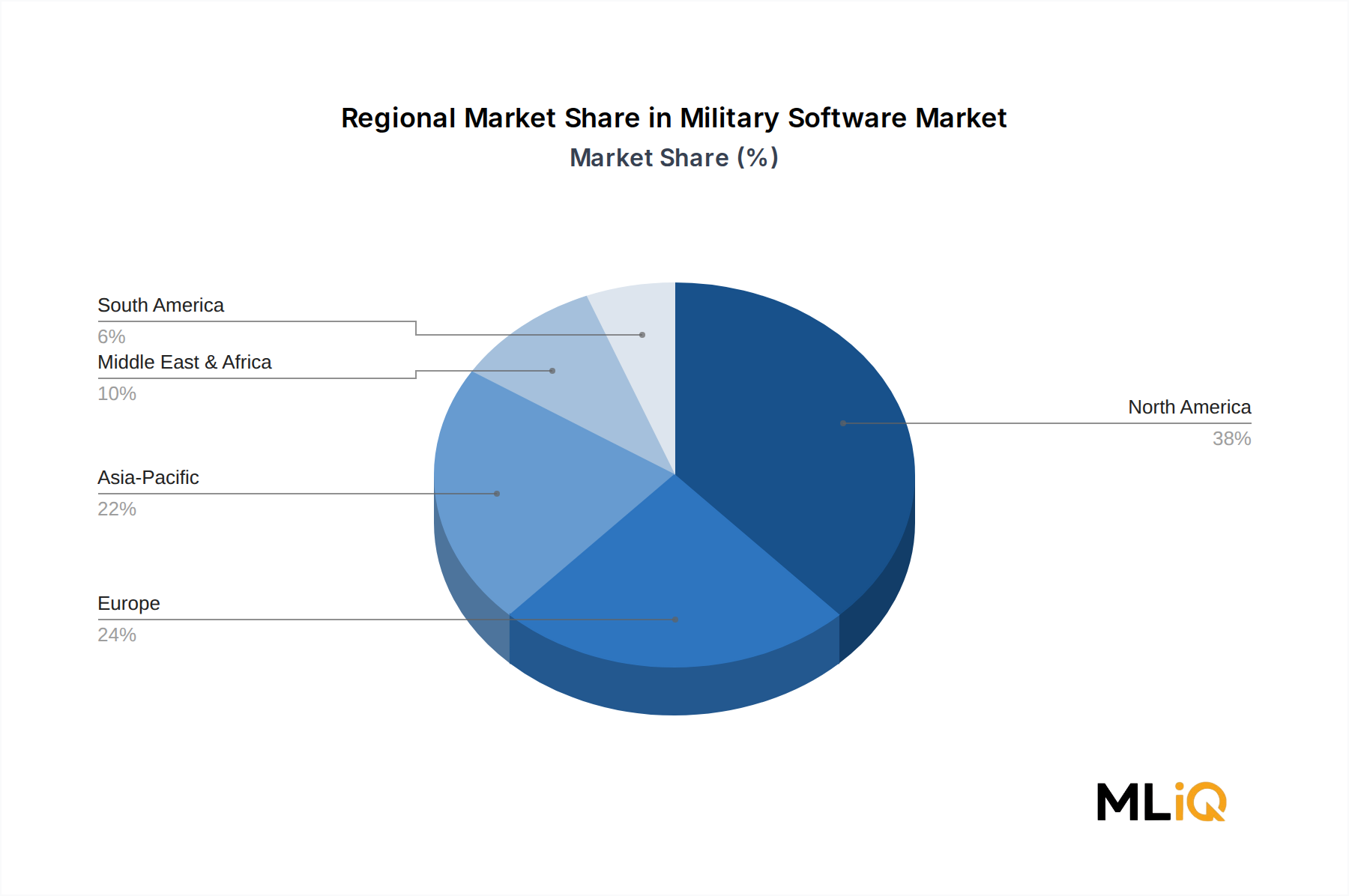

North America remains the most mature and the largest revenue-generating region in the Military Software Market, accounting for an estimated 38–42% of global market value. The United States is the dominant country-level contributor, driven by the DoD's multi-billion-dollar investments in JADC2, cyber capabilities, and AI-enabled decision support. The U.S. defense software budget is structurally supported by bipartisan congressional backing, ensuring relative insulation from fiscal cycle volatility. Canada and Mexico contribute modestly, primarily through NATO-interoperable communications software procurement and border security applications, respectively. North America's CAGR is estimated at 4.8% through 2033, reflecting a mature but consistently expanding base.

Europe is the second-largest regional market, with the United Kingdom, Germany, and France leading procurement volumes. Post-2022 geopolitical developments, particularly the Russia-Ukraine conflict, have catalyzed a significant acceleration in European defense software spending, with NATO members committing to accelerated digitization of land forces and enhanced cyber defense capabilities. Germany's Zeitenwende policy, which reallocated €100 billion toward defense modernization, includes substantial software procurement for command, control, and communications systems. Europe's regional CAGR is estimated at 5.8%, marginally above the global average.

Asia Pacific is the fastest-growing regional market, with a projected CAGR of 6.9% through 2033. China's continued military modernization, India's indigenization push under the Defence Acquisition Procedure 2020, and South Korea's and Japan's expanding defense software investments collectively drive this outperformance. The Command and Control Systems Market in Asia Pacific is a particularly active procurement category, as regional powers seek to develop sovereign situational awareness capabilities independent of Western supply chains.

The Middle East & Africa region is experiencing accelerating growth, particularly in GCC states (Saudi Arabia, UAE, Qatar), which are investing in military software for border security, unmanned systems integration, and electronic warfare. Israel remains a technology exporter and innovation hub, with Elbit Systems Ltd. and Rafael Advanced Defense Systems anchoring a robust domestic software ecosystem. Regional CAGR is estimated at 5.2%.

South America represents the smallest market share, with Brazil as the primary participant through its SISFRON border monitoring program and naval software modernization initiatives. Growth is constrained by fiscal pressures and currency volatility, with a modest regional CAGR of approximately 3.4% through 2033.

The Military Software Market has attracted significant and increasingly diversified capital flows over the 2022–2025 period, spanning traditional prime contractor M&A, venture capital, and government-sponsored investment vehicles.

M&A activity has been particularly pronounced in the cybersecurity and AI sub-segments. Large defense primes have moved aggressively to acquire commercial software talent and technology, recognizing that organic development timelines are incompatible with the pace of threat evolution. RTX acquired several smaller AI and data analytics firms to bolster its intelligence software capabilities, while General Dynamics expanded its IT services portfolio through targeted acquisitions of cleared software developers.

Venture capital and private equity have discovered the defense software sector as a resilient, non-cyclical investment category. Firms such as Andreessen Horowitz (through its dedicated defense technology fund), Shield Capital, and Paladin Capital Group have deployed hundreds of millions of dollars into defense software startups, with a concentration on autonomous systems software, AI-enabled mission planning tools, and zero-trust cybersecurity platforms. The Embedded Computing Market has emerged as a particularly active focus for PE roll-up strategies, as integrators consolidate rugged hardware-software platform providers.

Strategic partnerships between defense primes and hyperscale cloud providers — notably Microsoft's JEDI/JWCC contract trajectory with DoD, and AWS's classified cloud infrastructure — are reshaping how military software is developed, tested, and deployed. These partnerships inject commercial agility into government software programs while providing cloud providers with access to one of the world's most technically demanding customer bases.

The Military Simulation and Training Market sub-segment has attracted dedicated investment from simulation-focused private equity, driven by the recognition that software-based training systems offer a cost-

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.5% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Military Software Market market expansion.

Key companies in the market include BAE Systems, IBM Corporation, Honeywell International, Inc., Aselsan A.S., Elbit Systems Ltd., General Dynamics Corporation, Rohde & Schwarz, Rolta India Limited, RTX, Teledyne FLIR LLC.

The market segments include Type, Technology, Application.

The market size is estimated to be USD 715.45 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3222, USD 5370, and USD 8995 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Military Software Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Military Software Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.