1. What are the major growth drivers for the Aircraft Doors Market market?

Factors such as are projected to boost the Aircraft Doors Market market expansion.

+1 2315155523

Aircraft Doors Market

Aircraft Doors Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

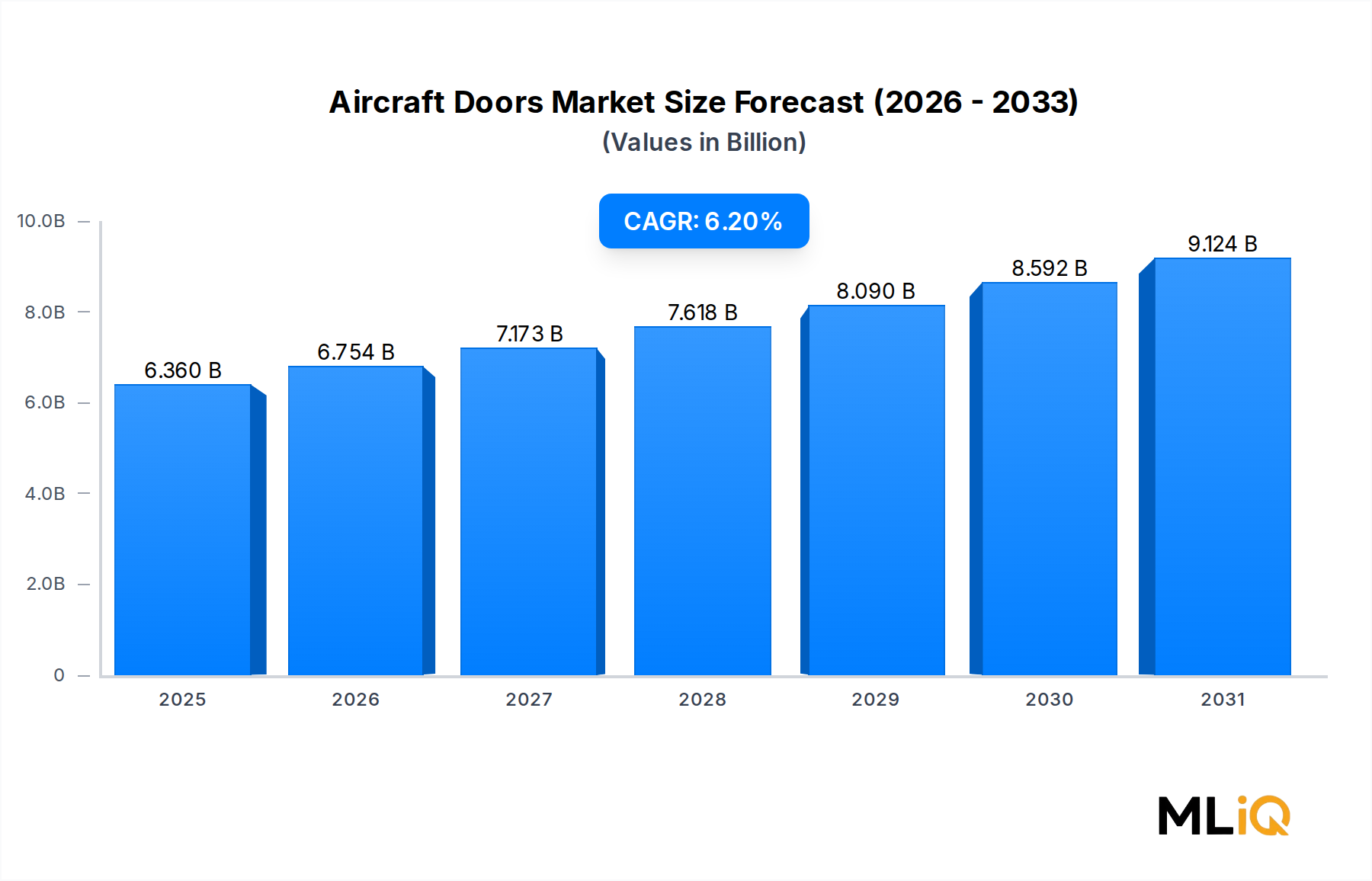

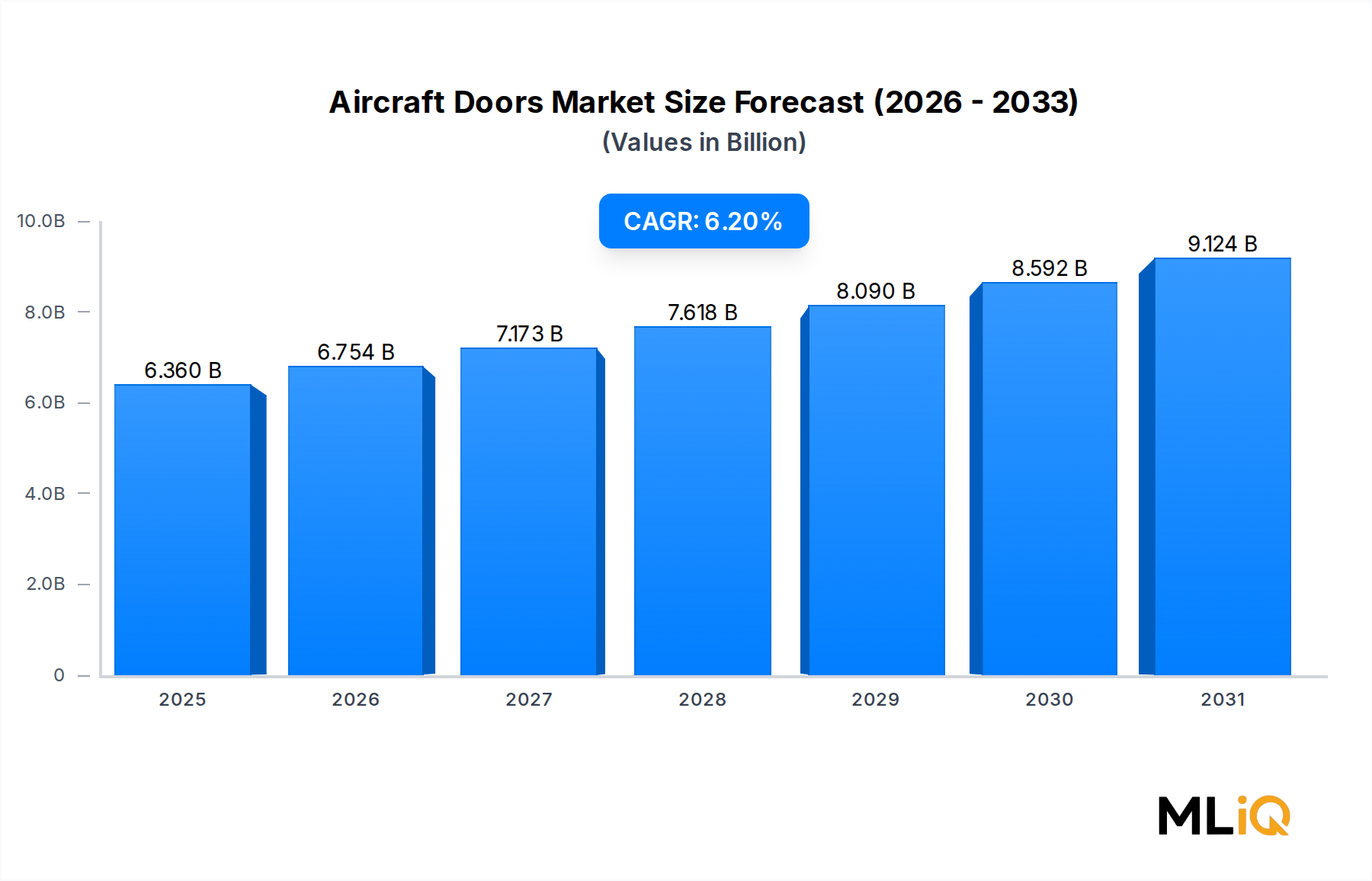

The global Aircraft Doors Market is valued at $6.36 billion as of the base year and is forecast to expand at a compound annual growth rate of 6.2% over the projection period, reflecting robust structural demand from both commercial aviation recovery and defense fleet modernization. The market encompasses a broad spectrum of door configurations—passenger doors, cargo doors, emergency exits, cockpit doors, and specialized access panels—serving original equipment manufacturers (OEMs) and the aftermarket channel across civil and military platforms.

A primary macro tailwind is the accelerating pace of global air traffic recovery following pandemic-era disruptions. The International Air Transport Association (IATA) has reported passenger volumes approaching and, in select regions, surpassing 2019 levels, directly stimulating new aircraft orders. Airbus and Boeing backlogs collectively exceed 12,000 aircraft units, each requiring multiple certified door assemblies, which structurally underpins near- to medium-term demand for door manufacturers and Tier-1 suppliers.

On the defense side, geopolitical realignments—particularly NATO member spending commitments and Indo-Pacific theater build-ups—are driving procurement of new military transport, surveillance, and multi-role aircraft, each demanding ruggedized door solutions rated for extreme operational envelopes. This dual-market exposure insulates the Aircraft Doors Market from single-sector cyclicality.

Lightweighting imperatives are reshaping product design. Regulatory pressure on fuel efficiency and airlines' own net-zero commitments are compelling OEMs to specify advanced composite panels and hybrid metallic-composite door structures, increasing the average unit value of door assemblies and lifting revenue per aircraft delivered. Thermoplastic composites, titanium fastener systems, and smart sensor-integrated latching mechanisms are transitioning from experimental to serial-production status, adding premium content per shipset.

Aftermarket dynamics represent a significant growth vector. With a global commercial fleet exceeding 28,000 active narrowbody and widebody jets, door overhaul, seal replacement, hinge refurbishment, and full door swap cycles generate recurring, high-margin revenue streams that are largely decoupled from new production volatility. Airlines operating on thin margins increasingly outsource these services to specialized MRO providers, expanding the addressable aftermarket pool.

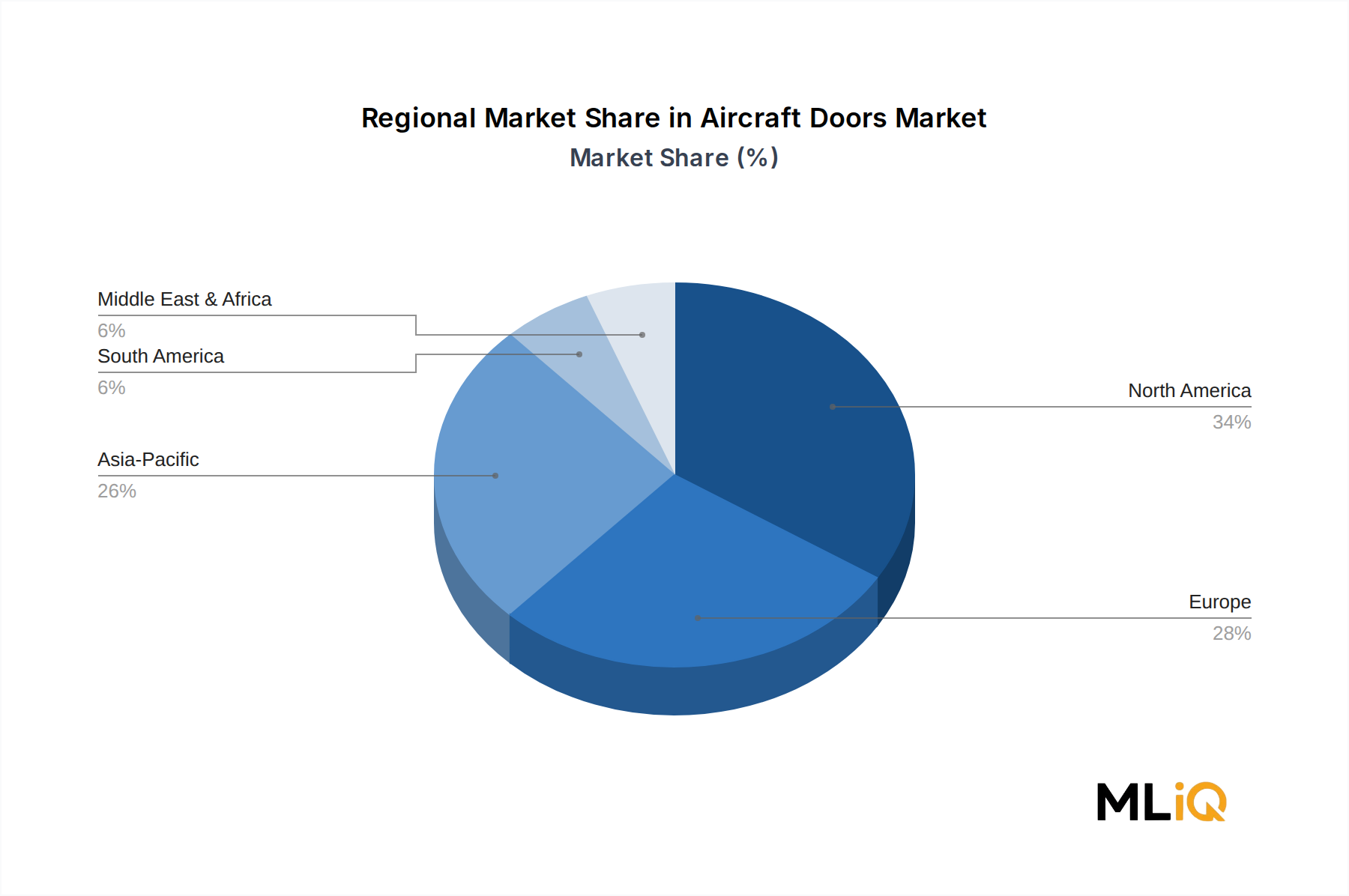

Geographically, Asia Pacific is the fastest-growing regional market, propelled by Chinese domestic aviation expansion, Indian fleet growth, and Southeast Asian low-cost carrier proliferation. North America retains the largest absolute revenue share owing to its dense OEM and MRO ecosystem. Looking ahead, the convergence of advanced manufacturing techniques, digitalized supply chains, and electrified/hybrid propulsion architectures for urban air mobility platforms will open entirely new door-system design requirements, extending the market's secular growth runway well into the 2030s.

Within the Aircraft Doors Market's segmentation by aircraft type, the commercial aviation segment commands the dominant revenue share, a position that reflects the sheer volume of civil aircraft in production and operation globally. Commercial aircraft—spanning narrowbody single-aisle jets such as the Airbus A320neo family and Boeing 737 MAX, widebody twin-aisle platforms including the A350, A330neo, 787 Dreamliner, and 777X, as well as regional jets—collectively require the highest door counts per fleet unit compared to their military counterparts. A single narrowbody aircraft typically integrates between 8 and 12 door assemblies (including passenger, emergency, and cargo variants), while widebody jets may incorporate 16 or more certified door units per airframe.

The dominance of the commercial segment is structurally reinforced by the duopolistic production cadence of Airbus and Boeing, whose combined annual delivery rates are on a trajectory toward 1,200–1,400 aircraft per year by the late 2020s, contingent on supply chain normalization. Each delivery represents a confirmed, contractually binding door shipset order, creating highly predictable revenue visibility for Tier-1 door suppliers such as Groupe Latécoère and Collins Aerospace. The OEM channel within the commercial segment accounts for the majority of new-build door revenue, while the aftermarket sub-channel captures ongoing maintenance, repair, and overhaul spend across the installed fleet.

Passenger doors are the highest-value sub-segment within commercial aircraft door systems. These doors must satisfy rigorous airworthiness standards—including FAA FAR Part 25 and EASA CS-25 certification—covering pressure differential loads, evacuation slide compatibility, emergency egress timing, and fail-safe latching. The engineering complexity translates directly to higher average selling prices and significant barriers to entry for new suppliers. Groupe Latécoère, a vertically integrated French aerospace specialist, has long-term supply agreements with Airbus covering A320 and A350 fuselage sections and doors, illustrating the deep programmatic embeds that characterize this segment.

Emergency exits represent a technically distinct and growing sub-segment. Regulatory agencies have tightened evacuation certification standards in the wake of high-profile incidents, requiring more frequent overhaul intervals and, in some cases, retroactive design modifications. This regulatory dynamic is additive to aftermarket revenue for the commercial segment.

Cargo doors, while lower in unit count per aircraft, command premium pricing due to the structural loads they must withstand during pressurization cycling and ground loading operations. The surge in dedicated freighter conversions—driven by e-commerce logistics demand—has created incremental cargo door demand beyond what new-production narrowbodies generate, as passenger-to-freighter (PTF) conversion programs require certified cargo door installations in repurposed fuselage panels.

The commercial segment's share is expected to consolidate further as next-generation narrowbody replacement programs and potential new-entrant aircraft from Chinese manufacturer COMAC (C919 ramp-up) and other regional programs add additional demand layers. The ongoing adoption of advanced composites and smart door health monitoring systems within commercial platforms also elevates average revenue per shipset, supporting both topline growth and margin improvement for established suppliers. The Aerospace and Defense Market broadly benefits from these commercial aviation tailwinds, but the aircraft doors sub-vertical is particularly well-positioned given its programmatic stability and aftermarket depth.

Several quantifiable forces are driving revenue expansion in the Aircraft Doors Market, while a distinct set of constraints moderates the pace of growth.

Driver 1 — New Aircraft Order Backlogs: Airbus reported a backlog of approximately 8,600 aircraft as of early 2024, while Boeing's backlog stood near 5,600 units. These combined figures translate to roughly 7–9 years of production at current delivery rates, providing extraordinary long-cycle revenue assurance to door system suppliers. Each backlog unit represents a committed door shipset, making this the single most significant demand driver in the market.

Driver 2 — Defense Spending Escalation: NATO member nations have committed to defense budgets of at least 2% of GDP, with several members exceeding this threshold. The United States Department of Defense's fiscal 2024 budget allocated over $140 billion to aircraft procurement and R&D, a portion of which flows into door system contracts for military transport and tactical aircraft. This drives demand in the Military Aircraft Market, which is an important adjacent segment for door suppliers offering hardened, blast-resistant, and pressure-capable door architectures.

Driver 3 — Aftermarket Service Intensity: Industry data indicates that commercial aircraft doors undergo full overhaul cycles every 6–12 years depending on utilization and operator maintenance programs. With a global fleet age averaging over 12 years for narrowbodies, a significant proportion of in-service doors are approaching or within overhaul windows, structurally elevating aftermarket revenue.

Constraint 1 — Supply Chain Fragility: The aerospace supply chain remains under stress post-pandemic. Titanium shortages following Russia-Ukraine trade disruptions and ongoing labor shortages at Tier-2 and Tier-3 fabricators have caused delivery delays and cost inflation for door manufacturers, compressing margins and limiting output growth rates.

Constraint 2 — Certification Lead Times: FAA and EASA certification for new door designs—particularly those incorporating novel composite architectures or electronic latch systems—can extend 3–5 years, delaying time-to-market for next-generation products and limiting competitive entry.

Constraint 3 — Concentration Risk: The market's reliance on two primary OEM customers (Airbus and Boeing) means that production rate changes at either manufacturer disproportionately impact supplier revenue, as evidenced by the 2019–2021 Boeing 737 MAX grounding and subsequent rate cuts.

Potez Aéronautique: A French aerospace manufacturer with deep roots in structural aerostructures, Potez Aéronautique provides specialized door assemblies and access panels for both civil and military platforms, leveraging its precision metalworking heritage to serve European OEM programs.

Groupe Latécoère: One of the world's most established aerostructures specialists, Groupe Latécoère holds long-term supply agreements with Airbus for fuselage sections and passenger doors on the A320 and A350 families, making it a pivotal Tier-1 supplier with integrated design-to-delivery capabilities.

Airbus: As both an OEM and an internal door systems developer, Airbus drives design specifications and airworthiness standards for its entire aircraft family, influencing the supply ecosystem through in-house design authority and strategic supplier selection processes.

SAAB: The Swedish aerospace and defense group supplies structural components and door systems for military and commercial aircraft, with particular expertise in composite aerostructures supporting next-generation fighter and transport platforms through its Aerostructures business unit.

Aviation Technical Services: A U.S.-based MRO provider, Aviation Technical Services delivers door overhaul, repair, and replacement services for commercial airline fleets, occupying a critical position in the aftermarket channel with FAA-approved repair station certifications.

Primus Aerospace: Specializing in precision machined components and complex assemblies for aerospace primes, Primus Aerospace supplies structural door components—including hinges, fittings, and frames—to major OEMs and Tier-1 integrators across North America and Europe.

Hellenic Aerospace Industry: The state-linked Greek aerospace company provides maintenance, overhaul, and manufacturing support for military and civil aircraft structures including door assemblies, serving NATO alliance operators and international commercial clients.

Collins Aerospace: A Raytheon Technologies subsidiary and global aerospace systems leader, Collins Aerospace delivers highly engineered door systems—including cargo and emergency exit assemblies—with advanced sealing, actuation, and monitoring technologies integrated across major commercial and defense platforms.

Altitude Aerospace: A mid-market aerostructures supplier with specialized capabilities in composite and metallic door panel fabrication, Altitude Aerospace serves regional aircraft OEMs and PTF conversion programs requiring certified structural modifications.

FACC AG: The Austrian composite aerostructures specialist manufactures lightweight composite door panels and interior structural components for Airbus and Boeing programs, with a strong technology position in thermoplastic and thermoset composite door architectures that align with OEM lightweighting mandates.

January 2024: Collins Aerospace announced the successful completion of qualification testing for its next-generation composite cargo door system intended for widebody freighter conversions, achieving a 15% weight reduction versus the incumbent metallic baseline.

March 2024: Groupe Latécoère secured a multi-year contract extension with Airbus covering door and fuselage section deliveries for the A320neo family at increased production rates aligned with Airbus's ramp-up toward 75 aircraft per month.

May 2024: FACC AG unveiled a thermoplastic composite passenger door panel prototype at the Aircraft Interiors Expo in Hamburg, marking a significant advance toward serial thermoplastic door production with recyclability credentials supporting airline sustainability commitments.

July 2024: The FAA issued an Airworthiness Directive (AD) requiring enhanced inspection intervals for specific Boeing 737 plug-type door assemblies following the January 2024 mid-flight door panel separation incident on an Alaska Airlines 737 MAX 9, directly impacting aftermarket inspection and overhaul revenue across the U.S. commercial fleet.

September 2024: SAAB's Aerostructures division announced a partnership with a Nordic composite materials supplier to co-develop next-generation blast-resistant door panels for military transport aircraft, targeting NATO procurement cycles commencing 2026.

November 2024: Hellenic Aerospace Industry signed an MRO services agreement with a Middle Eastern carrier to provide door overhaul and recertification services for a 50-aircraft A320 family fleet, strengthening its commercial aftermarket revenue base.

February 2025: Primus Aerospace expanded its Wichita, Kansas precision machining facility to increase door fitting and hinge production capacity by 30%, responding to rising OEM delivery rate demands from both Airbus and Boeing supply chain partners.

The Aircraft Doors Market is served by two structurally distinct end-user segments: OEMs and the aftermarket, each exhibiting markedly different purchasing criteria, procurement channels, and price sensitivity profiles.

OEM customers—principally Airbus, Boeing, COMAC, Embraer, and military prime contractors—are the dominant revenue generators at the new-build stage. Their procurement is characterized by long-cycle, program-level sourcing decisions made years in advance of production, governed by rigorous supplier qualification processes, and structured through multi-year supply agreements with volume commitments. Price sensitivity at this tier is moderated by engineering specification compliance, certification standing, delivery reliability, and total lifecycle cost rather than spot pricing. OEM buyers increasingly mandate design collaboration from Tier-1 suppliers, expecting door vendors to hold design authority, manage sub-tier sourcing, and deliver fully assembled shipsets with integrated actuation and sealing systems. The shift toward "risk-sharing supplier" models means that Tier-1 door suppliers co-invest in non-recurring engineering costs in exchange for long-term exclusivity on specific programs, reducing OEM procurement risk but increasing supplier capital commitment.

Aftermarket buyers encompass commercial airlines, military operators, MRO service providers, and PTF conversion specialists. This segment is more price-competitive and transactional, with procurement driven by airworthiness compliance deadlines, lease return conditions, and unscheduled maintenance events. Airlines operating under thin margin structures exhibit high price sensitivity for consumable door components—seals, hinges, actuator assemblies—but prioritize FAA/EASA-approved parts to avoid certification risk. Low-cost carriers have been observed deferring non-mandatory door refurbishments to the latest permissible maintenance window, compressing short-cycle aftermarket demand but creating concentrated demand spikes at overhaul due dates.

A notable shift in buyer behavior is the growing adoption of power-by-the-hour (PBH) and component-as-a-service contracting models, where airlines pay per flight cycle for door system availability rather than purchasing components outright. This model, pioneered in engine and avionics markets, is gaining traction in the structural door aftermarket as MRO providers seek to lock in recurring revenue streams. The Aircraft MRO Market dynamics are directly influencing this behavioral shift, as integrated MRO providers bundle door services into broader airframe maintenance contracts. Additionally, the increasing complexity of composite door structures is shifting procurement toward OEM-certified repair stations, reducing the pool of competitive aftermarket providers and marginally elevating pricing power for qualified MRO vendors.

Regulatory frameworks governing the Aircraft Doors Market are among the most stringent in the broader manufacturing sector, reflecting the direct safety implications of door system failures at altitude and during ground operations.

In the United States, the Federal Aviation Administration (FAA) regulates civil aircraft doors under Title 14 of the Code of Federal Regulations, specifically FAR Part 25 (Transport Category Airplanes) and FAR Part 23 (Normal Category), which establish mandatory requirements for door structural integrity, emergency evacuation compatibility, latching mechanism reliability, and pressurization load resistance. The January 2024 Alaska Airlines door panel incident prompted the FAA to issue emergency Airworthiness Directives with enhanced inspection mandates, and the agency subsequently announced a broader review of plug-type door design certification standards, signaling potential rule tightening that could mandate retroactive structural modifications across affected fleets.

In Europe

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Aircraft Doors Market market expansion.

Key companies in the market include Potez Aéronautique, Groupe Latécoère, Airbus, SAAB, Aviation Technical Services, Primus Aerospace, Hellenic Aerospace Industry, Collins Aerospace, Altitude Aerospace, FACC AG.

The market segments include Door Type, Aircraft Type, End-user.

The market size is estimated to be USD 6.36 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Aircraft Doors Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Aircraft Doors Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.