1. What are the major growth drivers for the Digital Power Management Multichannel IC Market market?

Factors such as are projected to boost the Digital Power Management Multichannel IC Market market expansion.

+1 2315155523

Digital Power Management Multichannel IC Market

Digital Power Management Multichannel IC Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

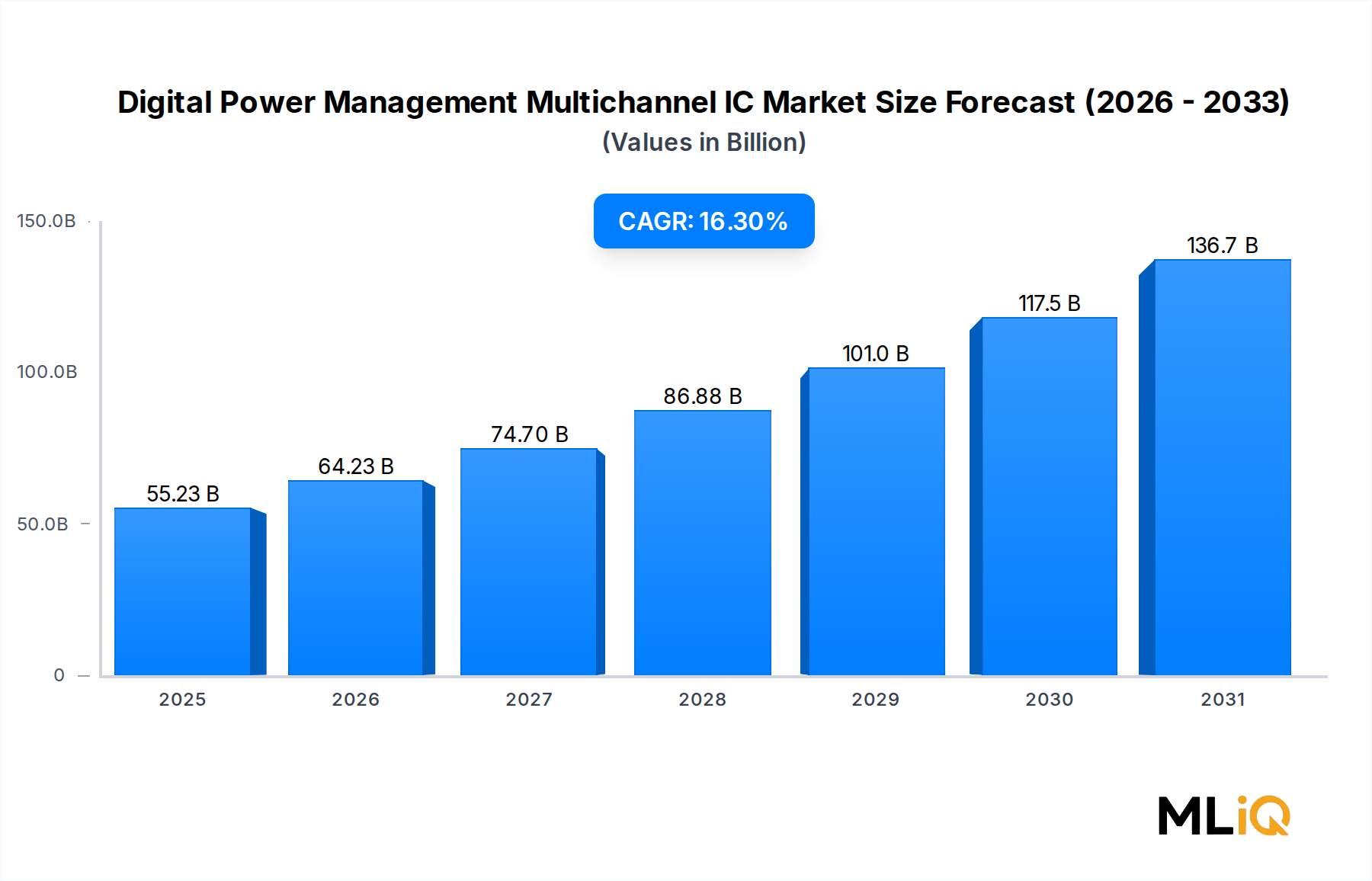

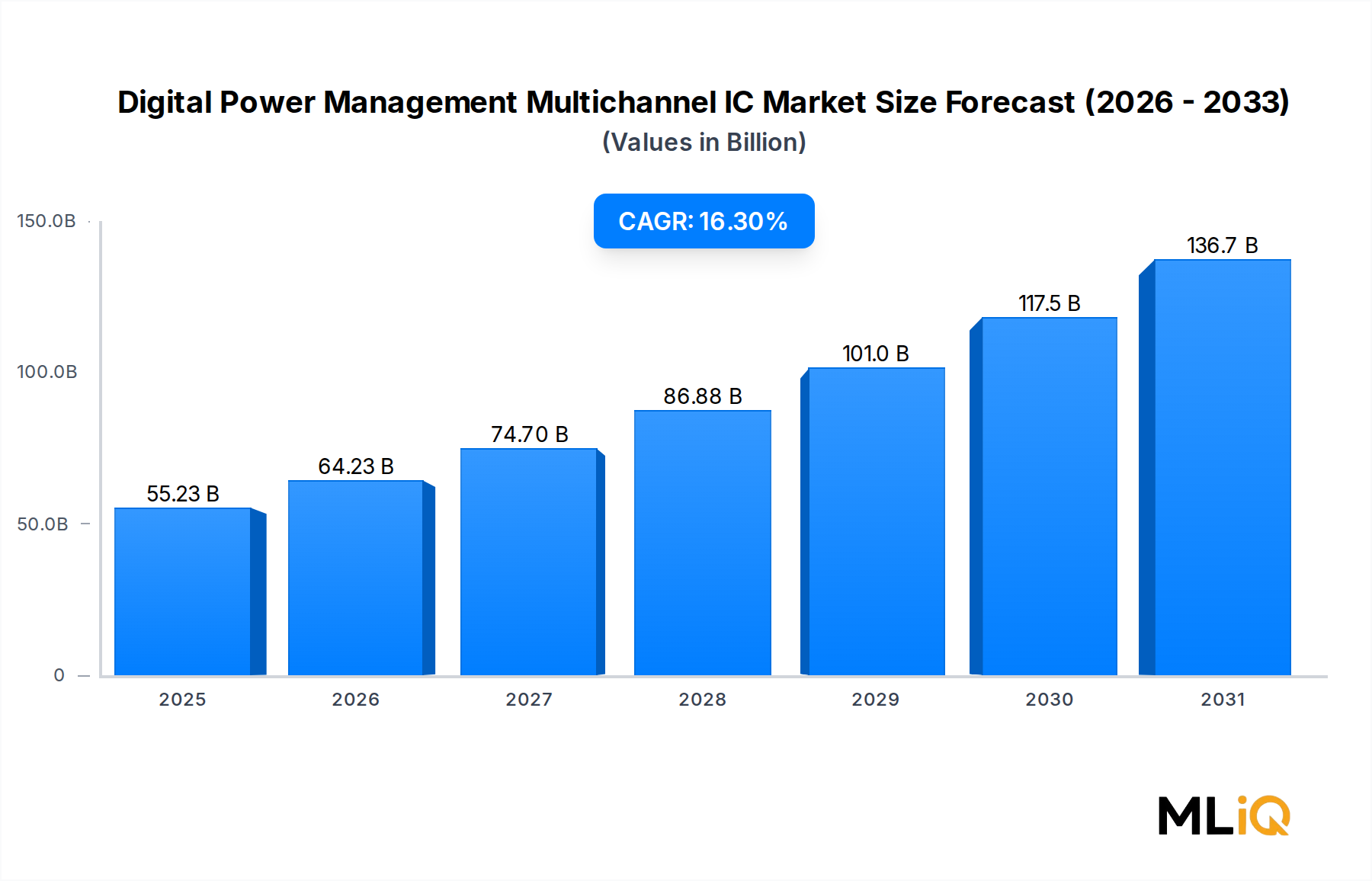

The global Digital Power Management Multichannel IC Market is poised for robust, sustained expansion over the forecast horizon. As of the base assessment period, the market is valued at approximately $55,227.78 million, driven by accelerating semiconductor integration requirements across consumer, industrial, automotive, and telecommunications verticals. The market is projected to grow at a compound annual growth rate (CAGR) of 16.3%, reflecting strong demand for energy-efficient, highly integrated power management solutions that can handle multiple voltage rails and dynamic load conditions simultaneously.

The proliferation of advanced node processors, system-on-chip (SoC) architectures, and artificial intelligence accelerators has dramatically increased the complexity of power delivery networks. Modern compute platforms require precise, programmable, and real-time power regulation across dozens of independent channels — a functional requirement that multichannel digital power management ICs are uniquely positioned to satisfy. This structural shift from analog to digital power control is one of the most significant catalysts behind the market's double-digit CAGR trajectory.

From a macro perspective, the global push toward electrification — spanning electric vehicles, renewable energy storage systems, smart grid infrastructure, and 5G base stations — is generating multifaceted demand vectors. Governments in the United States, European Union, China, South Korea, and Japan are deploying industrial policy frameworks that incentivize domestic semiconductor production and energy efficiency compliance, directly benefiting multichannel power management IC suppliers.

On the supply side, leading semiconductor companies are channeling unprecedented capital expenditure into advanced fabrication nodes (7nm, 5nm, and below), where power density and thermal management challenges are most acute. The ability to digitally program, monitor, and telemetry power delivery in real time differentiates multichannel digital ICs from legacy analog counterparts, justifying premium pricing and attracting design wins across high-margin end markets.

Key demand drivers include: the global rollout of 5G infrastructure requiring high-efficiency power management for radio access network (RAN) equipment; the migration to DDR5 and LPDDR5 memory platforms that demand tighter voltage tolerances; and the rapid adoption of AI inference hardware in data centers, where power budgets are critically constrained. Additionally, the miniaturization trend in wearable and portable devices places a premium on highly integrated, low-quiescent-current multichannel solutions.

Looking ahead, the market's forward trajectory appears anchored by structural, not cyclical, growth drivers. As edge AI, autonomous vehicles, and industrial IoT platforms mature into mass deployment phases, the demand for sophisticated multichannel digital power management will intensify further, sustaining the 16.3% CAGR well through the latter half of the forecast period.

Among all application segments tracked within the Digital Power Management Multichannel IC Market, Consumer Electronics consistently commands the largest revenue share, a position reinforced by both volume intensity and the accelerating complexity of end-device power architectures. Smartphones, tablets, laptops, smart TVs, gaming consoles, wearables, and truly wireless stereo (TWS) audio devices collectively represent the highest-volume deployment environment for multichannel power management ICs globally.

The dominance of consumer electronics is rooted in several reinforcing structural dynamics. First, the form factor miniaturization imperative in portable electronics demands highly integrated, space-efficient power management solutions. A modern flagship smartphone may require eight to twelve independently regulated voltage domains to power its application processor, memory stack, display driver, RF front-end, camera module, and always-on sensor hub — a configuration that only multichannel digital ICs can handle within the thermal and spatial budget available to OEM designers.

Second, the consumer electronics segment benefits from the shortest product refresh cycles of any end market. Annual or biennial product transitions at major smartphone OEMs create recurring design-win opportunities and a perpetual demand refresh cycle for power management IC suppliers. Companies like Texas Instruments Inc., Dialog Semiconductor Plc., and Qualcomm, Inc. have historically secured a disproportionate share of design wins in this segment by offering tightly co-engineered power management solutions alongside their application processor and connectivity chipset portfolios.

Third, the transition to USB Power Delivery (USB-PD) and GaN-based fast charging architectures has introduced a new layer of complexity — and opportunity — in consumer electronics power management. Fast chargers capable of delivering 45W, 65W, or even 100W to portable devices require sophisticated multichannel controllers that manage input voltage regulation, battery charging algorithms, system load balancing, and thermal cutoff simultaneously. This functional expansion increases the average selling price (ASP) of multichannel ICs deployed in premium consumer devices.

The segment's share is currently consolidating rather than fragmenting, as Tier-1 smartphone OEMs — including those based in China, South Korea, and the United States — increasingly shift toward custom power management ICs developed in partnership with a small cohort of trusted semiconductor partners. This trend toward co-development relationships reduces the addressable market for merchant market suppliers while simultaneously increasing the value per design win for those who secure strategic partnerships.

Notably, the gaming console and PC markets have emerged as secondary growth engines within consumer electronics. Next-generation gaming platforms and high-performance laptops equipped with discrete GPU architectures require power delivery networks capable of managing rapid transient responses — a capability that digital multichannel ICs with telemetry feedback loops handle more effectively than legacy analog alternatives.

The wearables sub-segment — including smartwatches, fitness trackers, and hearables — presents a distinct but equally compelling opportunity. These devices operate under extreme power budget constraints, where quiescent current measured in nanoamperes and sleep-mode efficiency can determine battery life outcomes over multiple years of use. Specialized multichannel ICs optimized for ultra-low-power wearable applications represent one of the fastest-growing niches within the broader consumer electronics segment, with several fabless and IDM suppliers introducing purpose-built product families targeting this vertical.

Overall, the Consumer Electronics application segment is expected to maintain its leading revenue share position throughout the forecast period, even as automotive and industrial verticals grow at comparatively faster absolute rates. The sheer volume of devices deployed annually and the increasing power management complexity per device ensure that this segment remains the market's revenue anchor.

The Digital Power Management Multichannel IC Market is shaped by a constellation of quantifiable drivers and measurable constraints that collectively determine its growth trajectory at a 16.3% CAGR.

Primary Driver — 5G Infrastructure Buildout: Global 5G capital expenditure by telecom operators is projected to exceed $900 billion cumulatively through 2030, according to industry infrastructure spend trackers. Each 5G base station requires up to three times the power management complexity of its 4G LTE predecessor, directly expanding the total addressable market for multichannel digital power ICs in the Telecom & Networking application segment.

Primary Driver — Data Center AI Expansion: Hyperscale data center operators are deploying AI accelerator clusters (GPUs, TPUs, custom ASICs) at an unprecedented rate. Each AI accelerator rack may consume 10kW to 30kW, demanding sophisticated per-chip and per-board power regulation. The shift from 12V bus architectures to 48V power distribution buses has catalyzed demand for new multichannel step-down regulators, directly benefiting vendors with advanced digital controller portfolios.

Primary Driver — Automotive Electrification: The global electric vehicle (EV) market surpassed 10 million annual unit sales in recent years, with battery electric vehicles requiring complex battery management systems and multi-domain power architectures (ADAS, infotainment, drivetrain). This trend is a major stimulus for the Automotive Semiconductor Market and directly drives demand for automotive-grade multichannel power management ICs with AEC-Q100 qualification.

Key Constraint — Supply Chain Geopolitical Risk: Semiconductor supply chain concentration in Taiwan and South Korea introduces systemic risk. The U.S. CHIPS and Science Act and EU Chips Act are structural policy responses, but capacity rebalancing will take three to five years, creating near-term supply uncertainty that limits revenue realization during ramp phases.

Key Constraint — Design Complexity and Engineering Talent Shortage: Multichannel digital power management IC design requires specialized expertise in mixed-signal circuit design, firmware development, and system-level power architecture. The global shortage of qualified power electronics engineers creates design cycle delays, particularly at smaller OEMs and start-ups, which can slow market adoption rates in emerging application segments.

Key Constraint — Pricing Pressure in Consumer Segments: Aggressive competition among merchant market suppliers and the trend toward OEM in-house IC development compress ASPs in the consumer electronics channel, partially offsetting volume growth benefits.

The competitive landscape of the Digital Power Management Multichannel IC Market is characterized by a mix of vertically integrated IDMs, fabless specialists, and diversified analog semiconductor conglomerates. Below is a structured overview of key participants:

Texas Instruments Inc.: Texas Instruments Inc. is one of the broadest-portfolio power management IC suppliers globally, offering an extensive catalog of multichannel regulators, controllers, and PMICs spanning automotive, industrial, and consumer segments. The company leverages its proprietary 300mm analog fabrication facilities in Texas and Maine to achieve cost-advantaged manufacturing at scale.

Dialog Semiconductor Plc.: Dialog Semiconductor Plc. has historically been a dominant supplier of highly integrated PMICs to Tier-1 smartphone OEMs, including Apple. Following its acquisition by Renesas Electronics Corp., Dialog's power management product lines have been integrated into a broader mixed-signal portfolio targeting IoT, automotive, and mobile applications.

Linear Technology Corporation: Linear Technology Corporation, now operating as part of Analog Devices, Inc. after a landmark acquisition, contributed advanced multichannel buck-boost and bidirectional converter IP to the combined entity's power management portfolio. Its LTC product family remains a benchmark for high-performance, high-reliability power management in industrial and communications infrastructure.

Integrated Products, Inc.: Integrated Products, Inc. focuses on cost-optimized, high-integration power management solutions targeting mid-tier consumer electronics and industrial control markets, competing primarily on integration density and price-to-performance ratios.

STMicroelectronics N.V.: STMicroelectronics N.V. brings a strong automotive and industrial power management heritage, with multichannel IC offerings certified to stringent automotive functional safety standards (ISO 26262). The company has invested heavily in SiC and GaN power device integration, positioning its digital power management portfolio for next-generation EV and renewable energy applications.

NXP Semiconductors: NXP Semiconductors is a leading supplier of automotive-grade multichannel power management solutions, with a product portfolio closely aligned with ADAS, vehicle electrification, and in-vehicle networking requirements. NXP's acquisition of Freescale Semiconductor significantly expanded its power management IP base.

Analog Devices, Inc.: Analog Devices, Inc. (inclusive of the Linear Technology acquisition) holds one of the deepest portfolios in high-accuracy, low-noise multichannel power management for precision instrumentation, communications, and defense applications. The company's Power by Linear and PowerPath product families address demanding load transient and sequencing requirements.

On Semiconductor Corporation: On Semiconductor Corporation (rebranded as onsemi) has strategically repositioned around intelligent power management for automotive, industrial, and 5G infrastructure markets, divesting non-core businesses to concentrate resources on high-growth power efficiency segments.

Qualcomm, Inc.: Qualcomm, Inc. develops proprietary multichannel PMICs co-engineered with its Snapdragon application processor platforms, maintaining tight vertical integration advantages in the premium Android smartphone ecosystem.

Renesas Electronics Corp.: Renesas Electronics Corp. has significantly expanded its power management IC portfolio through strategic acquisitions, including Dialog Semiconductor and Intersil, positioning itself as a comprehensive provider of multichannel digital power solutions for automotive, industrial, and IoT markets.

January 2024: Texas Instruments Inc. launched a new family of automotive-grade multichannel power management ICs compliant with ISO 26262 ASIL-D functional safety requirements, targeting ADAS domain controllers and zone ECU architectures in next-generation electric vehicles.

March 2024: Analog Devices, Inc. announced an expanded collaboration with a leading hyperscale data center operator to co-develop 48V-to-point-of-load digital power management solutions optimized for AI accelerator rack power delivery architectures, targeting sub-1% voltage regulation accuracy under high transient load conditions.

May 2024: STMicroelectronics N.V. unveiled a new generation of multichannel GaN-integrated digital power controllers, marking a significant step toward monolithic integration of GaN switching stages with digital control logic for telecom rectifier and EV on-board charger applications.

July 2024: NXP Semiconductors received AEC-Q100 Grade 0 qualification for its latest multichannel automotive PMIC family, enabling deployment in under-hood automotive environments with operating temperatures up to 150°C.

September 2024: Renesas Electronics Corp. completed the integration of Dialog Semiconductor's PMIC portfolio into its unified power management product line, releasing a consolidated selection guide covering over 400 multichannel power management IC variants across automotive, industrial, and consumer segments.

November 2024: On Semiconductor Corporation announced a strategic supply agreement with a major North American EV manufacturer to supply multichannel intelligent power management modules for battery management system applications across a new EV platform launching in 2026.

February 2025: Qualcomm, Inc. disclosed design details of its next-generation integrated PMIC co-packaged with the Snapdragon 8 Elite Gen 2 platform, featuring eight independently programmable power domains with AI-driven load anticipation algorithms.

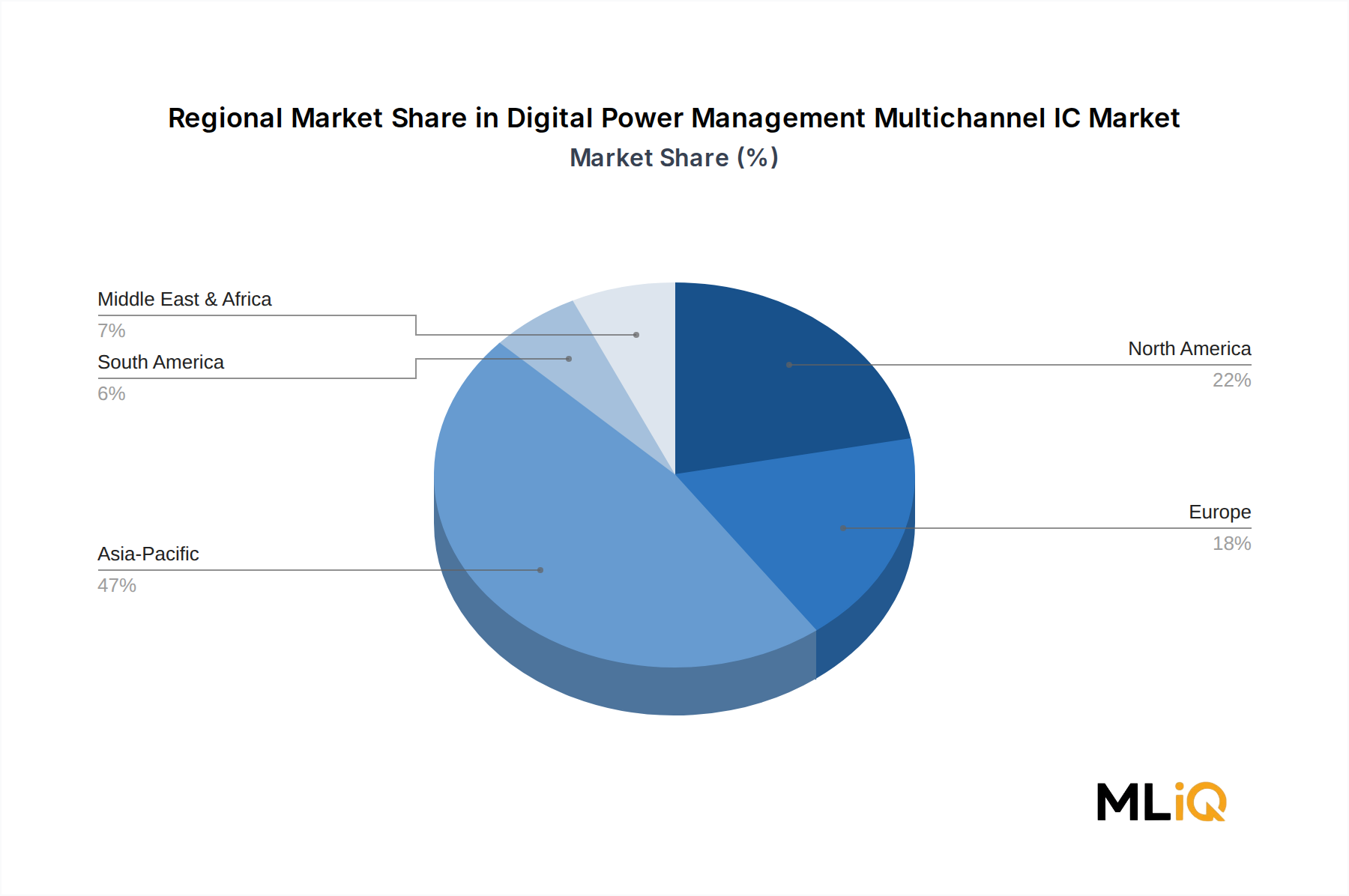

The Digital Power Management Multichannel IC Market exhibits pronounced regional heterogeneity, with Asia Pacific, North America, Europe, and the Middle East & Africa each contributing distinctly differentiated growth profiles.

Asia Pacific dominates the global market in both revenue share and volume, accounting for an estimated 48–52% of total global revenues in the base year. China, Japan, South Korea, and ASEAN nations collectively house the world's highest concentration of consumer electronics manufacturing capacity, semiconductor assembly and test operations, and EV production facilities. China alone represents the world's largest consumer electronics assembly market and the largest EV market by annual unit volume, making it the single most critical demand geography for multichannel power management IC suppliers. Asia Pacific is also the fastest-growing region, with a regional CAGR estimated at 17.8–18.5%, driven by continued electronics manufacturing expansion, domestic 5G network densification, and the Chinese government's aggressive semiconductor self-sufficiency policies under initiatives like the "Made in China 2025" and subsequent industrial strategy updates.

North America represents the second-largest regional market by revenue, underpinned by strong demand from data center and cloud infrastructure operators, defense electronics programs, and the rapidly expanding domestic EV supply chain stimulated by the Inflation Reduction Act. The United States hosts the headquarters of several leading multichannel power management IC vendors, including Texas Instruments Inc., Analog Devices, Inc., and Qualcomm, Inc., creating a dense innovation ecosystem. North America's regional CAGR is estimated at 14.5–15.5%, slightly below the global average, reflecting a more mature foundational market structure.

Europe is a strategically important market driven by automotive OEM demand, industrial automation, and renewable energy infrastructure. Germany, France, and the Nordics are particularly active demand centers, with European automotive OEMs investing heavily in EV platform development. STMicroelectronics N.V. and NXP Semiconductors serve as regionally anchored strategic suppliers. Europe's regional CAGR is estimated at 13.8–14.8%, with the EU Chips Act expected to progressively stimulate domestic semiconductor production capacity through 2030.

The Middle East & Africa region, while currently representing a smaller absolute revenue share, exhibits emerging growth potential linked to 5G network rollout investments by GCC-region telecom operators and expanding renewable energy project pipelines in North Africa and South Africa. The region's CAGR is estimated at 12.5–13.5%, with growth primarily concentrated in Turkey, GCC nations

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.3% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Digital Power Management Multichannel IC Market market expansion.

Key companies in the market include Texas Instruments Inc., Dialog Semiconductor Plc., Linear Technology Corporation, Integrated Products, Inc., STMicroelectronics N.V., NXP Semiconductors, Analog Devices, Inc., On Semiconductor Corporation, Qualcomm, Inc., Renesas Electronics Corp..

The market segments include Product Type, Application.

The market size is estimated to be USD 55227.78 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3217, USD 4999, and USD 9373 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Digital Power Management Multichannel IC Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Digital Power Management Multichannel IC Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.