1. What are the major growth drivers for the Intelligent Industrial Arm Market market?

Factors such as are projected to boost the Intelligent Industrial Arm Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

Intelligent Industrial Arm Market

Intelligent Industrial Arm Market+1 2315155523

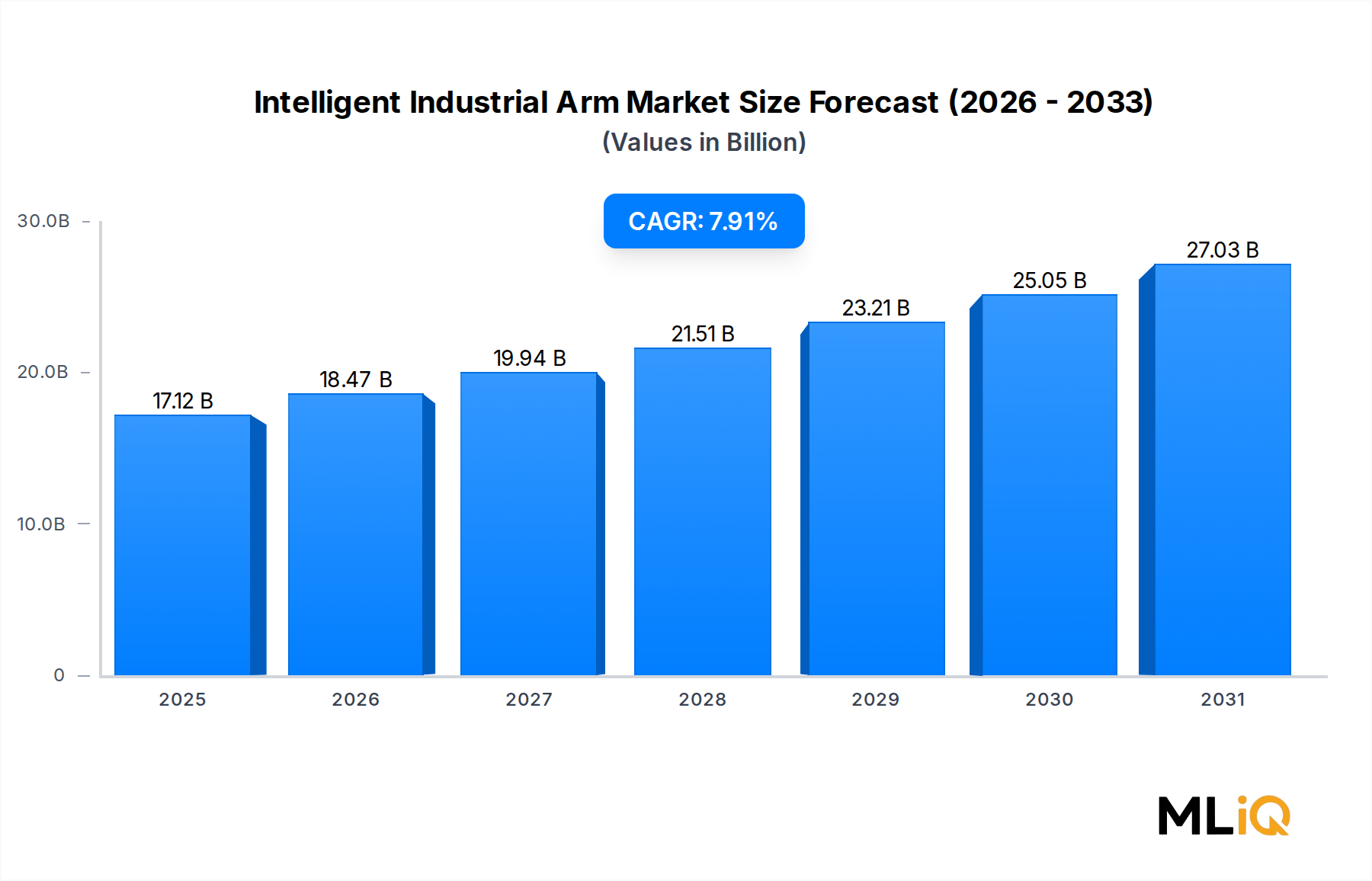

The global Intelligent Industrial Arm Market is valued at $17.12 billion in 2025 and is forecast to expand at a compound annual growth rate of 7.91% through 2033, driven by accelerating automation adoption across discrete and process manufacturing sectors. This robust trajectory reflects a confluence of macro forces: persistent labor shortages in developed economies, the reshoring of advanced manufacturing to North America and Europe, and the rapid integration of artificial intelligence, machine learning, and real-time sensor fusion into robotic control architectures.

At its core, the market addresses the industrial need for precision, repeatability, and throughput that human operators cannot consistently deliver at scale. Intelligent industrial arms — encompassing articulated, Cartesian, SCARA, and cylindrical configurations — are no longer confined to high-volume automotive assembly lines. They are penetrating electronics fabrication, pharmaceutical packaging, food processing, and logistics sortation, broadening the addressable base considerably.

Several macro tailwinds reinforce the growth case. First, global capital expenditure on smart factory infrastructure is rising as manufacturers respond to supply chain vulnerabilities exposed by the COVID-19 pandemic and geopolitical disruptions. Second, falling hardware costs, particularly for vision systems, force-torque sensors, and embedded AI accelerators, are reducing the total cost of ownership and shortening payback periods to under three years for many deployments. Third, government initiatives — including the U.S. CHIPS and Science Act, Germany's Industrie 4.0 framework, and China's Made in China 2025 successor policies — are directing capital toward automated production capacity.

On the demand side, the electrical and electronics end-use segment is emerging as a high-growth vertical, driven by the need for sub-millimeter precision in semiconductor assembly and printed circuit board handling. Simultaneously, the automotive sector continues to represent the largest installed base, with ongoing retooling cycles tied to electric vehicle platform transitions.

Looking forward, the market is expected to benefit from the proliferation of edge computing architectures that allow intelligent arms to process vision and force feedback data locally, reducing latency and enabling deployment in environments where cloud connectivity is unreliable. The integration of digital twin technology for virtual commissioning and predictive maintenance is also compressing deployment timelines, making intelligent arms accessible to mid-market manufacturers that previously lacked the engineering resources for complex robotic integration projects. By 2033, the market is projected to approximately double its 2025 valuation, underscoring the structural, not cyclical, nature of demand.

Among all configuration types, articulated robots constitute the single largest revenue-generating segment within the Intelligent Industrial Arm Market, commanding an estimated share exceeding 55% of total market revenue in 2025. This dominance is structural and self-reinforcing, rooted in the mechanical versatility, payload range, and reach envelope that articulated designs offer relative to their Cartesian, SCARA, and cylindrical counterparts.

Articulated arms replicate the degrees of freedom of the human arm — typically six rotational axes — enabling them to access workpieces from virtually any angle and perform complex, multi-step operations within a compact floor footprint. This geometric flexibility is irreplaceable in applications such as arc welding on automotive body structures, spray painting of complex curved surfaces, assembly of consumer electronics, and palletizing of irregularly shaped goods. The breadth of compatible applications ensures that articulated designs appear across nearly every end-use vertical covered in the market segmentation, from metal machinery and automotive to plastics, chemicals, and electrical electronics.

The payload spectrum further explains segment leadership. Articulated robots are commercially available across a payload range spanning less than 1 kg for micro-assembly tasks to more than 1,000 kg for heavy foundry and press-tending operations, providing a single architectural platform that scales with customer requirements. This scalability reduces the engineering overhead for manufacturers operating multiple production lines, as control software, programming interfaces, and peripheral tooling can often be standardized across payload classes.

Key players within this segment include FANUC Corporation, which has built one of the world's largest installed bases of articulated arms and continues to invest in AI-driven zero-downtime diagnostics; ABB, whose GoFa and YuMi collaborative articulated arms are expanding the segment into human-robot co-working environments; KUKA AG, which leverages its iiwa lightweight robot platform for sensitive assembly in automotive and medical device manufacturing; and Yaskawa Electric Corporation, whose Motoman series remains a benchmark for welding and handling applications. Kawasaki Heavy Industries and Mitsubishi Electric Corporation are also significant contributors, particularly in Asia-Pacific markets where demand for high-speed electronics assembly is concentrated.

The segment's share is not merely holding — it is consolidating. Three dynamics are accelerating further share gain. First, the commoditization of six-axis kinematics is driving down unit prices, making articulated arms competitive against fixed automation in lower-volume production environments. Second, advances in force-torque control and compliance algorithms are enabling articulated arms to perform tasks previously reserved for SCARA robots, such as peg-in-hole assembly, narrowing the technical gap that historically favored specialized configurations. Third, the rapid growth of collaborative robot variants built on articulated architectures is opening entirely new deployment contexts — small batch production, laboratory automation, and retail order fulfillment — that were previously inaccessible due to safety fencing requirements.

Cartesian robots retain relevance in gantry-style pick-and-place and CNC machine tending, while SCARA robots maintain a position in high-speed horizontal assembly and packaging. However, neither configuration can match the geometric versatility of articulated designs, ensuring that the dominant segment retains its leadership position through the forecast horizon of 2033.

The Intelligent Industrial Arm Market is propelled by a set of quantifiable drivers while simultaneously navigating a distinct set of structural constraints that modulate the pace and distribution of growth.

Driver 1 — Labor Cost Arbitrage Erosion: Average manufacturing wages in China rose by more than 300% between 2005 and 2023 in nominal terms, substantially eroding the labor cost advantage that historically deterred automation investment in Asia. As wage differentials narrow globally, the economic case for robotic arms strengthens across all geographies, not just high-wage Western markets.

Driver 2 — EV Retooling Cycles: The global transition to electric vehicle manufacturing is triggering the largest retooling of automotive production facilities since the introduction of mass production. EV platforms require different body joining techniques, battery module assembly, and power electronics integration, all of which demand new robotic arm installations. Automotive remains the largest end-use vertical, and this structural retooling cycle is expected to sustain elevated capital expenditure on intelligent arms through at least 2030.

Driver 3 — AI and Vision System Cost Reduction: The cost of machine vision components used in robotic guidance has declined at a rate of approximately 15–20% per annum over the past five years, driven by volume production of CMOS imaging sensors and the availability of open-source deep learning frameworks. This cost reduction directly improves the return on investment for intelligent arm deployments in quality inspection and adaptive assembly tasks.

Constraint 1 — Skilled Integration Labor Shortage: Despite falling hardware costs, the availability of robotics systems integrators and programmers remains a binding constraint. Industry surveys consistently identify the shortage of qualified integration engineers as the primary barrier cited by small and medium-sized enterprises considering their first robotic deployment.

Constraint 2 — Supply Chain Concentration for Critical Components: Key subcomponents — precision harmonic drive reducers, high-resolution encoders, and specialized servo amplifiers — are produced by a limited number of suppliers concentrated in Japan and Germany. This geographic concentration creates supply risk, as evidenced by delivery lead time extensions observed during 2021–2022.

Constraint 3 — Cybersecurity and Connectivity Risks: As intelligent arms are networked into industrial IoT ecosystems, they become potential attack vectors. Regulatory pressure for cybersecurity certification adds compliance costs and extends product development cycles.

The competitive landscape is characterized by a tier of deeply established global incumbents with broad portfolios and significant installed base advantages, alongside a growing cohort of specialist and collaborative robot vendors:

ABB: A Swiss-Swedish multinational with one of the broadest intelligent arm portfolios spanning collaborative, industrial, and paint robots. ABB's RobotStudio digital twin platform is a key differentiator for virtual commissioning, and the company has made significant investments in AI-based motion planning software.

Yaskawa Electric Corporation: A Japanese leader in servo technology and motion control, Yaskawa's Motoman robot series covers a payload range from 0.5 kg to 620 kg. The company's integrated approach — combining servo drives, controllers, and arms under one platform — reduces integration complexity for customers.

KUKA AG: A German robotics and automation company acquired by Midea Group, KUKA focuses on automotive and general industry applications. Its iiwa collaborative arm is widely deployed in assembly tasks requiring precise force control, and KUKA's software stack supports mobile robotic integration.

Universal Robotics: A pioneer in the collaborative robot sub-segment, Universal Robotics offers a portfolio of lightweight, safety-rated arms that do not require external safety fencing in most operating conditions. Their ease-of-programming model appeals strongly to SME customers.

FANUC Corporation: A Japanese automation powerhouse with one of the largest global installed bases of industrial robots and CNC systems. FANUC's zero-downtime philosophy, underpinned by its FIELD system IoT platform, is a key competitive advantage in high-uptime manufacturing environments.

NACHI-FUJIKOSHI CORP: A Japanese manufacturer offering intelligent arms with integrated servo controllers and end effectors. NACHI is particularly strong in automotive body welding and handling applications across Asia-Pacific markets.

Kawasaki Heavy Industries: A diversified Japanese industrial conglomerate whose Robotics Division produces articulated arms for welding, painting, and general handling. Kawasaki has been expanding its collaborative robot offerings to address growing demand in small-batch production.

DENSO: A Japanese automotive component manufacturer whose Robotics Division produces compact, high-speed SCARA and articulated arms used extensively in electronics assembly and automotive parts production. DENSO's arms benefit from tight integration with its automotive supply chain expertise.

Mitsubishi Electric Corporation: A major Japanese conglomerate with a robotics portfolio spanning SCARA, articulated, and parallel link robots. Mitsubishi Electric integrates its arms with its MELSEC PLC and MELFA series controllers, creating a closed-loop factory automation ecosystem.

Rockwell Automation: A U.S.-based industrial automation leader that positions itself as a system integrator and software provider for robotic deployments. Rockwell's FactoryTalk software suite provides the supervisory layer connecting intelligent arms to enterprise manufacturing execution systems.

January 2024: ABB launched the IRB 1300 articulated robot series featuring an integrated torque sensing architecture, enabling direct force-feedback assembly without external sensor hardware, targeting the consumer electronics and medical device assembly verticals.

March 2024: FANUC Corporation announced a strategic partnership with NVIDIA to integrate NVIDIA Isaac robotics simulation and AI training tools directly into the FANUC FIELD system platform, accelerating AI-driven motion planning capabilities for deployed arms.

May 2024: KUKA AG opened a new automated manufacturing facility in Augsburg, Germany, dedicated to producing next-generation collaborative arm components, with an annual output capacity increase of 30% relative to the previous facility.

July 2024: Yaskawa Electric Corporation introduced the Motoman HC30PL collaborative arm with a 30 kg payload rating — the highest in its collaborative series — addressing material handling tasks in logistics and automotive parts feeding that previously required industrial-class arms with full safety fencing.

September 2024: Universal Robotics completed a Series C funding round, securing capital earmarked for expansion of its distributor network in Southeast Asia and development of AI-native programming interfaces designed to reduce first-deployment time to under four hours.

November 2024: Mitsubishi Electric Corporation released firmware updates enabling real-time digital twin synchronization for its MELFA FR series arms, allowing live operational state mirroring in a virtual environment for predictive maintenance and offline program optimization.

February 2025: Rockwell Automation announced an expanded integration agreement with a leading MES vendor to enable seamless task-level orchestration between intelligent arm controllers and production scheduling systems, reducing changeover times by an estimated 18% in pilot deployments.

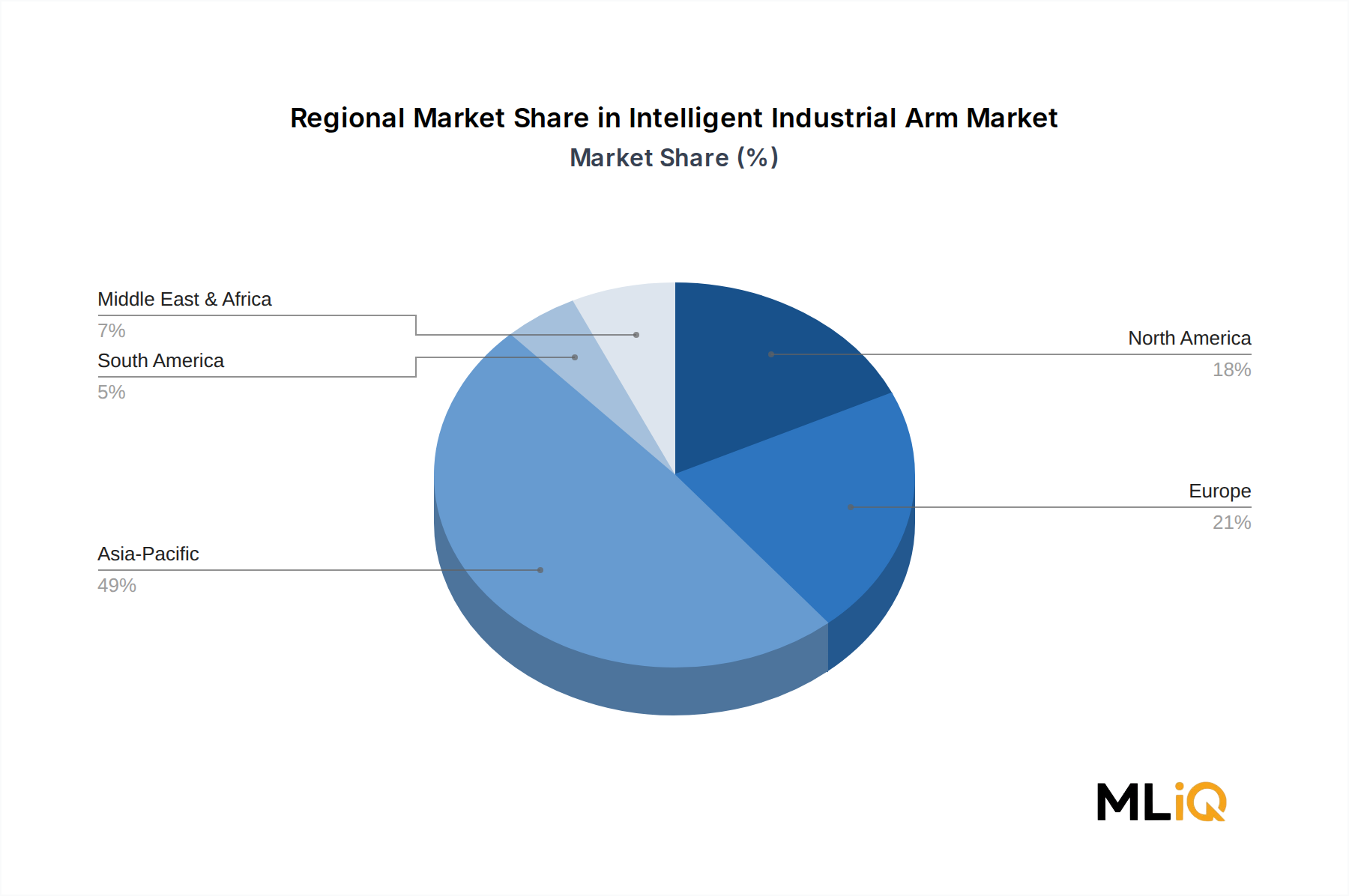

The geographic distribution of the Intelligent Industrial Arm Market reflects the uneven distribution of advanced manufacturing capacity, government automation incentives, and labor market conditions across global regions.

Asia Pacific is the dominant region, accounting for an estimated 47% of global market revenue in 2025, and is simultaneously the fastest-growing region, with a projected regional CAGR of approximately 9.2% through 2033. China is the single largest national market, driven by the government's continued push for domestic robotics capability under its industrial policy frameworks, combined with massive electronics and EV manufacturing capacity. Japan and South Korea contribute significant revenue through their concentrated automotive and semiconductor manufacturing industries. India is an emerging growth pocket as domestic electronics manufacturing scales under the Production-Linked Incentive scheme.

North America represents approximately 22% of global revenue in 2025, with the United States as the primary demand center. The reshoring of semiconductor fabrication and EV battery manufacturing — catalyzed by the CHIPS and Science Act and Inflation Reduction Act — is generating a multi-year wave of greenfield factory construction that requires dense robotic arm deployment. Canada and Mexico contribute through their automotive manufacturing clusters integrated into North American supply chains. The regional CAGR is estimated at 7.5%.

Europe accounts for roughly 21% of global revenue, with Germany, France, Italy, and the United Kingdom as the largest national markets. Germany's Industrie 4.0 framework has driven deep penetration of intelligent arms in precision manufacturing and automotive sectors. European regulatory pressure on worker safety and ergonomics is accelerating arm adoption for heavy material handling tasks. The regional CAGR is estimated at 6.8%, reflecting a more mature installed base relative to Asia Pacific.

Middle East & Africa and South America collectively represent approximately 10% of global revenue in 2025. South America, led by Brazil and Argentina, is driven by automotive assembly and agribusiness automation. The Middle East is experiencing nascent demand growth linked to Vision 2030 industrial diversification initiatives in Saudi Arabia and the UAE. Both regions are expected to grow at rates above the global average over the medium term as manufacturing base development progresses, with combined regional CAGR estimated at 8.3%.

The customer base for the Intelligent Industrial Arm Market is stratified into three broad tiers that differ significantly in purchasing criteria, procurement channels, and price sensitivity.

Tier 1 consists of large-scale automotive and electronics original equipment manufacturers (OEMs). These buyers — including global automotive assemblers and major electronics contract manufacturers — typically operate centralized procurement functions that evaluate robotic arm vendors on total cost of ownership over a 10–15 year asset life, global service network breadth, compatibility with existing factory automation ecosystems, and the availability of application engineering support. Price sensitivity at the unit level is relatively low; instead, lifecycle cost modeling, uptime guarantees, and software integration capabilities dominate vendor selection criteria. Procurement is often managed through long-term framework agreements with direct engagement from the robotic arm manufacturer's enterprise sales teams.

Tier 2 encompasses mid-market manufacturers in sectors such as plastics, chemicals, food and beverage, and general metal fabrication. These buyers are more price-sensitive and typically rely on third-party systems integrators to specify, program, and commission robotic arm installations. The buying cycle is longer due to limited in-house automation expertise, and the availability of a trusted local integrator often influences OEM brand selection more than direct manufacturer capabilities. Lease and robotics-as-a-service financing models are gaining traction in this tier, reducing upfront capital commitment.

Tier 3 consists of small and medium-sized enterprises (SMEs) representing the fastest-growing buyer cohort by unit volume, though not by revenue. These buyers are highly sensitive to ease of programming, rapid deployment time, and low total installation cost. The rise of the Collaborative Robot Market has been largely propelled by this

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.91% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Intelligent Industrial Arm Market market expansion.

Key companies in the market include ABB, Yaskawa Electric Corporation, KUKA AG, Universal Robotics, FANUC Corporation, NACHI-FUJIKOSHI CORP, Kawasaki Heavy Industries., Ltd, DENSO, Mitsubishi Electric Corporation, Rockwell Automation.

The market segments include Type, Application, End User.

The market size is estimated to be USD 17.12 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Intelligent Industrial Arm Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Intelligent Industrial Arm Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.