1. What are the major growth drivers for the Smart Light Fixture and Control Market market?

Factors such as are projected to boost the Smart Light Fixture and Control Market market expansion.

+1 2315155523

Smart Light Fixture and Control Market

Smart Light Fixture and Control Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

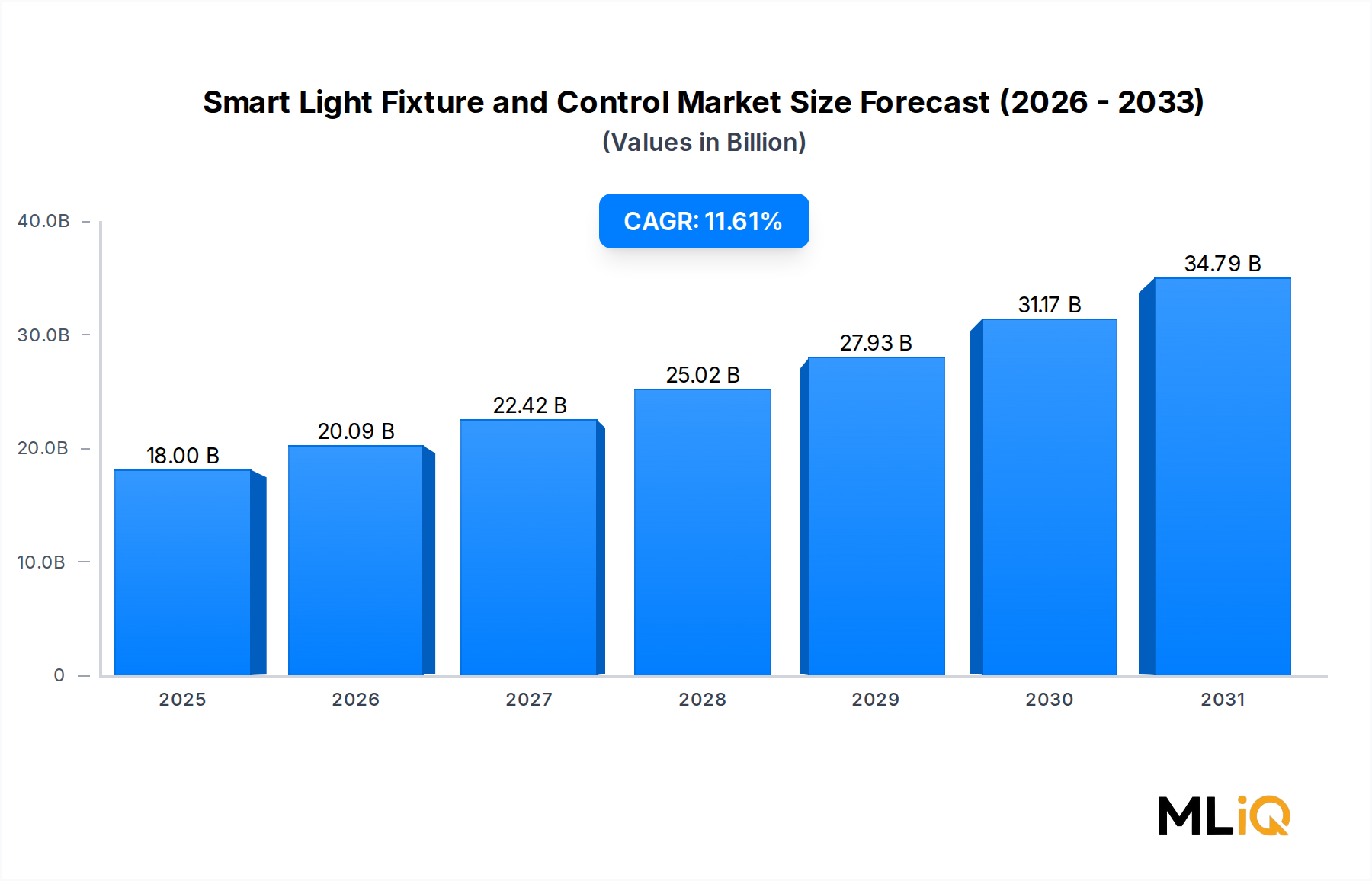

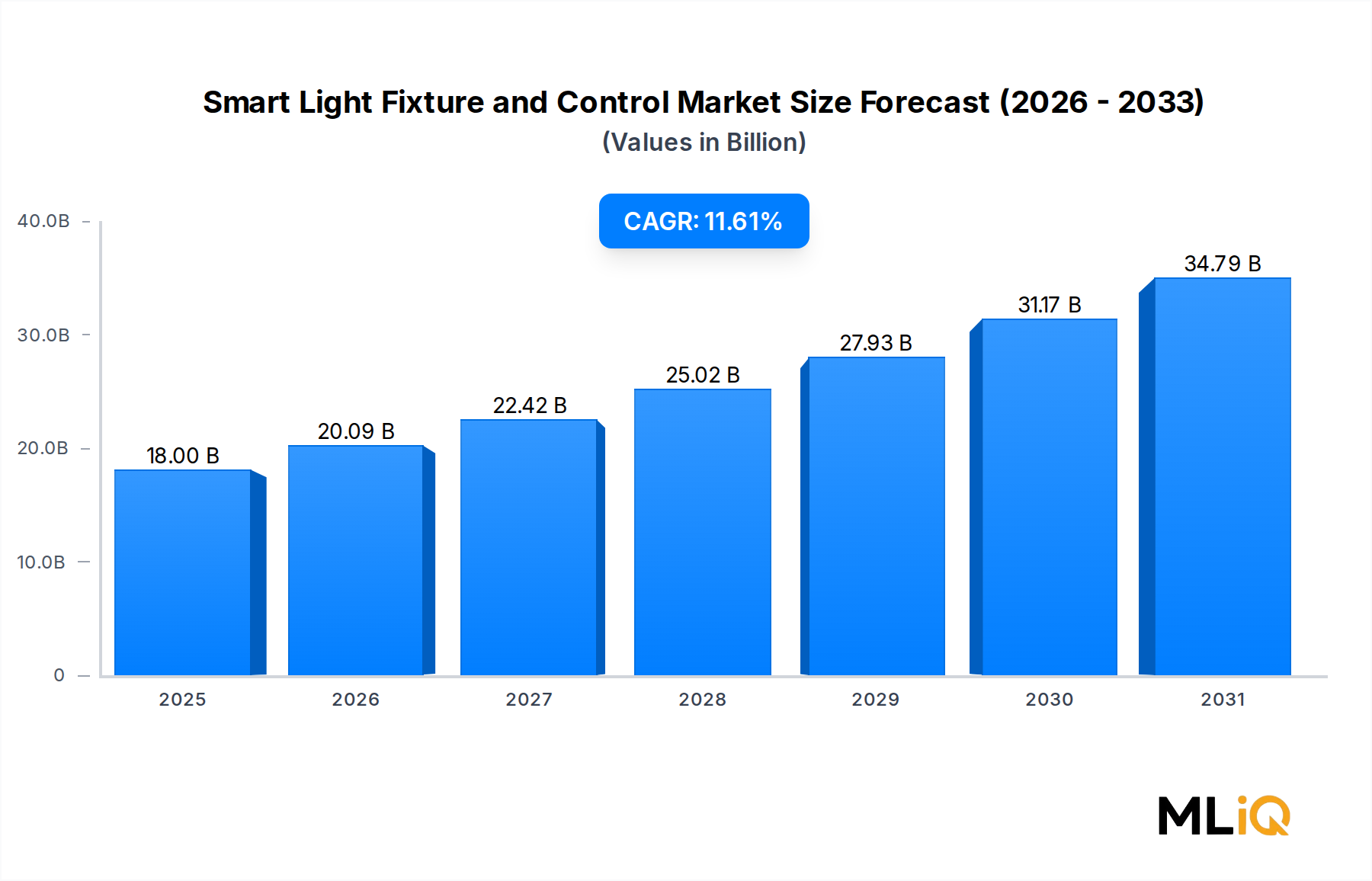

The global Smart Light Fixture and Control Market is valued at $18 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 11.61% through 2033, reflecting one of the most robust growth trajectories observed across the broader Semiconductor and Electronics category. This acceleration is underpinned by the convergence of energy efficiency mandates, rapid urbanization, and the proliferation of Internet of Things (IoT) infrastructure across residential, commercial, and industrial verticals.

Several macro tailwinds are shaping the market's outlook. First, global electricity prices have risen significantly, compelling facility managers and homeowners alike to adopt intelligent lighting systems that optimize energy consumption in real time. Second, net-zero carbon commitments by governments spanning the European Union, the United States, China, and India are translating into binding codes that favor smart, connected luminaires over conventional alternatives. Third, the increasing penetration of 5G networks and low-power wide-area network (LPWAN) technologies is removing connectivity barriers that previously constrained the scalability of smart lighting deployments.

On the demand side, the commercial sector — encompassing offices, retail environments, healthcare facilities, and educational institutions — accounts for a dominant revenue share, driven by the dual imperative of occupant comfort and operational cost reduction. Simultaneously, smart city initiatives across Asia Pacific and the Middle East are injecting significant public-sector capital into outdoor street lighting upgrades, adding another layer of structural demand.

From a product standpoint, hardware — including smart luminaires, sensors, drivers, and gateways — continues to represent the largest revenue pool, though software and services are growing at a faster clip as managed lighting-as-a-service (LaaS) models gain traction among enterprise clients seeking predictable opex structures.

Looking forward to 2033, the market is expected to be fundamentally reshaped by advances in human-centric lighting (HCL), edge-AI integration within fixtures, and the maturation of digital twin platforms that allow facility operators to model and simulate lighting environments before physical deployment. The intersection of the Smart Light Fixture and Control Market with adjacent ecosystems — including the LED Lighting Market, the Smart Building Market, and the Lighting Control System Market — will create compounding network effects that further expand addressable opportunities. Investors and OEMs positioning early in software-defined lighting architectures and open-protocol ecosystems are expected to capture outsized returns over the forecast horizon.

Among the offering segments — Hardware, Software, and Services — hardware commands the largest revenue share within the Smart Light Fixture and Control Market in 2025, accounting for an estimated 62–65% of total market value. This dominance stems from the capital-intensive nature of luminaire replacement cycles, the high average selling price of smart fixtures relative to conventional alternatives, and the foundational role that physical devices play in any connected lighting deployment.

Smart hardware encompasses a broad ecosystem of components: LED-integrated smart luminaires, dimming drivers, occupancy and daylight sensors, wireless communication modules, and edge-computing gateways embedded within fixture housings. The growing complexity of these assemblies — driven by the integration of Bluetooth mesh, Zigbee, DALI-2, and Wi-Fi 6 radios alongside onboard microcontrollers — has kept average selling prices elevated even as unit costs for individual components decline.

Within the hardware sub-segment, LED-based smart luminaires are the dominant product category, a trajectory closely tied to the broader LED Lighting Market which has itself undergone dramatic cost reduction over the past decade. The shift from fluorescent and HID sources to solid-state LED platforms created the foundational substrate upon which smart controls could be economically integrated. Today, luminaire OEMs are embedding sensor arrays and wireless stacks directly into the fixture body, eliminating the need for separate add-on control modules and reducing installation labor costs.

Retrofit installations represent a particularly high-growth sub-segment within hardware, as the global installed base of commercial buildings constructed prior to 2015 presents a multi-billion-dollar opportunity for smart upgrade kits. These retrofit solutions — which include smart drivers, screw-in connected lamps, and plug-and-play wireless sensor overlays — allow building owners to achieve smart lighting functionality without full fixture replacement, dramatically lowering capex thresholds.

Key players within the hardware segment include Signify, which leverages its Philips Hue and Interact platforms to offer vertically integrated luminaire-to-cloud solutions; Acuity Brands, Inc, which competes through its Atrius IoT platform and a broad portfolio of commercial and industrial fixtures; and Zumtobel Group, which targets the premium architectural and workplace lighting segment with sensor-embedded smart luminaires. RAB Lighting has carved a strong position in the outdoor and industrial retrofit space, while Legrand S.A. integrates smart lighting hardware within its broader electrical infrastructure ecosystem.

The hardware segment's share, while still dominant, is gradually compressing as software and services grow faster. Managed LaaS contracts, which bundle hardware, software, installation, and ongoing optimization into subscription structures, are beginning to shift revenue recognition patterns. However, for the near-to-mid forecast period through 2029, hardware will remain the primary revenue driver, particularly as smart city outdoor lighting upgrades in Asia Pacific and the Middle East translate into large-scale luminaire procurement contracts.

New installation projects in greenfield commercial developments and smart campus initiatives are also sustaining hardware demand, as architects and MEP engineers increasingly specify connected lighting systems at the design stage rather than retrofitting post-construction. This trend is structurally positive for hardware revenue concentration within the Smart Light Fixture and Control Market over the 2025–2033 forecast window.

The Smart Light Fixture and Control Market is propelled by a set of quantifiable drivers that together justify its 11.61% CAGR through 2033.

Energy cost reduction is the primary commercial driver. Smart lighting systems equipped with occupancy sensors and daylight harvesting algorithms have been documented to reduce lighting energy consumption by 40–70% compared to conventional fixed-output systems. Given that lighting accounts for approximately 15–20% of total commercial building electricity consumption globally, the financial payback periods for smart lighting investments have compressed to 2–4 years in many retrofit scenarios, making the business case compelling even without regulatory mandates.

Government energy codes and building standards represent a structural accelerating force. The EU's Energy Performance of Buildings Directive (EPBD) recast, the U.S. Department of Energy's appliance standards updates, and China's Green Building Evaluation Standard GB/T 50378 all include provisions that effectively necessitate lighting control capabilities in new and substantially renovated commercial buildings. These regulations are creating a non-discretionary replacement cycle that will inject consistent demand through the forecast period.

The proliferation of smart building infrastructure is a powerful co-driver. As the Building Automation System Market scales globally, lighting control systems are increasingly integrated into unified building management platforms, raising the strategic value of connected luminaires beyond simple energy savings to include occupancy analytics, asset tracking, and indoor positioning services.

On the constraint side, cybersecurity vulnerabilities in networked lighting systems represent a material barrier to enterprise adoption. High-profile incidents involving compromised building IoT devices have made corporate IT departments cautious about onboarding new connected endpoints. This has extended procurement cycles and imposed additional compliance costs on vendors seeking to meet frameworks such as NIST SP 800-213 and the EU Cyber Resilience Act.

Interoperability fragmentation also constrains market expansion. The coexistence of multiple wireless protocols — Zigbee, Z-Wave, Bluetooth mesh, Thread, and proprietary stacks — creates integration complexity for specifiers and installers, particularly in multi-vendor building environments. Industry bodies such as the Connectivity Standards Alliance (CSA) are working to address this through the Matter protocol, but widespread adoption remains in early stages as of 2025.

High upfront hardware costs continue to deter adoption in price-sensitive segments, particularly small and medium-sized commercial establishments and residential markets in emerging economies, where smart lighting premiums over conventional alternatives can reach 3–5x the per-unit cost.

The competitive landscape of the Smart Light Fixture and Control Market is moderately consolidated at the top tier, with a mix of diversified conglomerates, specialist lighting OEMs, and technology-focused newcomers competing across hardware, software, and services dimensions.

Signify: The global leader in connected lighting, Signify operates the Philips Hue consumer platform and the Interact professional IoT lighting ecosystem, serving retail, office, industry, and smart city applications across more than 70 countries. The company's scale in LED component manufacturing and its open-API software architecture give it a defensible competitive position across multiple verticals.

Acuity Brands, Inc: A dominant force in North American commercial and industrial lighting, Acuity Brands, Inc leverages its Atrius platform to deliver data-driven lighting analytics alongside a broad portfolio of smart luminaires under the Lithonia Lighting and Holophane brands. The company's strong specification-channel relationships with architects and electrical contractors provide a durable distribution moat.

Legrand S.A.: Operating at the intersection of electrical infrastructure and smart building systems, Legrand S.A. integrates smart lighting control within its broader Eliot connected building program, targeting residential, commercial, and data center segments with a strong European base and growing presence in North America and Asia.

Honeywell International Inc.: Honeywell International Inc. competes through its building technologies division, offering integrated lighting and HVAC control solutions under unified building management platforms, with particular strength in large commercial, hospitality, and healthcare accounts.

Lutron Electronics: Renowned for its premium dimming technology and Radio RA 3 wireless platform, Lutron Electronics holds a commanding position in the high-end residential and boutique commercial segment, with a reputation for reliability and aesthetic integration that commands significant price premiums.

Leviton Manufacturing Company, Inc.: Leviton Manufacturing Company, Inc. targets the residential and light commercial smart lighting control segment through its Decora Smart platform, competing on ease of installation and broad compatibility with Amazon Alexa, Google Home, and Apple HomeKit ecosystems.

Zumtobel Group: An Austrian specialist in architectural and workplace luminaires, Zumtobel Group differentiates through its TECTON and SLOTLIGHT product families and its Limelight IoT lighting management system, serving premium office, retail, and healthcare environments across Europe.

RAB Lighting: RAB Lighting focuses on value-oriented LED and smart outdoor lighting for commercial and industrial applications, competing on price-performance ratios in the North American market with a growing line of networked area and site luminaires.

Synapse Wireless: Synapse Wireless provides wireless mesh networking technology specifically targeting smart outdoor and street lighting deployments, with a platform-agnostic approach that allows integration with multiple luminaire brands.

Ideal Industries: Ideal Industries operates in the smart lighting control accessories and wiring device space, supplying installers and contractors with components that enable smart lighting system assembly across residential and commercial projects.

Adesto Technologies: Adesto Technologies contributes semiconductor and embedded flash memory solutions that underpin the microcontroller and gateway components used in smart lighting fixtures, addressing the IoT Connectivity Market from a silicon layer perspective.

January 2025: Signify announced the expansion of its Interact Pro platform to support the Matter over Thread protocol, enabling interoperability with third-party smart home and building ecosystems and accelerating enterprise adoption across Europe and North America.

February 2025: Acuity Brands, Inc launched its next-generation nLight AIR 2.0 wireless lighting control system, featuring enhanced Bluetooth mesh range and integrated occupancy analytics, targeting large open-plan office and warehouse applications.

March 2025: The U.S. Department of Energy published updated minimum efficiency standards for commercial luminaires, effectively mandating smart-ready drivers in new installations above 10,000 lumens from 2027 onward, creating a structural upgrade cycle.

April 2025: Legrand S.A. completed the acquisition of a European smart building software startup, strengthening its Eliot platform's data analytics capabilities and expanding its presence in the facilities management software segment.

May 2025: The European Commission confirmed inclusion of smart lighting control requirements within the revised Energy Performance of Buildings Directive implementation guidelines, setting a compliance deadline of 2028 for member state building codes.

June 2025: Lutron Electronics introduced a new architectural dimming engine compatible with tunable white LED drivers, targeting the human-centric lighting segment in premium healthcare and education facilities.

August 2025: Honeywell International Inc. announced a strategic partnership with a major U.S. telecommunications provider to deliver cloud-managed smart lighting services for smart city street lighting programs across three metropolitan areas.

October 2025: Synapse Wireless secured a municipal contract for the deployment of 50,000 connected street light nodes in a Gulf Cooperation Council (GCC) smart city development, representing one of the largest single outdoor smart lighting awards of the year.

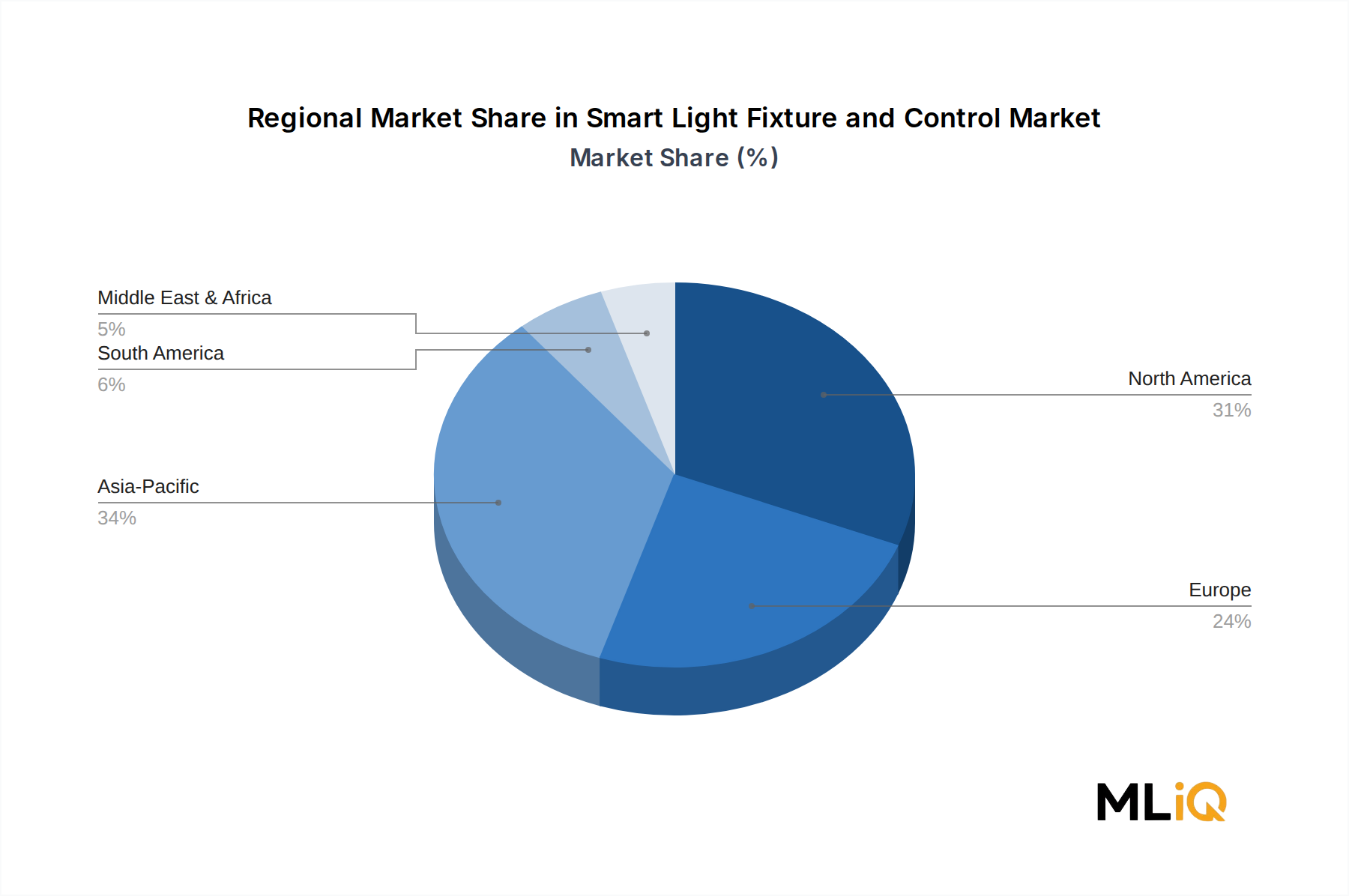

The Smart Light Fixture and Control Market exhibits distinct regional growth profiles, shaped by differing regulatory environments, infrastructure investment cycles, and levels of smart building adoption.

North America is the most mature regional market, accounting for an estimated 34–36% of global revenue in 2025. The United States drives the bulk of regional demand, supported by utility rebate programs, the DOE's Better Buildings Initiative, and extensive commercial real estate renovation activity. Canada and Mexico contribute meaningful volumes through smart city pilot programs and retail sector upgrades. The regional CAGR is projected at approximately 9.8% through 2033, reflecting a market transitioning from early adoption to mainstream replacement cycles.

Europe represents the second-largest regional market, holding approximately 28–30% of global share. Germany, the United Kingdom, France, and the Nordics are the principal revenue contributors, driven by stringent EU energy directives and corporate ESG procurement policies. The Benelux region has emerged as a testbed for human-centric lighting in office environments. European regional CAGR is estimated at 10.4%, accelerated by the EPBD recast compliance timeline and the EU Green Deal's emphasis on building decarbonization.

Asia Pacific is the fastest-growing regional market, with a CAGR projected at 13.8% through 2033. China dominates absolute volume, supported by national smart city programs under the 14th and 15th Five-Year Plans and government subsidies for LED and smart lighting adoption. India is experiencing rapid growth driven by the UJALA and Smart Cities Mission programs. Japan and South Korea contribute high-value commercial and industrial deployments. The ASEAN bloc is emerging as a significant opportunity as urban construction activity accelerates across Vietnam, Indonesia, and Thailand.

Middle East and Africa is an increasingly significant market, with GCC nations — particularly Saudi Arabia and the UAE — investing heavily in smart outdoor lighting as part of Vision 2030 and related national transformation agendas. The regional CAGR is estimated at 12.1%, supported by large-scale greenfield smart city developments including NEOM and Masdar City. South Africa and North Africa represent earlier-stage markets with growing momentum.

South America is the smallest regional market but is expanding at a CAGR of approximately 9.2%, led by Brazil's commercial real estate sector and municipal lighting upgrade programs in major urban centers including São Paulo and Bogotá.

The regulatory environment governing the Smart Light Fixture and Control Market has intensified materially across all major geographies between 2023 and 2025, establishing a compliance-driven demand floor that is structurally supportive of market growth through the forecast period.

In the United States, the Department of Energy's enforcement of updated Lamp, Luminaire, and Controls efficiency standards under the Energy Policy and Conservation Act (EPCA) has effectively eliminated non-dimmable fluorescent luminaires from new commercial installations. The DOE's ongoing rulemaking on smart-ready driver requirements — anticipated to take effect by 2027 — will mandate wireless control capability in high-lumen commercial fixtures, creating an estimated $2.1 billion addressable upgrade opportunity in the U.S. market alone.

The European Union's regulatory framework is arguably the most comprehensive globally. The revised Energy Performance of Buildings

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.61% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Smart Light Fixture and Control Market market expansion.

Key companies in the market include Zumtobel Group, RAB Lighting, Legrand S.A., Honeywell International Inc., Leviton Manufacturing Company, Inc., Ideal Industries, Acuity Brands, Inc, Synapse Wireless, Signify, Adesto Technologies, Lutron Electronics.

The market segments include Offering, Installation Type, End Use Application, Communication Technology.

The market size is estimated to be USD 18 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Smart Light Fixture and Control Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Smart Light Fixture and Control Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.