1. What are the major growth drivers for the Health Ingredients Market market?

Factors such as are projected to boost the Health Ingredients Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

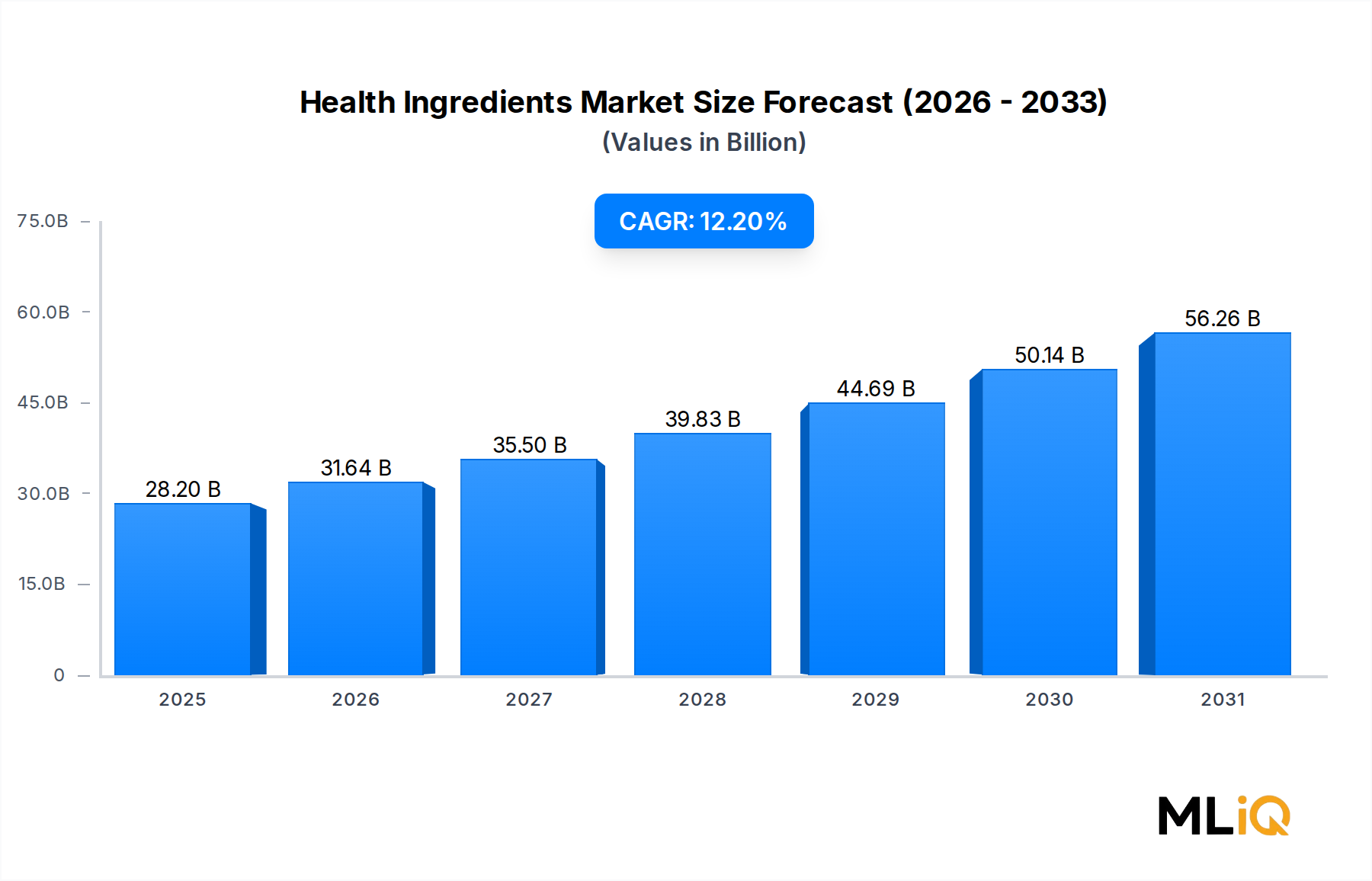

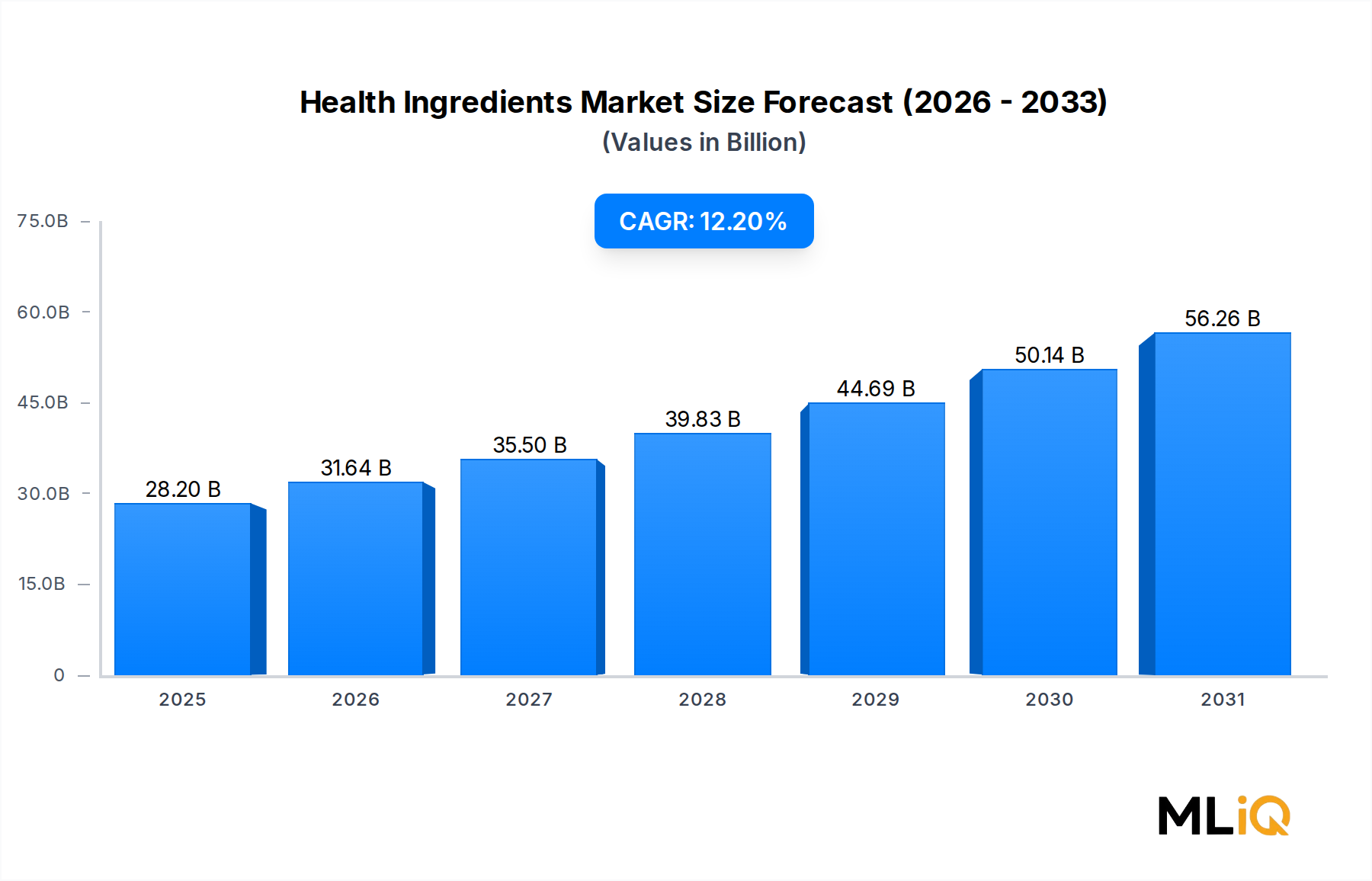

The global Health Ingredients Market was valued at $28.2 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 12.2% through 2033, reflecting accelerating consumer demand for science-backed, bioactive nutritional components integrated into everyday food, beverage, and supplement products. This robust trajectory positions the market to surpass $79 billion by the close of the forecast horizon, underpinned by structural shifts in global dietary behavior, aging demographics, and post-pandemic health consciousness.

Several macro tailwinds are converging to sustain this growth momentum. Rising prevalence of non-communicable diseases (NCDs), including obesity, type 2 diabetes, and cardiovascular disorders, is propelling consumers toward preventive nutrition strategies. According to the World Health Organization, NCDs account for approximately 74% of all global deaths annually, creating a vast addressable demand pool for functional and health-promoting ingredients. Simultaneously, urbanization and rising disposable incomes across emerging markets in Asia Pacific, Latin America, and the Middle East are unlocking new consumer segments previously underserved by premium health ingredient categories.

From a product typology perspective, proteins, prebiotics, and vitamins collectively represent the highest-revenue sub-segments, while nutritional lipids and plant fruit extracts are emerging as the fastest-growing specialty categories. The diversification of ingredient sources — spanning plant, animal, microbial, and synthetic origins — is enabling manufacturers to cater to vegan, allergen-free, and clean-label preferences simultaneously. The Nutraceutical Ingredients Market increasingly converges with the Health Ingredients Market, as bioavailability-enhanced delivery formats drive premiumization across formulations.

Application-wise, the food and beverage segment commands dominant revenue share, though pharmaceutical co-applications and personalized nutrition platforms are beginning to challenge that hierarchy. Digital health ecosystems, direct-to-consumer supplement brands, and e-commerce distribution channels have further accelerated ingredient adoption at scale.

On the supply side, strategic investments in fermentation biotechnology, precision extraction, and microencapsulation are compressing costs while improving ingredient efficacy and shelf-life stability. The competitive landscape is consolidating, with major players deploying M&A strategies to acquire novel ingredient pipelines and geographic market access. Looking ahead through 2033, innovation in postbiotics, biofortified crops, and AI-driven formulation science will define the next wave of differentiation in this high-growth market.

The protein sub-segment represents the single largest revenue contributor within the Health Ingredients Market, accounting for an estimated 22–25% of total market value as of 2024. This dominance is rooted in protein's dual functionality as both a structural macronutrient and a bioactive ingredient capable of supporting muscle synthesis, satiety signaling, immune modulation, and gut barrier integrity. The convergence of sports nutrition, clinical nutrition, and mainstream consumer wellness has created an exceptionally broad demand base that few other ingredient categories can match.

Within the protein sub-segment, plant-derived proteins — including pea, soy, rice, and hemp isolates — have emerged as the growth frontier, driven by the sustained expansion of the Plant Protein Market globally. Pea protein isolate has attracted particular commercial attention due to its complete amino acid profile relative to other legume-based sources, its allergen-free positioning compared to soy, and its compatibility with clean-label formulations. Consumer acceptance of plant proteins has normalized substantially since 2019, when alt-protein products entered mainstream retail channels, and this normalization has produced compounding volume growth through food service, snack, and ready-to-drink categories.

Animal-derived proteins — including whey concentrate, whey isolate, casein, collagen peptides, and egg albumin — retain strong footholds in sports performance and clinical nutrition segments. Whey protein, in particular, commands premium pricing due to its high biological value and rapid digestibility metrics. However, dairy commodity cycles create margin volatility for formulators dependent on whey-derived inputs, particularly in Europe and North America where raw milk pricing is sensitive to feed cost and regulatory shifts.

Microbial proteins represent a nascent but strategically significant frontier. Single-cell protein derived from yeast, fungi, and algae feedstocks is attracting significant research and commercialization investment. Companies such as Parabel USA, Inc. are pioneering duckweed-based protein platforms that promise exceptionally high protein density per cultivated hectare with minimal freshwater and land inputs — attributes that position microbial and aquatic proteins as long-term supply resilience hedges against climate-driven agricultural disruption.

Key players dominating the protein ingredient sub-segment include Cargill Incorporated, Archer Daniels Midland Company, Roquette Frères, Ingredion Corporation, and Kerry Group Plc. These firms have made substantial capital investments in protein fractionation capacity, functional texturization capabilities, and application development laboratories designed to help food and beverage manufacturers integrate high-protein claims into end products without compromising sensory attributes.

The protein segment's share is currently growing, not consolidating. Volume growth in emerging markets — particularly India, China, and Brazil — is amplifying demand from a low per-capita protein supplement baseline. Simultaneously, regulatory tailwinds such as front-of-pack nutrition labeling requirements in the European Union and protein quality scoring systems (DIAAS adoption by formulators) are increasing the technical sophistication of procurement decisions, favoring established suppliers with validated nutritional claims and traceability infrastructure. Competitive differentiation is increasingly achieved through post-processing innovations such as enzymatic hydrolysis, Maillard reaction control, and nanoencapsulation to improve solubility, flavor neutrality, and bioavailability of protein ingredients across applications.

The Health Ingredients Market is shaped by a complex interplay of demand-side catalysts and supply-side constraints that collectively define its growth trajectory through 2033.

Driver 1 — Preventive Healthcare Spending Escalation: Global out-of-pocket spending on preventive nutrition and supplementation has grown at an average of 8–9% annually since 2020, according to industry health expenditure tracking data. This spending shift reflects growing consumer awareness that diet-mediated interventions can reduce chronic disease risk, lowering long-term healthcare expenditure. This behavioral shift directly increases ingredient pull-through across vitamins, minerals, and bioactive botanical extracts.

Driver 2 — Regulatory Endorsement of Functional Claims: In the European Union, EFSA-approved health claims for specific ingredients — including omega-3 fatty acids for cardiovascular function, calcium for bone maintenance, and certain probiotic strains for digestive health — have provided a regulatory framework that legitimizes product differentiation. The expansion of permitted claims in Southeast Asian markets (notably Singapore, South Korea, and Japan) has similarly unlocked premium shelf positioning for health ingredient-enriched products.

Driver 3 — E-Commerce Distribution Democratization: Online sales channels now represent approximately 18–22% of total health ingredient-containing product sales in North America and Europe, a figure that has more than doubled since 2019. This digital shift has lowered barriers for specialty ingredient adoption by enabling small and mid-scale formulators to reach health-conscious consumer segments without requiring mass retail distribution partnerships.

Constraint 1 — Raw Material Price Volatility: Ingredients such as omega-3 fish oil, certain botanical extracts, and fermentation-derived vitamins are exposed to commodity cycles driven by climate variability, fishing quotas, and energy costs. Price swings of 15–30% within a single calendar year have been documented for marine oil feedstocks, creating formulation cost instability that compresses margins across the value chain.

Constraint 2 — Regulatory Fragmentation: Divergent regulatory frameworks across the United States (FDA DSHEA), European Union (EFSA Novel Foods Regulation), and Asia Pacific national food safety authorities create compliance complexity and market entry costs that disproportionately disadvantage smaller ingredient innovators, slowing overall market innovation velocity.

Roquette Frères: A global leader in plant-based ingredients with a particularly strong portfolio in pea protein, specialty starches, and dietary fibers; the company has invested heavily in its protein fractionation facility in Vic-sur-Aisne, France, to scale plant protein supply for food and pharmaceutical applications.

Arla Foods: Denmark-based dairy cooperative with a dominant position in whey protein ingredients and functional dairy-derived bioactives; Arla's Ingredients division develops clinically substantiated milk protein fractions targeting sports nutrition and healthy aging formulations.

BASF SE: One of the world's largest producers of vitamins, carotenoids, and omega-3 fatty acids for human and animal nutrition; BASF's Human Nutrition division integrates synthetic and biotechnology-derived ingredient production at industrial scale.

Koninklijke DSM N.V.: A science-based nutrition leader with a broad portfolio spanning vitamins, premixes, lipids, and probiotic solutions; following its strategic combination with Firmenich, DSM-Firmenich is repositioning as an integrated health and biosciences platform.

Kerry Group Plc: An Irish multinational with extensive taste and nutrition ingredient capabilities, including bioactive proteins, prebiotics, and enzyme systems; Kerry's ProDiem and Wellmune branded ingredients hold strong positions in the immune health sub-segment.

Cargill Incorporated: A vertically integrated agri-food giant with significant health ingredient capabilities in plant proteins, specialty oils, and functional carbohydrates; Cargill's texturizing and nutrition platforms serve major food manufacturers globally across multiple ingredient categories.

Lonza Group: A Swiss life sciences company with specialized capabilities in capsule technologies, probiotic manufacturing, and nutraceutical ingredient supply; Lonza's Capsugel and nutritional ingredient divisions serve both pharma-grade and consumer supplement markets.

Archer Daniels Midland Company: A major global originator and processor of agricultural commodities with a health ingredients portfolio covering soy proteins, dietary fibers, and specialty lipids; ADM's nutrition business has expanded through acquisitions including the Eatem Foods and Wild Flavors integrations.

Ingredion Corporation: Specializes in ingredient solutions derived from corn, tapioca, potato, and other plant sources, with a growing clean-label and specialty nutrition ingredient platform; Ingredion serves formulators across food, beverage, and dietary supplement categories globally.

Tate & Lyle Plc: A UK-based ingredients company focused on dietary fibers, sweetener systems, and functional food ingredients; Tate & Lyle's PROMITOR soluble corn fiber and other prebiotic fiber solutions hold established positions in the gut health ingredient segment.

Parabel USA, Inc.: An emerging innovator commercializing water lentil (duckweed)-derived protein and nutritional ingredients under the LENTEIN brand, targeting sustainable, high-protein ingredient solutions for food and beverage formulators seeking novel plant protein alternatives.

March 2025: DSM-Firmenich launched a next-generation omega-3 algal oil ingredient line under its life'sOMEGA brand, expanding sustainable, fish-free DHA and EPA supply options for functional food and infant nutrition formulators globally.

January 2025: Kerry Group announced the expansion of its probiotic manufacturing facility in Beloit, Wisconsin, adding 40,000 square feet of GMP-certified production capacity dedicated to shelf-stable probiotic ingredient formats for dietary supplement and functional food clients.

November 2024: Cargill completed the acquisition of a specialty plant protein processing company in the Netherlands, strengthening its pea and fava bean protein fractionation capacity within the European market to address growing demand in the Functional Food Market.

September 2024: Roquette Frères received GRAS (Generally Recognized as Safe) affirmation from the U.S. FDA for a novel pea protein hydrolysate ingredient targeting sports recovery and senior nutrition applications, enabling accelerated U.S. commercial rollout.

July 2024: BASF SE announced a strategic collaboration with a leading Asian pharmaceutical manufacturer to co-develop vitamin D3 and K2 combination premix solutions targeting the osteoporosis prevention segment in Japan and South Korea.

April 2024: Ingredion Corporation launched a new line of resistant starch ingredients branded VERSAFIBE, formulated to support the Dietary Supplements Market and functional food segment with clinically supported gut health and glycemic management benefits.

February 2024: Lonza Group completed the divestiture of its specialty ingredients segment, sharpening its strategic focus on biotechnology-derived nutraceutical and pharmaceutical ingredient manufacturing to improve portfolio profitability margins.

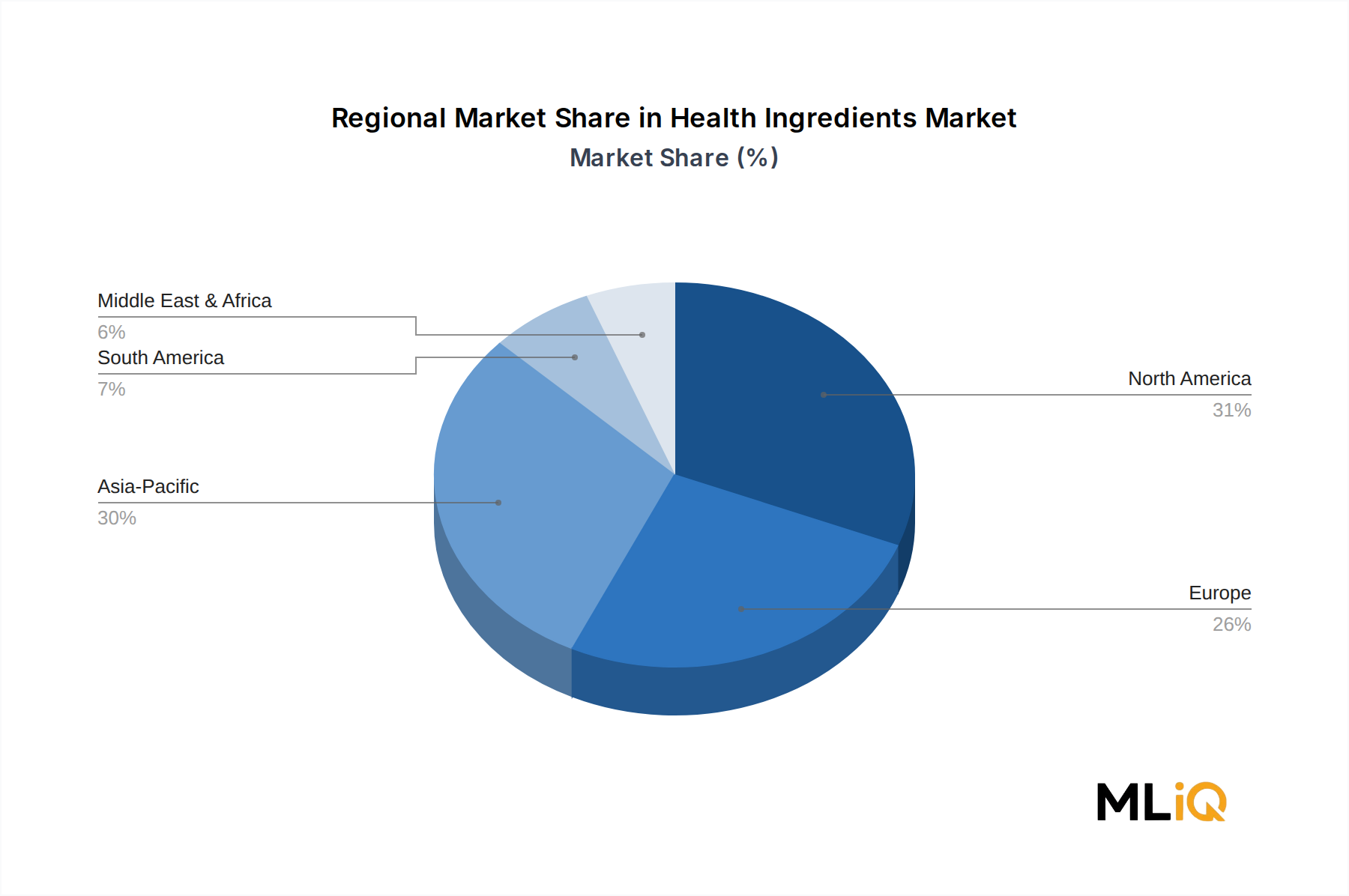

North America remains the most mature and highest-revenue region within the Health Ingredients Market, accounting for approximately 34–36% of global market value in 2024. The United States is the primary driver, supported by a deeply entrenched dietary supplement culture, a permissive regulatory environment under DSHEA, and high per-capita spending on functional foods and wellness products. The region is projected to maintain a CAGR of approximately 9.5–10.5% through 2033, with growth driven primarily by personalized nutrition technologies, the expansion of the Dietary Supplements Market, and increasing clinical nutrition adoption among aging baby boomers.

Europe represents the second-largest regional market, with Germany, the United Kingdom, France, and the Nordic countries serving as the principal consumption hubs. European demand is characterized by strong regulatory rigor under EFSA frameworks and heightened consumer preference for clean-label, organic-certified, and sustainably sourced health ingredients. The region is expected to grow at a CAGR of approximately 10.0–11.0%, with plant-based protein ingredients and probiotic cultures registering above-average expansion rates. The Food Fortification Market in Europe is also a significant demand channel, particularly for vitamins and minerals added to staple food categories.

Asia Pacific is the fastest-growing region, projected to expand at a CAGR of 14.5–16.0% through 2033, driven by rapid urbanization, rising middle-class health awareness, and government-backed nutrition intervention programs in China, India, and Indonesia. China alone accounts for over 40% of regional demand, with a particular concentration in vitamins, minerals, and traditional botanical extract ingredients. India's market is accelerating through the intersection of Ayurvedic heritage ingredients and modern nutraceutical science, creating a unique hybrid demand profile. The Animal Nutrition Market in Asia Pacific is also channeling significant health ingredient volumes, particularly enzymes and amino acids, as protein-efficient livestock production becomes a national food security priority.

Latin America and the Middle East & Africa collectively represent emerging but rapidly expanding markets. Brazil leads Latin American demand, supported by a large functional beverage sector and growing clinical nutrition infrastructure. GCC countries are experiencing above-average growth in the premium sports nutrition and weight management ingredient categories, with the Enzyme Technology Market playing an expanding role in food processing optimization across the region.

Pricing across the Health Ingredients Market is highly heterogeneous, reflecting the wide spectrum of ingredient complexity, synthesis routes, and regulatory certification requirements embedded in different product categories. At the commodity end of the spectrum, bulk vitamins (particularly vitamin C and B-complex vitamins) and standard mineral salts face intense price competition driven by large-scale Chinese and Indian manufacturer participation, with average selling prices experiencing 10–20% deflationary pressure over the 2020–2024 period due to capacity expansions and supply chain normalization post-COVID.

In contrast, specialty and patented ingredients — including specific probiotic strain cultures, clinically validated bioactive peptides, and branded omega-3 concentrates — command significant price premiums, often 3x–8x the cost of commodity-grade equivalents. These premium ingredients benefit from proprietary manufacturing know-how, clinical substantiation costs embedded in pricing, and limited competitive supply. The Probiotic Ingredients Market exemplifies this dynamic, where differentiated strains with validated health effect data sustain durable pricing power even as the overall supplement market grows more competitive.

Margin structures across the value chain reflect these polarized dynamics. Raw material extractors and primary processors operate at thinner margins (8–15% EBITDA), while ingredient manufacturers with branded, IP-protected formulations achieve significantly higher margin profiles (**20–35% EBIT

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Health Ingredients Market market expansion.

Key companies in the market include Roquette Frères, Arla Foods, BASF SE, Koninklijke DSM N.V., Kerry Group Plc, Cargill Incorporated, Lonza Group, Archer Daniels Midland Company, Ingredion Corporation, Tate & Lyle Plc, Parabel USA, Inc..

The market segments include Type, Source, Application, Distribution Channel.

The market size is estimated to be USD 28.2 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Health Ingredients Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Health Ingredients Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.