Open Marine Insurance Policy Dominance in the Marine Freight Insurance Market

Among the various policy types that constitute the Marine Freight Insurance Market, the Open Marine Insurance Policy segment commands the largest revenue share and continues to consolidate its position as the preferred coverage structure for high-frequency shippers and large-scale freight operators. This segment's dominance is rooted in its operational versatility — an open policy provides automatic, continuous coverage for all shipments made by the insured during a defined period, eliminating the need to declare each cargo movement individually. For multinational traders, commodity exporters, and third-party logistics providers managing hundreds of consignments monthly, this structure offers both administrative efficiency and cost optimization.

The structural appeal of open marine insurance is particularly pronounced among mid-to-large enterprises operating in manufacturing-intensive export economies such as China, Germany, South Korea, and the United States. These entities require seamless insurance continuity to satisfy letters of credit requirements stipulated by international banks under UCP 600 (Uniform Customs and Practice for Documentary Credits) rules. Any lapse in coverage or delay in policy issuance could trigger financial penalties, cargo holdups, or trade finance rejection — making the perpetual-coverage model of open policies commercially indispensable.

From a market share perspective, the Open Marine Insurance Policy segment benefits disproportionately from the secular growth in containerized trade. Global container port throughput exceeded 800 million TEUs annually in recent estimates, and the insurance demand tied to these movements overwhelmingly gravitates toward open and floating policy structures rather than single-voyage or time-limited plans. Floating plans — the closest competitor segment — capture a portion of the bulk commodity and specialized cargo market but lack the administrative simplicity that drives enterprise adoption of open policies.

Key players within this segment include Allianz, Zurich, Chubb, and Munich Re, all of which have developed digitally-integrated open policy platforms that allow policyholders to declare shipments, adjust insured values, and obtain endorsements via API-connected enterprise resource planning (ERP) systems. Marsh, as one of the world's leading insurance brokers, plays a pivotal role in structuring bespoke open policy frameworks for Fortune 500 clients, frequently incorporating clauses tailored to specific trade lanes, commodity types, and Incoterms arrangements.

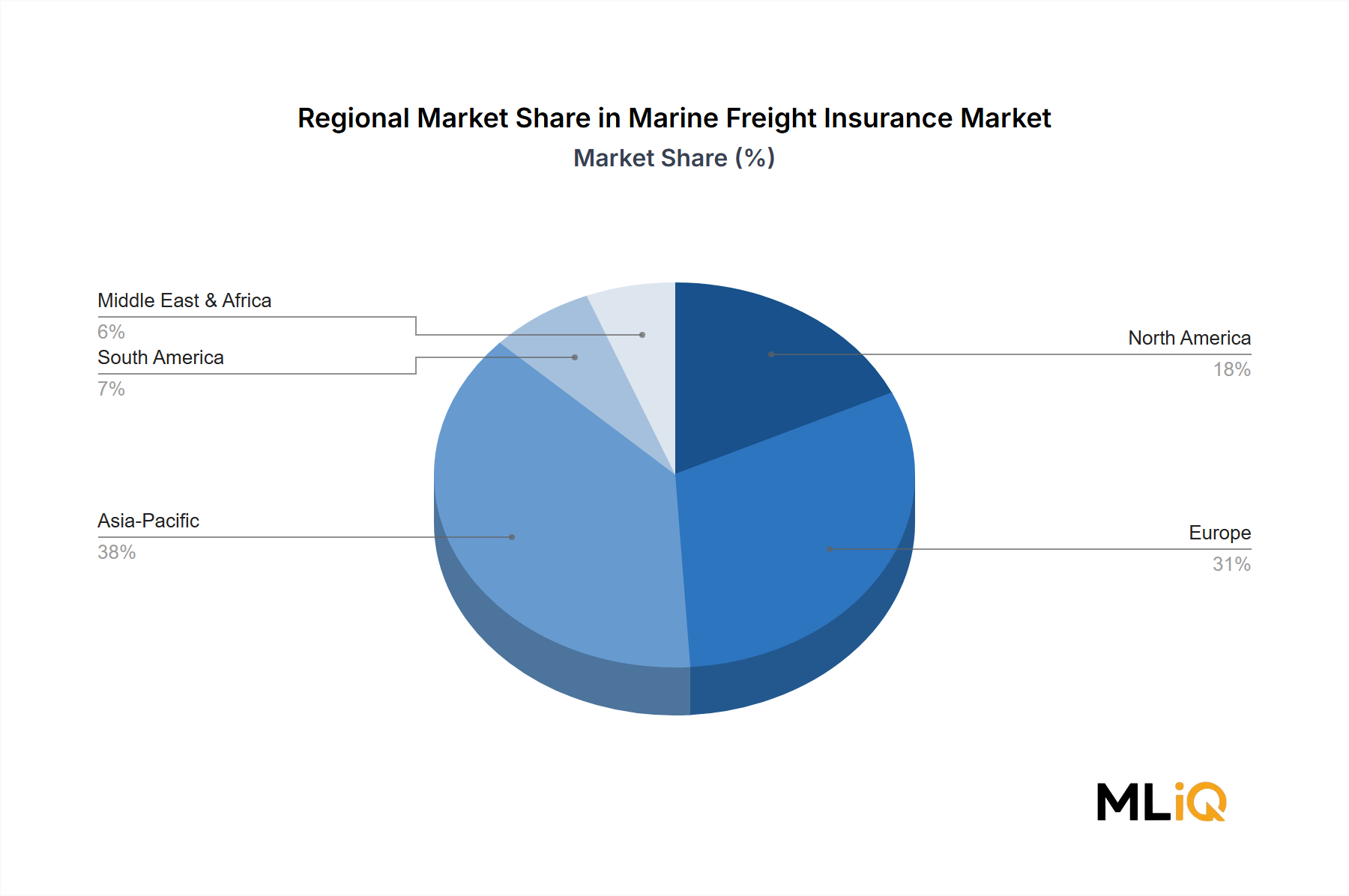

The segment's share is not merely holding steady — it is actively expanding into new geographies. In Asia Pacific, regulatory liberalization in markets such as India and Indonesia has enabled foreign insurers to offer open policy products directly to domestic exporters, previously a restricted activity. This opening has attracted players like Samsung Fire and Marine Insurance Co Ltd and Liberty Mutual Insurance, which are aggressively marketing open policy solutions to textile, electronics, and automotive parts exporters in these high-growth corridors.

Another dimension reinforcing this segment's dominance is its compatibility with parametric insurance add-ons. Parametric triggers tied to route-specific weather indices, port congestion indicators, or commodity price benchmarks are increasingly being layered onto open policy frameworks, providing additional financial protection during disruption events without requiring loss adjustment. This hybrid product innovation is attracting a new cohort of sophisticated buyers who previously self-insured, further expanding the addressable market for open marine insurance policies.

The pricing environment for open policies remains competitive but disciplined. Underwriters have implemented rate corrections following consecutive years of elevated claims from container fires (notably the X-Press Pearl incident), vessel allisions, and weather-related cargo damage. These corrections, while modest, have improved underwriting profitability and incentivized capacity providers to maintain or expand their open policy books, ensuring adequate market supply even as demand rises.