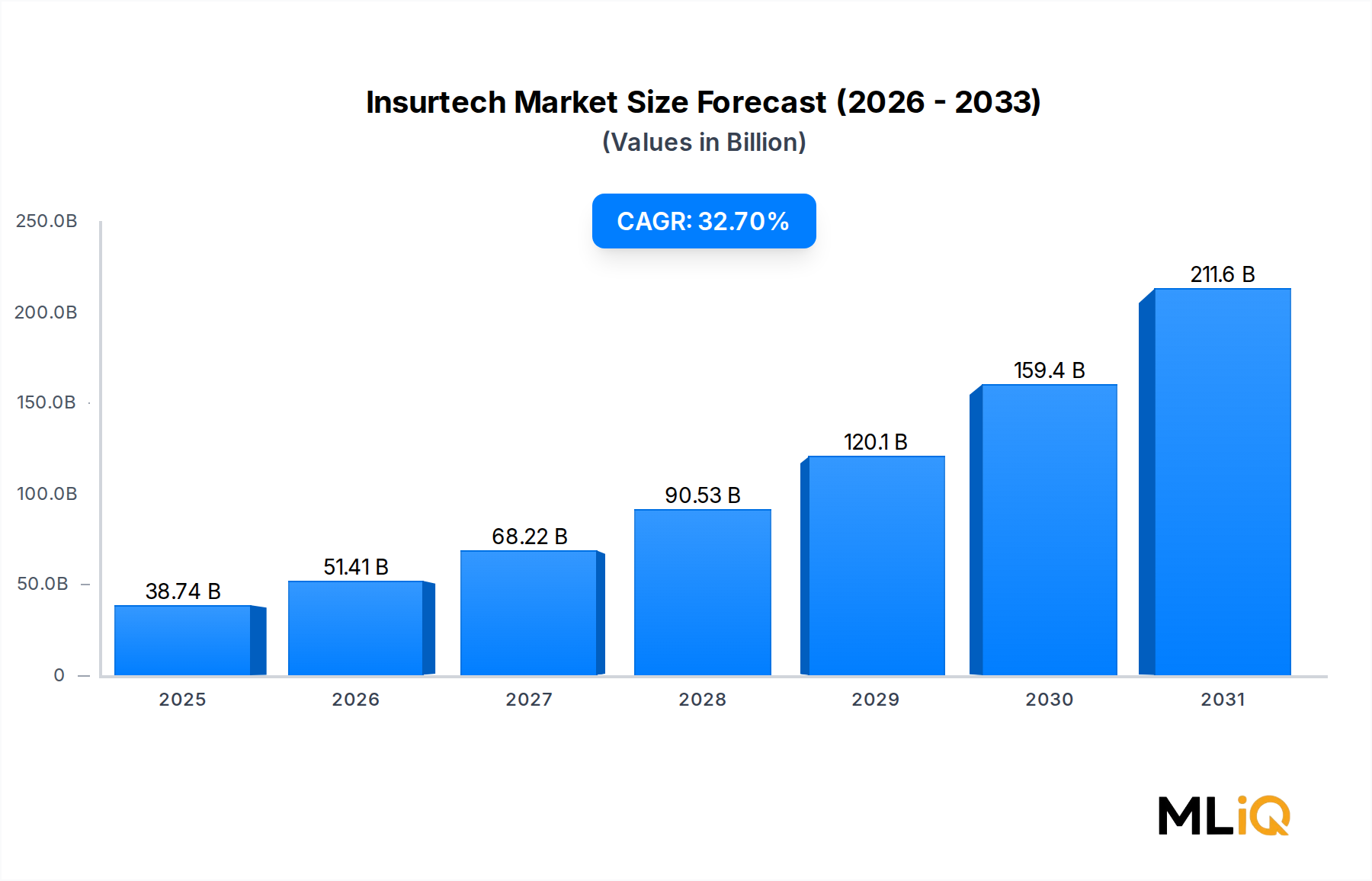

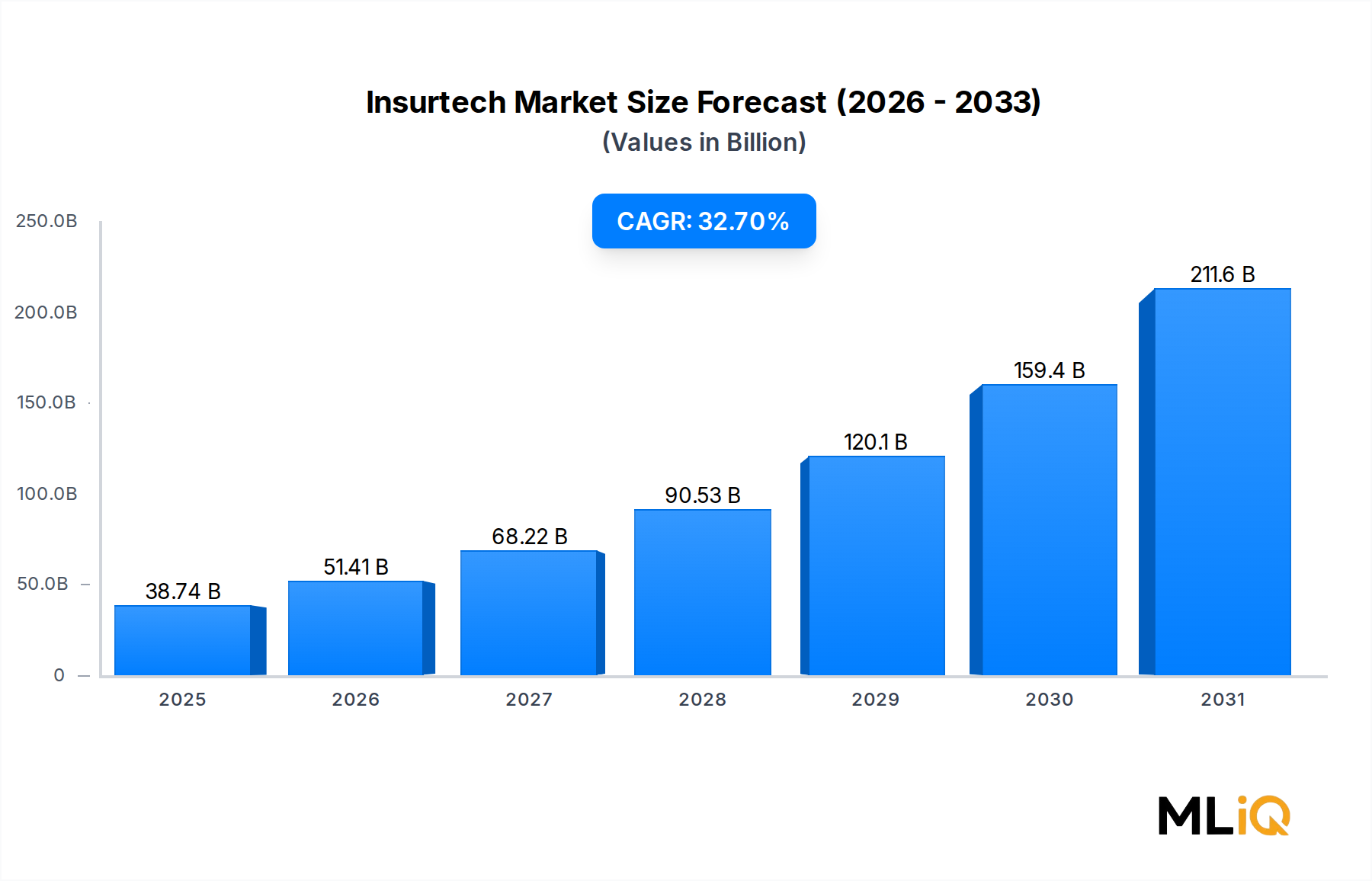

The global Insurtech Market is undergoing a period of transformative expansion, anchored by the convergence of advanced digital technologies, shifting consumer expectations, and structural inefficiencies in traditional insurance models. As of the base year, the market is valued at approximately $38,742.52 million, and it is projected to scale substantially through the forecast horizon of 2025–2033, registering a robust compound annual growth rate (CAGR) of 32.7%. This growth trajectory positions the insurtech sector as one of the fastest-growing verticals within the broader financial services ecosystem.

The core demand drivers for this market are deeply rooted in the digitization imperative that now defines the BFSI landscape. Insurers worldwide face mounting pressure to reduce loss ratios, improve underwriting accuracy, and streamline claims processing — all areas where insurtech platforms deliver measurable impact. Artificial intelligence and machine learning have emerged as cornerstone technologies, enabling real-time risk scoring and behavioral analytics. Cloud-based infrastructure has reduced the capital expenditure burden for mid-tier insurers seeking digital transformation at scale.

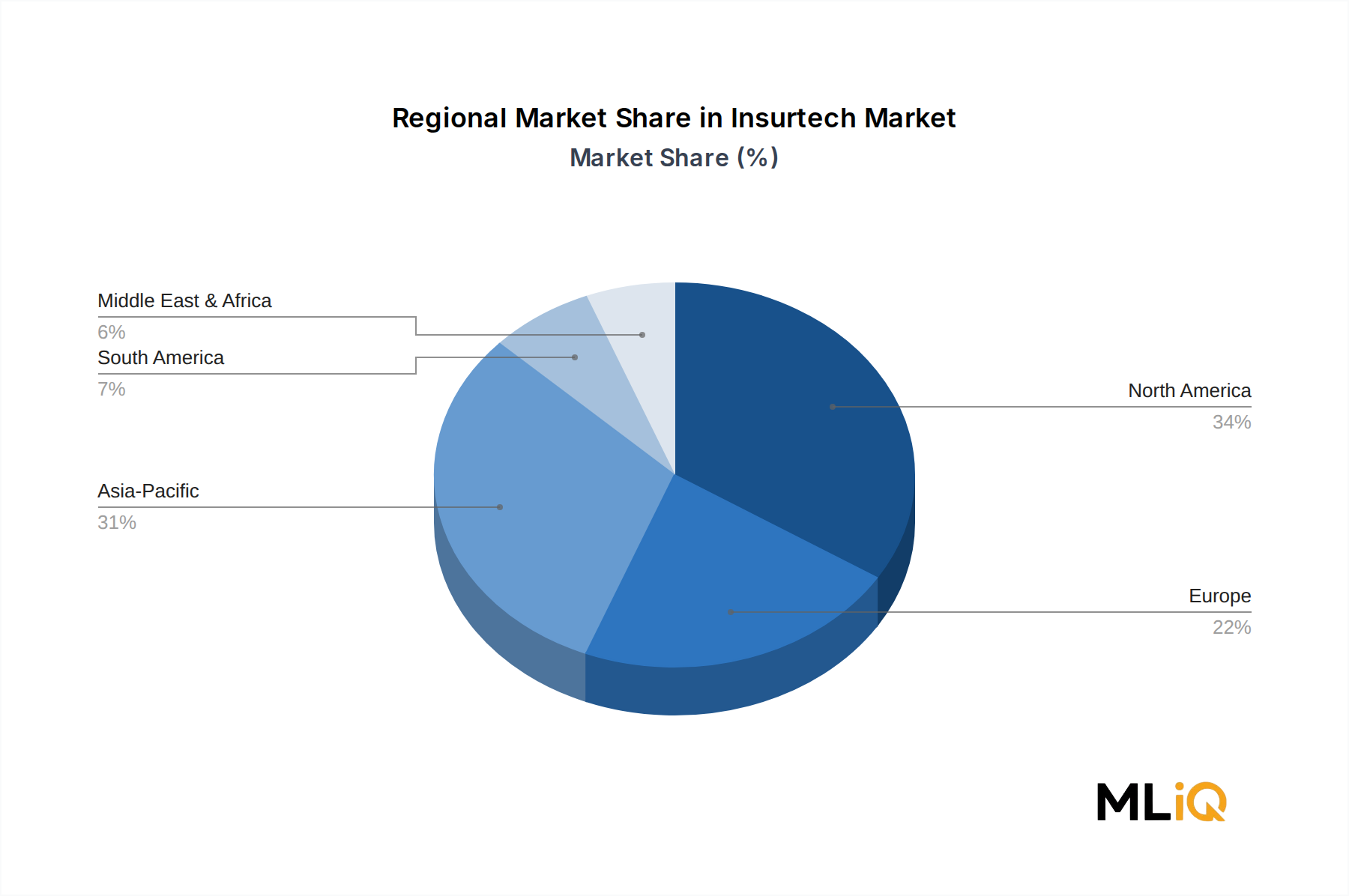

The macroeconomic tailwinds further reinforce this trajectory. Rising insurance penetration in emerging economies, particularly across Asia Pacific and Latin America, is generating new addressable markets for lightweight digital-first insurance models. Meanwhile, regulatory modernization in the European Union, the United Kingdom, and the United States is progressively creating sandbox environments that lower barriers to insurtech product launches.

On the demand side, post-pandemic behavioral shifts have accelerated consumer appetite for on-demand, embedded, and personalized insurance products. This has elevated the strategic relevance of usage-based insurance (UBI), parametric coverage, and microinsurance — all fundamentally insurtech-native product categories that legacy carriers struggle to replicate efficiently.

From a competitive standpoint, the market is characterized by a hybrid ecosystem comprising pure-play insurtech startups, incumbent carrier-affiliated digital ventures, and enterprise technology vendors pivoting into the space. Venture capital and private equity inflows into the insurtech segment have exceeded multi-billion-dollar annual thresholds in recent years, validating investor confidence in the long-term structural opportunity.

Looking forward, the 2025–2033 forecast period is expected to witness intensification in platform consolidation, with larger players acquiring niche specialists in telematics, cyber insurance modeling, and claims automation. The intersection of generative AI with policy personalization represents perhaps the most disruptive near-term development. Organizations that build proprietary data assets and decisioning engines are likely to command dominant market positions as the decade progresses.

In summary, the Insurtech Market is transitioning from an experimental growth phase to a structurally mature segment of the global insurance value chain, with clearly defined revenue streams, scalable technology stacks, and regulatory frameworks beginning to catch up with innovation velocity.