Dominance of Commercial Real Estate-Backed Loans Segment in the NPL Servicing Market

Among all loan type segments within the NPL Servicing Market, commercial real estate (CRE)-backed loans consistently command the largest revenue share. This dominance reflects the inherent complexity, ticket size, and resolution duration associated with CRE non-performing assets, all of which translate directly into higher fee income per case for servicers. CRE-backed NPLs typically involve multi-party collateral structures, cross-jurisdictional legal frameworks, and extended workout timelines that demand specialized due diligence capabilities — characteristics that create a significant barrier to entry and sustain premium pricing for experienced servicers.

The structural weight of CRE-backed NPLs in the global portfolio is substantial. Post-COVID-19, the commercial real estate sector experienced severe stress across office, retail, and hospitality sub-sectors. The work-from-home transition accelerated vacancy rates in prime office markets across New York, London, and Frankfurt, while the hospitality sub-sector — which constitutes a distinct sub-segment under hospitality-related loans — saw occupancy metrics collapse and subsequently recover unevenly. These dynamics created a large pipeline of distressed CRE assets that required professional NPL servicing intervention throughout 2021–2024.

In 2025, the CRE-backed loan segment maintains its leading position as institutional investors — including private equity real estate funds and sovereign wealth vehicles — continue to acquire distressed CRE portfolios from European and North American banks seeking to clean up balance sheets ahead of regulatory stress tests. The role of asset management companies in this ecosystem is particularly important; they often acquire CRE NPL portfolios outright and then engage specialist servicers to manage workout processes, borrower negotiations, and ultimately property disposition or debt restructuring.

Key players operating in this segment include large-scale servicers with dedicated CRE platforms, institutions such as Fannie Mae and Freddie Mac in the United States residential-commercial hybrid space, and global banks that have developed in-house NPL workout units. Technology companies providing collateral valuation analytics and workflow automation tools have also embedded themselves as critical infrastructure providers within CRE NPL resolution.

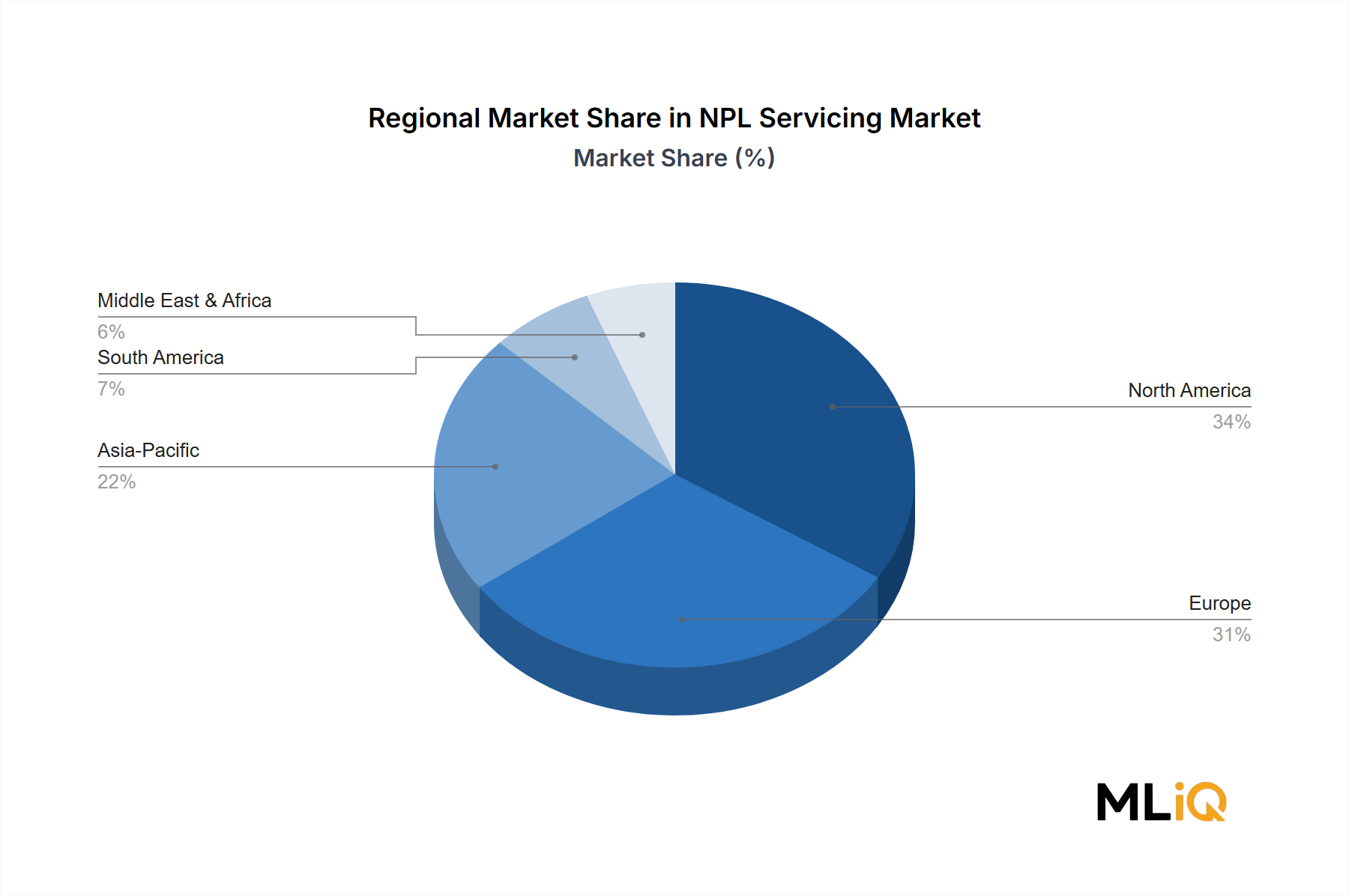

The segment's dominance is reinforced by regulatory dynamics. The European Banking Authority (EBA) guidelines on NPL management, introduced progressively since 2017 and tightened through 2022, require banks holding CRE-backed NPLs above defined thresholds to implement formal NPL reduction strategies, effectively mandating engagement with third-party servicers for institutions lacking internal workout capacity. In Asia Pacific, regulatory guidance from bodies such as the Reserve Bank of India and the China Banking and Insurance Regulatory Commission has similarly pushed CRE-related NPL resolution toward professional servicer frameworks.

From a service intensity perspective, CRE-backed NPL cases require the full spectrum of servicing capabilities: due diligence set-up involving property valuation and environmental assessment, on-boarding of complex loan documentation, ongoing asset loan management including tenant negotiations and rental income monitoring, and ultimately exit strategy execution through sale or restructuring. This comprehensive service requirement generates significantly higher revenue per loan than consumer unsecured or residential mortgage segments, explaining the segment's outsized revenue contribution relative to case volume.

Looking forward, the CRE-backed loan segment is expected to sustain its dominant position through 2033, though its share may modestly consolidate as consumer unsecured and residential mortgage NPL volumes grow faster in emerging markets. Office sector CRE distress in particular is expected to generate a sustained pipeline of new NPL cases in North America and Europe, maintaining servicer utilization rates at elevated levels. The growing involvement of the Debt Collection Software Market within CRE NPL workflows — particularly for automated borrower communication and legal case management — signals further technological deepening within this dominant segment.