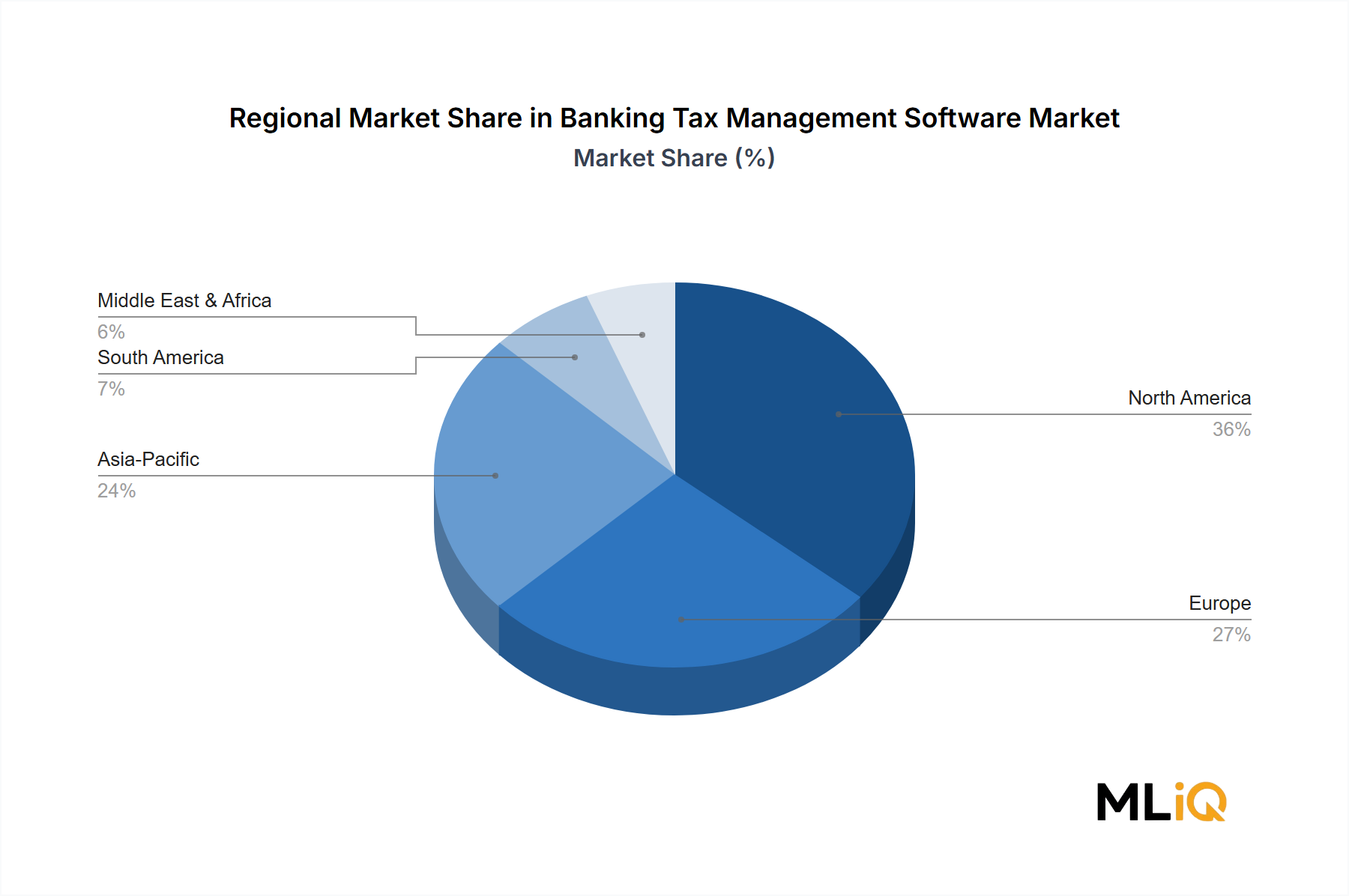

The Banking Tax Management Software Market exhibits distinct regional dynamics, with maturity levels, growth rates, and demand catalysts varying significantly across geographies.

North America — Largest Revenue Share: North America holds the largest regional share of the Banking Tax Management Software Market, accounting for approximately 38% of global revenue in 2025. The United States is the primary contributor, driven by the complexity of federal and state tax obligations, the IRS's aggressive digital filing mandates, and the high density of financial institutions requiring enterprise-grade compliance tools. Canada and Mexico contribute incrementally, with growing demand tied to cross-border trade tax reconciliation requirements under CUSMA. The regional CAGR is estimated at 9.8% through 2033, reflecting a mature but steadily growing market.

Europe — Regulatory-Driven Demand: Europe represents the second-largest regional market, with a revenue share of approximately 28% in 2025. Regulatory initiatives including DAC6, DAC7, DAC8, ATAD II, and the EU's VAT in the Digital Age (ViDA) package are compelling banks to overhaul their tax compliance infrastructure comprehensively. Germany, the United Kingdom, and France lead regional adoption. The European market is growing at a CAGR of 10.5%, with indirect tax software experiencing particularly rapid uptake.

Asia Pacific — Fastest-Growing Region: Asia Pacific is the fastest-growing region, projected to expand at a CAGR of 14.2% through 2033, driven by GST digitization in India, mandatory e-invoicing frameworks in China and Vietnam, and the maturation of fintech ecosystems across ASEAN markets. India and China collectively account for the majority of regional demand, with South Korea and Japan contributing through advanced banking sector modernization programs.

Middle East & Africa — Emerging Opportunity: The Middle East and Africa region is experiencing accelerating demand driven by VAT implementation across GCC member states and South Africa's expanding digital tax reporting framework. The regional CAGR is estimated at 12.7%, reflecting high growth from a comparatively low base. Turkey and Israel represent notable markets with sophisticated banking sectors investing in integrated tax platforms.

South America — Developing Market: South America, led by Brazil's SPED framework and Argentina's AFIP digital compliance mandates, is growing at a CAGR of 11.9%, with Brazil representing the dominant national market due to its complex, multi-layered indirect tax structure requiring specialized compliance technology.