Bank Loans as the Dominant Segment in the Debt Financing Market

Among the various debt instrument types — including bonds, debentures, bearer bonds, and other structured vehicles — bank loans represent the single largest revenue-generating segment within the Debt Financing Market. This dominance stems from several structural, regulatory, and behavioral factors that have entrenched bank lending as the primary conduit for corporate and institutional debt capital globally.

Bank loans offer borrowers a degree of flexibility that public bond markets cannot easily replicate. Features such as revolving credit facilities, covenant-light structuring, variable amortization schedules, and direct lender-borrower negotiation make them uniquely suited to both large corporations requiring multi-billion-dollar leveraged buyout financing and smaller enterprises seeking working capital lines. The bilateral and syndicated loan markets together command the largest share of total debt origination volume, and this share has shown resilience even as bond markets have grown in absolute terms.

From a supply perspective, major global banks including JPMorgan Chase & Co., Bank of America Corporation, Citigroup, Inc., Barclays Bank PLC, and Deutsche Bank AG have maintained extensive corporate lending divisions that serve as anchor participants in large syndicated loan transactions. These institutions leverage their balance sheet strength, relationship networks, and distribution capabilities to underwrite and syndicate high-value facilities to institutional investors, reducing concentration risk while maintaining origination fee income.

The leveraged loan sub-segment has been particularly dynamic, driven by private equity-sponsored acquisitions and recapitalizations. In 2022 and 2023, leveraged loan issuance exceeded $1.3 trillion in the U.S. alone, according to industry data, reflecting the persistent role of borrowed capital in M&A-driven value creation. The Syndicated Loan Market, which operates as a closely adjacent segment to the bank loan category, has seen increased participation from non-bank lenders and collateralized loan obligation (CLO) vehicles, further deepening liquidity and broadening the investor base.

The duration dimension also favors bank loans as a dominant segment. Both short-term revolving facilities and long-term term loans B and C structures serve distinct borrower needs across the capital structure. Short-term bank lending supports inventory financing, trade finance, and seasonal working capital requirements, while long-term loans underpin capital-intensive infrastructure, energy, and real estate projects with multi-decade payback horizons.

Regulatory capital frameworks, particularly Basel III and its evolving Basel IV successor, have introduced constraints on bank balance sheet capacity, which paradoxically has reinforced the dominance of bank loans by channeling origination activity through loan sales, securitization, and participation markets — all of which scale off the foundational bank loan instrument. The Asset-Backed Securities Market has grown in tandem, as banks repackage loan pools into tradeable instruments that recycle capital for further lending.

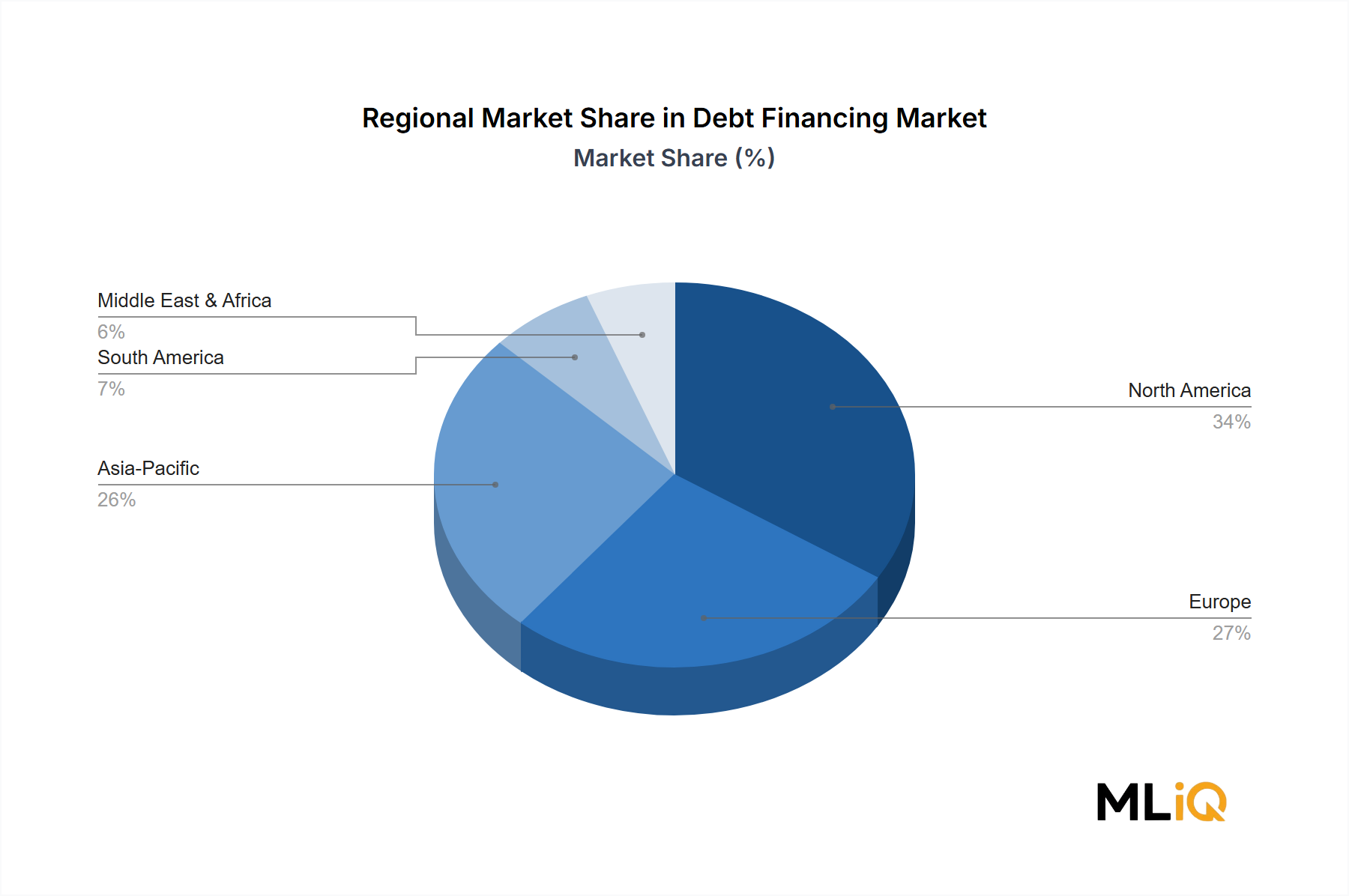

Bank loan market share is not merely sustaining — it is consolidating in certain geographies, particularly in Asia Pacific, where domestic banking systems are the primary or sole source of formal credit for large segments of the corporate sector. China's state-owned banking giants and India's public sector banks continue to dominate their respective national loan markets, making bank lending the de facto first port of call for corporate debt financing across the region's major economies.