Business-Oriented Application Segment Dominance in the Cash Payment Market

Among the two primary end-user segments — Business and Personal — the Business segment stands as the dominant revenue contributor within the Cash Payment Market, commanding the largest share of transaction volume and infrastructure investment globally. This dominance is rooted in the sheer scale of enterprise-level cash flows, which encompass payroll disbursements, vendor settlements, petty cash management, retail float operations, and large-volume bill payment processing across sectors including hospitality, utilities, retail, and logistics.

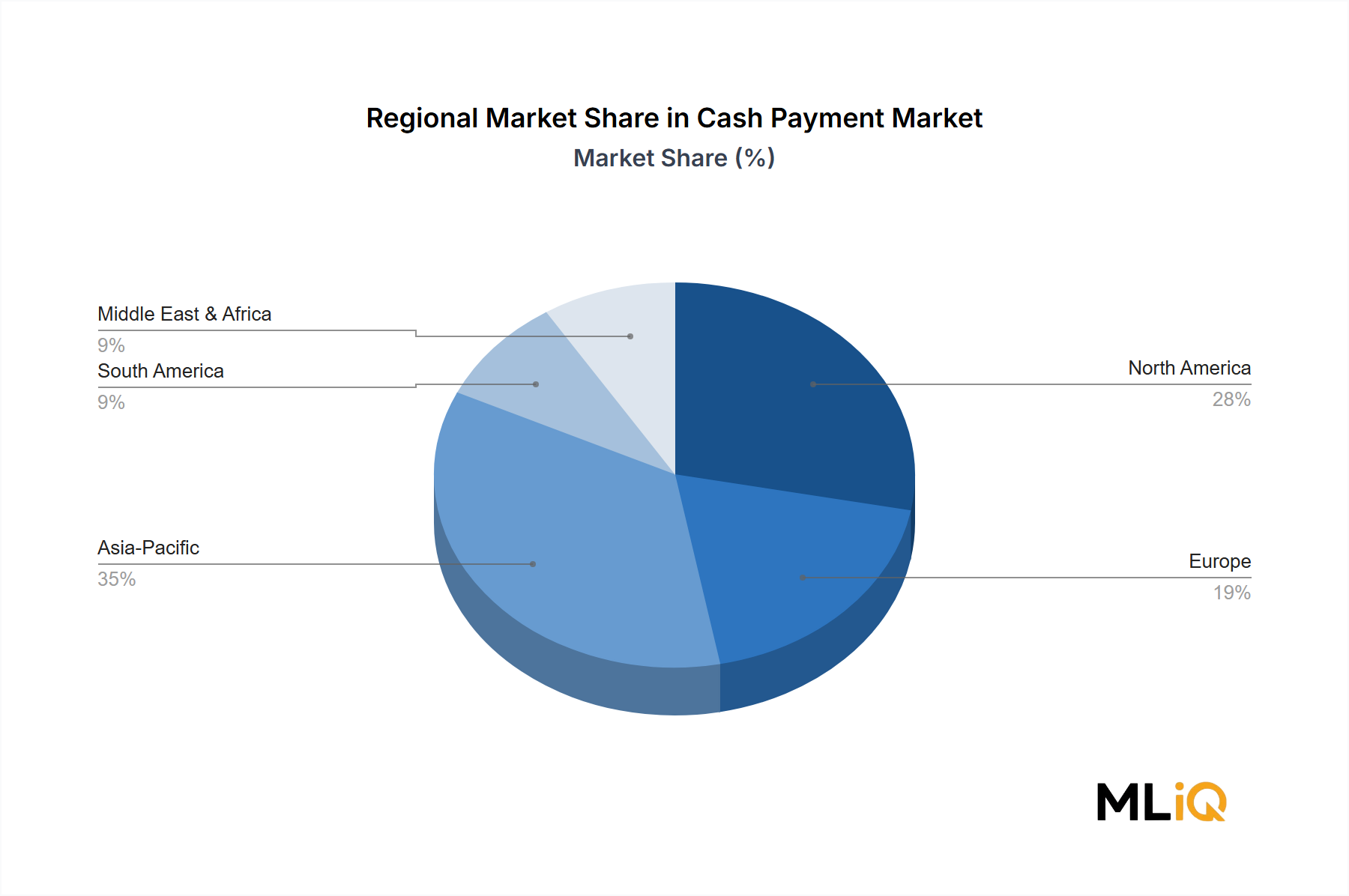

The Business end-user segment's primacy is especially pronounced in economies with high proportions of small and medium-sized enterprises (SMEs) that operate predominantly in cash. In markets such as India, Indonesia, Nigeria, and Mexico, cash transactions constitute the backbone of supply chain settlements, with SMEs relying on cash-in/cash-out networks for day-to-day operational liquidity. The formalization of these transactions through regulated cash payment channels is a key growth vector driving Business segment expansion.

Within the application sub-segments, Shopping accounts for the highest frequency of Business-related cash transactions, driven by the continuing prevalence of cash-accepting retail points of sale in tier-2 and tier-3 cities worldwide. Electricity Bill Payments and Hotel Bill Payments together represent a substantial and consistently growing portion of business cash outflows, particularly in markets where utility digitization lags behind consumer demand. Travel Bookings via cash, while diminishing in advanced economies, remain structurally significant in Southeast Asia and North Africa.

Key players active in the Business segment include Visa Inc., which has developed cash-compatible hybrid payment rails targeting enterprise clients; Mastercard Incorporated, whose cash access network serves millions of business accounts across 210 countries; and PayPal Payments Private Limited, which has expanded its merchant services to accommodate cash-equivalent disbursements via its working capital products. The Bank of America Corporation and Capital One Financial Corporation provide comprehensive cash management solutions to mid-market and large enterprise clients, integrating armored transport logistics with digital reconciliation.

Strategically, the Business segment's share within the Cash Payment Market is consolidating rather than fragmenting. The top five players collectively account for an estimated 60–65% of business-oriented cash payment infrastructure globally, driven by their ability to offer end-to-end cash management suites that combine physical currency handling with real-time digital reporting. This consolidation is expected to intensify through 2028 as enterprise demand for integrated treasury management and cash-flow visibility tools increases.

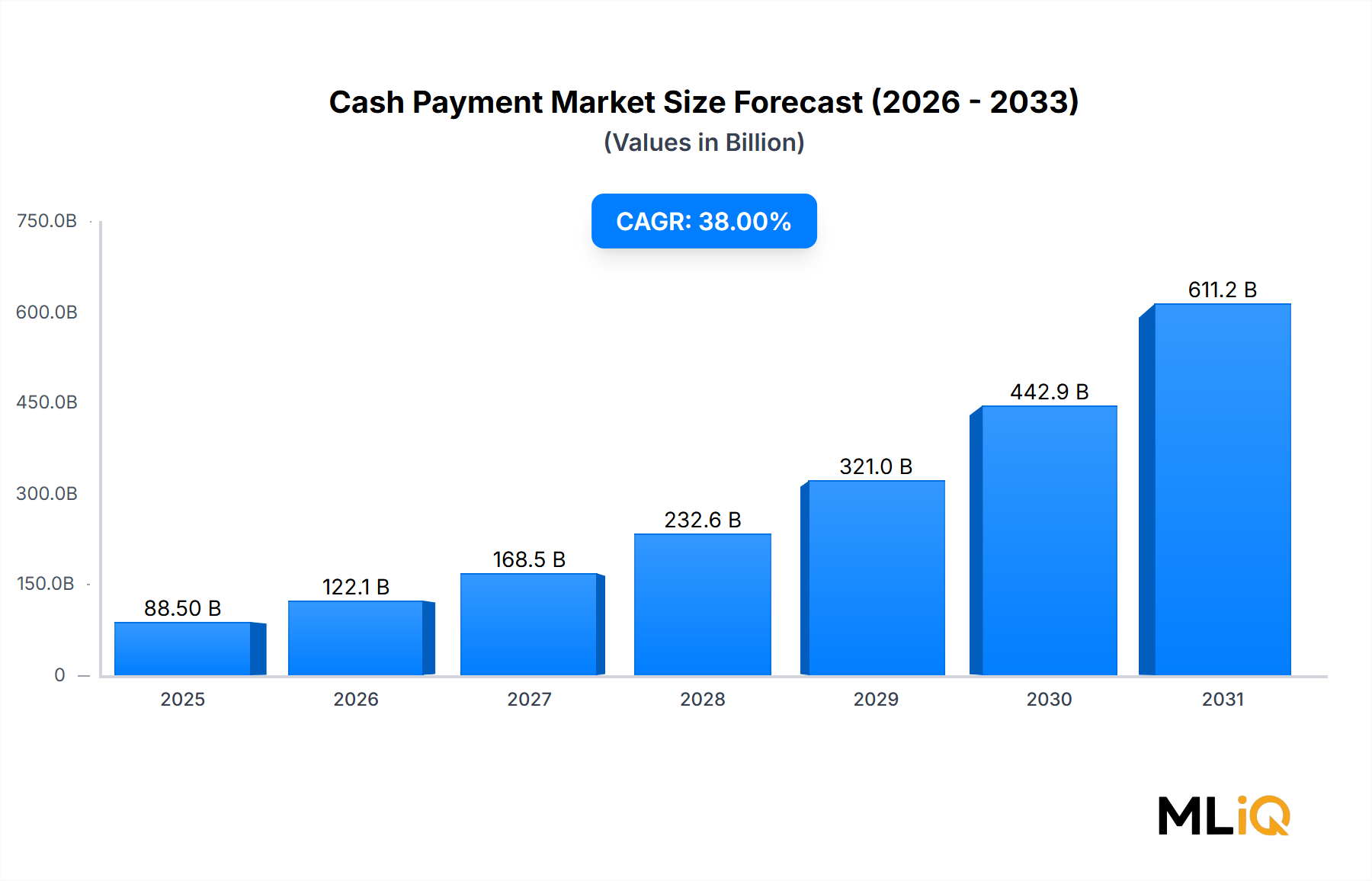

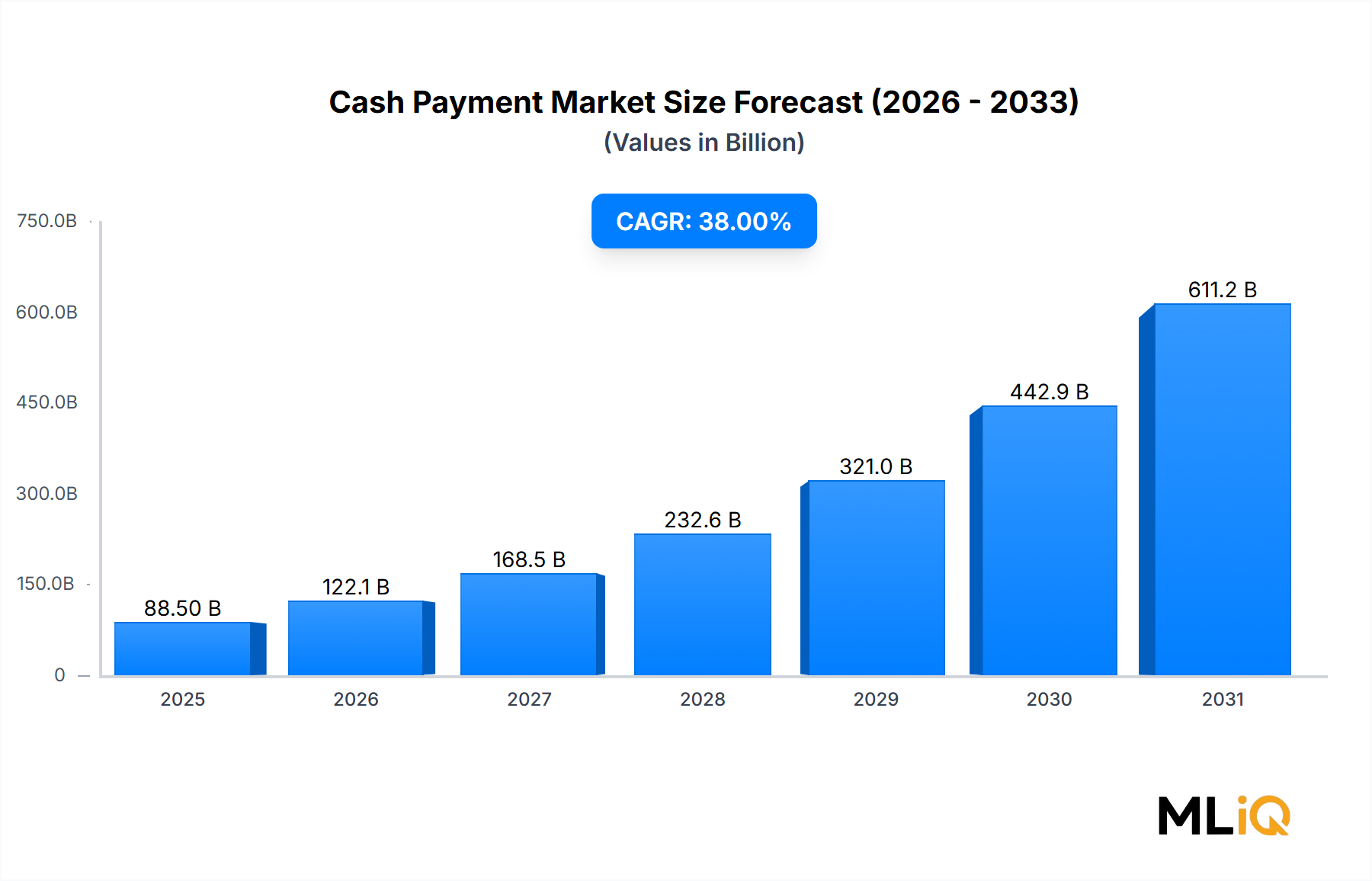

For mid-market businesses, Stripe and Payoneer Inc. are emerging as notable challengers, offering hybrid solutions that bridge cash deposits with digital payment orchestration, thereby expanding the Business segment's total addressable market by onboarding previously unbanked business entities. The net effect is a reinforcing feedback loop: as more businesses formalize their cash operations through regulated platforms, the overall market valuation continues to climb at rates consistent with the reported 38% CAGR.

The segment's forward outlook is further bolstered by regulatory mandates in the European Union, Gulf Cooperation Council states, and Southeast Asian jurisdictions requiring businesses above certain revenue thresholds to maintain documented cash transaction trails, which in turn necessitates investment in certified cash payment infrastructure and software.