1. What are the major growth drivers for the Microgrid Market market?

Factors such as are projected to boost the Microgrid Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

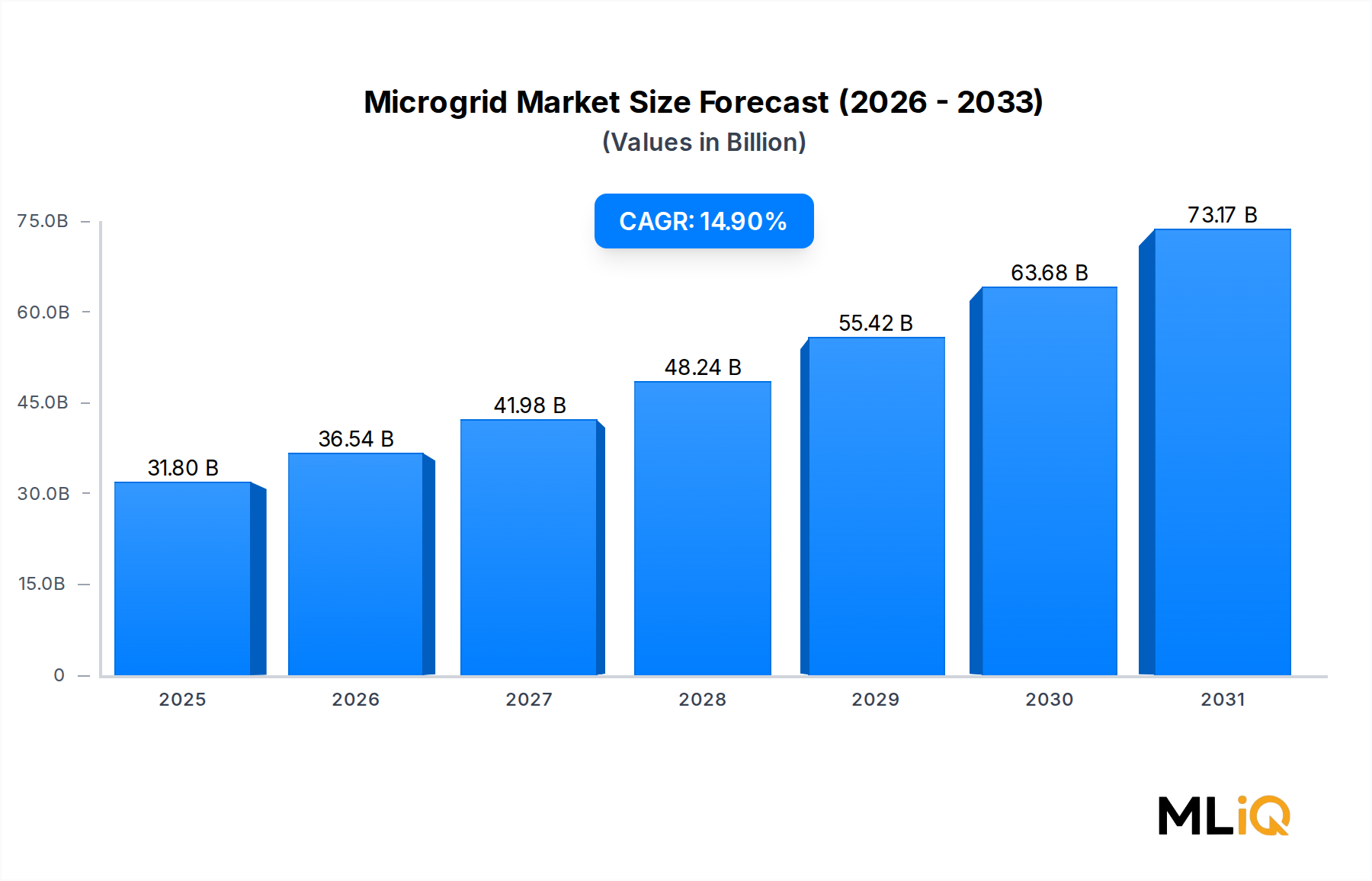

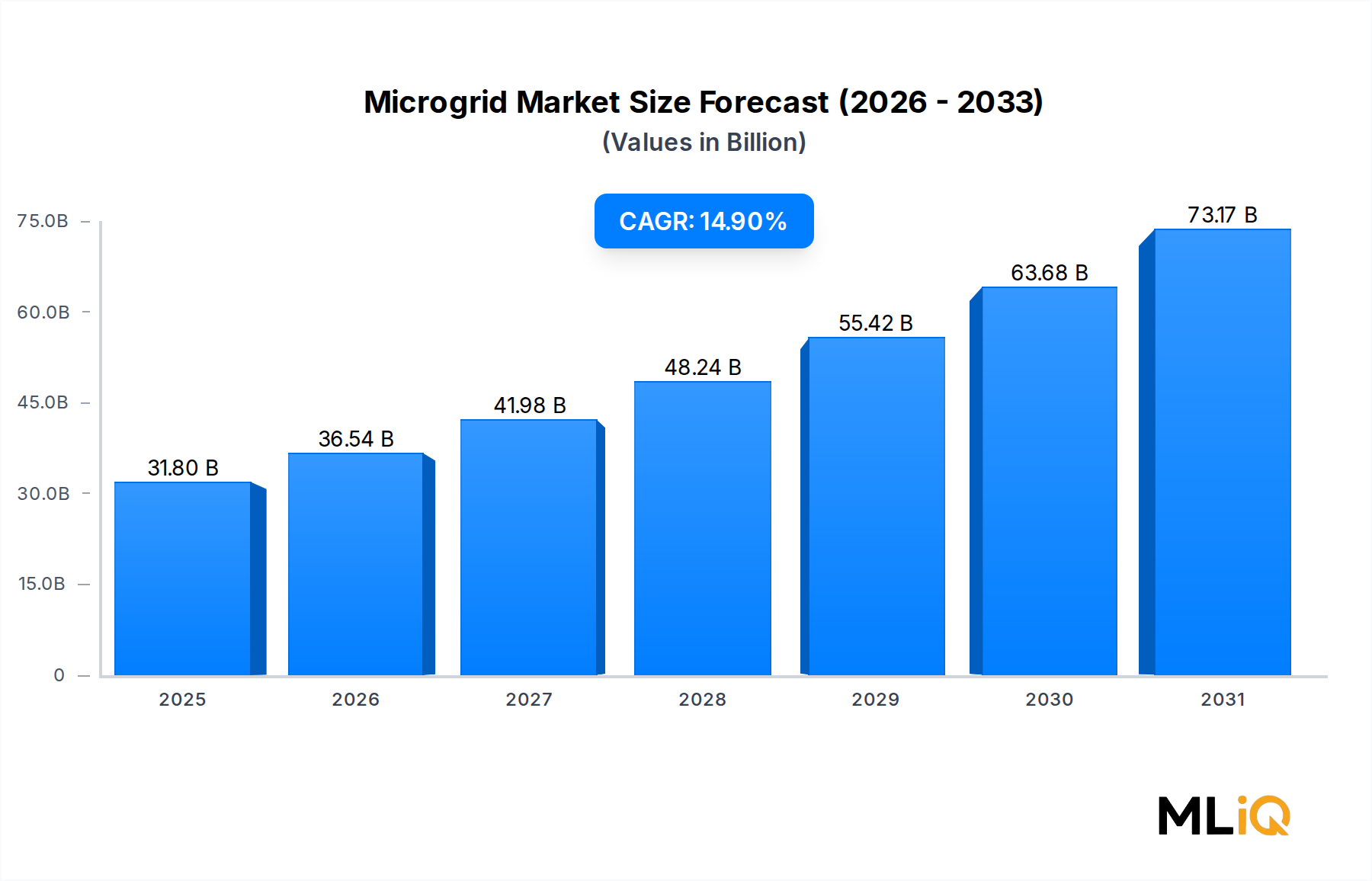

The global microgrid market is on a steep upward trajectory, with the market valued at $31.80 billion and projected to expand at a compound annual growth rate of 14.9% over the forecast period. This robust growth underscores the accelerating global shift toward decentralized, resilient, and clean energy architectures that can operate independently from or in coordination with the main utility grid.

At its core, the microgrid market is being propelled by three macro tailwinds: the energy transition away from fossil fuels, the escalating frequency of extreme weather events that expose the vulnerability of centralized grids, and the rapid cost reduction of distributed energy technologies such as solar photovoltaics and battery storage. Governments and utilities across the globe are increasingly recognizing microgrids as critical infrastructure for grid resilience, particularly in regions prone to natural disasters, grid outages, and energy access deficits.

The commercialization of advanced power electronics, bidirectional inverters, and sophisticated energy management software has made microgrids increasingly viable not just for remote or off-grid applications but also for urban commercial districts, military installations, university campuses, and hospital complexes. These diverse end-use cases are broadening the total addressable market considerably.

From a demand driver standpoint, the integration of distributed generation — including rooftop solar, wind turbines, and combined heat-and-power systems — is expanding the technical boundaries of what constitutes a microgrid. Simultaneously, the declining levelized cost of energy storage is enabling more economically attractive business cases. The Energy Storage System Market, the Solar Inverter Market, and the broader Renewable Energy Market are all converging to lower the capital expenditure threshold for microgrid deployment.

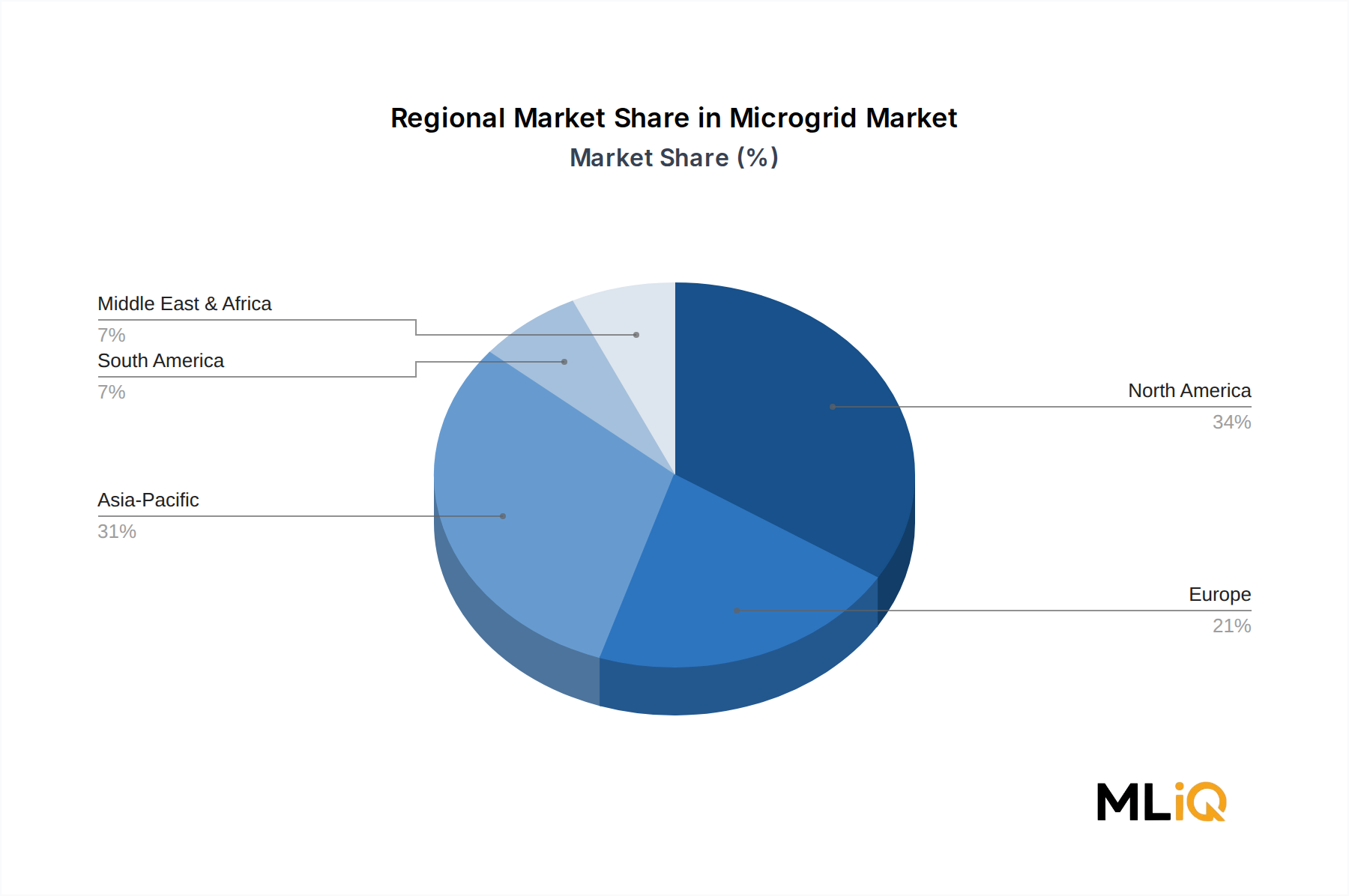

Regionally, North America currently holds the largest revenue share, driven by federal incentive programs, grid modernization mandates, and significant military microgrid investments. Asia Pacific is the fastest-growing region, supported by India's rural electrification agenda and China's industrial park microgrid initiatives. Europe is advancing through regulatory mandates tied to carbon neutrality targets by 2050.

Looking forward, the microgrid market is poised to become a cornerstone of the next-generation energy ecosystem. As digitalization deepens — through AI-driven energy dispatch, vehicle-to-grid integration, and peer-to-peer energy trading — microgrids will evolve from passive local grids into intelligent, transactive energy nodes. Strategic investment, technology innovation, and supportive policy environments collectively position this market for sustained double-digit growth well into the next decade.

Among the various technology configurations available in the microgrid market, AC microgrids represent the dominant segment by revenue share. This leadership is attributable to a confluence of legacy infrastructure compatibility, the established ecosystem of AC-native equipment, and the extensive installed base of alternating current electrical systems in commercial, industrial, and utility settings worldwide.

AC microgrids operate at standard alternating current frequencies — typically 50 Hz or 60 Hz — which allows them to interface seamlessly with existing grid infrastructure, conventional generators, and a vast portfolio of load equipment without requiring additional conversion hardware. This plug-and-play compatibility dramatically reduces the integration complexity and capital expenditure associated with brownfield deployments, making AC microgrids the default choice for utilities, municipalities, and large commercial operators retrofitting existing facilities.

From a technical standpoint, AC microgrids benefit from well-understood protection schemes, fault detection methodologies, and islanding detection protocols. Engineers and operators globally are trained and equipped to work with AC systems, reducing the human capital risk that might otherwise accompany the deployment of novel architectures. The standardization of AC protection relays, circuit breakers, and switchgear further reinforces the segment's economic advantage.

Key players actively driving growth within the AC microgrid segment include SIEMENS, which offers integrated AC microgrid solutions combining grid-tied and island-mode operations with advanced SCADA integration; ABB Group, whose AC microgrid platforms are widely deployed in utility-scale and remote mining applications; and Schneider Electric, which has developed modular AC microgrid architectures tailored to commercial campuses and data centers. GENERAL ELECTRIC contributes through its Grid Solutions division, offering turnkey AC microgrid deployments with predictive maintenance capabilities.

S&C ELECTRIC has established a strong position in utility-scale AC microgrid deployments, particularly in North America, where it has commissioned several high-profile projects integrating solar, storage, and diesel backup in a synchronized AC bus configuration. EATON CORPORATION provides AC power management and protection equipment that underpins a significant proportion of commercial and industrial AC microgrid installations globally.

The share of AC microgrids, while still dominant, is gradually consolidating rather than expanding proportionally. DC microgrids are gaining ground in data center applications, EV charging infrastructure, and certain industrial facilities where DC-native loads predominate, and where conversion losses associated with AC-DC-AC conversion cycles represent a meaningful efficiency penalty. Hybrid microgrids — architectures that incorporate both AC and DC buses linked by bidirectional power converters — are emerging as a middle-ground solution, capturing efficiency gains in DC-heavy subsystems while retaining the broad compatibility of AC distribution.

Nonetheless, for the foreseeable forecast horizon, AC microgrids will continue to command the majority of market revenue. The breadth of applicable end-use cases, the depth of the existing technology supply chain, and the institutional familiarity with AC systems among utilities and developers collectively ensure that AC microgrid configurations remain the workhorses of the global microgrid deployment pipeline. The segment's consolidation reflects market maturation rather than decline, as average project sizes increase and long-term service agreements become standard commercial structures within the space.

The Power Electronics Market plays a crucial enabling role within AC microgrid deployments, providing the inverters, converters, and static switches that manage power quality, synchronization, and seamless transitions between grid-connected and island modes.

Several powerful forces are driving adoption of microgrids at an accelerating pace, while a distinct set of structural constraints moderates the pace of market expansion.

On the driver side, grid resilience demand is quantifiable and urgent. The United States alone experienced over 180 major power outage events affecting more than 50,000 customers between 2015 and 2023, according to the Department of Energy. Each high-profile grid failure — such as the 2021 Texas winter storm, which left over 4.5 million homes without power — creates an immediate policy and investment response that translates into microgrid procurement contracts at federal, state, and utility levels. HONEYWELL has cited grid resilience as the primary procurement motivation in over 65% of its commercial microgrid engagements.

The falling cost of solar photovoltaic generation — which dropped by approximately 90% per watt between 2010 and 2023 — combined with lithium-ion battery storage costs declining to below $130/kWh at the pack level as of 2023, has dramatically improved the economics of microgrid projects. These cost curves directly stimulate the Lithium-Ion Battery Market and the Solar Inverter Market, which are both integral supply chain components for microgrid developers.

Electrification of remote and off-grid communities represents a structural long-term driver. An estimated 760 million people globally lack access to electricity as of the latest International Energy Agency data, and microgrids — particularly solar-diesel hybrid and solar-battery configurations — are widely recognized as the most cost-effective pathway to first-time electrification in Sub-Saharan Africa and Southeast Asia.

On the constraint side, the high upfront capital cost of microgrid deployment — ranging from $500,000 to over $5 million per MW for complex grid-connected configurations — remains a significant barrier, particularly for municipal and healthcare end-users with constrained capital budgets. Regulatory fragmentation across jurisdictions creates another material constraint: interconnection standards, net metering policies, and rate structures vary significantly across states and countries, creating project development risk that increases transaction costs and prolongs permitting timelines.

Cybersecurity vulnerabilities in digitally networked microgrid systems represent an emerging constraint. As microgrids become more software-defined and internet-connected, their attack surface expands, necessitating investment in cybersecurity frameworks that add to total project cost.

The competitive landscape of the microgrid market is characterized by a blend of diversified industrial conglomerates, specialist energy technology firms, and emerging pure-play microgrid solution providers. The following profiles capture the strategic posture of the market's leading participants:

SIEMENS: A global leader in integrated microgrid solutions, Siemens leverages its Spectrum Power and SICAM platforms to deliver advanced energy management and automation capabilities across utility, commercial, and industrial segments, with a particularly strong project pipeline in Europe and North America.

PARETO ENERGY: A specialist microgrid developer and operator, Pareto Energy focuses on behind-the-meter solutions for commercial and industrial clients, differentiating through performance-based contracts and long-term operational service agreements that reduce customer capital risk.

ABB Group: ABB brings deep expertise in power electronics, grid automation, and SCADA systems to its microgrid portfolio, with notable deployments in remote mining operations, island utilities, and university campuses across more than 40 countries.

Schneider Electric: Schneider's EcoStruxure microgrid architecture offers modular, scalable solutions for campus, data center, and utility applications, backed by a global services network and a strong software analytics layer for predictive energy optimization.

S&C ELECTRIC: S&C Electric is recognized for its PureWave microgrid controller and grid automation expertise, with a focus on utility-grade islanding, seamless reconnection, and multi-source distributed generation integration in North American markets.

GENERAL ELECTRIC: GE's Grid Solutions division offers a full-spectrum microgrid portfolio encompassing controls, protection, and energy storage integration, with deployments spanning military bases, remote communities, and industrial facilities globally.

SPIRAE INC.: Spirae is a specialized software and consulting firm focused on distributed energy resource management and microgrid control systems, providing the intelligence layer for complex multi-asset microgrid configurations at utility and campus scale.

EATON CORPORATION: Eaton delivers power management hardware and software for microgrid applications, including uninterruptible power supply systems, switchgear, and energy storage integration platforms targeting data center and critical facility markets.

HONEYWELL: Honeywell integrates building automation, energy management, and cybersecurity capabilities into its microgrid offerings, positioning itself as a full-stack solution provider for commercial real estate, healthcare, and government clients.

EXELON CORPORATION: As one of the largest utility holding companies in the United States, Exelon actively develops and operates community microgrids, participating in both the supply and demand sides of the market while advocating for favorable interconnection and rate policies.

January 2024: The U.S. Department of Energy announced a $366 million investment in 25 projects across 22 states under the Grid Resilience and Innovation Partnerships program, with a significant portion directed toward community and campus microgrid deployments.

March 2024: Schneider Electric launched EcoStruxure Microgrid Advisor 3.0, incorporating AI-driven load forecasting and multi-day ahead battery dispatch optimization, targeting large commercial and industrial clients in North America and Europe.

May 2024: ABB Group commissioned a 5 MW solar-plus-storage microgrid at a remote mining operation in Western Australia, demonstrating diesel displacement exceeding 70% and establishing a replicable model for off-grid industrial electrification.

July 2024: India's Ministry of New and Renewable Energy issued revised guidelines for solar microgrid installations under the PM-KUSUM scheme, targeting 10,000 new rural microgrid installations by 2026, unlocking an estimated $800 million in new project investment.

September 2024: SIEMENS and a major U.S. military branch signed a 10-year energy services agreement for microgrid operation and maintenance across 12 military installations, representing one of the largest long-term microgrid service contracts executed to date.

November 2024: The European Commission published its updated Net-Zero Industry Act implementing regulations, formally classifying microgrids as strategic net-zero technology, qualifying them for accelerated permitting and blended finance instruments through the European Investment Bank.

February 2025: HONEYWELL introduced its Forge Energy Optimization platform with native microgrid orchestration capability, integrating real-time carbon intensity signals from grid operators to dynamically switch between renewable generation, storage dispatch, and grid import.

The microgrid market exhibits distinct regional dynamics, shaped by varying policy environments, grid reliability profiles, energy access challenges, and technology adoption rates.

North America leads in absolute revenue terms, accounting for approximately 38% of global market share. The United States is the primary engine, driven by Department of Energy grant programs, military energy resilience mandates, and a growing number of state-level microgrid incentive programs in California, New York, and Connecticut. The regional CAGR is estimated at 13.2%, reflecting a relatively mature but still rapidly expanding market. Canada contributes through remote community electrification programs in northern territories, while Mexico is an emerging adopter driven by industrial park demand.

Asia Pacific is the fastest-growing region, with a projected CAGR of 17.6% through the forecast period. China's industrial microgrid deployments — particularly in economic development zones and port facilities — combined with India's ambitious rural electrification programs under PM-KUSUM and the national Smart Cities Mission are the primary growth catalysts. Japan and South Korea are advancing microgrids as disaster resilience infrastructure following lessons learned from major seismic and typhoon events. The Advanced Metering Infrastructure Market and the Smart Grid Market are both accelerating alongside microgrid adoption in the region.

Europe maintains a strong market position, estimated at a regional CAGR of 14.1%, underpinned by the European Green Deal's decarbonization mandates, island electrification programs in Greece, Spain, and Portugal, and significant investment in energy community frameworks that treat microgrids as shared infrastructure. Germany and the UK are leading adopters, while Nordic countries are deploying microgrids to support high penetrations of variable renewable generation.

Middle East and Africa represents a high-potential emerging region. Sub-Saharan Africa, where grid access deficits are most acute, is attracting increasing donor and development finance institution funding for solar microgrid rural electrification, supporting a regional CAGR of approximately 18.4% — the highest of any region. The GCC countries are deploying microgrids in industrial and desalination facilities as part of broader energy diversification strategies.

South America, led by Brazil and Chile, is an emerging market driven by mining sector demand for off-grid power solutions and growing interest in community energy resilience programs in geographically isolated regions. The Commercial and Industrial Energy Market is a key end-use anchor across all regions.

The supply chain underpinning the microgrid market is complex and multi-tiered, encompassing raw material extraction, component manufacturing, system integration, software development, and long-term operations and maintenance services. Understanding the upstream dependencies and sourcing risks is essential for accurately assessing market risk-adjusted growth trajectories.

Lithium, cobalt, and nickel are the three most critical raw materials for battery energy storage systems — the fastest-growing component category within microgrid deployments. Lithium carbonate prices experienced extreme volatility between 2021 and 2024, surging to over $80,000 per metric ton in early 2023 before retracing sharply to below $15,000 per metric ton by late 2024. This price cycle introduced significant project economics uncertainty for microgrid developers who had penciled in storage costs at pre-spike levels. Cobalt — predominantly sourced from the Democratic Republic of Congo, which accounts for over 70% of global supply — remains a geopolitical sourcing risk, with ongoing concerns around artisanal mining practices and supply concentration.

Silicon carbide (SiC) and gallium nitride (GaN) are increasingly critical semiconductor materials for the power electronics and inverter components that form the control backbone of microgrids.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.9% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Microgrid Market market expansion.

Key companies in the market include SIEMENS, PARETO ENERGY, ABB Group, Schneider Electric, S&C ELECTRIC, GENERAL ELECTRIC, SPIRAE INC., EATON CORPORATION, HONEYWELL, EXELON CORPORATION.

The market segments include Connectivity, Type, End User.

The market size is estimated to be USD 31.80 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3713, USD 5770, and USD 10665 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Microgrid Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Microgrid Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.