1. What are the major growth drivers for the Aircraft Electric Motor Market market?

Factors such as are projected to boost the Aircraft Electric Motor Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

Aircraft Electric Motor Market

Aircraft Electric Motor Market+1 2315155523

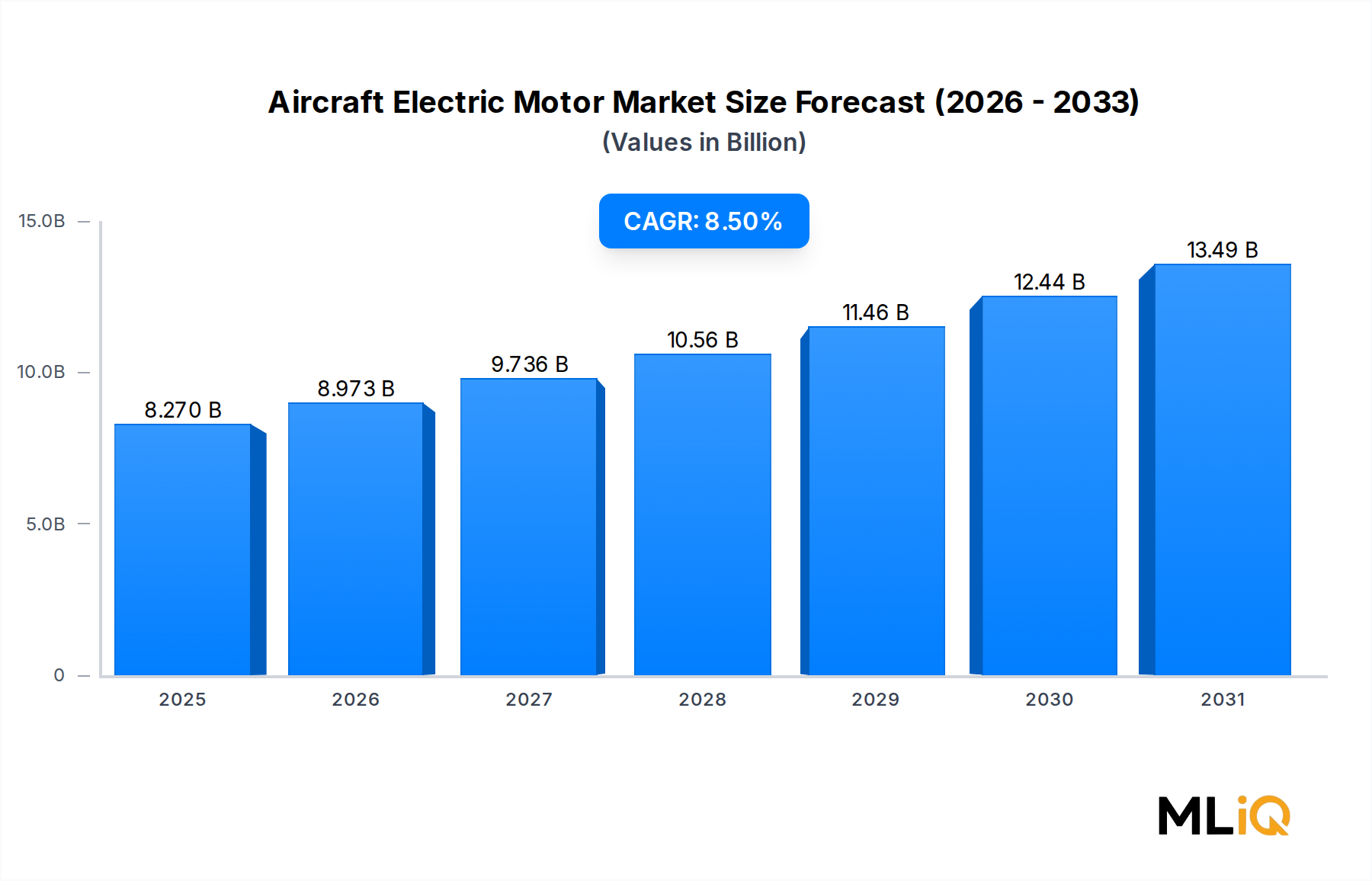

The global Aircraft Electric Motor Market is valued at $8,270.45 million and is projected to expand at a compound annual growth rate of 8.5% over the forecast horizon, reflecting the aviation industry's accelerating pivot toward electrification, decarbonization, and next-generation propulsion architectures. This robust growth trajectory is underpinned by converging macro forces: tightening carbon emission standards for commercial aviation, rising fuel costs that make electric alternatives economically compelling, increased government funding for sustainable aviation programs, and rapid advances in power-dense electric motor designs that have dramatically improved thrust-to-weight ratios.

The market encompasses electric motors deployed across propulsion systems, flight control surfaces, engine management, and environmental control systems—spanning both AC and DC motor types and output bands from sub-10 kW auxiliary units to 200 kW+ propulsion-grade assemblies. The proliferation of hybrid-electric regional aircraft programs, the exponential growth of unmanned aerial vehicle (UAV) platforms, and the emergence of advanced air mobility (AAM) corridors worldwide are collectively generating sustained, diversified demand across segments.

North America remains the dominant revenue contributor, anchored by significant R&D investments from U.S. Department of Defense programs and a dense cluster of aerospace OEMs and electric propulsion startups. Europe follows closely, driven by Airbus's hybrid-electric roadmap and the European Union Aviation Safety Agency (EASA) regulatory framework incentivizing zero-emission technologies. The Asia-Pacific region is emerging as the fastest-growing geography, fueled by China's aggressive electric aircraft ambitions, India's regional aviation expansion, and Japan's urban air mobility pilots.

Key demand drivers include the International Air Transport Association's net-zero carbon commitment by 2050, which has catalyzed procurement decisions across airline and aircraft OEM tiers. The broader Electric Aircraft Market is catalyzing upstream demand for high-performance motors capable of meeting stringent aerospace reliability and thermal management requirements. Meanwhile, advances in the Lithium-Ion Battery Market are directly enabling higher energy density storage solutions that make fully electric short-haul and air taxi operations commercially viable within this decade.

Looking ahead, the market is expected to witness intensified competition between established aerospace incumbents and well-funded deep-tech startups, increased verticalization of motor manufacturing, and a sharpening focus on certification pathways under evolving FAA and EASA guidelines. The intersection of digital twin simulation, additive manufacturing, and superconducting materials is expected to yield motors with power densities previously unattainable, further accelerating market adoption through 2030 and beyond.

Among all application segments, the propulsion system sub-market commands the largest revenue share within the Aircraft Electric Motor Market. This dominance is not incidental—it stems from the fundamental role that electric motors play in redefining how lift and thrust are generated in modern electric and hybrid-electric aircraft architectures. Propulsion motors must simultaneously satisfy extreme performance specifications: high continuous power output, peak torque density, fault tolerance, and operation across wide thermal envelopes. These requirements translate into higher unit values, longer development cycles, and stronger OEM-supplier partnerships compared with flight control or environmental system motors.

The propulsion segment's share is actively growing rather than merely consolidating. This expansion is driven by the commercialization of electric vertical takeoff and landing (eVTOL) platforms, hybrid-electric turboprop retrofits, and fully electric commuter aircraft programs. The Urban Air Mobility Market, which encompasses eVTOL air taxis and autonomous urban cargo drones, is a particularly potent demand accelerator: each multi-rotor eVTOL platform requires between six and twelve independent propulsion motors, multiplying per-vehicle motor content relative to conventional single-engine designs.

MagniX Corporation has established a commanding position in high-power propulsion motors for commuter-class aircraft, having powered the first all-electric commercial aircraft flights and securing agreements with multiple regional carriers for electric retrofit programs. H3X Technologies Inc. has differentiated itself through a proprietary integrated motor-drive architecture that achieves unprecedented power density exceeding 9 kW/kg, directly addressing the thrust-to-weight constraints that historically limited electric propulsion to light aircraft categories. Wright Electric is focused on developing megawatt-class motors targeting single-aisle commercial jets, representing the next frontier of propulsion electrification.

The Brushless DC Motor Market is deeply intertwined with propulsion applications due to the superior efficiency, lower maintenance requirements, and electronic controllability that brushless designs offer over legacy brushed alternatives. Most contemporary propulsion motors for UAVs and eVTOLs utilize permanent magnet brushless architectures, and the Permanent Magnet Motor Market is accordingly experiencing heightened demand from aerospace propulsion procurement teams seeking compact, high-efficiency powerplants.

From a power output segmentation perspective, the 10–200 kW band dominates propulsion applications for general aviation, UAVs, and early-generation eVTOLs, while a nascent but rapidly growing segment of motors exceeding 200 kW is emerging for hybrid-electric regional aircraft. The up-to-10 kW segment, while lower in absolute revenue contribution, is growing rapidly in volume terms driven by the explosive expansion of commercial drone fleets for logistics, inspection, and surveillance missions.

Competition in the propulsion segment is intensifying as incumbent aerospace suppliers such as SAFRAN and Moog Inc. leverage their certification expertise and existing OEM relationships to enter a space that was previously dominated by startups. This convergence of established players with agile innovators is accelerating the pace of product development while compressing commercialization timelines. The segment is also witnessing growing interest in superconducting motor technologies, which promise order-of-magnitude improvements in power density but require cryogenic cooling systems that remain a key engineering and cost challenge.

Overall, the propulsion segment is expected to sustain its dominant position and capture an increasing share of total market revenue through the forecast period, particularly as eVTOL certification milestones are achieved and hybrid-electric retrofit programs for existing regional aircraft fleets scale beyond demonstration phases.

The Aircraft Electric Motor Market is shaped by a clearly defined set of quantifiable drivers and measurable constraints that determine investment flows, product development priorities, and go-to-market timelines.

Driver 1: Regulatory decarbonization mandates. The European Union's Fit for 55 package and the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) impose binding emission reduction obligations on airlines, creating procurement incentives for electric and hybrid-electric platforms that directly consume aircraft electric motors. IATA's commitment to net-zero carbon by 2050 affects over 300 member airlines representing 83% of total air traffic, translating into a multi-decade structural demand signal.

Driver 2: Military UAV proliferation. Global defense UAV spending exceeded $11 billion in 2023 and is projected to sustain double-digit growth through 2030, driven by NATO member force modernization and Indo-Pacific defense buildups. Each surveillance or combat UAV platform integrates multiple electric motors for propulsion, gimbal actuation, and payload management, creating high-volume procurement pipelines for motor manufacturers with MIL-SPEC certifications.

Driver 3: eVTOL commercialization timelines. Over 200 eVTOL concepts are in active development globally, with approximately 15 platforms targeting FAA or EASA type certification within the 2025–2027 window. Each certified platform entering serial production will require assured, high-volume motor supply chains, prompting long-term supply agreements and vertical integration moves by leading motor manufacturers.

Constraint 1: Certification complexity and cost. FAA Special Conditions for novel propulsion systems and EASA's nascent Special Condition VTOL framework impose extensive testing, documentation, and compliance expenditure that can add 18–36 months to product development cycles, delaying revenue generation and increasing capital consumption for startup motor suppliers.

Constraint 2: Rare earth material supply chain risk. Permanent magnet motors—the dominant architecture in aerospace propulsion—rely on neodymium and dysprosium sourced predominantly from China, which controls over 60% of global rare earth refining capacity. Supply disruptions or export controls represent a tangible cost and availability risk, particularly given the Aerospace and Defense Electronics Market's sensitivity to geopolitical supply chain disruptions.

Constraint 3: Thermal management limitations. High power density motors generate significant heat that must be dissipated within strict weight budgets. Current thermal management solutions impose design trade-offs that limit the operational duty cycles of propulsion motors, constraining their applicability in high-endurance commercial mission profiles.

Wright Electric: Focused on developing megawatt-scale electric motors targeting short-haul commercial jet electrification, Wright Electric has secured NASA funding and airline partnership agreements to accelerate its high-power motor and power electronics development program.

MGM COMPRO: A Czech Republic-based specialist in high-performance electric motors and controllers for aviation and motorsport applications, MGM COMPRO supplies brushless motors and ESCs to UAV manufacturers across Europe and North America with a reputation for ruggedized, high-efficiency designs.

Maxon: A Swiss precision drive systems manufacturer, Maxon supplies miniaturized high-torque DC and brushless motors widely used in flight control actuators, sensor platforms, and auxiliary aircraft systems, leveraging its space and medical heritage for aerospace certification compliance.

Moog Inc.: A global leader in precision motion control, Moog Inc. provides electric actuation systems and motor assemblies for flight control, landing gear, and thrust vector control applications across commercial, military, and space platforms, with deep FAA and MIL-SPEC certification expertise.

Woodward, Inc.: Specializing in energy control and optimization solutions for aerospace and industrial applications, Woodward, Inc. integrates electric motor systems within fuel management, engine control, and actuation subsystems, serving major airframe and engine OEM primes globally.

Ametek, Inc.: Through its aerospace and defense division, Ametek, Inc. manufactures precision motors and motion control assemblies for environmental control, flight instrument actuation, and auxiliary power applications, supported by a global MRO and aftermarket service network.

SAFRAN: A French aerospace and defense conglomerate, SAFRAN is investing heavily in hybrid-electric propulsion architectures through its SAFRAN Electrical & Power division, targeting both narrow-body retrofit programs and next-generation regional aircraft platforms.

EMRAX d.o.o.: A Slovenian manufacturer of advanced axial flux permanent magnet motors, EMRAX d.o.o. has become a preferred supplier for light aircraft and eVTOL propulsion programs due to its industry-leading power-to-weight ratios and compact form factors.

H3X Technologies Inc.: A U.S.-based deep-tech startup, H3X Technologies Inc. has developed an integrated motor-inverter architecture achieving 9 kW/kg continuous power density, positioning it as a key technology partner for next-generation eVTOL and hybrid-electric commuter aircraft OEMs.

MagniX Corporation: An Australian-American electric propulsion company, MagniX Corporation has demonstrated its magni250 and magni500 motors in record-setting electric flight demonstrations and is partnering with multiple aircraft OEMs for FAA-certified electric commuter aircraft programs.

January 2024: MagniX Corporation announced a production supply agreement with a regional aircraft OEM for the integration of its magni500 electric propulsion motor into a nine-passenger electric commuter aircraft targeting FAA Part 23 certification by 2026.

March 2024: H3X Technologies Inc. completed a successful ground demonstration of its HPDM-250 integrated motor-drive system at 250 kW continuous output, validating its proprietary integrated architecture for eVTOL propulsion applications and triggering a Series B funding round.

May 2024: SAFRAN's Electrical & Power division was selected as the electric motor and power distribution supplier for a major European hybrid-electric regional aircraft demonstrator program co-funded under the EU Clean Aviation Joint Undertaking initiative.

August 2024: The FAA published updated Special Conditions for electric propulsion systems under Part 33 regulations, providing clearer certification pathways for propulsion-grade aircraft electric motors and reducing regulatory uncertainty for market entrants.

October 2024: Wright Electric disclosed successful bench testing of a 1 MW electric motor prototype developed under a NASA Electrified Powertrain Flight Demonstration (EPFD) contract, marking a significant milestone toward single-aisle commercial aircraft electrification.

December 2024: EMRAX d.o.o. launched its EMRAX 348 motor variant with an upgraded thermal management system, increasing continuous power output by 15% without weight penalty, targeting light aircraft and advanced air mobility OEM customers.

February 2025: Moog Inc. entered a joint development agreement with a Tier 1 eVTOL manufacturer to co-develop a flight-control electric motor actuation system optimized for distributed electric propulsion architectures, slated for certification testing in 2026.

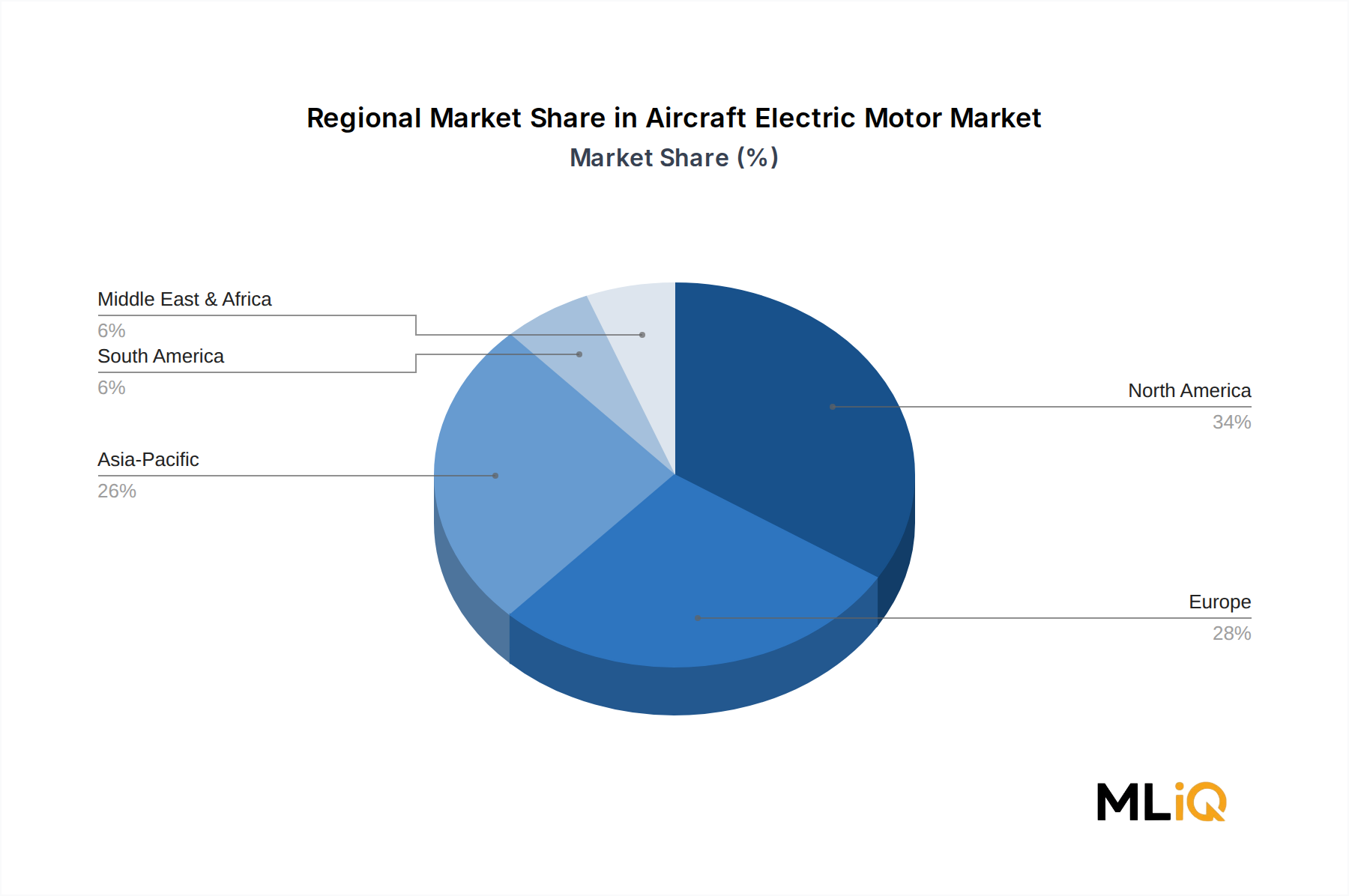

North America holds the largest revenue share of the Aircraft Electric Motor Market, accounting for an estimated 38–40% of global market value. The United States is the primary contributor, driven by robust Department of Defense UAV procurement, NASA-funded electrified propulsion research, and a dense ecosystem of eVTOL startups and electric aircraft OEMs concentrated in California, Washington, and Texas. Canada contributes through its regional aviation sector and growing investment in electric bush plane electrification. The region's CAGR is estimated at 8.2%, reflecting a mature base with steady incremental growth from new program launches.

Europe represents the second-largest regional market, with a revenue share of approximately 28–30% and a CAGR of 8.7%. The United Kingdom, Germany, and France collectively anchor European demand through Airbus's hybrid-electric demonstrator investments, Rolls-Royce's electrical systems division, and a well-funded network of aerospace SMEs. The European Union's Clean Aviation program has committed over €1.7 billion to sustainable aviation technology development through 2030, directly subsidizing aircraft electric motor R&D. The Power Electronics Market convergence with electric aviation is particularly advanced in Germany, where automotive electrification expertise is being transferred to aerospace motor design.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 10.1% through the forecast period. China's COMAC is developing hybrid-electric variants of its regional jet platforms, while Chinese eVTOL startups such as EHang and AutoFlight are scaling production of urban air mobility platforms requiring high-volume motor supply. India's civil aviation expansion, targeting 220 new airports by 2025, is creating infrastructure for electric regional aircraft operations. Japan and South Korea are investing in advanced air mobility infrastructure, with government-backed urban air mobility pilots scheduled in conjunction with major international events.

The Middle East and Africa region accounts for approximately 6–7% of global market revenue with a CAGR of 7.9%. Gulf state sovereign wealth fund investments in aviation infrastructure and growing interest in electric air taxi services for urban transport in Dubai and Riyadh are the primary demand catalysts. The Aerospace Actuator Market in this region is expanding alongside broader aerospace MRO hub development.

South America remains a smaller but steadily growing market, with Brazil leading regional adoption through Embraer's electric aircraft research programs and UAV procurement for border surveillance and agricultural applications. The region's CAGR is estimated at 7.4%, constrained by infrastructure limitations but supported by growing domestic aerospace manufacturing capabilities.

Environmental sustainability imperatives and ESG investor criteria are exerting profound, multi-layered pressure on the Aircraft Electric Motor Market, reshaping product design mandates, procurement specifications, and corporate strategy across the value chain.

From a regulatory standpoint, the EU's Corporate Sustainability Reporting Directive (CSRD) now requires large aerospace suppliers to disclose Scope 1, 2, and 3 greenhouse gas emissions, compelling motor manufacturers to conduct lifecycle assessments of their products and demonstrate measurable emission reductions over product generations. This has accelerated the adoption of low-carbon manufacturing processes, including renewable energy-powered production facilities and closed-loop rare earth material recycling programs.

The Electric

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.5% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Aircraft Electric Motor Market market expansion.

Key companies in the market include Wright Electric, MGM COMPRO, Maxon, Moog Inc., Woodward, Inc., Ametek, Inc., SAFRAN, EMRAX d.o.o., H3X Technologies Inc., MagniX Corporation.

The market segments include Type, Application, Output.

The market size is estimated to be USD 8270.45 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Aircraft Electric Motor Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Aircraft Electric Motor Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.