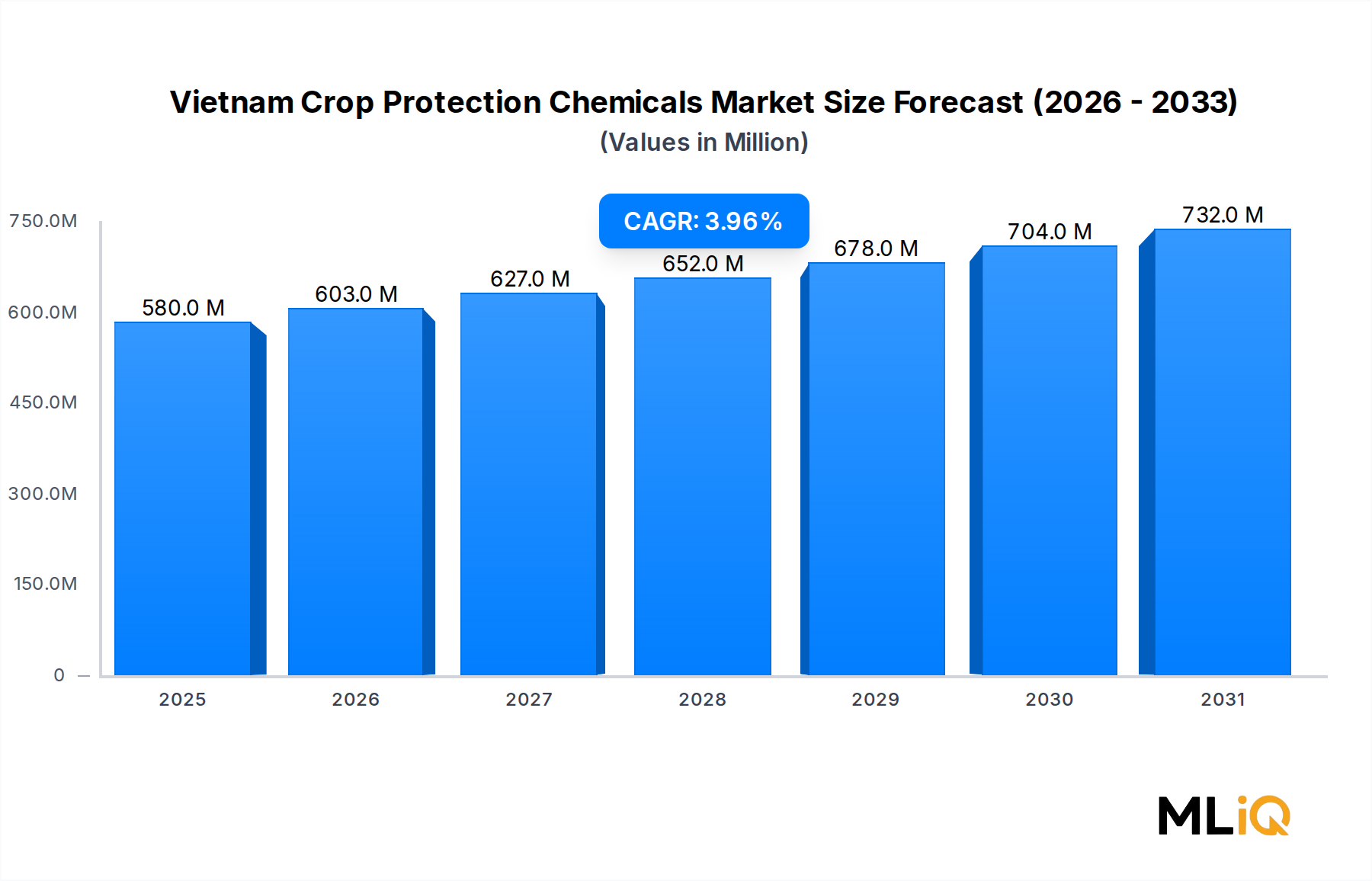

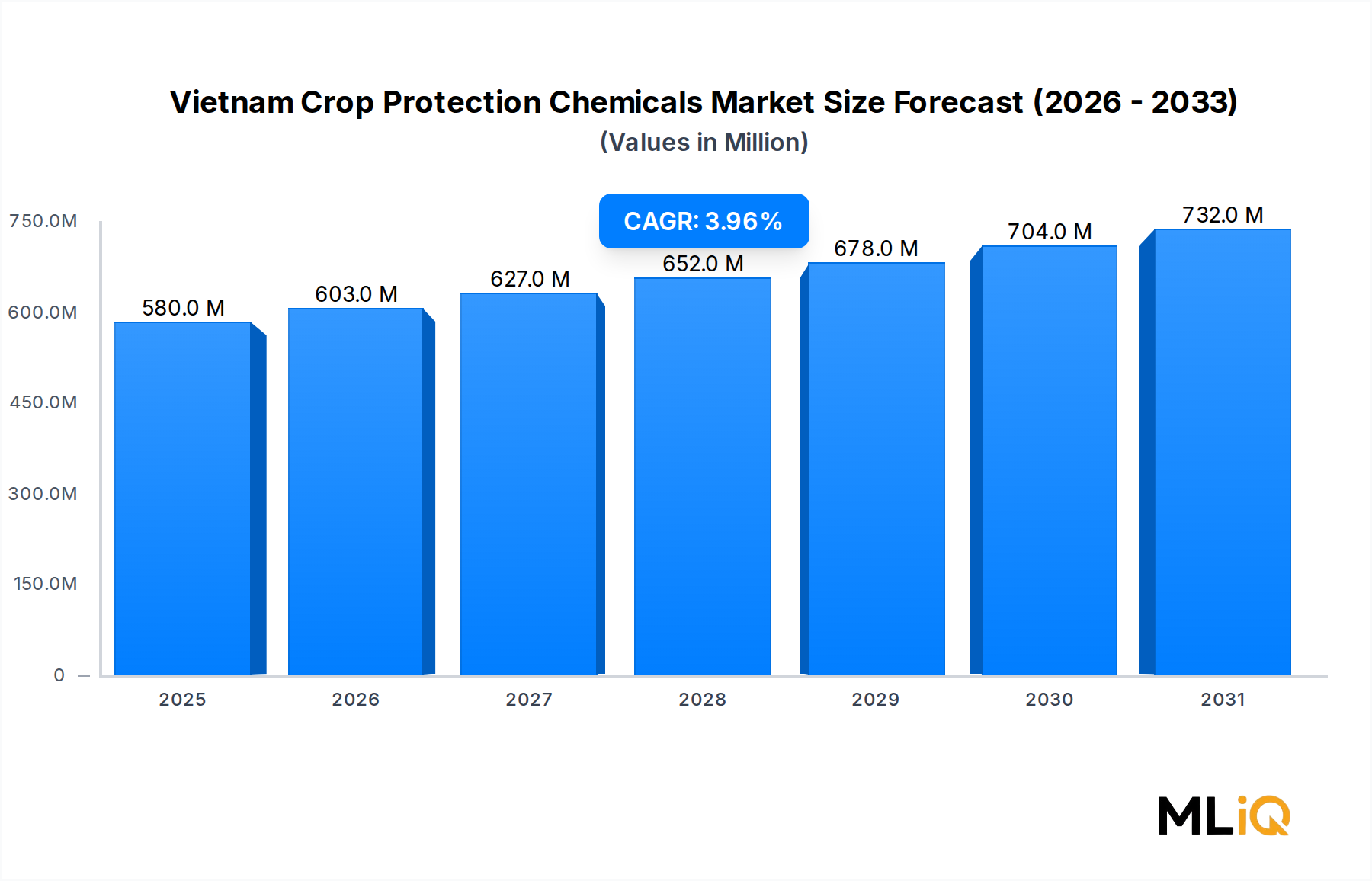

Dominance of the Insecticide Segment in the Vietnam Crop Protection Chemicals Market

Among all functional segments, the insecticide segment commands the largest revenue share within the Vietnam Crop Protection Chemicals Market, a dominance rooted in the country's agricultural composition, climate conditions, and cropping calendar. Vietnam's tropical and subtropical climate creates year-round conditions favorable to insect proliferation, making insecticide application a near-constant operational requirement for Vietnamese farmers across virtually all crop types.

Rice remains the anchor crop of Vietnam's agricultural economy, cultivated across approximately 7.3 million hectares annually, with three crop cycles per year in many delta regions. This intensive cultivation schedule creates continuous exposure windows for destructive pests including brown planthoppers (Nilaparvata lugens), stem borers (Chilo suppressalis), and leafhoppers, all of which cause significant yield losses without timely chemical intervention. The Insecticide Market thus derives its structural primacy from the sheer scale and frequency of rice pest management requirements.

Beyond rice, Vietnam's expanding horticulture sector — encompassing dragon fruit, vegetables, citrus, and coffee — adds additional layers of insecticide demand. Coffee berry borer (Hypothenemus hampei) management in the Central Highlands, and whitefly and aphid control in intensive vegetable cultivation zones near Ho Chi Minh City and Hanoi, represent high-value application niches where premium insecticide products command above-average price realization.

In terms of chemistry classes, organophosphates and pyrethroids continue to account for the majority of insecticide volumes by tonnage due to their cost-effectiveness and broad-spectrum activity. However, newer chemical classes — including diamides (chlorantraniliprole, flubendiamide), neonicotinoids, and spinosyns — are gaining share as resistance management concerns prompt farmers to rotate active ingredients. The diamide class in particular has witnessed rapid adoption given its favorable safety profile and selectivity toward target pests.

Key players actively competing within this segment include Syngenta Group, Bayer AG, Corteva Agriscience, and FMC Corporation, all of which have invested in localized formulation capabilities, distributor network expansion, and farmer education programs. Local and regional generics manufacturers, particularly from China and India, exert significant competitive pressure on pricing, especially in the commodity tier of the insecticide segment.

The insecticide segment's share within the broader Vietnam Crop Protection Chemicals Market shows signs of gradual consolidation rather than explosive growth. While absolute demand volumes remain robust, increasing regulatory scrutiny of certain active ingredients (notably chlorpyrifos and certain neonicotinoids) is creating category-level headwinds that are partially offsetting volumetric growth. This dynamic is simultaneously driving premiumization, as farmers seek safer yet efficacious alternatives.

Distribution channels play a critical role in insecticide segment dynamics. The country's estimated 30,000+ agrochemical retail points — ranging from large provincial distributors to village-level input shops — ensure broad product accessibility but also introduce counterfeit product risks, a challenge that leading multinational companies are addressing through track-and-trace technologies and authorized dealer programs.

Overall, the insecticide segment's dominance is structural and self-reinforcing: Vietnam's crop mix, climate profile, and farming intensity collectively guarantee sustained demand, while evolving resistance patterns and regulatory shifts create recurring opportunities for product innovation and portfolio renewal. The Seed Treatment Market is also growing as an adjacent delivery channel for insecticidal active ingredients, offering systemic protection from germination onward and reducing reliance on foliar spray applications.