1. What are the major growth drivers for the RF Mixers Market market?

Factors such as are projected to boost the RF Mixers Market market expansion.

+1 2315155523

RF Mixers Market

RF Mixers Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

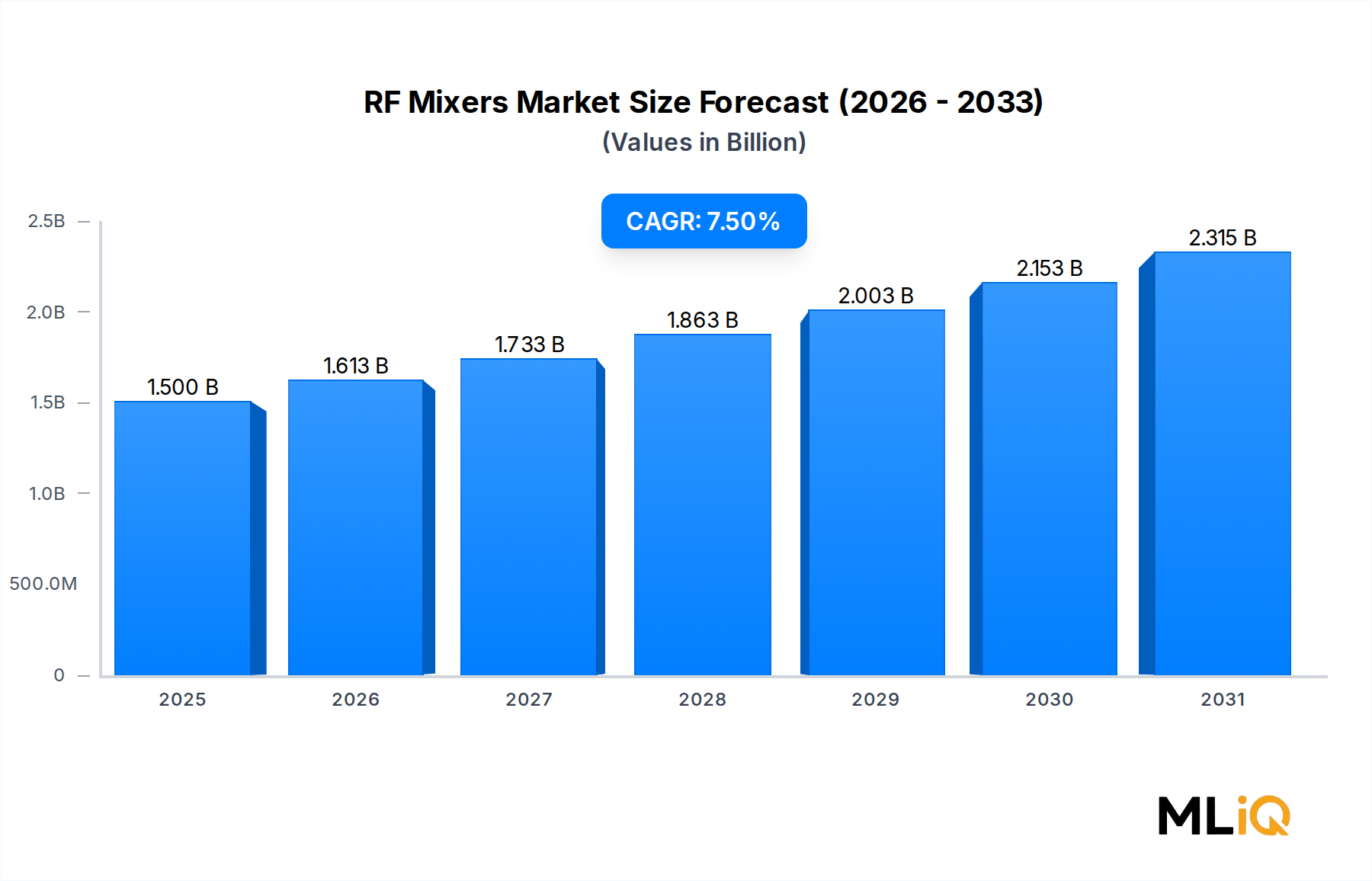

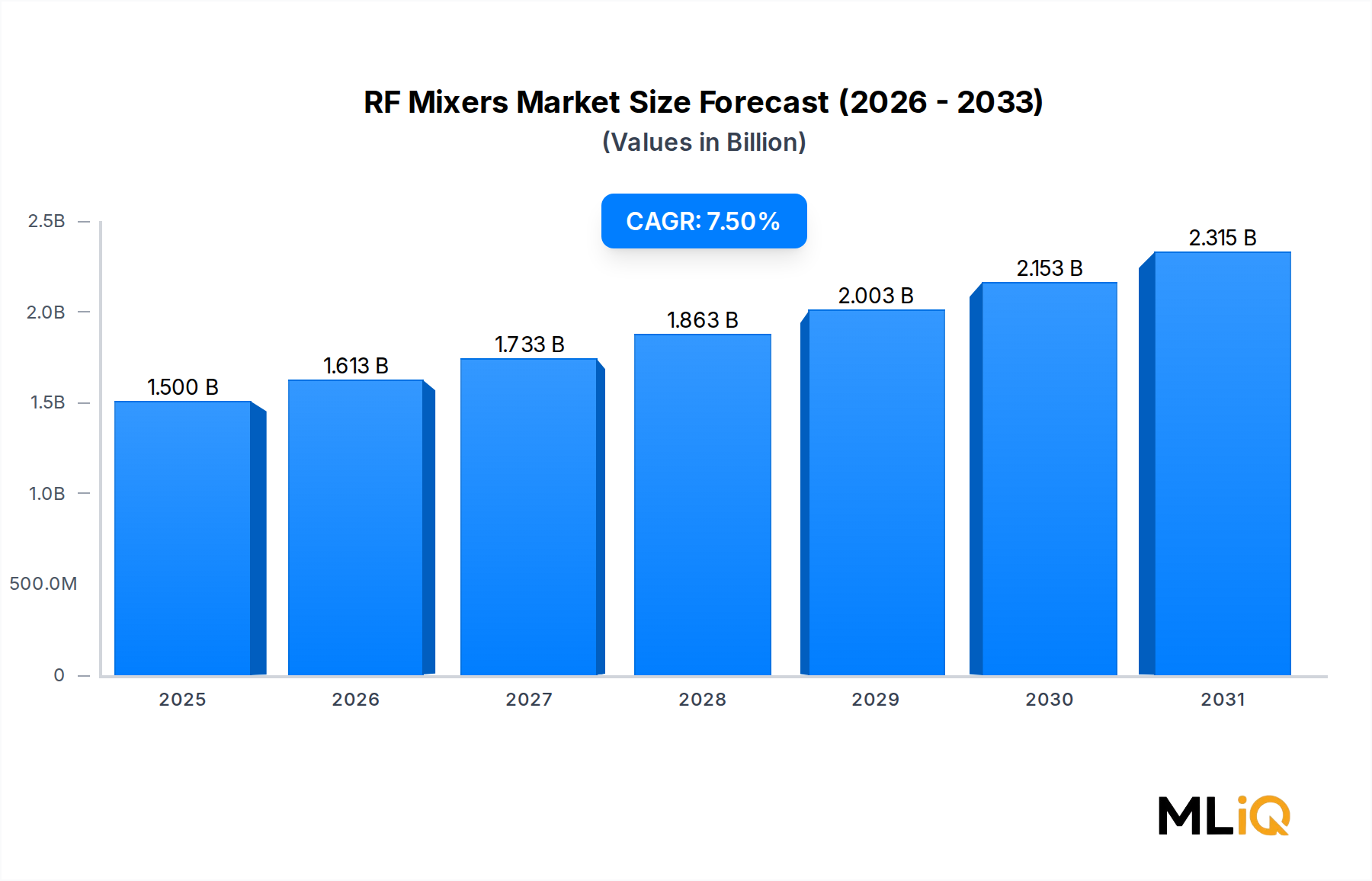

The global RF Mixers Market was valued at $1.5 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 7.5% through 2033, driven by accelerating deployment of next-generation wireless networks, growing defense electronics modernization programs, and surging demand for high-performance signal processing components across commercial and industrial verticals. By 2033, the market is expected to surpass $2.9 billion, reflecting robust structural demand across telecommunications, aerospace and defense, and broadband infrastructure sectors.

RF mixers serve as fundamental frequency-translation components in transceiver chains, converting radio-frequency signals from one frequency to another through nonlinear mixing of a local oscillator signal with an input RF signal. Their criticality in enabling frequency upconversion and downconversion makes them indispensable in virtually every wireless communication system, radar platform, electronic warfare suite, and satellite ground terminal deployed globally.

Key demand drivers include the rapid global rollout of 5G base station infrastructure, which requires high linearity, low noise figure mixers capable of operating across sub-6 GHz and millimeter-wave bands simultaneously. The increasing complexity of phased-array radar systems in defense platforms is further stimulating demand for broadband mixers with exceptional spurious-free dynamic range (SFDR) performance. Additionally, the proliferation of satellite communication terminals—particularly low earth orbit (LEO) constellations—is opening new high-volume procurement channels for passive and active mixer architectures.

Macro tailwinds include sustained government investment in defense modernization across North America and Europe, the emergence of private 5G networks in industrial automation environments, and the global expansion of fiber-to-the-node (FTTN) and cable broadband infrastructure requiring RF mixing stages at headend and customer premises equipment (CPE) nodes. The integration of RF mixers into monolithic microwave integrated circuits (MMICs) and system-on-chip (SoC) designs is also compressing form factors while improving power efficiency, making them more attractive for portable and space-constrained applications.

From a technology standpoint, the transition from silicon bipolar and GaAs MESFET process nodes toward advanced GaN and SiGe BiCMOS platforms is enabling mixers with higher operating frequencies, improved conversion efficiency, and tighter integration with adjacent RF chain elements. The convergence of these technology trends, combined with the secular growth of data-intensive wireless applications, positions the RF Mixers Market for sustained double-digit revenue expansion in several sub-segments through the forecast horizon.

Active mixers represent the dominant segment within the RF Mixers Market by revenue share, accounting for an estimated 55–60% of total market value in 2024. Their leadership position stems from a combination of conversion gain, port-to-port isolation advantages, and ease of integration into MMIC and integrated circuit architectures—attributes that passive designs fundamentally cannot replicate without external amplification stages.

Active mixers achieve frequency conversion through the transconductance nonlinearity of transistor-based switching or multiplying cores, typically implemented using differential Gilbert cell topologies in CMOS and BiCMOS processes, or via dual-gate MESFET/HEMT configurations in III-V compound semiconductor platforms. The inherent conversion gain—typically ranging from +3 dB to +12 dB depending on architecture and bias conditions—eliminates the need for a separate low-noise amplification stage ahead of the mixer in many receiver architectures, directly reducing system bill-of-materials cost and board space.

The sub-6 GHz active mixer segment is the most mature and highest-volume tier, anchored by demand from cellular base station transceivers, Wi-Fi 6/6E access points, and cable headend equipment. Here, linearity specifications—expressed as third-order intercept point (IP3)—are the primary competitive differentiator, with leading commercial devices from Texas Instruments and Analog Devices achieving input IP3 values exceeding +25 dBm while maintaining noise figures below 10 dB.

Millimeter-wave active mixers operating above 24 GHz constitute the fastest-growing sub-tier within the active segment, driven primarily by 5G NR FR2 band deployments and automotive radar applications in the 76–81 GHz automotive long-range radar band. These devices require advanced process nodes—typically 22 nm CMOS FD-SOI, 45 nm RF SOI, or 0.1 µm GaAs pHEMT—to achieve adequate transistor fT and fmax values for efficient mixing at millimeter-wave frequencies. Qorvo and Skyworks Solutions have made substantial foundry and design investments in this tier, with multiple wideband MMIC mixer products covering DC to 40 GHz and 6–40 GHz operating ranges respectively.

The active mixer segment's share is consolidating around vertically integrated semiconductor companies capable of offering full RF front-end chipset solutions rather than standalone mixer devices. Customers designing 5G massive MIMO radio units, electronic warfare receivers, and satellite modems increasingly procure integrated transmit/receive chains where the mixer function is embedded within a larger RFIC. This trend is compressing standalone active mixer revenue but expanding the total addressable market for companies offering integrated solutions.

Within industry verticals, telecommunications accounts for the largest consumption of active mixers, representing approximately 38% of segment revenue, followed by aerospace and defense at 28%, and entertainment/broadband infrastructure at 18%. Manufacturing and industrial automation applications—including wireless sensor networks operating in the 900 MHz and 2.4 GHz ISM bands—account for the remaining 16% and represent the highest-growth vertical by percentage, as private wireless network deployments accelerate across smart factory environments globally.

Key players reinforcing active mixer segment dominance include Texas Instruments with its LMX series broadband integrated synthesizer-mixer solutions, Analog Devices with its HMC-series GaAs MMIC mixers spanning DC–26 GHz, and Mini Circuits with its highly cost-competitive surface-mount active mixer catalog targeting commercial wireless infrastructure OEMs.

The RF Mixers Market is shaped by a set of quantifiable structural drivers offset by specific technological and supply-chain constraints that merit rigorous examination.

The foremost demand driver is the global 5G infrastructure buildout. According to industry deployment tracking, over 2 million 5G base stations were commercially operational globally as of late 2024, with the GSMA projecting cumulative 5G connections to exceed 5.9 billion by 2030. Each 5G NR radio unit contains between 4 and 64 mixer elements depending on antenna array configuration, translating to a direct and scalable unit demand multiplier for mixer suppliers.

Defense electronics modernization programs constitute the second major demand driver. The U.S. Department of Defense allocated over $145 billion toward research, development, testing, and evaluation in FY2024, with electronic warfare, radar modernization, and communications upgrades representing high-growth procurement categories. Active electronically scanned array (AESA) radar systems, which require wideband mixer arrays for simultaneous multi-beam operation, are a primary consumption vector.

The proliferation of LEO satellite constellations—with operators such as SpaceX Starlink, Amazon Kuiper, and OneWeb having collectively launched over 7,000 satellites by 2024—is creating demand for compact, radiation-tolerant mixer designs in both space and ground-segment equipment, further diversifying end-market exposure for leading suppliers.

On the constraint side, the transition to higher levels of RF integration—specifically the migration of mixer functions into large-scale RFICs and SoC devices—is reducing standalone mixer unit volumes even as RF system complexity grows. Additionally, export control regulations under the U.S. Export Administration Regulations (EAR) and ITAR classifications affect the international sale of high-performance military-grade mixer products, limiting addressable market size for the defense tier. Supply chain concentration risk around specialized III-V semiconductor foundries—primarily located in the United States, United Kingdom, and Taiwan—introduces procurement lead-time and pricing volatility for OEM customers.

The competitive landscape of the RF Mixers Market is characterized by a blend of diversified semiconductor giants, specialized RF component houses, and vertically integrated defense-focused suppliers. The following profiles capture the strategic positioning of leading participants:

Texas Instruments: A dominant force in the commercial RF and mixed-signal IC space, Texas Instruments leverages its broad CMOS and BiCMOS process portfolio to deliver cost-optimized active mixer solutions targeting wireless infrastructure, industrial IoT, and test-and-measurement applications. Its LMX series integrates PLL, VCO, and mixer functions, enabling single-chip signal chain simplification for OEM customers.

Qorvo: Qorvo occupies a leadership position in the GaN and GaAs MMIC mixer segment, with deep penetration into defense radar, electronic warfare, and 5G base station markets. The company's vertically integrated foundry capabilities—spanning GaN-on-SiC and GaAs pHEMT—provide a competitive moat in high-frequency, high-power mixer applications above 10 GHz.

Mini Circuits: Mini Circuits is the benchmark supplier for catalog RF/microwave component solutions, offering over 150 distinct mixer SKUs spanning coaxial, surface-mount, and MMIC form factors from DC to 65 GHz. Its cost-effective, high-volume production model makes it the preferred source for commercial wireless infrastructure and test equipment OEMs globally.

Skyworks Solutions: Skyworks focuses on highly integrated RF front-end modules and discrete mixer solutions for mobile handset, IoT, and broadband access infrastructure markets. Its strong position in the 5G handset supply chain provides stable, high-volume demand for its mixer-integrated front-end module products.

L-3 Narda-MITEQ: Specializing in high-performance RF and microwave subsystems for defense, satellite, and test applications, L-3 Narda-MITEQ provides precision mixer assemblies and subassemblies with stringent environmental and radiation-hardening qualifications demanded by aerospace customers.

Analog Devices: Analog Devices commands a premier position in the high-performance RF mixer segment through its HMC product line, which includes broadband GaAs MMIC mixers, image reject mixers, and IQ demodulators spanning frequencies up to 86 GHz. Its strength in test-and-measurement and phased-array radar channels is particularly noteworthy.

Marki Microwave: Marki Microwave is a specialist in ultra-broadband passive and active mixers serving the test-and-measurement, EW, and satellite communications sectors, with product coverage extending to 100 GHz and beyond using proprietary GaAs MMIC processes.

Peregrine Semiconductor: A subsidiary of Murata Manufacturing, Peregrine Semiconductor focuses on UltraCMOS SOI-based RF switches and mixers targeting IoT, wireless infrastructure, and medical device markets, with a strong emphasis on integration density and ultra-low power operation.

NXP Semiconductors: NXP brings significant scale and automotive-grade qualification to the mixer market, particularly in the 76–81 GHz automotive radar band, where its RFCMOS-based radar transceiver SoCs incorporate fully integrated mixer architectures alongside ADC, DAC, and DSP functions.

January 2024: Analog Devices announced production release of its HMC-series wideband IQ mixer covering 6–18 GHz with integrated LO buffer amplifier, targeting next-generation electronic warfare receiver designs requiring compact, high-dynamic-range downconversion.

March 2024: Qorvo introduced a GaN-on-SiC broadband double-balanced mixer MMIC rated for operation from 2 to 30 GHz, achieving an input IP3 of +38 dBm at X-band, specifically targeting active electronically scanned array radar upgrade programs under U.S. defense procurement frameworks.

May 2024: Mini Circuits expanded its surface-mount MMIC mixer catalog with eight new devices optimized for 5G NR FR1 band transceiver applications in the 3.3–4.2 GHz and 4.4–5.0 GHz frequency ranges, with conversion loss below 7 dB and LO-to-RF isolation exceeding 35 dB.

August 2024: NXP Semiconductors achieved automotive safety integrity level (ASIL-B) qualification for its RFCMOS radar transceiver SoC incorporating integrated mixer chains, enabling series production deployment in Level 3 autonomous vehicle programs across three major Tier-1 automotive suppliers.

October 2024: Texas Instruments released a new family of wideband direct-conversion mixers targeting O-RAN distributed unit (DU) radio implementations, with integrated LO path and compatibility with the open fronthaul interface standard, simplifying adoption by white-box radio unit manufacturers.

December 2024: Skyworks Solutions disclosed a strategic technology licensing agreement with a leading Asian OSAT provider to enable volume packaging of its flip-chip GaAs mixer MMICs in panel-level fan-out wafer-level packages, targeting cost reduction for mass-market 5G CPE applications.

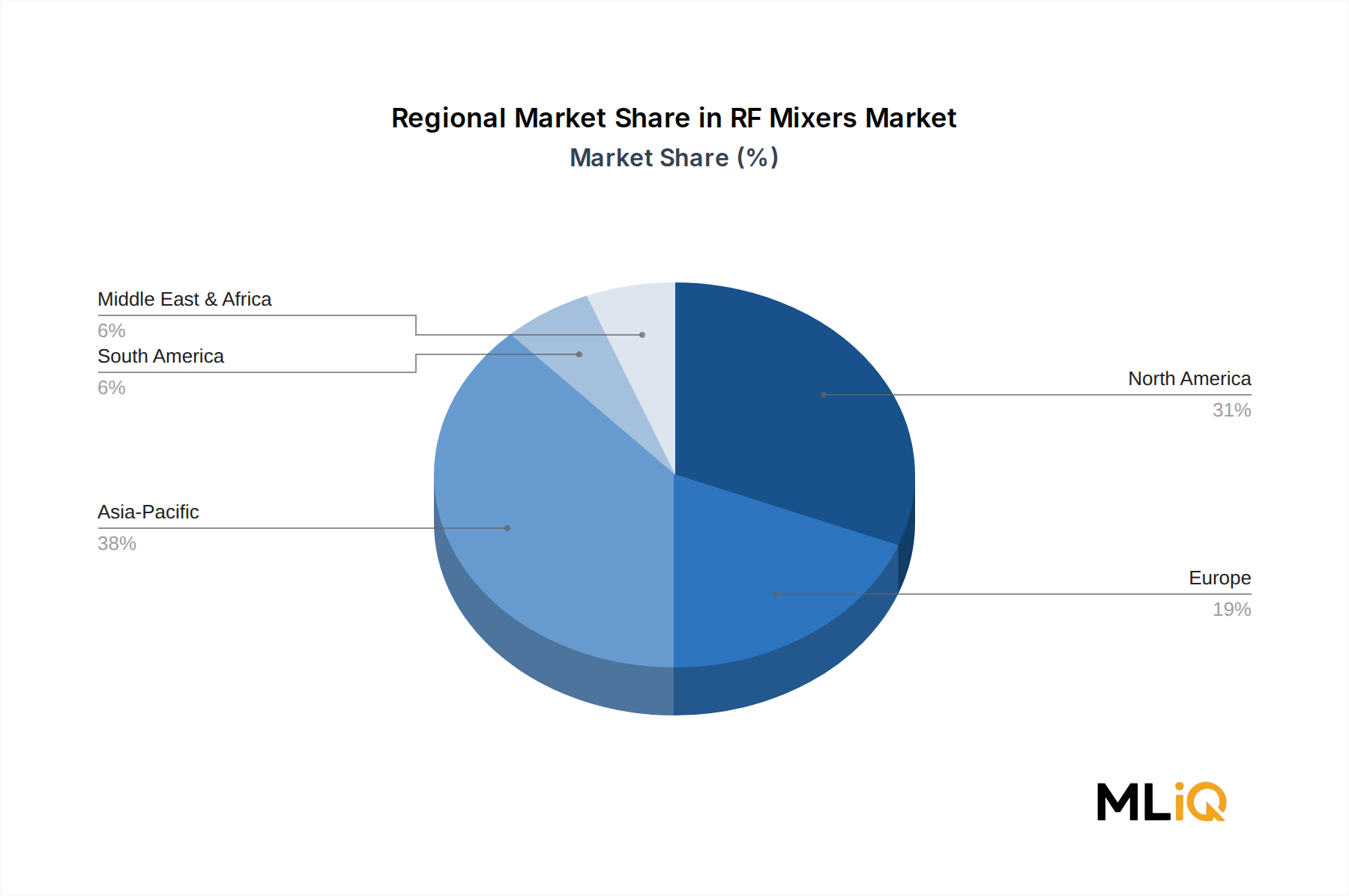

The RF Mixers Market exhibits distinct regional demand profiles driven by divergent technology adoption rates, defense spending patterns, and telecommunications infrastructure investment cycles.

North America remains the most mature and highest-revenue region, accounting for approximately 34% of global market value in 2024, equivalent to roughly $510 million. The United States is the primary contributor, underpinned by defense electronics procurement through programs administered by DARPA, the U.S. Army, Navy, and Air Force, as well as large-scale 5G infrastructure investments by major carriers. The regional CAGR is estimated at 6.2% through 2033, reflecting a mature but steadily growing market driven by defense modernization and mmWave 5G densification.

Asia Pacific is the fastest-growing region with a projected CAGR of 9.1% through 2033, driven by China's domestic 5G buildout—where over 3.3 million 5G base stations were installed by end-2024—alongside aggressive telecommunications infrastructure investment in India, South Korea, and Japan. China's government-mandated expansion of domestic semiconductor capabilities is stimulating local RF mixer IC development, while South Korea and Japan contribute through advanced consumer electronics and automotive radar programs. Asia Pacific held approximately 31% of global market share in 2024.

Europe accounted for roughly 22% of global revenue in 2024, with Germany, the United Kingdom, and France as the primary consumption centers. European demand is bifurcated between defense-related procurement—particularly from NATO-aligned modernization programs—and commercial 5G infrastructure, where mid-band spectrum auction completions in Germany and France are accelerating active radio unit deployments requiring high-performance mixer components. The regional CAGR is estimated at 6.8% through 2033.

The Middle East and Africa region, while representing only 7% of market value in 2024, is growing at an estimated 8.3% CAGR driven by satellite ground-station infrastructure investments in Gulf Cooperation Council (GCC) states and defense electronics procurement by Israel and Saudi Arabia.

South America accounts for the remaining 6%, with Brazil as the dominant market driven by ongoing 4G capacity expansion and early 5G deployments in major metropolitan areas.

Three disruptive technology vectors are fundamentally reshaping the RF Mixers Market and will determine competitive positioning through the 2025–2033 forecast window.

The first and most impactful is the adoption of GaN-on-silicon (GaN-on-Si) process technology for mixer fabrication. While GaN-on-SiC currently dominates high-power defense mixer applications, GaN-on-Si promises cost parity with GaAs within a 6–8 year horizon by enabling fabrication

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.5% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the RF Mixers Market market expansion.

Key companies in the market include Texas Instruments, Qorvo, Mini Circuits, Skyworks Solutions, L-3 Narda-MITEQ, Analog Devices, Marki Microwave, Peregrine Semiconductor, Mecury, NXP Semiconductors.

The market segments include Type, Application, Industry Vertical.

The market size is estimated to be USD 1.5 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "RF Mixers Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the RF Mixers Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.