1. What are the major growth drivers for the CoolMOS IC Market market?

Factors such as are projected to boost the CoolMOS IC Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

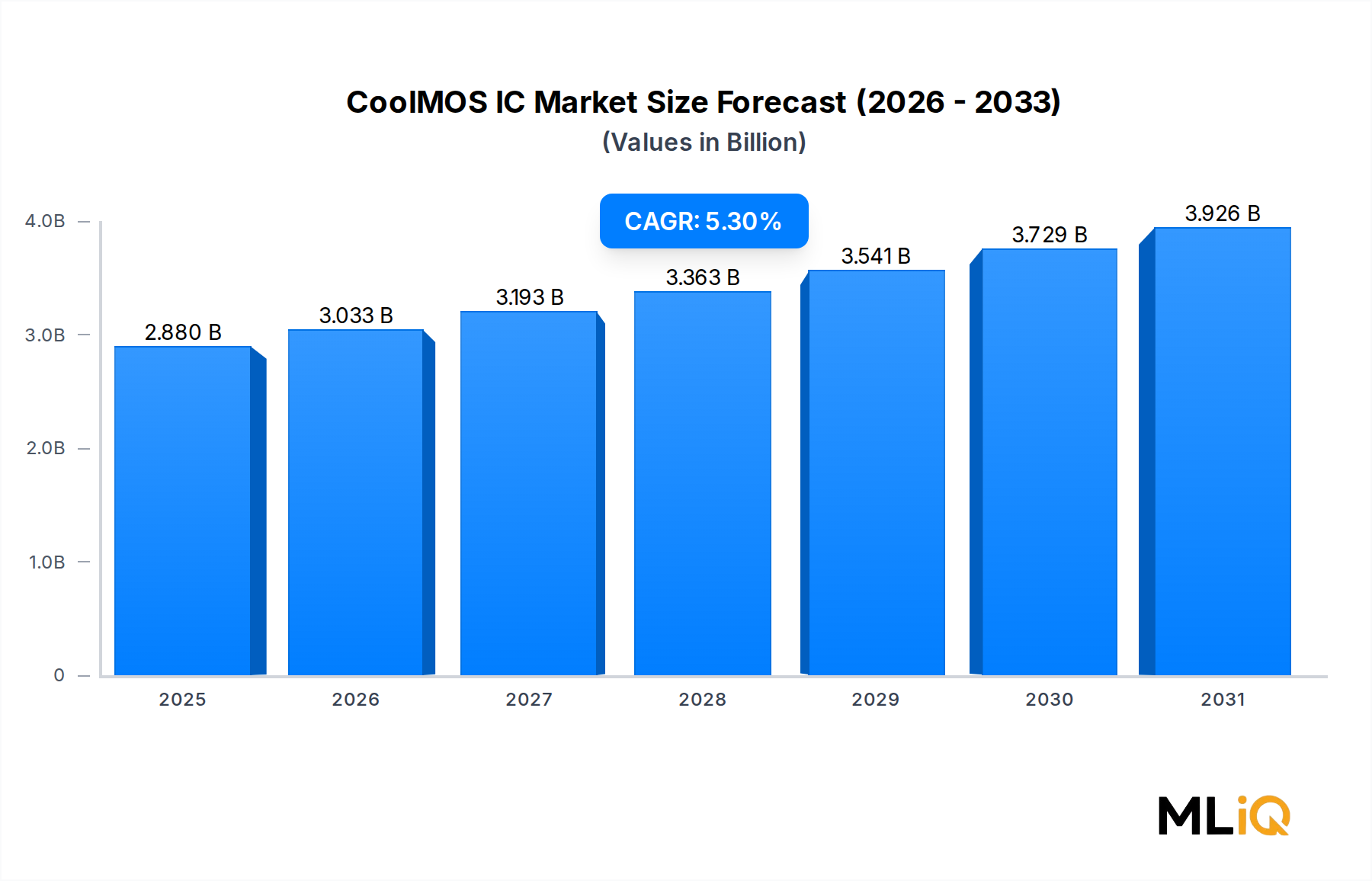

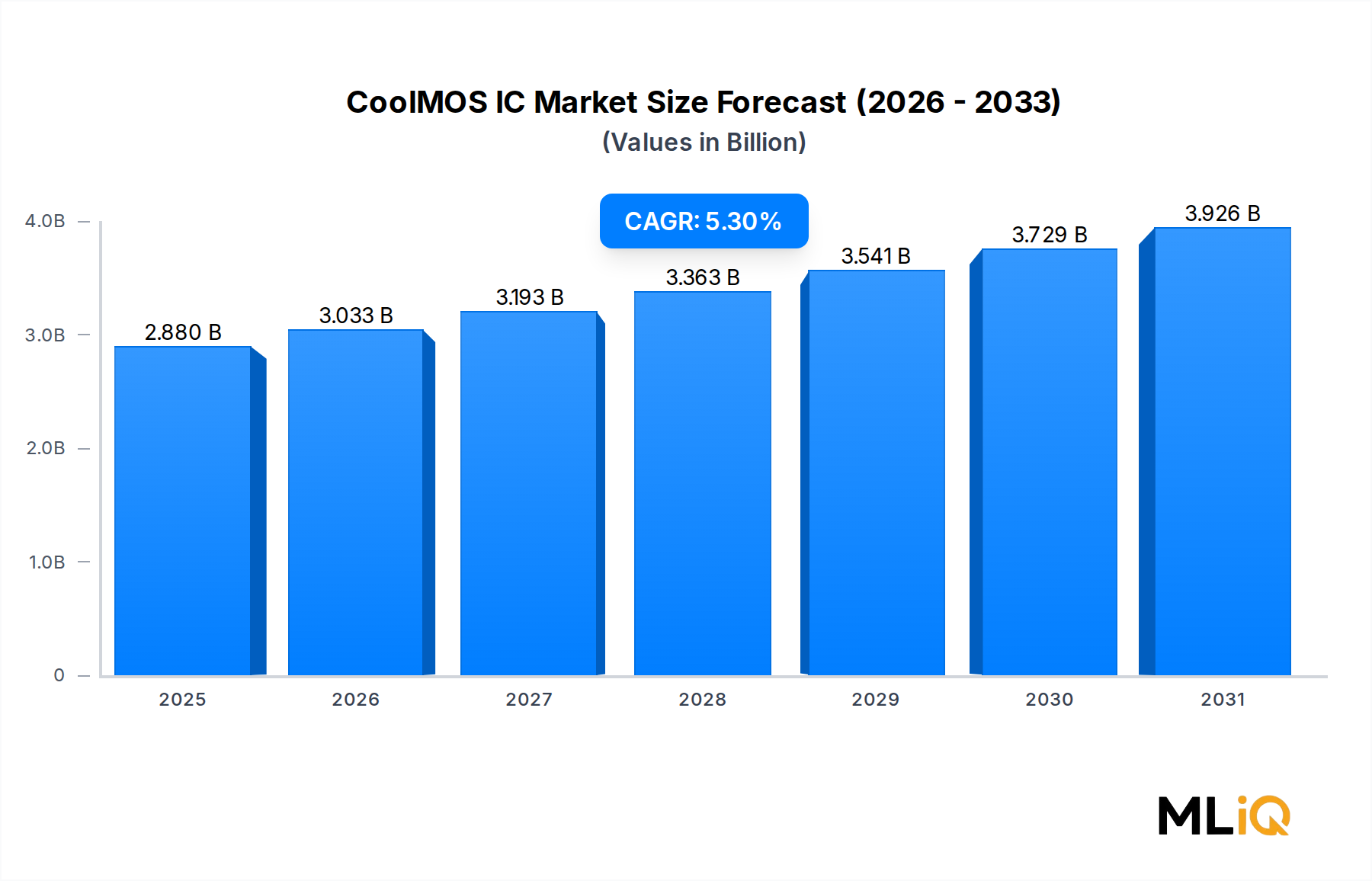

The global CoolMOS IC Market is valued at $2.88 billion as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 5.3% through the forecast window of 2025 to 2033. This trajectory reflects robust structural demand across power-sensitive verticals including automotive electrification, industrial automation, telecommunications infrastructure, and high-efficiency consumer electronics. CoolMOS devices, engineered by combining superjunction architecture with advanced silicon process nodes, deliver significantly lower on-state resistance (RDS(on)) per unit area compared to conventional planar MOSFETs, making them indispensable in high-frequency, high-efficiency switching applications.

Macro tailwinds reinforcing market growth include the global pivot toward energy efficiency regulations—particularly the European Union's Ecodesign Directive and the U.S. Department of Energy's efficiency mandates for power supplies—which are driving design engineers to adopt superjunction MOSFET solutions at an accelerated pace. The proliferation of electric vehicles (EVs) and hybrid electric vehicles (HEVs) is creating substantial demand for high-voltage, low-loss switching components capable of managing battery management system (BMS) loads, onboard chargers (OBCs), and DC-DC converters. Similarly, expanding 5G base station deployments require power amplifier and rectifier stages with superior switching efficiency, where CoolMOS ICs provide a competitive edge.

On the supply side, leading integrated device manufacturers (IDMs) such as Infineon Technologies AG, STMicroelectronics, and ON Semiconductor Corporation are investing heavily in 300mm wafer fab capacity and advanced superjunction process nodes to reduce cost per die and improve performance metrics. These investments are expected to support margin expansion even as average selling prices trend modestly downward due to competitive intensity.

From a segmentation perspective, the surface-mount technology (SMT) package format is gaining share over through-hole configurations, driven by the miniaturization requirements of modern power conversion platforms. Automotive and industrial end-use segments collectively account for the majority of revenue, with consumer electronics and telecommunications serving as incremental growth contributors.

Geographically, Asia Pacific dominates volume consumption, underpinned by China's massive electronics manufacturing base and India's rapidly expanding automotive OEM ecosystem. North America and Europe represent premium-value markets where design-in cycles are longer but average selling prices are higher due to stringent qualification requirements.

Looking forward through 2033, the CoolMOS IC Market is positioned to benefit from the convergence of electrification, digitalization, and sustainability mandates, creating a durable, multi-decade demand platform for high-performance superjunction power semiconductor solutions.

Within the CoolMOS IC Market, the surface-mount (SMT) sub-segment has emerged as the structurally dominant package format by revenue share, eclipsing through-hole configurations across the majority of end-use verticals. This dominance is attributable to a confluence of design, manufacturing, and performance factors that collectively make SMT the preferred interface between CoolMOS die and printed circuit board (PCB) assemblies in modern power electronics.

The primary driver of SMT dominance is the relentless miniaturization pressure in power conversion design. Designers of server power supply units (PSUs), telecom rectifiers, EV onboard chargers, and industrial variable frequency drives (VFDs) consistently prioritize board space efficiency, and SMT packages—including D2PAK, DPAK, TO-252, and PowerPAK formats—enable higher component density compared to leaded through-hole alternatives such as TO-220 or TO-247. In high-power-density applications targeting power density figures exceeding 10 W/cm³, SMT CoolMOS devices allow tighter component placement and reduced parasitic inductance in switching loops, directly improving electromagnetic interference (EMI) performance and switching loss.

Automated surface-mount assembly lines also deliver superior throughput and consistency relative to through-hole insertion processes, reducing manufacturing cost per board and enabling scalable production for high-volume consumer and automotive applications. The automotive segment, which increasingly demands AEC-Q101-qualified components in compact mechatronic modules, has been a particular accelerant for SMT CoolMOS adoption. Power modules for EV auxiliary systems, including power steering, braking assist, and HVAC compressors, predominantly utilize SMT superjunction MOSFETs due to thermal management integration requirements.

Key players capturing the largest share within the SMT CoolMOS segment include Infineon Technologies AG, which pioneered the CoolMOS brand and continues to maintain the broadest portfolio of surface-mount superjunction MOSFETs spanning voltage classes from 200V to 900V. STMicroelectronics competes aggressively with its MDmesh series in SMT formats, while ON Semiconductor Corporation has expanded its FAR series targeting server and telecom applications. ROHM Semiconductor and Toshiba are notable challengers in the Asia-centric supply chain, offering competitive SMT portfolios with differentiated gate charge (Qg) optimization.

Market share consolidation within the SMT segment is ongoing but not yet complete. The top three vendors—Infineon Technologies AG, STMicroelectronics, and ON Semiconductor Corporation—collectively hold an estimated 55–60% of SMT CoolMOS revenue, with the remainder fragmented across Toshiba, Vishay Intertechnology Inc., ROHM Semiconductor, and regional Chinese suppliers that are gradually improving process quality to penetrate industrial and consumer tiers.

Through-hole configurations retain meaningful relevance in retrofit industrial applications, legacy power supply designs, and markets where manual assembly or wave soldering remains cost-effective—notably in repair and maintenance segments across developing economies. However, the long-term structural trend clearly favors SMT, and new design starts overwhelmingly specify surface-mount CoolMOS variants. As wafer-level chip-scale packaging (WLCSP) and clip-bonded SMT formats mature, the performance gap relative to through-hole packages in thermal resistance (RθJC) is narrowing, further reinforcing SMT's trajectory toward near-total dominance in new design activity by 2030.

The CoolMOS IC Market is shaped by a set of quantifiable drivers and identifiable constraints that define its growth trajectory through 2033.

Driver 1 — Energy Efficiency Regulatory Mandates: The EU Ecodesign Regulation requires external power supplies and server PSUs to meet efficiency levels of 92% or higher under the ErP Lot 6 framework, directly mandating adoption of low-loss switching semiconductors. The 80 PLUS Titanium certification for data center PSUs, requiring 96% efficiency at 50% load, similarly necessitates CoolMOS-class devices. These mandates are non-negotiable for market access across the EU and increasingly influence procurement specifications globally.

Driver 2 — EV and Hybrid Vehicle Electrification: Global EV sales surpassed 10 million units annually and continue on an upward trajectory. Each EV platform incorporates multiple CoolMOS application nodes including OBCs rated at 3.3 kW to 22 kW, DC-DC converters, and BMS switching stages. As OBC power levels increase, the demand for high-voltage (650V–900V) CoolMOS variants with ultra-low RDS(on) intensifies correspondingly.

Driver 3 — 5G Infrastructure Rollout: Global 5G base station installations, projected to exceed 7 million cumulative units by 2027, require efficient power conversion at the radio unit and baseband unit levels. CoolMOS ICs are preferred in the rectifier and power factor correction (PFC) stages of these systems due to their low switching losses at frequencies above 100 kHz.

Constraint 1 — Competition from Wide Bandgap Semiconductors: Silicon carbide (SiC) MOSFETs and gallium nitride (GaN) HEMTs are increasingly displacing silicon-based CoolMOS in applications above 650V and above 100 kHz switching frequency. As SiC device pricing declines—with leading suppliers targeting price parity with premium silicon CoolMOS at roughly $1–$2 per ampere of current rating—the addressable market for silicon superjunction devices faces gradual compression at the high-performance frontier.

Constraint 2 — Geopolitical Supply Chain Risk: Concentration of advanced semiconductor fabrication capacity in Taiwan and South Korea introduces supply continuity risk, particularly for fabless and fab-lite CoolMOS suppliers dependent on TSMC and Samsung foundry services. This constraint contributed to lead time extensions of 26–52 weeks during the 2021–2022 semiconductor shortage, creating inventory distortions that suppressed demand in 2023.

The competitive landscape of the CoolMOS IC Market is characterized by a mix of global IDMs with proprietary superjunction process technology and specialized power semiconductor companies competing on performance, breadth of portfolio, and application-specific optimization.

Infineon Technologies AG: The originator of the CoolMOS brand, Infineon maintains the most extensive superjunction MOSFET portfolio globally, spanning voltage classes from 200V to 900V and covering automotive-grade, industrial, and consumer tiers. Its CoolMOS CFD7 and P7 series represent the current state of the art in low gate charge and low switching loss.

STMicroelectronics: STMicroelectronics competes with its MDmesh DM6 and K6 superjunction series, targeting server power supplies and solar inverter applications with differentiated body diode recovery characteristics optimized for hard-switching topologies.

Vishay Intertechnology Inc.: Vishay Intertechnology Inc. offers a broad catalog of superjunction MOSFETs spanning industrial and consumer power supply applications, leveraging its extensive global distribution network to serve Tier 2 and Tier 3 OEM customers.

Texas Instruments: Texas Instruments approaches the CoolMOS-adjacent market primarily through its GaN and silicon FET power stage solutions, integrating gate drivers with MOSFET switches to deliver system-level efficiency gains for telecom and computing applications.

ON Semiconductor Corporation: ON Semiconductor Corporation markets its FAR series superjunction MOSFETs with a focus on high-frequency PFC stages in server and telecom PSUs, competing directly with Infineon and STMicroelectronics on gate charge figures of merit.

ROHM Semiconductor: ROHM Semiconductor has invested in proprietary trench superjunction architecture to deliver competitive RDS(on) area products for the Asia-Pacific consumer and industrial markets, with particular strength in Japanese OEM supply chains.

Renesas Electronics: Renesas Electronics targets automotive and industrial power management applications, combining superjunction MOSFET expertise with integrated gate driver and protection circuitry to offer system-level solutions.

Toshiba: Toshiba's DTMOS and U-MOSIX series compete in the mid-tier industrial and consumer power supply segments, with manufacturing anchored in its proprietary fine-trench process technology developed at Japanese fabs.

Mitsubishi Electric Corporation: Mitsubishi Electric Corporation maintains a focused position in high-power industrial and railway traction applications, where its superjunction MOSFET modules serve as switching elements in multi-kilowatt converter systems.

NXP Semiconductors: NXP Semiconductors participates in the CoolMOS ecosystem through automotive-qualified power management ICs that incorporate superjunction switching stages, targeting body electronics and powertrain control applications in passenger vehicles.

January 2024: Infineon Technologies AG announced the commercial release of its CoolMOS CFD7A series, featuring a 25% reduction in effective output capacitance (Coss) compared to the prior generation, targeting high-frequency LLC resonant converter designs in data center applications.

March 2024: STMicroelectronics expanded its MDmesh K6 series with new 800V variants qualified to AEC-Q101 automotive standards, addressing the growing demand for high-voltage switching in EV onboard charging systems.

June 2023: ON Semiconductor Corporation completed the acquisition of additional 300mm fab capacity through its agreement with GLOBALFOUNDRIES, enabling incremental wafer starts dedicated to advanced power semiconductor processes including superjunction MOSFET production.

September 2023: ROHM Semiconductor unveiled a new 650V CoolMOS-class device with integrated gate resistor technology, reducing external component count in industrial motor drive reference designs by approximately 15%.

November 2023: The International Electrotechnical Commission (IEC) published updated efficiency benchmarks under IEC 62368-1 for audio/video and IT equipment power supplies, further tightening efficiency thresholds that incentivize CoolMOS adoption in consumer electronics power stages.

February 2025: Vishay Intertechnology Inc. launched a new through-hole CoolMOS-class product family targeting industrial UPS and solar edge inverter applications, with RDS(on) specifications competitive with leading SMT alternatives in the 500V class segment.

April 2025: Toshiba announced a strategic partnership with a Tier 1 European automotive supplier to co-develop next-generation superjunction MOSFET modules for 800V EV powertrain architectures, scheduled for production validation by 2027.

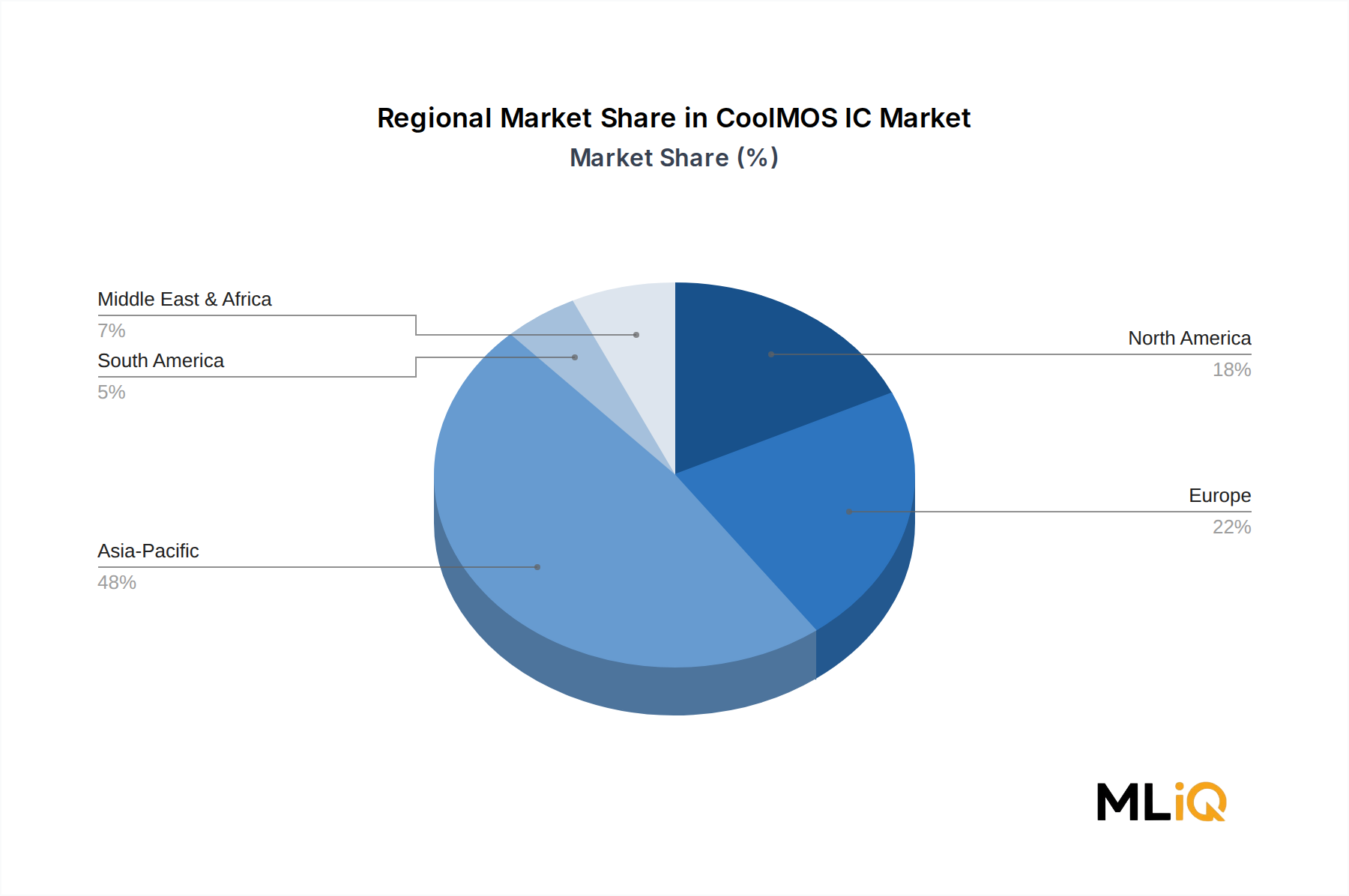

The CoolMOS IC Market exhibits distinct regional demand profiles driven by end-use industry concentration, regulatory environment, and manufacturing ecosystem maturity.

Asia Pacific is the dominant region by volume and absolute revenue, accounting for an estimated 42–45% of global CoolMOS IC Market value. China alone contributes the largest single-country share, driven by its massive consumer electronics manufacturing base, rapidly expanding EV production capacity, and domestic solar inverter industry. The region is also the fastest-growing, with an estimated regional CAGR of 6.8% through 2033, fueled by India's electronics manufacturing incentive schemes under the Production-Linked Incentive (PLI) program and Southeast Asia's expanding power electronics supply chain. Japan and South Korea contribute high-value demand through automotive and industrial automation OEMs.

Europe represents the most mature market in terms of technology sophistication, accounting for approximately 24–26% of global market value. Germany, the United Kingdom, France, and the Benelux region are primary demand centers, driven by industrial automation investment, automotive electrification (BMW, Mercedes-Benz, Volkswagen Group), and stringent EU Ecodesign efficiency mandates. European regional CAGR is estimated at 4.8%, reflecting a more saturated but premium-priced demand profile. The Nordics contribute incrementally through renewable energy inverter applications.

North America holds approximately 20–22% of global CoolMOS IC Market revenue, with the United States as the primary demand anchor. Data center construction activity, EV charging infrastructure deployment under the Infrastructure Investment and Jobs Act, and defense electronics modernization programs are the principal drivers. Canada and Mexico contribute modestly through automotive manufacturing supply chains tied to the broader USMCA region. North American CAGR is estimated at 5.1%.

Middle East and Africa represents an emerging growth pocket, with GCC nations investing in solar power infrastructure and Turkey hosting a growing electronics manufacturing sector. Regional CAGR is estimated at 5.6%, though the absolute base remains small at approximately 4–5% of global market value.

South America accounts for the smallest share at approximately 3–4% of global revenue, with Brazil as the dominant market driven by industrial motor drives and consumer electronics. Regional growth is constrained by macroeconomic volatility and limited local semiconductor ecosystem development, with an estimated CAGR of 4.2% through 2033.

Average selling prices (ASPs) in the CoolMOS IC Market have followed a structurally declining trend over the long run, with discrete price reductions of 3–6% annually in competitive voltage

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.3% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the CoolMOS IC Market market expansion.

Key companies in the market include Vishay Intertechnology Inc., Infineon Technologies AG, STMicroelectronics, Vishay Intertechnology Inc., Texas Instruments, ON Semiconductor Corporation, ROHM Semiconductor, Renesas Electronics, Toshiba, STMicroelectronics, Infineon Technologies AG, Toshiba, Mitsubishi Electric Corporation, NXP Semiconductors, Texas Instruments, Mitsubishi Electric Corporation, Renesas Electronics, ON Semiconductor Corporation, ROHM Semiconductor, NXP Semiconductors.

The market segments include Type, End User.

The market size is estimated to be USD 2.88 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4155, and USD 6960 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "CoolMOS IC Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the CoolMOS IC Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.