1. What are the major growth drivers for the Non-Contact Infrared Thermometer Market market?

Factors such as are projected to boost the Non-Contact Infrared Thermometer Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

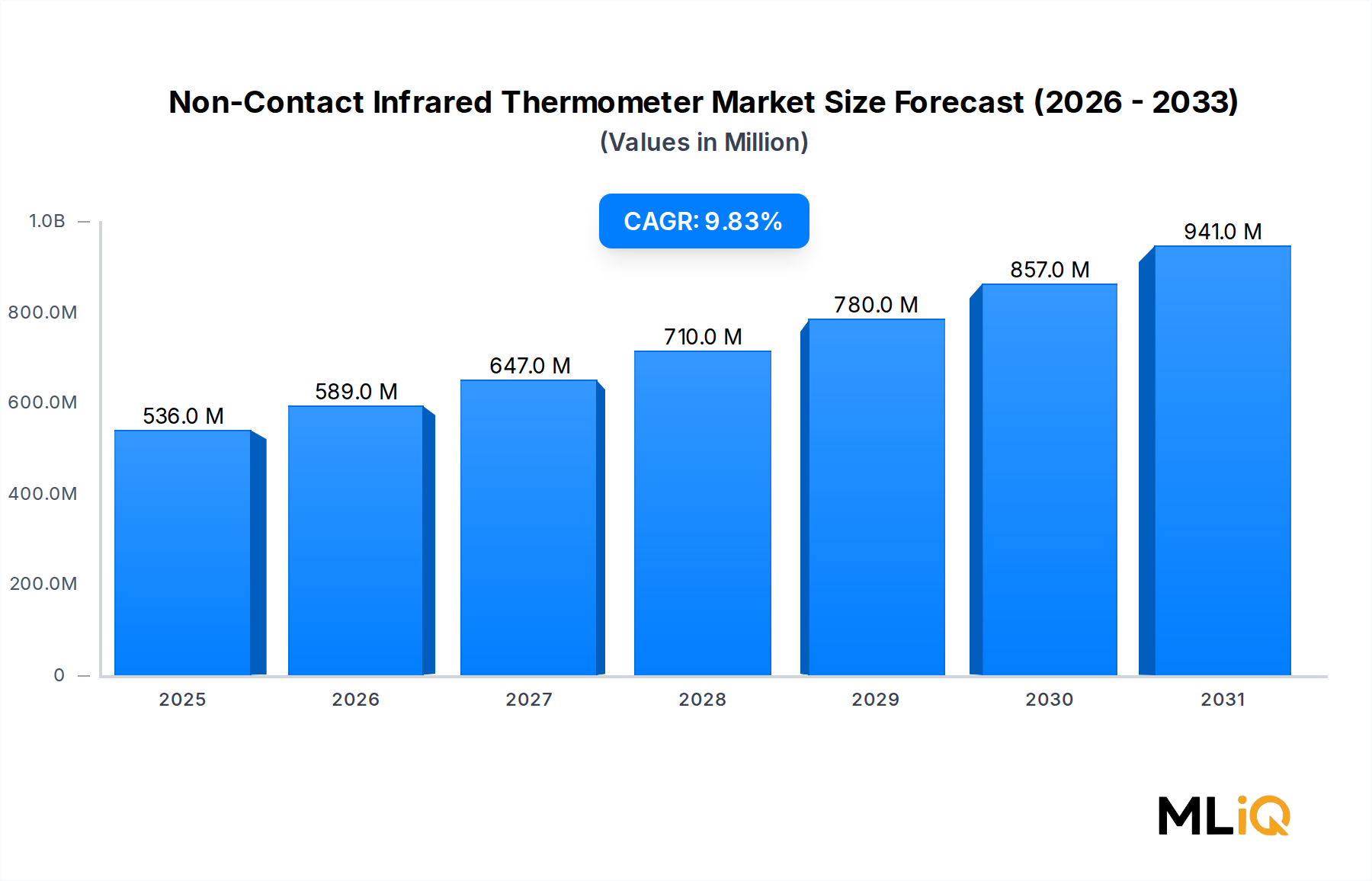

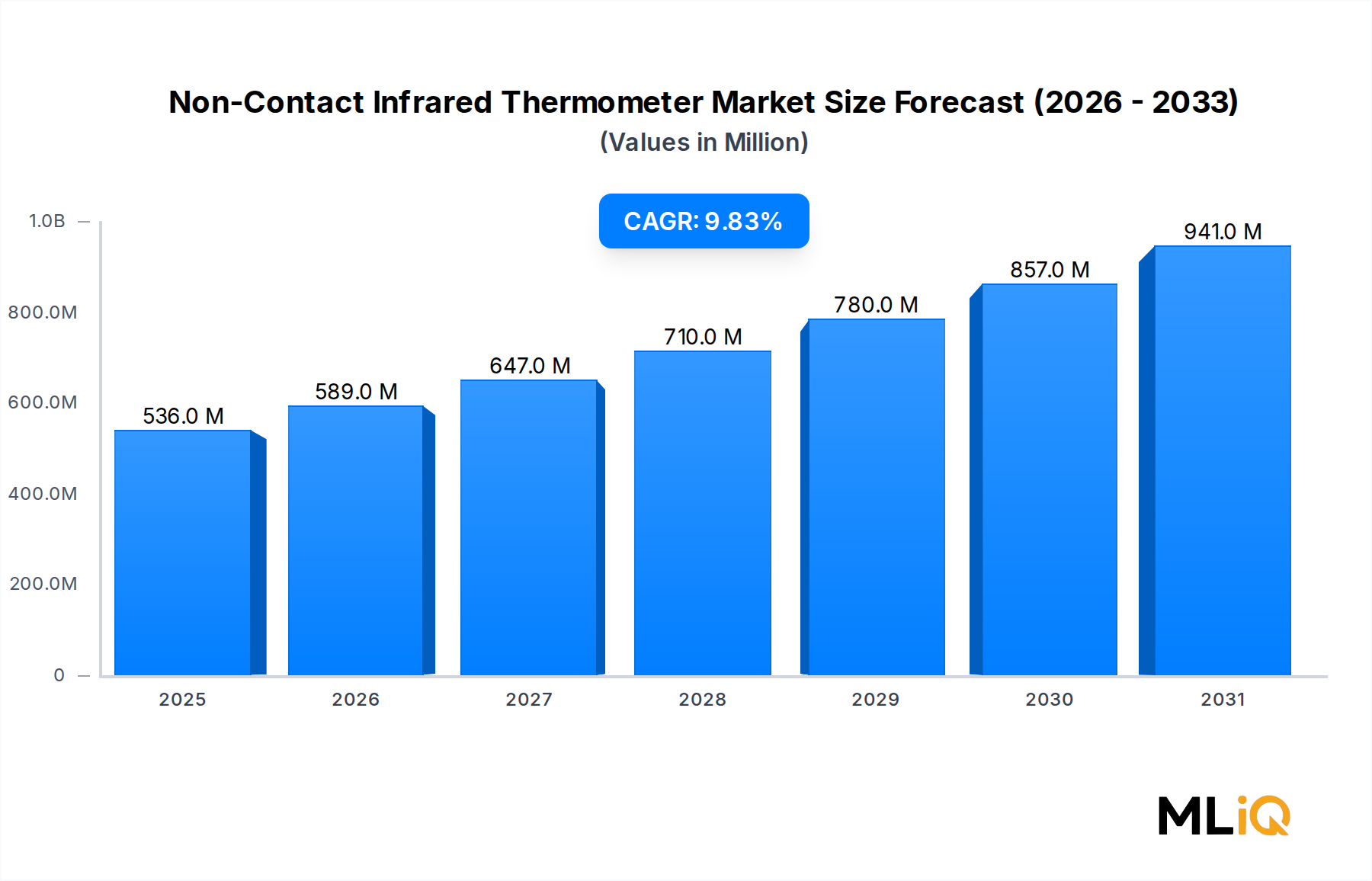

The global Non-Contact Infrared Thermometer Market is valued at $536.19 million in the current assessment period and is forecast to expand at a compound annual growth rate (CAGR) of 9.83% through 2025–2033. This robust growth trajectory reflects a confluence of structural demand shifts across medical, industrial, and consumer segments that have permanently recalibrated how temperature measurement is perceived and deployed worldwide.

The post-pandemic normalization has not diminished adoption; instead, it has reinforced the utility of non-contact thermometry as a standard-of-care instrument. Hospitals, clinics, and public health agencies have permanently integrated infrared forehead and tympanic thermometers into patient intake protocols, while industrial users have upgraded their predictive maintenance toolkits with fixed-mount pyrometers capable of continuous surface temperature surveillance. This dual-axis demand—medical and industrial—provides the market with a diversified revenue base that insulates it from sector-specific cyclicality.

Macro tailwinds further amplify the growth narrative. Rising healthcare expenditure across Asia Pacific, the proliferation of smart manufacturing initiatives in Europe and North America, and increasing regulatory emphasis on occupational health and safety standards are driving procurement volumes at institutional levels. Governments in emerging economies are expanding primary healthcare infrastructure, creating greenfield demand for affordable, accurate, non-invasive diagnostic tools.

Technological advancement is another critical catalyst. Manufacturers are integrating Bluetooth and Wi-Fi connectivity, cloud data logging, and AI-assisted fever detection algorithms into new-generation devices. This convergence of connectivity and diagnostics is elevating average selling prices while simultaneously broadening addressable markets into telehealth and remote patient monitoring verticals.

The distance-to-spot (D:S) ratio segmentation is becoming a key differentiator among industrial buyers. Devices with D:S ratios exceeding 50:1 command premium pricing and are increasingly specified in high-voltage electrical inspection, foundry operations, and food processing quality assurance applications. Meanwhile, the medical segment continues to favor handheld devices with D:S ratios between 1:1 and 12:1, optimized for human body surface measurement at practical clinical distances.

Looking forward, the market is expected to surpass a valuation significantly above $1.1 billion by 2033, underpinned by continuous product innovation, expanding healthcare access in low-and-middle-income countries, and the entrenchment of contactless temperature screening in high-traffic public venues such as airports, schools, and manufacturing facilities. The competitive landscape is intensifying, with both established medical device manufacturers and emerging semiconductor-integrated device companies vying for market share through differentiated feature sets and aggressive pricing strategies.

The medical application segment represents the single largest revenue contributor within the Non-Contact Infrared Thermometer Market, accounting for the majority of global sales value and sustaining the highest volume throughput among all end-use categories. This dominance is structural rather than cyclical, rooted in the irreversible adoption of non-contact thermometry as a frontline screening and diagnostic tool across global healthcare systems.

Several factors underpin the medical segment's commanding position. First, the COVID-19 pandemic functioned as a permanent demand accelerator. Between 2020 and 2021, global procurement of medical-grade infrared thermometers surged by estimated multiples, driven by hospital systems, public health agencies, school districts, and corporations. While demand normalized post-peak, baseline consumption settled at a structurally higher level, with many healthcare institutions standardizing non-contact devices as primary temperature assessment instruments.

Second, the clinical advantages of non-contact measurement—elimination of cross-contamination risk, speed of measurement (typically under two seconds), ease of use across pediatric populations, and elimination of probe covers as consumable costs—have made infrared thermometers the preferred choice over traditional mercury-in-glass and electronic contact probes in most clinical settings. Regulatory clearances from the U.S. FDA, CE marking in Europe, and equivalent approvals from national health regulators in Japan, South Korea, and China have further entrenched these devices as medically validated instruments.

Third, the expansion of outpatient care, home healthcare, and telehealth platforms is extending the medical segment's reach beyond institutional procurement into the direct-to-consumer (DTC) channel. Households with immunocompromised members, infants, or elderly patients are investing in consumer-grade infrared thermometers, a sub-segment growing at rates exceeding the overall market average.

Key players operating prominently in the medical segment include OMRON Healthcare Inc., which leverages its global brand equity in cardiovascular and wellness monitoring to market a comprehensive infrared thermometer portfolio across retail and clinical channels. Microlife Corporation maintains a strong position through its clinically validated, professional-grade forehead thermometers widely distributed across European and Asian healthcare systems. Briggs Healthcare serves the institutional and long-term care market with competitively priced handheld devices suited for high-volume screening environments. Advanced Energy Industries, Inc. contributes precision medical-grade temperature measurement solutions that meet stringent accuracy specifications demanded by hospital-grade procurement standards.

Within the medical segment, handheld devices dominate over fixed-mount configurations, given the need for versatile point-of-care use by clinical personnel. However, fixed infrared thermometry systems are gaining traction in hospital triage areas, airport health screening stations, and mass casualty management scenarios where automated, continuous monitoring of large populations is required.

The medical segment's market share is not only large but consolidating upward. As reimbursement frameworks in developed markets increasingly recognize remote patient monitoring and digital health data capture, manufacturers are investing in medical-grade devices with electronic health record (EHR) integration capabilities. This stratification between basic consumer devices and premium connected medical instruments is creating a two-speed market within the medical segment itself, with the premium tier exhibiting faster revenue growth and superior margin profiles. The broader Patient Monitoring Devices Market provides strategic context for understanding how infrared thermometry is being absorbed into integrated care pathways rather than remaining a standalone diagnostic tool.

The Non-Contact Infrared Thermometer Market's 9.83% CAGR through 2033 is propelled by a set of quantifiable drivers, while certain structural constraints temper the pace of expansion in specific sub-segments.

Primary Driver — Healthcare Infrastructure Expansion: Global healthcare expenditure surpassed $9 trillion in 2023 according to World Health Organization estimates, with a disproportionate share allocated to diagnostics and point-of-care tools in emerging markets. Governments in India, Brazil, and across ASEAN are deploying community health worker programs that require affordable, durable, accurate thermometers, directly benefiting handheld infrared device manufacturers.

Secondary Driver — Industrial Predictive Maintenance Adoption: The global predictive maintenance market is projected to exceed $28 billion by 2026, with thermal imaging and infrared temperature measurement constituting a core toolset. Manufacturing plants increasingly mandate infrared thermometers in preventive maintenance protocols for electrical panels, rotating equipment, and refractory monitoring. This is driving adoption of high D:S ratio devices and fueling demand across the Infrared Sensor Market and adjacent instrumentation segments.

Tertiary Driver — Regulatory Mandates for Worker Health Screening: Occupational health regulations in the EU, the U.S. (OSHA guidelines), and equivalent frameworks in Asia Pacific have institutionalized temperature screening in food processing, pharmaceuticals, and semiconductor fabs, creating recurring procurement cycles.

Constraint — Accuracy Limitations vs. Contact Thermometry: Non-contact infrared devices exhibit measurement uncertainty of ±0.2°C to ±0.5°C under standard clinical conditions, which is acceptable for screening but insufficient for certain critical care diagnostics. This limitation constrains penetration into ICU and surgical monitoring environments where continuous, high-precision core body temperature data is required.

Constraint — Market Price Commoditization: Aggressive manufacturing by Chinese OEMs has compressed average selling prices for consumer and entry-level clinical devices. The price of a standard handheld forehead thermometer declined by approximately 30–40% between 2021 and 2023 as post-pandemic excess inventory was liquidated, squeezing margins for mid-tier manufacturers.

Constraint — Calibration and Maintenance Complexity in Industrial Settings: Fixed-mount industrial pyrometers require periodic recalibration and emissivity adjustment for different target materials, adding operational overhead that can slow adoption among smaller manufacturing operations without dedicated metrology staff.

The competitive landscape of the Non-Contact Infrared Thermometer Market is fragmented at the global level, with a mix of diversified medical device corporations, precision instrumentation specialists, and vertically integrated electronics manufacturers competing across medical, industrial, and consumer segments.

American Diagnostics Corporation: A U.S.-based manufacturer specializing in diagnostic and monitoring instruments for the medical and veterinary sectors, offering a range of infrared thermometers designed for clinical accuracy and ease of use in point-of-care environments.

a&d medical: A globally recognized brand within the A&D Company group, known for precision medical measurement devices including non-contact thermometers integrated into its broader patient monitoring portfolio, particularly strong in the North American retail and clinical channels.

omega engineering: A leading provider of industrial measurement and control instrumentation, including a comprehensive catalog of infrared thermometers and pyrometers serving manufacturing, process control, and R&D applications globally, with particular strength in high D:S ratio industrial devices.

AMETEK Land: A division of AMETEK Inc. specializing in continuous non-contact temperature measurement for industrial applications including metals processing, glass manufacturing, and power generation; recognized for high-accuracy fixed-mount pyrometers operating in harsh environments.

kobold messring gmbh: A German precision instrumentation manufacturer offering infrared measurement solutions for industrial process monitoring, with strong distribution across European industrial end-markets and a reputation for engineering-grade accuracy.

OMRON Healthcare Inc.: A subsidiary of OMRON Corporation with a dominant consumer and clinical healthcare device portfolio; its infrared thermometer range benefits from strong retail distribution, brand recognition in cardiovascular monitoring, and integration with its OMRON Connect health data ecosystem.

PCE Holding GmbH: A European test and measurement instrument specialist providing a broad portfolio of infrared thermometers across industrial and HVAC applications, competing primarily on product breadth and competitive pricing in the European and export markets.

Microlife Corporation: A Swiss-headquartered medical device company recognized for clinically validated vital signs monitoring instruments; its professional infrared thermometers are widely used in European and Asian hospital systems and primary care settings.

Advanced Energy Industries, Inc.: A precision power and measurement technology company whose thermal measurement capabilities span semiconductor manufacturing, industrial processes, and medical-grade temperature sensing applications.

briggs healthcare: A U.S.-based supplier of durable medical equipment and diagnostics targeting the institutional long-term care and home health markets, distributing infrared thermometers through wholesale and retail healthcare channels.

January 2023: OMRON Healthcare Inc. launched an upgraded connected infrared thermometer series with Bluetooth Low Energy (BLE) integration and compatibility with its OMRON Connect app, enabling automatic synchronization of temperature readings with iOS and Android health platforms.

March 2023: Advanced Energy Industries, Inc. announced expansion of its Mikron infrared thermometer product line with new models targeting semiconductor wafer processing environments requiring sub-degree accuracy at elevated operating temperatures.

June 2023: Microlife Corporation received expanded CE certification under the updated EU Medical Device Regulation (MDR 2017/745) for its professional-grade forehead thermometer range, securing continued market access across EU member states under the new regulatory framework.

September 2023: AMETEK Land introduced a new generation of fixed-mount infrared pyrometers with integrated AI-based emissivity correction algorithms, targeting the steel and aluminum processing industries where surface emissivity variability had previously been a source of measurement error.

February 2024: A major distribution agreement was signed between a leading Asia Pacific healthcare distributor and Microlife Corporation, significantly expanding Microlife's retail and institutional reach across Southeast Asian markets including Indonesia, Vietnam, and the Philippines.

May 2024: omega engineering released a new series of handheld industrial infrared thermometers with extended D:S ratios up to 60:1, targeting electrical maintenance and predictive maintenance professionals in the North American utilities and manufacturing sectors.

October 2024: PCE Holding GmbH launched a compact multi-function infrared thermometer targeting the food safety and HVAC installation markets in Europe, combining surface temperature measurement with ambient humidity sensing in a single device.

The Non-Contact Infrared Thermometer Market exhibits pronounced regional heterogeneity in terms of growth velocity, demand composition, and competitive structure. Analysis across five major regions reveals distinct market maturity profiles and growth catalysts.

North America remains the most mature regional market, accounting for a substantial share of global revenue driven by the United States' large installed base of clinical and industrial infrared thermometers. The U.S. market benefits from high per-capita healthcare expenditure, rigorous FDA regulatory frameworks that favor premium devices, and broad industrial adoption in manufacturing and utilities sectors. Canada and Mexico contribute incremental growth, with Mexico emerging as a moderate-growth sub-market within the region as healthcare infrastructure investment increases. North America's CAGR is estimated at approximately 7.5–8.0% through 2033, reflecting consolidation dynamics in a high-penetration market.

Asia Pacific is the fastest-growing region, projected to expand at a CAGR of approximately 12–13% through 2033. China dominates regional volume, functioning simultaneously as the world's largest manufacturer and a rapidly expanding end-market. India represents the highest-potential greenfield opportunity, driven by government-mandated expansion of public health diagnostics infrastructure under programs such as Ayushman Bharat. Japan and South Korea contribute premium market demand, particularly for connected, clinical-grade devices. The ASEAN bloc is emerging as a high-growth sub-region as hospital construction and public health program spending accelerate.

Europe represents a significant revenue contributor with a CAGR of approximately 8.5–9.0%. Germany, France, and the United Kingdom are the largest national markets, driven by advanced healthcare systems and sophisticated industrial manufacturing bases. EU MDR compliance requirements are raising entry barriers, consolidating market share among certified device manufacturers. The Nordics and Benelux markets exhibit strong industrial demand tied to process manufacturing and food safety inspection.

Middle East & Africa is a nascent but structurally growing market, with GCC countries investing heavily in healthcare facility modernization. The UAE and Saudi Arabia are priority markets for premium clinical devices, while South Africa leads Sub-Saharan adoption. Regional CAGR is estimated at 10–11%, though from a lower absolute base.

South America, led by Brazil and Argentina, exhibits moderate growth at approximately 8% CAGR, constrained by macroeconomic volatility but supported by expanding public health procurement programs and industrial automation investment in Brazil's manufacturing corridor.

Investment activity in the Non-Contact Infrared Thermometer Market over 2022–2024 has been characterized by strategic consolidation, targeted R&D investment, and cross-segment expansion rather than large-scale venture funding rounds, reflecting the market's positioning as a mature-growth rather than early-stage technology space.

Mergers and acquisitions have been the dominant capital deployment mechanism. Large diversified medical device and instrumentation conglomerates have pursued bolt-on acquisitions of niche infrared measurement technology firms to supplement their organic product development pipelines. AMETEK Inc.'s continued investment in its AMETEK Land division exemplifies this strategy, with capital directed toward expanding pyrometry capabilities in high-growth industrial verticals including semiconductor manufacturing and battery cell production for electric vehicles.

The convergence of the Non-Contact Infrared Thermometer Market with the broader Wearable Health Monitoring Market has attracted venture capital interest in startups developing continuous, wearable infrared thermometry patches for remote patient monitoring and sports performance applications. Several early-stage companies in the United States and Israel have raised seed-to-Series A funding rounds in the $5–25 million range to develop thin-film infrared sensors capable of continuous skin temperature monitoring without contact

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.83% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Non-Contact Infrared Thermometer Market market expansion.

Key companies in the market include American Diagnostics Corporation, a&d medical, omega engineering, AMETEK Land, kobold messring gmbh, OMRON Healthcare Inc., PCE Holding GmbH, Microlife Corporation, Advanced Energy Industries, Inc., briggs healthcare.

The market segments include Mounting Type, Application Area, Distance to Spot Ratio.

The market size is estimated to be USD 536.19 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3456, USD 5769, and USD 9995 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Non-Contact Infrared Thermometer Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Non-Contact Infrared Thermometer Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.