1. What are the major growth drivers for the Power Metering Market market?

Factors such as are projected to boost the Power Metering Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

Power Metering Market

Power Metering Market+1 2315155523

The global power metering market was valued at $13.42 billion and is projected to expand at a compound annual growth rate of 6.2% through 2033, driven by a convergence of regulatory mandates, grid modernization initiatives, and the accelerating transition toward decentralized energy architectures. As utilities and commercial operators worldwide face intensifying pressure to reduce transmission losses, improve billing accuracy, and integrate renewable energy sources, demand for advanced metering solutions has entered a structurally elevated phase.

The primary macro tailwinds supporting this trajectory include government-backed smart grid deployment programs across North America, Europe, and Asia Pacific, as well as mandatory meter replacement cycles in markets such as the United Kingdom, Germany, and India. The European Union's Energy Efficiency Directive and the United States' Infrastructure Investment and Jobs Act have collectively earmarked billions of dollars for grid digitalization, creating a long-term demand runway for both hardware and software-enabled metering platforms.

On the demand side, commercial and industrial end-users are emerging as high-growth adopters of power metering technology, driven by energy cost optimization strategies and evolving Environmental, Social, and Governance (ESG) compliance requirements. The residential segment continues to benefit from mass rollouts of smart meter programs globally, with over 1 billion smart meters expected to be deployed worldwide by 2025 according to industry estimates.

Technology convergence is reshaping the competitive landscape. The integration of Internet of Things (IoT) connectivity, edge computing capabilities, and advanced data analytics within metering platforms is elevating average selling prices while simultaneously broadening the addressable market. Power metering is no longer a standalone hardware function; it is increasingly positioned as a node within a larger smart energy ecosystem, encompassing demand response, real-time load monitoring, and predictive grid management.

Key risks to the forecast include supply chain disruptions affecting semiconductor components, cybersecurity vulnerabilities in networked meters, and slower-than-anticipated utility capital expenditure cycles in emerging economies. Nonetheless, the fundamental demand equation — characterized by aging grid infrastructure, global electrification trends, and renewable energy integration requirements — provides robust structural support for sustained market expansion through the forecast horizon. Companies investing in open-protocol, interoperable metering architectures are best positioned to capture disproportionate share as procurement patterns shift toward platform-based purchasing.

Within the power metering market, segmentation by phase reveals that three-phase metering solutions constitute the dominant revenue-generating segment, accounting for the largest share of total market value. This dominance is rooted in the segment's critical role across industrial and large commercial applications, where three-phase electrical distribution is the standard infrastructure configuration for high-load operations.

Three-phase meters are engineered to measure electrical consumption across three alternating current (AC) conductors simultaneously, providing precise load balancing data, power quality monitoring, and harmonic analysis capabilities that are indispensable in manufacturing facilities, data centers, hospitals, and large retail complexes. The segment's revenue superiority is reinforced by significantly higher average selling prices compared to single-phase counterparts — a function of greater hardware complexity, advanced communication modules, and the inclusion of tamper-detection and remote disconnect features.

The industrial application sub-segment is the primary revenue anchor for three-phase metering. Manufacturers operating capital-intensive facilities increasingly deploy three-phase meters not merely for utility billing compliance, but as active instruments within broader energy management frameworks. Integration with supervisory control and data acquisition (SCADA) systems and building automation platforms has extended the functional value proposition of three-phase meters well beyond simple consumption recording.

Key players commanding significant share within this segment include ABB Ltd., Siemens AG, and Eaton Corporation plc. ABB has leveraged its comprehensive power distribution portfolio to embed three-phase metering capabilities within switchgear and substation automation packages, creating bundled value propositions that are difficult for smaller competitors to replicate. Siemens AG has pursued a software-enhanced metering strategy, integrating its SICAM and SENTRON product lines with cloud-based energy analytics, elevating the three-phase meter from a commodity hardware item to a subscription-enabled digital service. Eaton Corporation plc has focused on industrial-grade metering solutions designed for harsh environments, capturing premium pricing in sectors such as oil and gas, mining, and heavy manufacturing.

Geographically, Asia Pacific is the fastest-growing region for three-phase metering adoption, propelled by rapid industrialization in China and India, where government programs are mandating high-accuracy metering across industrial consumers to reduce aggregate technical and commercial losses. China's State Grid Corporation has been a particularly significant driver, rolling out large-scale smart three-phase meter deployments as part of its national grid modernization agenda.

The segment's share is not merely stable — it is actively consolidating. As utilities in developed markets undertake meter replacement cycles, there is a clear upgrade trajectory from legacy electromechanical three-phase meters toward solid-state, communication-enabled smart meters. This replacement dynamic creates a recurring revenue opportunity for incumbent manufacturers and new entrants alike. The commercial application sub-segment is also gaining traction, as retail chains, office buildings, and hospitality operators adopt three-phase metering to comply with energy disclosure regulations and optimize utility cost allocation across multi-tenant properties. The overall three-phase segment is expected to sustain above-market growth rates through 2033, reinforcing its position as the structural backbone of the power metering industry's revenue profile.

The power metering market's growth trajectory is governed by a set of precisely quantifiable drivers and constraints that interact across technology, policy, and macroeconomic dimensions.

Driver 1: Smart Meter Mandates and Regulatory Policy. Government mandates remain the single most powerful demand catalyst. The European Union's target of deploying smart meters in at least 80% of households by 2024 — revised and extended under the Energy Efficiency Directive — has compelled member-state utilities to accelerate procurement cycles. In the United States, the Department of Energy's Grid Modernization Initiative has allocated over $3.5 billion toward grid technology upgrades, of which metering infrastructure represents a substantial portion. India's Revamped Distribution Sector Scheme (RDSS) targets the installation of 250 million prepaid smart meters by 2025, representing one of the largest single-country metering procurement programs in history.

Driver 2: Renewable Energy Integration Requirements. As solar and wind penetration rates rise — global renewable capacity additions reached a record 295 GW in 2022 — bidirectional metering capable of measuring both consumption and export is becoming a grid necessity. Net metering programs in over 100 countries have created structural demand for advanced metering hardware with real-time interval data recording and two-way communication capabilities.

Driver 3: Energy Theft and Loss Reduction. Utilities in emerging economies face aggregate technical and commercial losses averaging 15–25% of total electricity distributed. Smart power metering with tamper-detection algorithms directly addresses this loss vector, creating compelling return-on-investment justifications for procurement.

Constraint 1: Semiconductor Supply Chain Volatility. Power metering hardware is critically dependent on microcontroller units (MCUs), power management ICs, and communication chips. The global semiconductor shortage of 2021–2023 inflated component lead times to 52+ weeks, disrupting production schedules for major meter manufacturers and compressing margins.

Constraint 2: Cybersecurity Regulatory Complexity. As meters become networked endpoints, compliance with frameworks such as NERC CIP in North America and NIS2 in Europe adds certification costs and development timelines, disproportionately burdening smaller vendors and acting as a competitive consolidation accelerant.

The competitive landscape of the power metering market is moderately consolidated at the tier-one level, with global conglomerates competing alongside specialized metering pure-plays and regional champions.

ABB Ltd.: A global leader in electrification and automation, ABB integrates power metering within its broader energy management and grid automation portfolio, leveraging installed base relationships across utilities and industrial customers in over 100 countries.

Toshiba Corporation.: Toshiba's metering division focuses on high-accuracy electronic meters for utility-grade applications, with particular strength in the Asia Pacific region and a growing emphasis on IoT-enabled smart meter platforms.

Eaton Corporation plc: Eaton offers a comprehensive range of single and three-phase power meters engineered for industrial and commercial applications, with deep integration capabilities into its power distribution and UPS product ecosystems.

Aclara Technologies LLC: A specialist in Advanced Metering Infrastructure and smart grid communication solutions, Aclara serves North American utilities with end-to-end meter-to-cash platforms including hardware, network, and software components.

General Electric: GE's Grid Solutions division delivers power metering and monitoring solutions for transmission and distribution applications, with a focus on high-voltage metering and substation automation integration.

Sensus: A Xylem brand, Sensus provides smart utility infrastructure including electricity, gas, and water meters, with its FlexNet communication network offering long-range, low-power connectivity to utility operators.

holley metering ltd.: A leading Chinese manufacturer of static electricity meters and smart metering solutions, Holley Metering benefits from strong domestic procurement contracts with State Grid Corporation and is expanding internationally across Southeast Asia and Africa.

Wasion Holdings Limited.: Wasion is a prominent manufacturer of advanced electricity metering and energy efficiency management solutions, with significant market penetration across China and growing exports to emerging markets in Africa and South Asia.

Siemens AG: Siemens delivers digitally integrated metering solutions through its Smart Infrastructure division, with SENTRON-branded meters combining energy measurement with communication and analytics capabilities for industrial and building applications.

Melrose Industries PLC: Through its subsidiary holdings, Melrose maintains exposure to power metering components and electrical measurement technologies, focusing on value creation through operational improvement of acquired industrial businesses.

March 2023: Siemens AG announced the expansion of its SENTRON smart meter portfolio with new IEC 62056 DLMS/COSEM-compliant devices targeting European utility smart metering upgrade cycles, enhancing interoperability with third-party AMI head-end systems.

June 2023: ABB Ltd. completed the integration of its Ability Energy Manager platform with its MID-certified power meters, enabling real-time energy analytics and cloud-based dashboarding for commercial building operators across the European market.

September 2023: Aclara Technologies LLC secured a major contract with a Midwestern U.S. investor-owned utility for the deployment of over 1.2 million smart electric meters as part of a grid modernization initiative, one of the largest AMI rollouts announced in North America that year.

January 2024: India's Ministry of Power reported cumulative installation of over 15 million smart prepaid meters under the RDSS program, marking a significant milestone in the country's national metering modernization effort and signaling accelerating procurement velocity.

April 2024: Wasion Holdings Limited. announced a strategic partnership with an East African power utility to supply advanced metering infrastructure for a 500,000-meter deployment, expanding the company's footprint in sub-Saharan Africa.

July 2024: Eaton Corporation plc launched its next-generation IQ Meter series featuring embedded power quality analytics, harmonic distortion monitoring, and secure HTTPS/TLS data transmission, targeting data center and critical infrastructure operators.

October 2024: The European Commission published updated guidance under the Energy Efficiency Directive requiring member states to report on smart meter rollout progress, reinforcing procurement timelines and driving Q4 utility budget allocations toward metering upgrades.

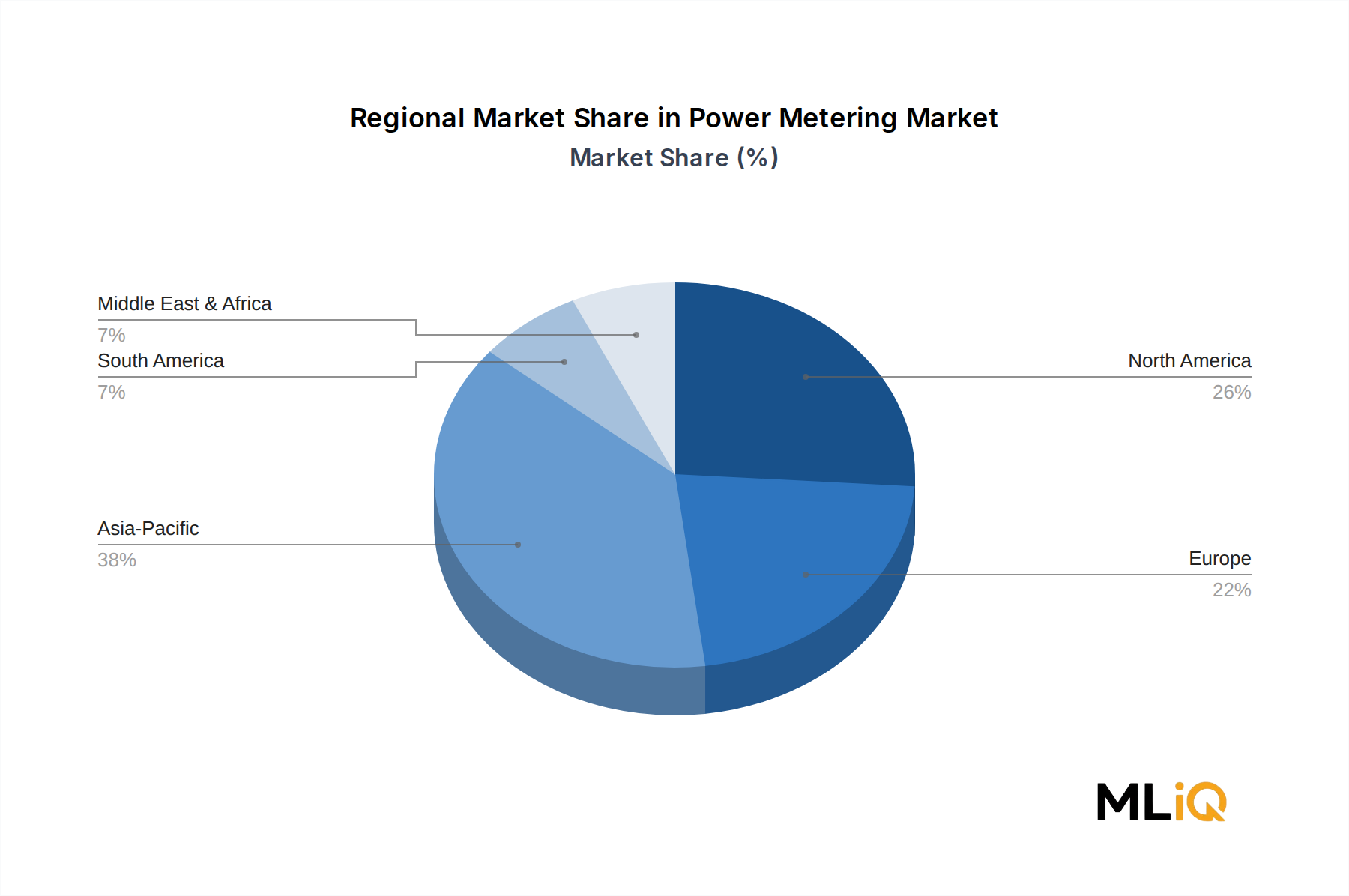

The power metering market exhibits pronounced regional heterogeneity in terms of growth velocity, technology adoption stage, and procurement driver profile.

Asia Pacific represents the largest regional market by absolute revenue and is simultaneously among the fastest-growing, driven primarily by China and India. China's State Grid Corporation and Southern Power Grid together operate the world's largest installed smart meter base, with cumulative deployments exceeding 500 million units. India's RDSS program adds significant incremental demand through 2025–2026. The Asia Pacific region is estimated to account for approximately 38–40% of global power metering revenues, with a regional CAGR tracking above the global average at approximately 7.5% through 2033. Infrastructure investment by regional development banks and government-owned utilities provides resilient procurement volumes even during macroeconomic softening.

North America is the most mature regional market, characterized by a second-wave smart meter replacement cycle as first-generation AMI deployments from the 2008–2015 era reach end-of-life. The United States dominates regional revenues, with utilities investing in advanced two-way communication meters compatible with distributed energy resource management systems (DERMS). North America's regional CAGR is estimated at 5.1%, slightly below the global average, reflecting market maturity rather than contraction. Canada and Mexico represent incremental growth vectors tied to provincial and federal grid modernization programs.

Europe is a high-value, regulation-driven market. The EU's smart meter rollout mandates, combined with the REPowerEU plan's emphasis on energy efficiency, sustain steady procurement volumes across Germany, France, Italy, Spain, and the Nordics. The United Kingdom's advanced meter rollout — targeting all households and small businesses — remains ongoing following program delays. Europe accounts for approximately 22–24% of global revenues with a regional CAGR of 5.8%.

Middle East and Africa represent the fastest-growing emerging region within the global power metering market, albeit from a smaller base. GCC countries are investing in smart grid infrastructure tied to economic diversification programs such as Saudi Vision 2030, while sub-Saharan Africa is deploying prepaid metering solutions to combat revenue losses and extend grid access. The region's CAGR is estimated at 8.3% through 2033.

South America, led by Brazil and Argentina, presents growth opportunities tied to utility privatization reforms and anti-theft metering initiatives, though fiscal constraints and currency volatility create procurement timing uncertainty, holding the regional CAGR at approximately 4.8%.

Pricing dynamics within the power metering market are shaped by a complex interplay of component cost cycles, competitive intensity, procurement scale, and technology differentiation premiums.

At the hardware level, average selling prices for single-phase residential smart meters have declined materially over the past decade due to manufacturing scale efficiencies, particularly among Chinese producers such as holley metering ltd. and Wasion Holdings Limited., which have leveraged high-volume domestic contracts to achieve cost structures that are difficult for Western manufacturers to match on a pure hardware basis. Basic single-phase smart meters in high-volume tender markets now transact at price points as low as $15–$25 per unit, compressing margins for manufacturers competing primarily on hardware cost.

Three-phase industrial and commercial meters command substantially higher average selling prices, typically ranging from $150 to over $600 per unit depending on accuracy class, communication protocol, power quality measurement capability, and enclosure specification. This segment remains relatively insulated from commoditization pressures due to the application-specific engineering requirements and the importance of vendor certification and warranty support in utility and industrial procurement processes.

Across the value chain, meter manufacturers face margin pressure from two directions: upstream, semiconductor and printed circuit board component costs remain elevated relative to pre-2020 baselines, and the Power Semiconductor Market has experienced structural price inflation due to capacity constraints in specialized metering-grade ICs. Downstream, utility procurement processes — increasingly dominated by competitive tenders and multi-year framework agreements — systematically drive down hardware margins, shifting profitability toward software licensing, connectivity services, and extended warranty programs.

The strategic response from leading players has been to pursue platform-based revenue models. By bundling meters with cloud analytics subscriptions, cybersecurity services, and data management platforms, companies such as Siemens AG, Aclara Technologies LLC, and ABB Ltd. are protecting blended gross margins in the 35–45% range even as standalone hardware margins compress. This transition mirrors dynamics observed in the broader Smart Grid Market and the Energy Management System Market, where recurring software revenues increasingly underpin company valuations.

Commodity cost levers — particularly copper, aluminum, and plastics — affect meter housing and wiring costs but represent a smaller proportion of total bill-of-materials relative to semiconductor content, limiting the margin sensitivity to base metal price

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Power Metering Market market expansion.

Key companies in the market include ABB Ltd., Toshiba Corporation., Eaton Corporation plc, Aclara Technologies LLC, General Electric, Sensus, holley metering ltd., Wasion Holdings Limited., Siemens AG, Melrose Industries PLC.

The market segments include Phase, Application.

The market size is estimated to be USD 13.42 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Power Metering Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Power Metering Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.