1. What are the major growth drivers for the Biogas Upgrading Technology Market market?

Factors such as are projected to boost the Biogas Upgrading Technology Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

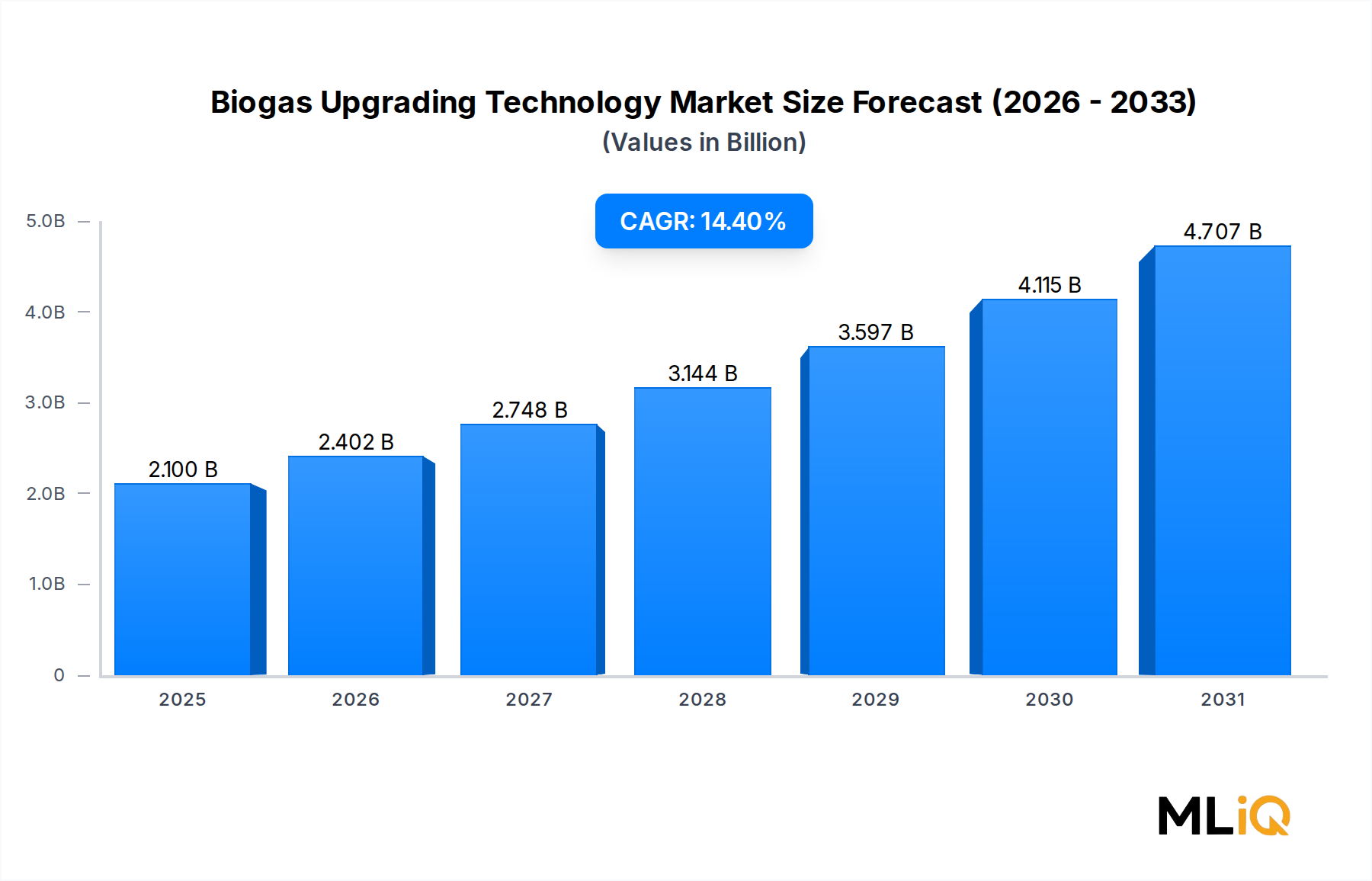

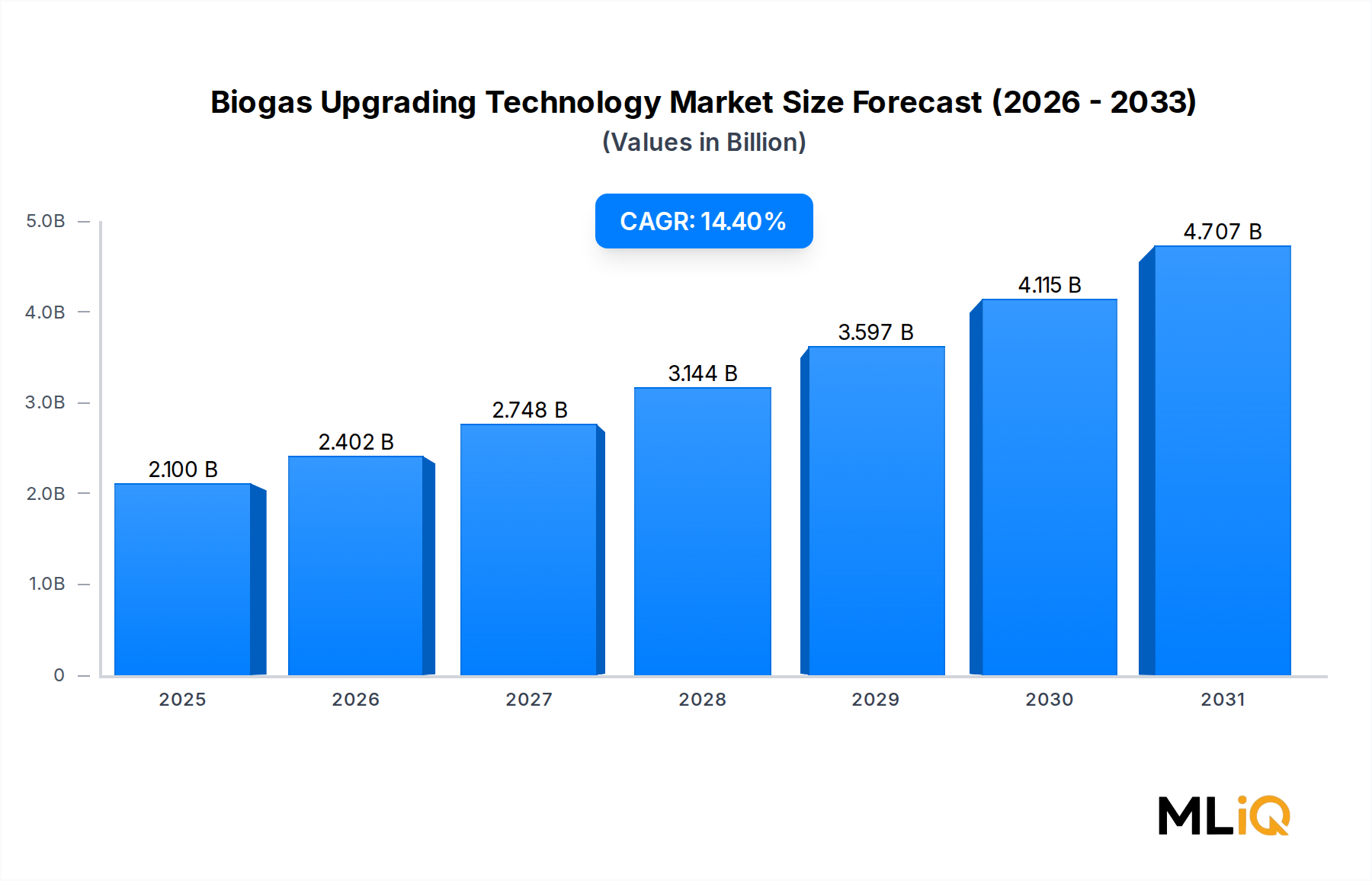

The global Biogas Upgrading Technology Market is valued at $2.10 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 14.4% through 2033, reaching an estimated valuation exceeding $6.0 billion by the end of the forecast period. This robust growth trajectory reflects accelerating policy mandates for decarbonization, surging investments in circular economy infrastructure, and the rising commercial viability of biomethane as a drop-in substitute for fossil natural gas.

At its core, biogas upgrading refers to the suite of processes that remove carbon dioxide, hydrogen sulfide, water vapor, and other contaminants from raw biogas—predominantly generated through anaerobic digestion of organic waste—to produce biomethane with a methane purity typically exceeding 95%. The resulting grid-quality biomethane can be injected directly into natural gas networks, used as vehicle fuel, or converted into electricity and heat, making biogas upgrading a critical enabler of the energy transition.

Several macro tailwinds are converging to accelerate market expansion. First, the European Union's REPowerEU plan has set a target of producing 35 billion cubic meters of biomethane annually by 2030, unlocking billions in public and private capital across the upgrading value chain. Second, the United States Inflation Reduction Act (2022) introduced enhanced tax credits for renewable natural gas production, directly stimulating demand for upgrading systems in North America. Third, rapidly falling costs for membrane and pressure swing adsorption technologies have reduced the levelized cost of biomethane production by an estimated 20–30% over the past five years, improving project economics for mid- and small-scale operators.

Key demand drivers include the proliferation of municipal solid waste treatment facilities, the expansion of agricultural biogas plants, and tightening vehicle emission standards that are accelerating fleet transitions to compressed biomethane. Industrial gas demand from food, pharmaceutical, and chemical sectors further broadens the end-use base.

The forward-looking outlook is strongly positive. As carbon pricing mechanisms mature across Europe, North America, and select Asia-Pacific jurisdictions, the financial incentive structure for upgrading investment will intensify. Technological innovation—particularly in high-flux membrane modules and hybrid absorption-adsorption systems—will continue to compress capital expenditure requirements, enabling market penetration into emerging economies where feedstock availability is high but infrastructure investment has historically been constrained. Overall, the Biogas Upgrading Technology Market stands at an inflection point, transitioning from a niche environmental solution to a mainstream energy infrastructure asset class.

Among the technology segments that define the Biogas Upgrading Technology Market, absorption-based upgrading—encompassing both water scrubbing and chemical amine scrubbing—commands the largest revenue share, accounting for an estimated 38–42% of total market revenue in 2025. This dominance stems from a combination of technological maturity, operational simplicity, and the economies of scale achievable at large biogas plants processing more than 1,000 cubic meters per hour of raw biogas.

Water scrubbing, the most widely deployed absorption variant, exploits the differential solubility of CO₂ and CH₄ in water under elevated pressure. The technology requires no chemical reagents, generates no hazardous byproducts, and can be constructed from standard pressure vessel components available globally. This accessibility has made water scrubbing the default choice for municipal wastewater treatment plants and large-scale agricultural digesters, particularly in Scandinavia, Germany, and the United Kingdom, where the technology has been deployed commercially since the early 2000s.

Chemical amine scrubbing, by contrast, offers methane recoveries exceeding 99.9% and is preferred in applications where biomethane purity is paramount—such as grid injection with strict Wobbe index requirements or liquefied biomethane production for heavy-duty transport. The higher capital cost of amine scrubbers is offset by lower methane slip, which is increasingly important as carbon accounting frameworks penalize fugitive methane emissions. The growing adoption of amine scrubbing is a key factor sustaining absorption's revenue leadership even as newer technologies gain traction.

Key players active within the absorption segment include Xebec Adsorption Inc, which has developed modular water scrubbing systems optimized for decentralized deployment, and Prodeval Corp., a French specialist with a strong installed base of pressurized water scrubbing units across Europe. DMT Environmental Technology has carved a significant niche in high-capacity water scrubbing for large industrial biogas facilities, while Air Liquide leverages its global industrial gas infrastructure to offer integrated amine scrubbing solutions with on-site gas quality management.

The absorption segment's revenue share is consolidating rather than growing, a natural consequence of market maturation. Vacuum Pressure Swing Adsorption (VPSA) and membrane separation are gaining share at the expense of water scrubbing in the sub-500 cubic meters per hour segment, driven by lower water consumption, reduced footprint, and improved energy efficiency. Nevertheless, absorption retains a structural advantage in large-scale applications where its high throughput capacity and well-understood operational profile reduce project financing risk.

Regulatory developments are also reinforcing absorption's position. Several European grid operators have tightened biomethane specifications to require methane purities above 97%, a threshold more reliably achieved by chemical scrubbing than by some competing technologies. This regulatory dynamic is expected to sustain demand for amine-based systems even as the overall technology mix diversifies over the 2025–2033 forecast window.

Investment activity within the absorption sub-segment remains vigorous. Greenlane Renewables Inc. reported a backlog of absorption-based upgrading projects in 2024 valued at over $50 million, underscoring continued commercial demand. As the Biomethane Market expands globally, absorption technology is expected to maintain its foundational role while commanding premium pricing in high-purity, grid-injection applications.

The Biogas Upgrading Technology Market is shaped by a well-defined set of structural drivers and tangible constraints that collectively determine investment pace and technology adoption rates.

Primary Driver — Regulatory Mandates and Renewable Gas Targets: The European Commission's mandate to blend 5.5% biomethane into the gas grid by 2030 under the revised Renewable Energy Directive (RED III) is the single most powerful demand catalyst in the market. Germany alone has targeted 10 billion cubic meters of biomethane production by 2030, up from approximately 2 billion cubic meters in 2023, implying a need for several hundred new or expanded upgrading plants. In the United States, California's Low Carbon Fuel Standard assigns a carbon intensity score to upgraded biomethane that can generate tradeable credits worth $80–$120 per metric ton of CO₂ equivalent, providing a significant revenue subsidy for project developers.

Secondary Driver — Feedstock Expansion: The global proliferation of anaerobic digestion infrastructure is expanding the available feedstock base for upgrading. The number of biogas plants in the EU exceeded 18,000 as of 2023, with the majority not yet equipped with upgrading capability, representing a large addressable retrofit market. The Anaerobic Digestion Market itself is expanding at a CAGR of approximately 7–9%, providing a structural pipeline of future upgrading project opportunities.

Primary Constraint — High Capital Expenditure: Upgrading systems for large-scale plants carry capital costs of $1.5–$4.5 million per 1,000 cubic meters per hour of installed capacity, depending on technology type. For agricultural and community-scale operators, this investment threshold remains prohibitive without grant support or long-term off-take agreements, limiting market penetration in price-sensitive geographies including Southeast Asia and Sub-Saharan Africa.

Secondary Constraint — Methane Slip and Regulatory Uncertainty: Methane slip—the unintentional release of methane during the upgrading process—is an emerging regulatory liability. Several jurisdictions are beginning to monitor and penalize methane emissions from upgrading facilities. Technologies with methane slip above 0.5% face potential retrofit requirements, creating operational uncertainty for installed plant owners and adding hidden lifecycle costs to capex-focused procurement decisions.

The competitive landscape of the Biogas Upgrading Technology Market is moderately fragmented, with a mix of global industrial gas majors, specialized biogas engineering firms, and emerging technology developers.

Xebec Adsorption Inc: A Canadian specialist in pressure swing adsorption and membrane-based upgrading systems, Xebec has built a global installed base exceeding 300 upgrading units and is expanding its service and O&M revenue streams to improve recurring revenue visibility.

Prodeval Corp.: A French pioneer in pressurized water scrubbing, Prodeval operates one of the largest installed bases of upgrading units in Europe and has recently expanded into North American markets through strategic distribution partnerships.

DMT Environmental Technology: A Netherlands-based engineering firm specializing in Carborex water scrubbing and membrane systems, DMT serves municipal, industrial, and agricultural biogas clients across more than 40 countries.

Clarke Energy: A leading distributed energy engineering company active in the integration of upgraded biomethane with combined heat and power (CHP) systems, Clarke Energy supports the full value chain from gas upgrading to power generation infrastructure.

Clean Energy Fuels Corporation: A major provider of renewable natural gas as a transportation fuel in North America, Clean Energy Fuels is vertically integrated into biogas upgrading to secure domestic biomethane supply for its fueling network.

Metener Oy: A Finnish specialist in small- and medium-scale biogas upgrading, Metener focuses on agricultural and municipal applications and has a strong reference base in Nordic markets.

Malmberg Bioerdgastech GmbH: A Swedish-German firm with deep expertise in water scrubbing technology, Malmberg offers turnkey upgrading solutions and has completed more than 200 installations worldwide.

AB HOLDING SPA: An Italian engineering conglomerate active in biogas plant construction and upgrading integration, AB HOLDING serves primarily Southern European markets and has expanded into North Africa.

Bright Renewables B.V.: A Dutch technology developer focused on high-efficiency membrane upgrading modules, Bright Renewables targets the fast-growing decentralized and small-scale upgrading segment.

VERBIO Vereinigte BioEnergie AG: A German bioenergy company that operates large-scale biogas-to-biomethane facilities and is one of the largest biomethane producers in Europe, providing a vertically integrated benchmark for the market.

Greenlane Renewables Inc.: A Vancouver-based upgrading technology provider offering water scrubbing, pressure swing adsorption, and membrane systems, Greenlane has one of the broadest technology portfolios in the market and a growing North American and European project pipeline.

Air Liquide: A global industrial gas leader that offers integrated biomethane production, purification, and distribution solutions, leveraging its gas infrastructure network to provide end-to-end project development for large-scale upgrading investments.

Wartsila: A Finnish marine and energy technology company that integrates biogas upgrading into broader decentralized energy system solutions, targeting industrial and municipal clients requiring multi-vector energy management.

Pentair plc: A global water and fluid management company with filtration and separation product lines applicable to biogas pre-treatment, Pentair serves as a component supplier to upgrading system integrators.

Evonik Industries: A German specialty chemicals company that has developed high-performance polyimide membrane modules specifically for biogas upgrading, positioning itself as a key materials supplier to membrane-based upgrading system manufacturers.

January 2024: Greenlane Renewables Inc. announced the commissioning of a 1,200 cubic meters per hour water scrubbing upgrading plant at a municipal wastewater facility in the Netherlands, one of the largest single-site installations in its project history.

March 2024: The European Commission published the Biomethane Industrial Partnership roadmap, committing €83 billion in public and private investment to scale biomethane production capacity to 35 billion cubic meters per year by 2030, directly stimulating upgrading equipment procurement across member states.

May 2024: Evonik Industries launched its SEPURAN Green second-generation membrane module, claiming a 15% improvement in CO₂/CH₄ selectivity and a 10% reduction in energy consumption versus its predecessor, targeting the sub-500 cubic meters per hour market segment.

August 2024: Clean Energy Fuels Corporation secured a 20-year off-take agreement for biomethane produced at a California dairy cluster project, underlining the long-term contractual structures increasingly underpinning upgrading project finance.

October 2024: VERBIO Vereinigte BioEnergie AG commissioned a new straw-to-biomethane facility in Schwedt, Germany, with an upgrading capacity of 3,000 cubic meters per hour, the largest agricultural biomethane upgrading plant in Germany at the time of commissioning.

December 2024: Xebec Adsorption Inc completed a strategic partnership with a Japanese industrial gas distributor to market pressure swing adsorption upgrading systems across the Asia-Pacific region, targeting the rapidly growing biogas sector in Japan and South Korea.

February 2025: The United States Environmental Protection Agency finalized updated renewable fuel pathway approvals under RFS2, expanding eligible feedstocks for biogas upgrading to cellulosic waste streams, significantly broadening the economic case for new upgrading installations.

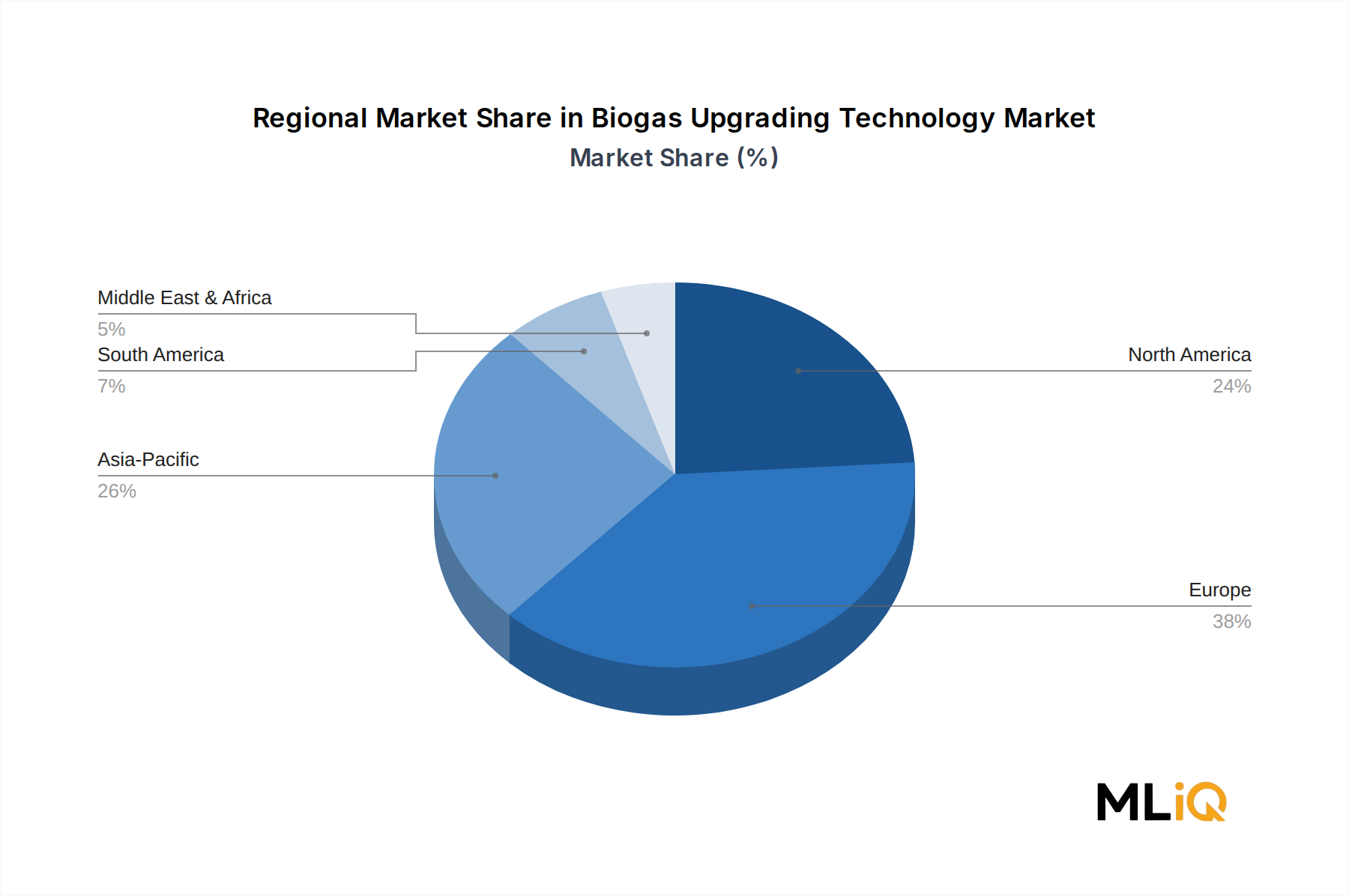

Europe dominates the global Biogas Upgrading Technology Market, accounting for approximately 48–52% of total revenue in 2025, driven by the world's most developed policy framework for biomethane, the highest density of anaerobic digestion infrastructure, and extensive gas grid injection regulation. Germany, Sweden, Denmark, and the United Kingdom are the four largest national markets. Germany alone hosts more than 250 active biomethane upgrading plants, with the national Renewable Energy Sources Act (EEG) and its successor frameworks providing feed-in premiums that underwrite project economics. Europe's market is relatively mature in terms of technology adoption but continues to grow as the EU's 2030 biomethane targets drive a new wave of plant construction and capacity expansion. The regional CAGR is estimated at 11–12% through 2033.

North America is the second-largest regional market, with the United States accounting for the bulk of activity. The combination of California's Low Carbon Fuel Standard credits, federal Renewable Fuel Standard incentives, and the Inflation Reduction Act's Section 45Z clean fuel production tax credit has created one of the most financially attractive environments for biomethane production globally. The regional CAGR is projected at 15–17%, making North America one of the fastest-growing regions in the forecast period. Dairy farm clusters in California, Texas, and the Midwest represent the primary feedstock source, while municipal solid waste and food processing waste are expanding the feedstock base. Canada is also emerging as a notable market following federal clean fuel regulations enacted in 2022.

Asia-Pacific represents the fastest-growing regional market, with a projected CAGR of 18–20% through 2033. China, India, Japan, and South Korea are the primary growth markets. China's 14th Five-Year Plan explicitly targets biogas industrialization, with central government funding supporting upgrading technology pilots at large agricultural and municipal sites. India's SATAT scheme aims to establish 5,000 compressed biomethane production plants, creating a significant addressable market for small- and medium-scale upgrading systems. Japan and South Korea are investing in domestic biomethane production to reduce LNG import dependence following the energy security shocks of 2022.

The Middle East & Africa and South America are nascent but emerging markets. Brazil, with its abundant agro-industrial waste from sugarcane and livestock operations, holds significant long-term potential. The regional CAGR for South America is estimated at 12–14%, while Middle East & Africa growth

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.4% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Biogas Upgrading Technology Market market expansion.

Key companies in the market include Xebec Adsorption Inc, Prodeval Corp., DMT Environmental Technology, Inc., Clarke Energy, Clean Energy Fuels Corporation, Metener Oy, Malmberg Bioerdgastech GmbH, AB HOLDING SPA, Bright Renewables B.V., VERBIO Vereinigte BioEnergie AG, Acrona Projects SARL, Air Liquide, Greenlane Renewables Inc., B-Sustain Energy Projects Private Ltd., Wartsila, Atmos Power Pvt Ltd., Pentair plc, Evonik Industries, Aemetis, Inc., Spectrum Renewable Energy Limited.

The market segments include Technology, End-Use.

The market size is estimated to be USD 2.10 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Biogas Upgrading Technology Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Biogas Upgrading Technology Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.