1. What are the major growth drivers for the South America Coiled Tubing Market market?

Factors such as are projected to boost the South America Coiled Tubing Market market expansion.

+1 2315155523

South America Coiled Tubing Market

South America Coiled Tubing Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

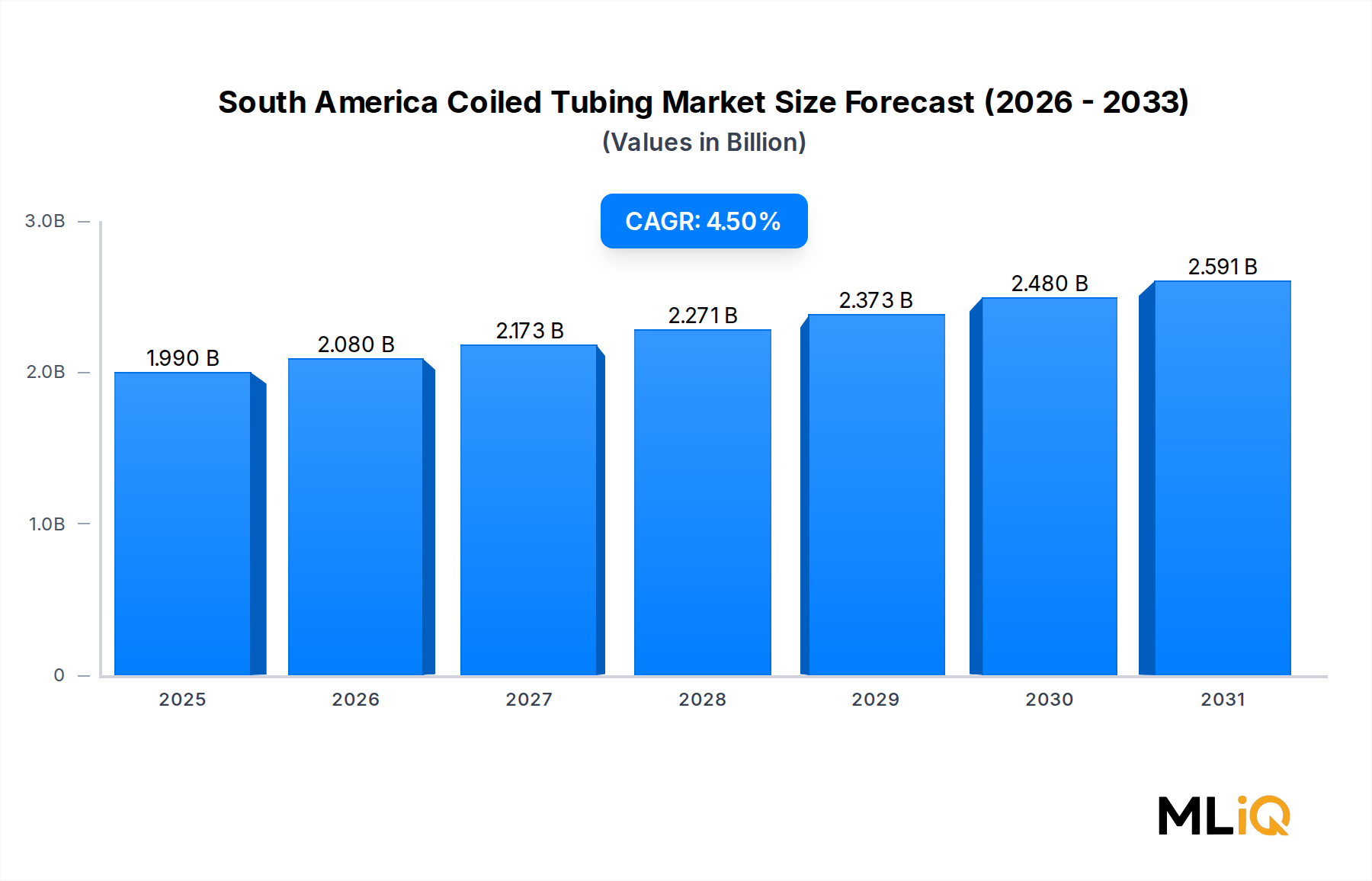

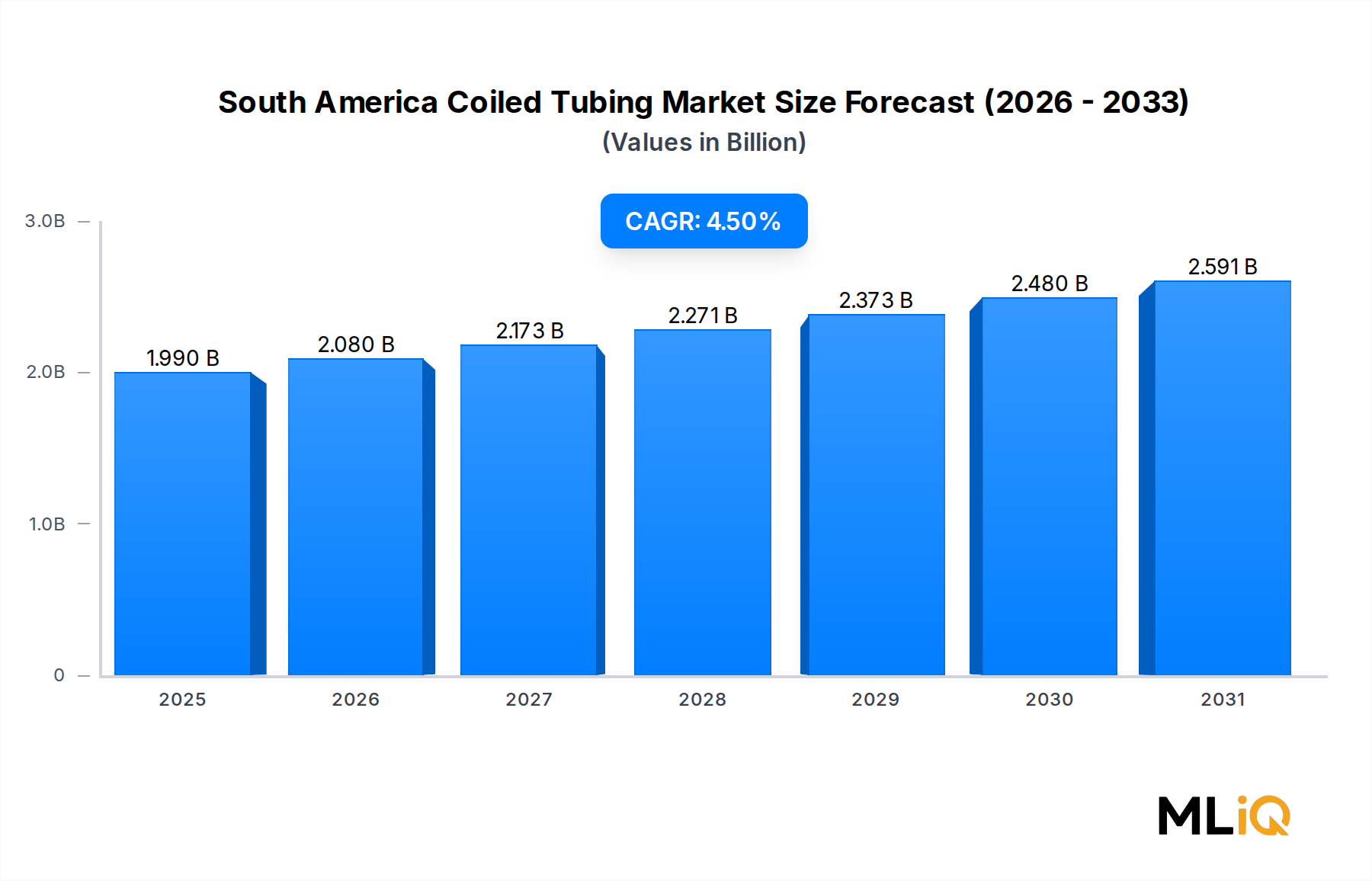

The South America Coiled Tubing Market is valued at $1.99 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 4.5% through 2033, driven by escalating upstream oil and gas investment, maturing field redevelopment programs, and the growing operational complexity of deepwater and unconventional reservoirs across the continent. Brazil, Argentina, and Colombia collectively represent the primary demand centers, each presenting differentiated growth vectors anchored in distinct geological profiles and regulatory environments.

The market encompasses coiled tubing services deployed across well intervention, drilling, and ancillary operations in both onshore and offshore environments. Well intervention activities currently constitute the dominant revenue-generating segment, reflecting the large installed base of producing wells requiring stimulation, cleanout, and workover operations. Coiled tubing's advantage over conventional workover rigs—including reduced rig-up time, live well intervention capability, and lower operational footprint—makes it the preferred technology in high-cost deepwater environments prevalent along Brazil's pre-salt corridor.

Key macro tailwinds propelling the South America Coiled Tubing Market include sustained crude oil prices maintaining breakeven viability for deepwater projects, national oil company capital expenditure expansion, and an increasing shift toward mature field optimization rather than greenfield development. Petrobras's multi-year investment program targeting pre-salt production enhancement has directly stimulated demand for coiled tubing services, with the company committing billions in upstream activity through 2029. Argentina's Vaca Muerta shale formation represents an additional structural demand driver, as unconventional completions increasingly rely on coiled tubing for perforation, stimulation, and post-fracture cleanout operations.

The competitive landscape is shaped by multinational oilfield services majors alongside regional specialists, with service quality differentiation, proprietary downhole tool assemblies, and integrated project delivery emerging as primary competitive axes. Digitalization of coiled tubing operations, including real-time data analytics and remote monitoring, is gaining traction and represents a meaningful frontier for service differentiation.

Looking ahead through 2033, the South America Coiled Tubing Market is expected to benefit from the convergence of aging field redevelopment mandates, expanding offshore infrastructure, and regulatory incentives supporting domestic energy security. Markets adjacent to coiled tubing—including the Coiled Tubing Services Market and related Well Intervention Market—are simultaneously experiencing growth, reinforcing the broader upstream services expansion cycle underway across the continent. Operators are increasingly bundling coiled tubing with complementary well services, creating integrated service packages that expand addressable revenue per well while compressing total project costs.

Within the South America Coiled Tubing Market, the Well Intervention service segment commands the largest share of revenues, a position underpinned by structural characteristics of the regional production base, the maturity profile of existing reservoirs, and the economic imperative to maximize recovery from costly offshore wells. Well intervention via coiled tubing encompasses a broad operational spectrum including nitrogen kickoffs, scale removal, sand cleanout, chemical injection, perforation, plug setting and milling, and production logging—all of which are increasingly required as reservoir depletion accelerates across Brazil's pre-salt fields and Argentina's conventional onshore basins.

Brazil's offshore pre-salt complex, anchored in the Santos and Campos basins, features ultra-deepwater wells with exceptional productive lifetimes but significant intervention requirements driven by carbonate reservoir complexity and high-pressure, high-temperature (HPHT) conditions. Coiled tubing intervention in these environments demands specialized equipment configurations—including high-strength composite or tapered coiled tubing strings, advanced injector head designs, and real-time downhole telemetry—creating substantial barriers to entry and supporting premium service pricing. The intervention segment's revenue dominance is partly a function of the frequency of required operations: a single deepwater well may require multiple intervention campaigns over its productive life, generating recurring service revenue streams.

In Argentina, the Vaca Muerta formation's unconventional development program drives intervention demand from a different angle. Multi-stage hydraulically fractured horizontal wells in Vaca Muerta require coiled tubing for post-fracture plug milling, sand removal, and production optimization, activities that are operationally intensive and time-sensitive given the high day-rate costs of completion equipment. YPF and its international partners have progressively scaled unconventional activity, with drilled well counts growing year-over-year and creating a compounding backlog of intervention requirements.

The Well Intervention Market globally is experiencing parallel growth dynamics, and South American operators are benefiting from technology transfer and capital investment channeled through multinational service companies operating across both hemispheres. Schlumberger, Halliburton, and Baker Hughes all maintain dedicated intervention service lines that leverage proprietary tooling and data analytics platforms developed through global operations and localized for South American well conditions.

Consolidation within the intervention segment is occurring through two mechanisms: vertical integration by major oilfield service companies acquiring niche intervention technology providers, and long-term service agreements between national oil companies and preferred service partners that effectively lock in multi-year revenue commitments. Petrobras has pursued framework agreements with multiple coiled tubing service providers, distributing risk while ensuring operational continuity across its diversified well portfolio.

Competition within the intervention segment increasingly centers on operational efficiency metrics—specifically, intervention success rates, non-productive time reduction, and the ability to execute complex multi-zone operations in a single run. Service providers investing in digital twin modeling of well conditions and predictive analytics for tool failure prevention are gaining competitive advantage and securing premium contract terms. The intervention segment's share within the South America Coiled Tubing Market is assessed to be growing marginally as a proportion of total revenues, reflecting both the aging of producing wells and the technical complexity escalation in new deepwater completions.

Several quantifiable drivers and constraints define the trajectory of the South America Coiled Tubing Market, with the balance of forces currently favoring sustained expansion through the forecast horizon.

On the demand side, Petrobras's 2024–2028 strategic plan allocated approximately $102 billion in total capital investment, with upstream activities—including pre-salt well drilling and intervention—accounting for the largest programmatic share. This capital commitment directly translates to coiled tubing service demand, as pre-salt wells statistically require intervention services earlier and more frequently than conventional offshore wells due to reservoir complexity. The Oilfield Services Market in South America broadly benefits from this capex environment, with coiled tubing services capturing a disproportionate share given the technical barriers associated with deepwater operations.

Argentina's Vaca Muerta formation presents a second structural driver. Unconventional production in the Neuquén Basin surpassed 300,000 barrels of oil equivalent per day in 2023, with projections targeting further expansion as pipeline infrastructure constraints ease. Each incremental fractured horizontal well generates coiled tubing demand for completion and post-completion operations, creating a durable demand signal tied to the unconventional growth curve.

The Hydraulic Fracturing Market's expansion in Argentina is directly correlated with coiled tubing service demand, as plug-and-perforate completion designs require coiled tubing for plug milling operations before wells can be placed on production. This interdependence creates a demand multiplier effect as fracturing activity scales.

On the constraint side, currency volatility in Argentina poses operational cost unpredictability for foreign service providers pricing contracts in USD while incurring peso-denominated operating costs. Import restrictions have historically delayed equipment mobilization, though recent regulatory reforms have partially mitigated this friction. Additionally, the capital-intensive nature of coiled tubing equipment—particularly high-specification units designed for deepwater operations—creates supply-side bottlenecks when demand surges, as manufacturing lead times for premium coiled tubing strings and injector units can extend to 12–18 months. Workforce skill availability in technically demanding coiled tubing operations also represents a constraint, with experienced operators in limited supply relative to regional demand growth.

The competitive landscape of the South America Coiled Tubing Market is concentrated among a small number of global oilfield services leaders, supplemented by regional specialists. The following profiles characterize the primary participants:

Schlumberger Ltd. (now SLB): The market leader by revenue share in South American coiled tubing services, SLB leverages its integrated well services platform and proprietary VIRTUAL Advisor real-time coiled tubing modeling technology to deliver premium intervention solutions across Brazilian pre-salt and Argentine unconventional operations. The company's local content compliance frameworks in Brazil position it advantageously for Petrobras contract awards.

Weatherford International Plc: Weatherford maintains a targeted coiled tubing service presence in South America, emphasizing well intervention and production enhancement applications. The company has invested in expanding its coiled tubing fleet with HPHT-rated equipment suited for deepwater Brazilian operations and has pursued cost optimization through operational streamlining following its 2019 balance sheet restructuring.

Baker Hughes Inc: Baker Hughes offers coiled tubing services integrated within its broader well intervention and completions portfolio, with particular strength in data-driven downhole diagnostics. The company's BHGE legacy technology assets support differentiated service delivery in complex multilateral well environments increasingly common in Brazil's pre-salt.

Halliburton Co.: Halliburton's coiled tubing service line in South America benefits from the company's established completions and stimulation infrastructure, particularly in Argentina's Vaca Muerta basin. Its CT pumping and nitrogen services are frequently bundled with stimulation programs, creating integrated revenue capture per well.

Trican Well Service: Trican represents a mid-tier competitive presence in South American coiled tubing services, focusing on cost-competitive service delivery in onshore markets. The company's operational model emphasizes high equipment utilization and rapid mobilization, appealing to independent operators managing budget-constrained workovers.

Calfrac Well Services: Calfrac operates primarily in the pressure pumping and well stimulation space, with coiled tubing services constituting a complementary offering in markets where it maintains stimulation infrastructure, including Argentina's unconventional plays. The company's South American footprint has expanded alongside the Vaca Muerta development cycle.

March 2024: Petrobras announced an expanded framework agreement with multiple coiled tubing service providers for well intervention operations across its Santos Basin pre-salt fields, covering an estimated 47 wells over a 36-month service window, signaling sustained demand visibility for the sector.

January 2024: SLB completed the deployment of a new generation high-pressure coiled tubing unit rated for HPHT deepwater applications in Brazil, with specifications including a 2-7/8 inch coiled tubing string and 25,000 psi pressure rating, extending the technical capability frontier for pre-salt intervention.

October 2023: Argentina's YPF and Halliburton executed a multi-year service agreement for integrated completion and coiled tubing operations in the Vaca Muerta formation, covering approximately 120 horizontal well completions annually and encompassing post-fracture plug milling services.

July 2023: Weatherford International announced the commissioning of an enhanced coiled tubing training facility in Rio de Janeiro, designed to address skilled operator shortages in Brazil and support local content requirements under ANP regulatory frameworks.

April 2023: The Argentine government issued updated import facilitation measures for oilfield equipment, reducing customs clearance timelines for coiled tubing units and associated tooling from an average of 90 days to approximately 45 days, directly improving service mobilization efficiency for international providers.

February 2023: Baker Hughes introduced its advanced real-time coiled tubing simulation platform in South American operations, initially deployed across Brazilian offshore intervention campaigns, reducing non-productive time by an estimated 15% in pilot implementations.

The South America Coiled Tubing Market exhibits significant regional heterogeneity, with Brazil, Argentina, and the Rest of South America presenting distinct demand profiles, growth trajectories, and competitive conditions.

Brazil constitutes the largest single country market within the South America Coiled Tubing Market, accounting for an estimated 55–60% of total regional revenue. The country's dominance reflects the scale of Petrobras's offshore operations, particularly in the pre-salt Santos and Campos basins where deepwater well counts are substantial and intervention frequency is elevated. Brazil's regional CAGR is estimated at approximately 4.2% through 2033, reflecting a mature but high-value market with stable incremental growth driven by production optimization mandates. The primary demand driver is pre-salt field life extension and enhanced recovery operations. The Offshore Drilling Market in Brazil remains the most active in South America, and its activity level serves as a leading indicator for coiled tubing service demand.

Argentina represents the fastest-growing country market within the region, with an estimated CAGR of 6.1% through 2033, propelled by Vaca Muerta unconventional development. Onshore coiled tubing demand for post-fracture operations, production enhancement, and artificial lift optimization is scaling rapidly alongside well count growth. Argentina's share of total South American coiled tubing revenue stands at approximately 25–28% in 2025, up from lower levels a decade prior, reflecting the transformational impact of shale development on service demand composition.

Rest of South America, encompassing Colombia, Ecuador, Venezuela, and other producing nations, collectively accounts for the remaining 12–18% of regional revenue. Colombia's mature onshore basins generate steady but slower-growth coiled tubing demand, with a regional CAGR estimated at 2.8%, reflecting production decline management in conventional fields. Venezuela's constrained investment environment has suppressed coiled tubing service demand relative to its theoretical resource base, while Ecuador's activity remains modest but stable.

Across the region, the Downhole Tools Market is expanding in parallel with coiled tubing service growth, as operators require increasingly sophisticated bottomhole assemblies for complex intervention operations. The most mature sub-market is Brazil's deepwater intervention segment, while Argentina's unconventional onshore operations represent the most dynamic growth frontier within the broader South America Coiled Tubing Market landscape.

The South America Coiled Tubing Market is structurally dependent on cross-border equipment and component flows, as the region lacks domestic manufacturing capacity for high-specification coiled tubing units, injector heads, and associated downhole tooling. The primary trade corridors run from North America—specifically the United States and Canada—to Brazil, Argentina, and Colombia, with U.S. manufacturers supplying the majority of premium coiled tubing strings, power packs, and control systems.

Coiled tubing strings, typically manufactured from high-grade steel alloys, are predominantly sourced from North American and European mills with specialized capabilities in tube welding and quality certification to API standards. The Oil Country Tubular Goods Market dynamics directly influence coiled tubing string costs and availability, as pricing pressures in tubular steel cascade into coiled tubing procurement budgets. When Oil Country Tubular Goods Market conditions tighten due to demand spikes in North American completions activity, South American operators face elongated delivery timelines and elevated pricing.

Brazil's local content regulations administered by the ANP create non-tariff barriers that incentivize service companies to establish in-country operational bases and, where feasible, source locally. While full in-country manufacturing of coiled tubing units remains economically unviable at current market scale, local content compliance requirements drive investment in maintenance facilities, personnel training, and component refurbishment capabilities.

Argentina's complex import regulatory framework has historically imposed significant friction on equipment importation, with import licenses required for capital equipment categories encompassing coiled tubing units. The 2023 regulatory reforms partially streamlined these processes, but currency controls limiting USD availability for import payments continue to create operational complications for foreign service providers. Tariff rates on oilfield equipment imports into Argentina range from 0–10% depending on equipment classification, with periodic special regimes providing temporary relief for strategic energy sector imports.

From an export perspective, South America is not a significant exporter of coiled tubing equipment or services, with the trade flow direction firmly oriented toward equipment importation. Regional demand growth will continue to depend on the stability of North American and European

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the South America Coiled Tubing Market market expansion.

Key companies in the market include Schlumberger Ltd.Calfrac Well Services, Weatherford International Plc, Trican Well Service, Baker Hughes Inc, Halliburton Co..

The market segments include Service, Application.

The market size is estimated to be USD 1.99 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 3930, and USD 5830 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "South America Coiled Tubing Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the South America Coiled Tubing Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.