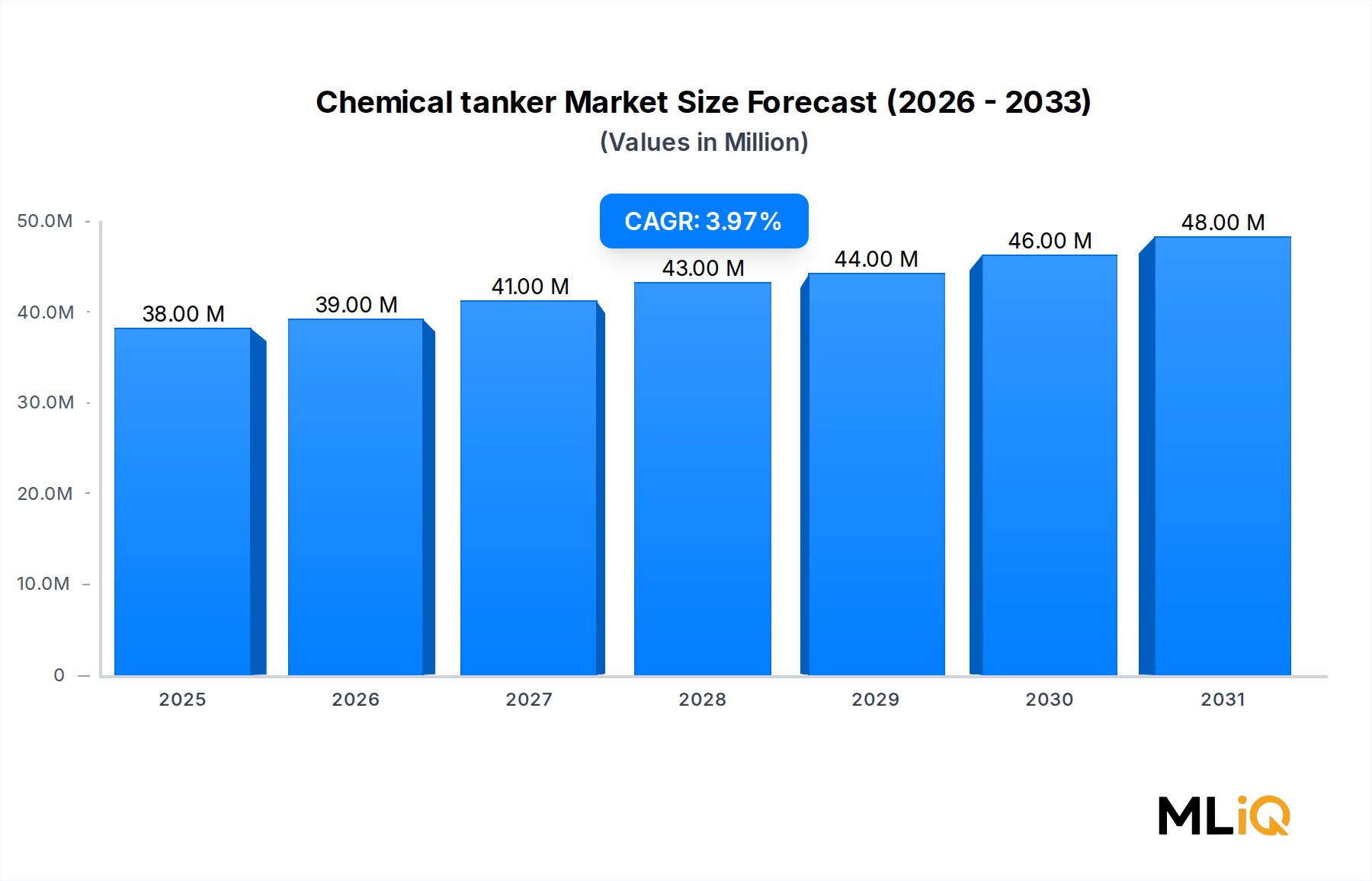

Regional Market Breakdown for the Chemical Tanker Market

The Chemical Tanker Market exhibits pronounced regional variation in growth momentum, cargo composition, and infrastructure maturity, with Asia Pacific, North America, the Middle East, and Europe representing the four most strategically significant geographies.

Asia Pacific is the fastest-growing regional market, driven by expanding petrochemical production capacity in China, India, South Korea, and Southeast Asia. China alone accounts for a disproportionate share of regional chemical import demand, importing significant volumes of organic chemicals, specialty solvents, and lubricant base stocks from the Middle East and Europe. India's growing pharmaceutical and agrochemical manufacturing base is generating incremental demand for caustic soda, methanol, and glycerin shipments. The regional CAGR for Asia Pacific is estimated at approximately 5.8%, outpacing the global average and reflecting both supply-side and demand-side expansion.

The Middle East and Africa region is the most dynamic export origin for the Chemical Tanker Market, driven by the commissioning of large-scale integrated petrochemical complexes in Saudi Arabia, the UAE, and Qatar. Arabian Gulf chemical producers are increasingly targeting Asian and European markets, generating long-haul voyage demand that benefits deep-sea fleet operators. Regional freight volumes from GCC ports have grown materially over the past decade, with further expansion anticipated as Vision 2030 and related industrial diversification programs mature.

North America represents a mature but high-value regional market, characterized by strong chemical export activity from the United States Gulf Coast. American chemical producers, benefiting from competitively priced natural gas feedstocks, export significant volumes of methanol, ethylene glycol, and caustic soda to Asian and Latin American markets. Canada and Mexico contribute additional coastal chemical tanker demand within the inland and short-sea sub-segments. The regional CAGR is estimated at 3.6%, reflecting market maturity offset by continued export volume growth.

Europe is the most mature regional market, with established chemical production centers in Germany, the Netherlands, Belgium, and France generating consistent demand for both intra-regional coastal tonnage and deep-sea import shipping from the Middle East and Asia. European operators are leading the transition toward decarbonized fleet operations, with regulatory pressure from the EU Emissions Trading System (EU ETS) creating both cost headwinds and incentives for early fleet modernization. The regional CAGR is estimated at 3.1%, the lowest among major regions, reflecting fleet renewal costs and subdued industrial production growth.

The Port Logistics Market and Industrial Chemicals Market are deeply intertwined with these regional dynamics, as terminal infrastructure capacity and chemical manufacturing output directly constrain and enable chemical tanker demand across all geographies.