1. What are the major growth drivers for the Oil and Gas Instrumentation Market market?

Factors such as are projected to boost the Oil and Gas Instrumentation Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

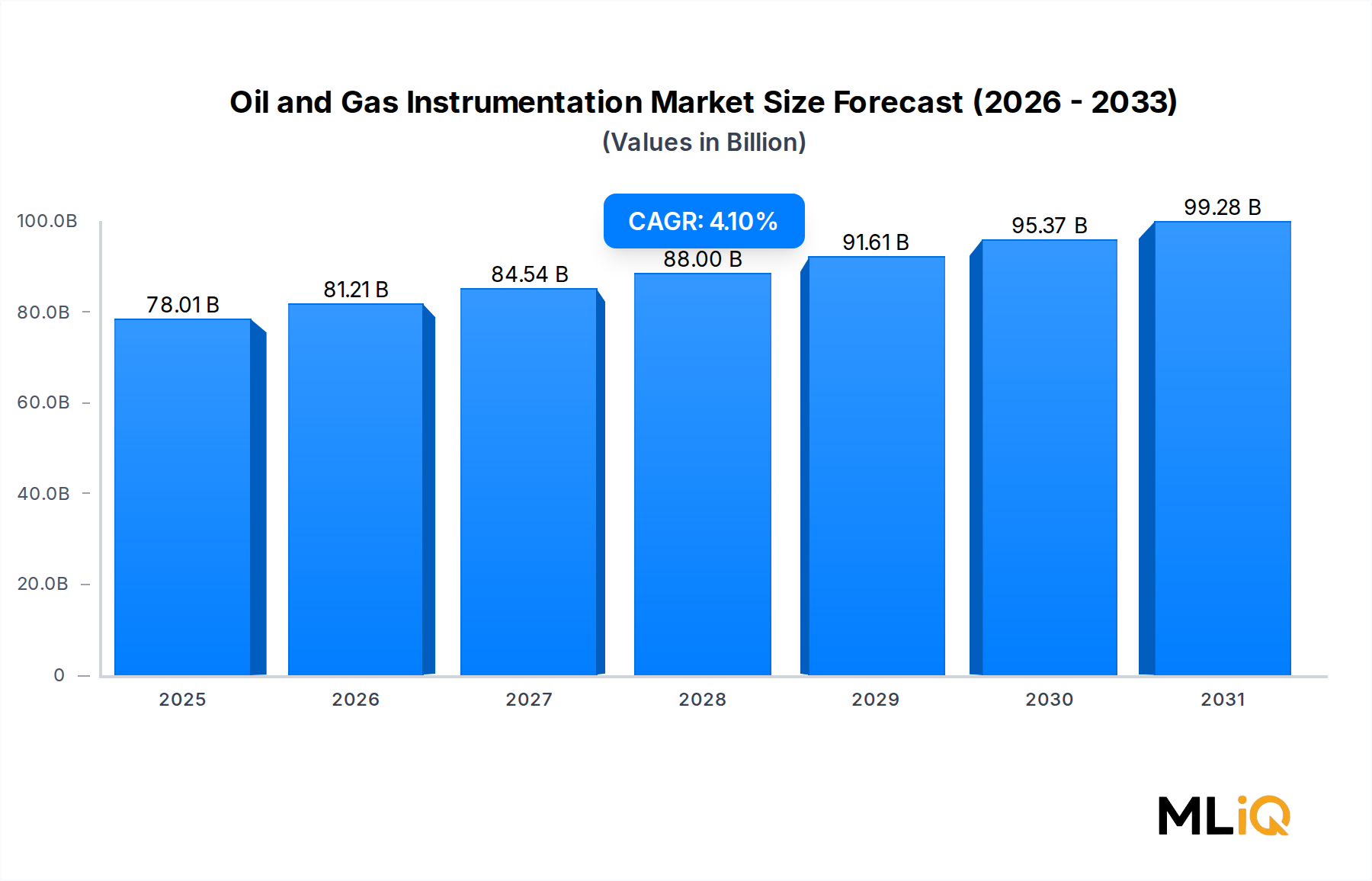

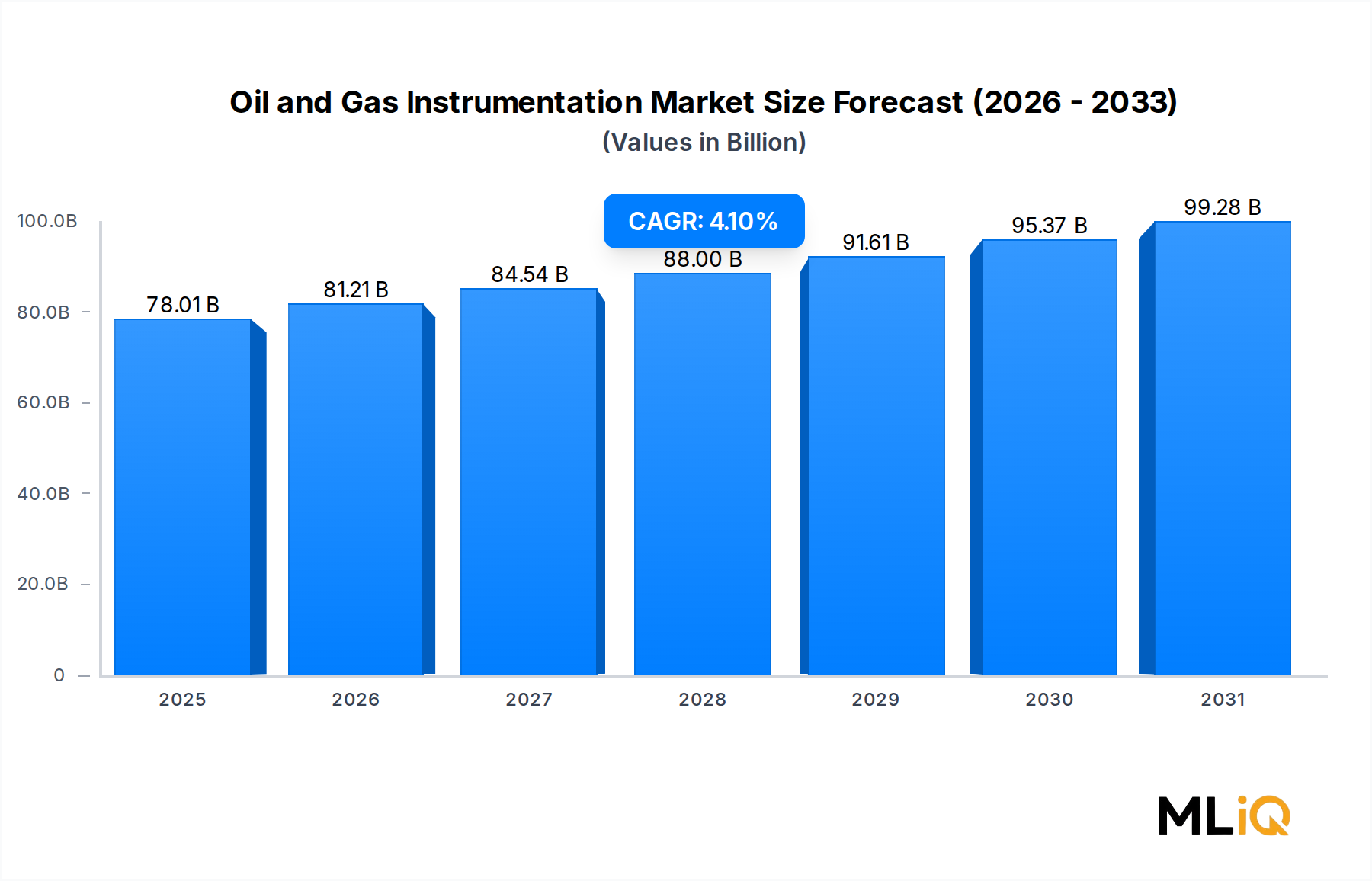

The global Oil and Gas Instrumentation Market is valued at $78.01 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 4.1% through the forecast horizon. This sustained trajectory reflects the industry's intensifying focus on operational precision, process safety, and digital transformation across upstream, midstream, and downstream segments. As energy demand continues to rise globally and capital expenditure in hydrocarbon exploration and production recovers from pandemic-era lows, the instrumentation sector stands to benefit from upstream reinvestment cycles and the retrofitting of legacy infrastructure with advanced sensing and control technologies.

A key macro tailwind is the growing regulatory pressure around emissions monitoring and process safety compliance. National and supranational environmental agencies are mandating more granular measurement capabilities at wellheads, pipelines, and refineries, which directly elevates demand for precision field instruments, analyzers, and safety-critical control systems. In parallel, the global energy transition is paradoxically accelerating investment in oil and gas automation as operators seek to maximize recoverable reserves from existing assets while minimizing operational expenditure per barrel.

Digitalization is emerging as the defining commercial theme of the current decade. Operators are progressively integrating Industrial Internet of Things (IIoT) architectures with legacy plant control systems, creating demand for smart transmitters, wireless instrumentation, and edge analytics platforms. This convergence is broadening the addressable market well beyond traditional hardware, extending into software-as-a-service (SaaS) licensing and managed services for predictive maintenance and performance optimization.

Geographically, the Middle East and Asia Pacific are emerging as the fastest-growing consumption centers, driven by national oil company (NOC) expansions and LNG infrastructure buildout respectively. North America remains the largest absolute revenue contributor, underpinned by shale production resilience and ongoing pipeline modernization programs in the United States and Canada.

From a competitive standpoint, the market is moderately consolidated, with top-tier automation and measurement conglomerates holding dominant positions through integrated product portfolios and long-term service agreements. However, niche players offering specialized process analytics or wireless solutions are capturing incremental market share in high-growth niches.

The forward-looking outlook remains constructive. As hydrocarbon asset lifecycles extend and operators prioritize production efficiency over greenfield expansion, the installed base of instrumentation equipment will require continuous upgrades, calibration services, and digital retrofits — collectively sustaining a multi-decade demand runway for vendors across the value chain.

Within the technology segmentation of the Oil and Gas Instrumentation Market, Distributed Control Systems (DCS) represent the single largest revenue-generating sub-segment. Their dominance is rooted in the fundamental architecture of modern refining, gas processing, and LNG liquefaction facilities, where centralized yet geographically distributed process control is non-negotiable for safe and efficient operations.

A DCS platform integrates thousands of measurement points — temperature, pressure, flow, and level — into a unified control narrative managed from centralized operator workstations. Unlike Programmable Logic Controller deployments, which tend to dominate discrete and batch processes, DCS architectures are inherently suited to the continuous process environments that characterize downstream petroleum refining, upstream separator trains, and midstream compression stations. This alignment with the oil and gas sector's core operational modalities explains why DCS commands a disproportionately high revenue share within the technology segment.

The dominance of DCS is further reinforced by the Distributed Control System Market's evolution toward open, interoperable architectures. Legacy proprietary DCS platforms from vendors such as Emerson Electric Co., Yokogawa Electric Corporation, ABB Ltd., and Honeywell International Inc. are being modernized with open process automation (OPA) standards, enabling operators to source best-of-breed components without vendor lock-in. This transition is triggering a significant wave of upgrade contracts, as installed bases dating from the 1990s and early 2000s reach the end of their supported lifecycles.

Emerson's DeltaV platform, Honeywell's Experion PKS, Yokogawa's CENTUM VP, and ABB's System 800xA collectively account for a substantial majority of the installed DCS base in major hydrocarbon-producing nations. These vendors compete not merely on hardware specifications but on the richness of their digital ecosystems — encompassing advanced process control (APC) modules, simulation environments, cybersecurity overlays, and cloud-based historian integrations.

The share of DCS within the broader instrumentation landscape is consolidating rather than expanding rapidly, as adjacent technologies such as Supervisory Control Data Acquisition and edge computing begin to absorb incremental digitalization budgets. Nevertheless, the installed base effect — encompassing spare parts, software licenses, training, and periodic hardware refreshes — ensures that DCS generates durable, recurring revenue streams that are largely insulated from short-term capital expenditure cycles.

The Manufacturing Execution System Market is increasingly intersecting with DCS deployments, as operators seek to close the loop between plant-level control and enterprise resource planning (ERP) systems. This integration elevates DCS from a purely operational tool to a strategic asset for production optimization and regulatory reporting, further entrenching its position within the Oil and Gas Instrumentation Market hierarchy.

For end users, the primary purchasing criterion for DCS platforms remains reliability and mean time between failures (MTBF), given the catastrophic consequences of unplanned downtime in high-pressure hydrocarbon environments. Vendors that can demonstrate superior reliability track records and rapid technical support response times consistently win competitive tenders, even at premium price points.

Several structurally significant drivers and constraints shape the growth trajectory of the Oil and Gas Instrumentation Market, each quantifiable against observable industry benchmarks.

The primary driver is capital reinvestment in upstream exploration and production. Global upstream E&P spending recovered to approximately $500 billion in 2023 and is forecast to sustain elevated levels through 2027, according to industry expenditure surveys. A meaningful fraction of this capital flows into instrumentation upgrades for new wells, subsea tie-backs, and production optimization initiatives on mature fields. This correlation between E&P capex and instrumentation demand is well-established and historically robust.

Process safety regulation constitutes a second material driver. Following a series of high-profile industrial accidents, regulators in the United States (OSHA PSM standard), Europe (Seveso III Directive), and the Middle East have significantly tightened requirements for Safety Instrumented Systems and process hazard analyses. Compliance mandates are effectively non-discretionary capex, insulating a portion of instrumentation demand from commodity price volatility.

The Industrial Sensors Market is a closely adjacent growth engine, as the proliferation of wireless and smart sensor technologies enables condition-based maintenance strategies that reduce unplanned downtime by an estimated 30–40% compared to time-based maintenance schedules. This productivity argument is compelling operators to accelerate sensor deployment across existing assets.

On the constraint side, the cyclicality of oil prices remains the dominant headwind. Crude price drawdowns — such as the 2020 collapse to sub-$20/barrel — trigger sharp capex curtailments that disproportionately affect instrumentation procurement lead times and project deferrals. Even in the current elevated price environment, capital discipline among major international oil companies (IOCs) means that instrumentation budgets are scrutinized for return-on-investment justification.

Cybersecurity risk is an emerging structural constraint. As operational technology (OT) systems become increasingly networked, the attack surface for industrial cyber threats expands. This creates procurement friction as end users demand more rigorous cybersecurity certifications from vendors, extending sales cycles and increasing compliance costs.

Skilled labor shortages in instrumentation engineering and maintenance represent a further bottleneck, particularly in mature markets such as the North Sea and the Gulf of Mexico, where workforce demographics are skewing older.

The competitive landscape of the Oil and Gas Instrumentation Market is anchored by a group of globally diversified technology and automation conglomerates, with competitive differentiation driven by integration depth, service network breadth, and digital platform capabilities.

Siemens AG: A global automation leader, Siemens brings an integrated portfolio spanning process instrumentation, DCS, and industrial software, with particular strength in European refining and LNG infrastructure. Its SIMATIC PCS 7 and PCS neo platforms are widely deployed across midstream and downstream segments.

Emerson Electric Co.: One of the most dominant vendors in the sector, Emerson's Automation Solutions business encompasses the Rosemount measurement brand, DeltaV DCS, and Fisher control valves. Its digital twin and asset management software platforms are setting competitive benchmarks for integrated lifecycle management.

ABB Ltd.: ABB's Process Automation division delivers an end-to-end instrumentation and control portfolio anchored by the System 800xA DCS and a broad range of analytical and measurement instruments. The company is investing heavily in AI-driven process optimization capabilities.

Hima Paul Hildebrandt GmbH & Co KG: A specialist in safety-critical automation, Hima occupies a distinctive niche in safety instrumented systems and emergency shutdown (ESD) systems for hazardous process environments, maintaining strong relationships with major NOCs and IOCs globally.

Yokogawa Electric Corporation: The Japanese automation giant is a leading supplier of DCS, field instruments, and industrial analyzers, with an expanding presence in subsea instrumentation and digital transformation consulting for Asia Pacific operators.

Schneider Electric SE: Schneider Electric's EcoStruxure architecture provides a converged IT/OT platform for oil and gas operations, integrating SCADA, energy management, and process safety in a unified software environment.

Endress+Hauser Management AG: Renowned for measurement instrumentation across flow, level, pressure, and temperature domains, Endress+Hauser commands strong loyalty among process engineers for product reliability and calibration service networks.

Rockwell Automation Inc.: A key player in programmable logic controller and manufacturing execution system deployments, Rockwell Automation is extending its oil and gas footprint through strategic partnerships and its FactoryTalk industrial software suite.

Honeywell International Inc.: Honeywell's Process Solutions division is a tier-one competitor across DCS, safety systems, and gas analyzers. Its Forge industrial IoT platform represents a significant investment in cloud-native operational intelligence for refining and petrochemical clients.

GE Oil and Gas: Now operating within Baker Hughes, the former GE Oil and Gas business contributes advanced measurement, compression instrumentation, and subsea control systems, particularly relevant to deepwater E&P applications.

January 2024: Emerson Electric Co. completed the acquisition of NovaTech Process Solutions, strengthening its distributed control system portfolio for downstream refining applications and expanding its installed base in North American processing facilities.

March 2024: Honeywell International Inc. launched an upgraded version of its Experion PKS Highly Integrated Virtual Environment (HIVE) architecture, enabling modular, cloud-connected process control deployments with enhanced cybersecurity isolation for offshore platforms.

June 2024: ABB Ltd. announced a strategic partnership with a major Middle Eastern NOC to deploy its System 800xA DCS across a new gas processing complex in Saudi Arabia, representing one of the largest DCS contract awards in the region in over a decade.

August 2024: Yokogawa Electric Corporation introduced its OpreX Asset Health Insights platform, an AI-powered predictive maintenance solution designed for field instrumentation deployed in hazardous upstream environments.

October 2024: Endress+Hauser Management AG unveiled a next-generation Coriolis flow transmitter with integrated WirelessHART connectivity, targeting greenfield LNG terminals and floating production storage and offloading (FPSO) vessel applications.

February 2025: Schneider Electric SE released an updated version of its EcoStruxure Geo SCADA Expert software, featuring enhanced edge analytics and offline resilience capabilities for remote pipeline monitoring stations.

April 2025: The International Electrotechnical Commission (IEC) published revised guidelines under IEC 61511 for safety instrumented systems, prompting a wave of compliance assessments and upgrade contracts across global refining and petrochemical operators.

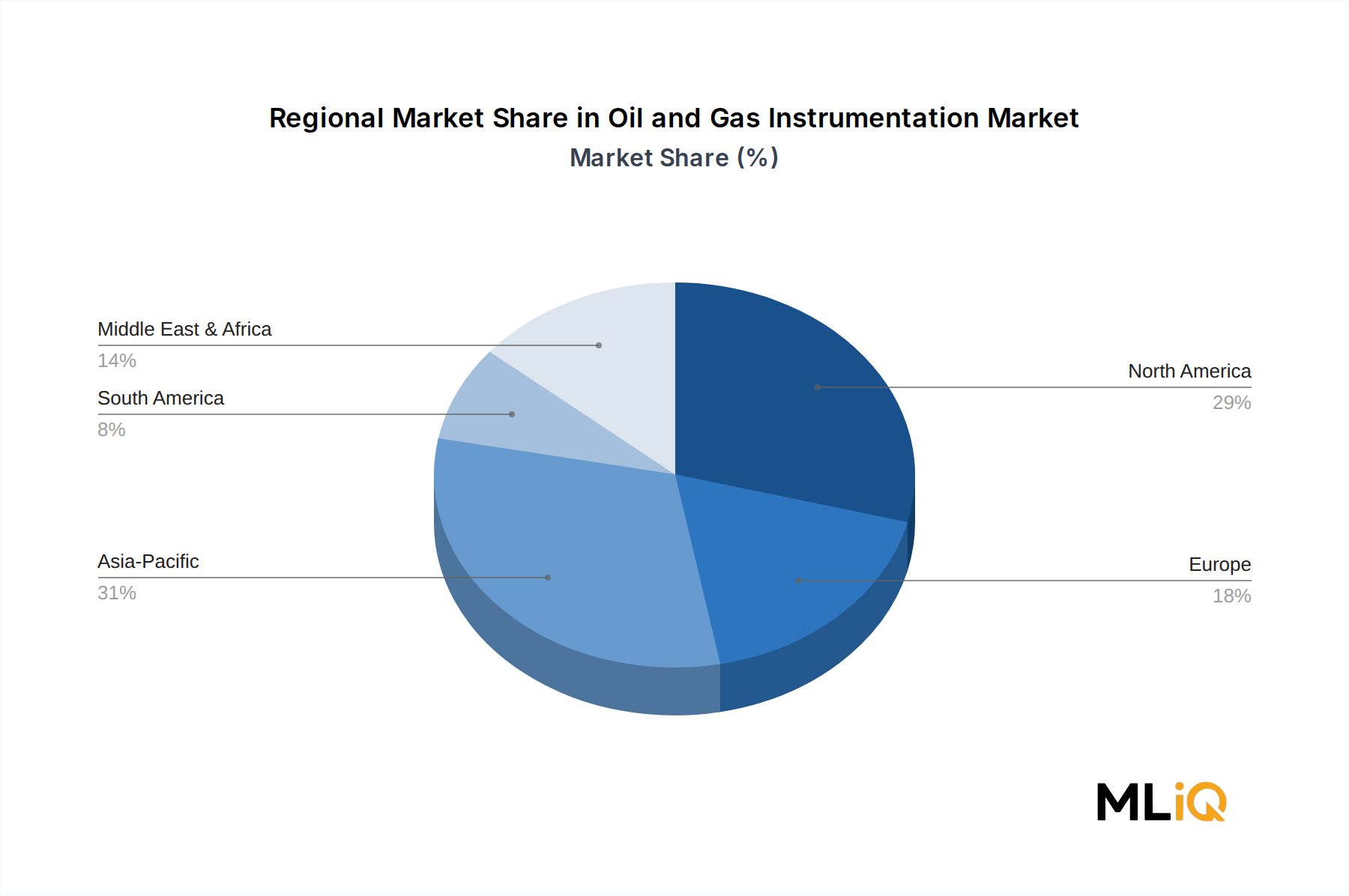

The Oil and Gas Instrumentation Market exhibits distinct regional growth dynamics, reflecting differences in production maturity, regulatory environment, and capital investment cycles.

North America commands the largest absolute revenue share, accounting for an estimated 32–35% of global market value in 2025. The United States remains the dominant contributor, driven by Permian Basin shale production, Gulf of Mexico deepwater operations, and an extensive pipeline and refinery modernization agenda. Canada's oil sands sector adds incremental demand for specialized temperature and flow measurement in viscous-fluid applications. The regional CAGR is estimated at 3.6%, reflecting market maturity and high existing penetration of automation technology.

The Middle East and Africa region is among the fastest-growing, with a projected CAGR of 5.2% through the forecast period. GCC nations — particularly Saudi Arabia, the UAE, and Qatar — are executing multi-billion-dollar hydrocarbon capacity expansion programs that embed advanced instrumentation from project inception. Qatar's LNG capacity expansion to 126 million tonnes per annum by 2027 is a particularly significant demand catalyst for precision flow and cryogenic measurement technologies.

Asia Pacific is the second-fastest-growing region, with a CAGR of approximately 4.8%, propelled by refinery capacity additions in China and India, LNG import terminal infrastructure in Southeast Asia, and offshore E&P expansion across ASEAN member states. China's national refinery upgrade programs and India's Petroleum, Chemicals and Petrochemicals Investment Region (PCPIR) policy are structurally supportive of sustained instrumentation demand.

Europe presents a more complex picture. Regulatory-driven investment in emissions monitoring and process safety is supporting instrumentation demand, particularly in Germany, the Netherlands, and Norway. However, energy transition policies are creating uncertainty over the long-term investment horizon for fossil fuel infrastructure, moderating the regional CAGR to approximately 2.8%.

South America, led by Brazil's pre-salt deepwater E&P sector, is emerging as a notable growth pocket, with Petrobras's multi-year capital plan driving demand for subsea instrumentation and topside automation systems.

The customer base for the Oil and Gas Instrumentation Market bifurcates into three primary end-user categories: international oil companies (IOCs), national oil companies (NOCs), and independent operators, each exhibiting distinct procurement behaviors and evaluation criteria.

IOCs such as Shell, bp, TotalEnergies, and ExxonMobil operate global technology standardization programs, typically nominating approved vendor lists (AVLs) at the corporate level and enforcing these across project portfolios. For IOCs, total cost of ownership (TCO) over a 20–30 year asset lifecycle is the dominant purchasing criterion, and vendors that can demonstrate superior mean time between failures and lower lifecycle maintenance costs consistently outperform on price-only comparisons. These buyers also place high value on vendor digital ecosystem integration, preferring instrumentation that natively communicates with their enterprise data historians and cloud analytics platforms.

NOCs, which dominate the Upstream Oil and Gas Market in the Middle East, Russia, and parts of Asia, tend toward government-influenced procurement processes, where local content requirements, government-to-government technology agreements, and in-country value (ICV) policies play significant roles. This creates commercial opportunities for vendors willing to establish local manufacturing or assembly operations.

Independent operators — particularly prevalent in North American shale and European North Sea markets — are more price-sensitive and tend to procure through distributors and system integrators rather than directly from OEMs. For this segment, instrument standardization, off-the-shelf availability, and fast delivery lead times are critical purchasing criteria.

A notable recent shift is the growing influence of digital and software capabilities in vendor selection decisions across all segments. Buyers are increasingly evaluating instrumentation vendors on the basis of their IIoT connectivity options, cloud integration roadmaps, and cybersecurity certification profiles — dimensions that were secondary considerations as recently as five years ago. This shift is favorably positioning vendors with integrated hardware-software offerings relative to pure-play hardware manufacturers.

The Flow

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.1% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Oil and Gas Instrumentation Market market expansion.

Key companies in the market include Siemens AG, Emerson Electric Co., ABB Ltd., Hima Paul Hildebrandt GmbH & Co KG, Yokogawa Electric Corporation, Schneider Electric SE, Endress+Hauser Management AG, Rockwell Automation Inc., Honeywell International Inc., GE Oil and Gas.

The market segments include Technology, Solution, Instruments.

The market size is estimated to be USD 78.01 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Oil and Gas Instrumentation Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Oil and Gas Instrumentation Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.