1. What are the major growth drivers for the Amorphous Core Power Transformers Market market?

Factors such as are projected to boost the Amorphous Core Power Transformers Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

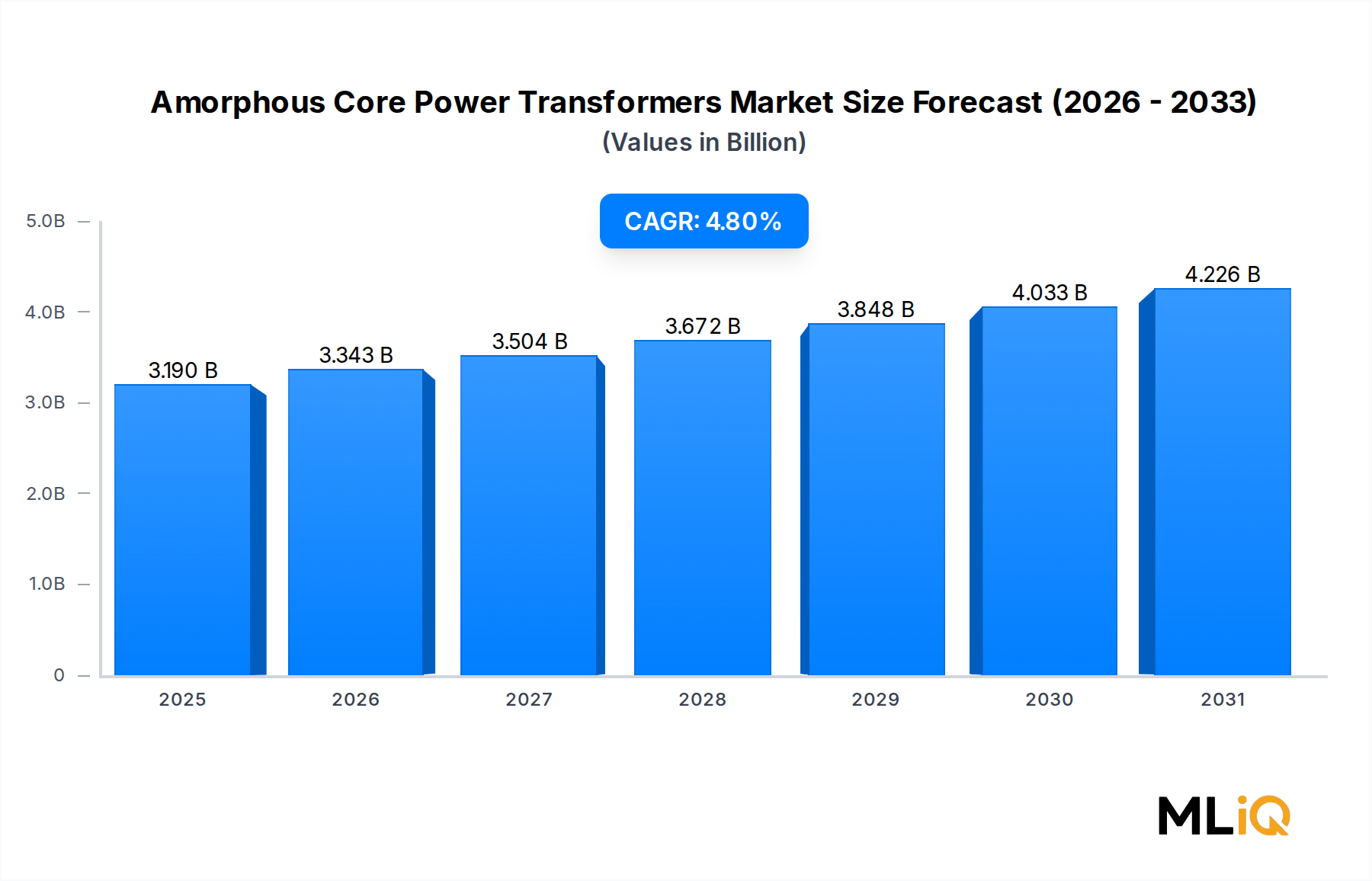

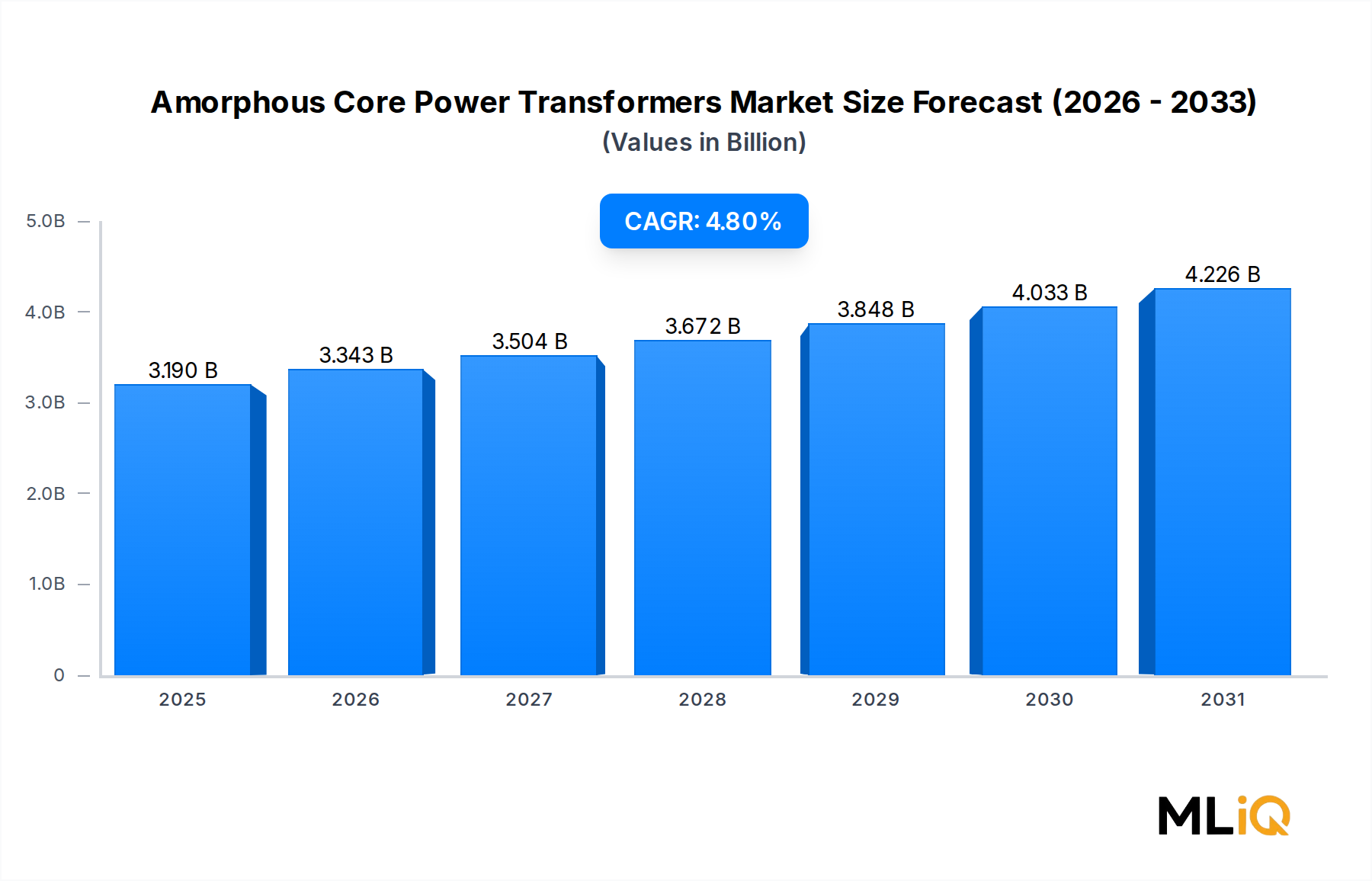

The global Amorphous Core Power Transformers Market was valued at $3.19 billion in the base year and is projected to expand at a compound annual growth rate (CAGR) of 4.8% through the forecast period of 2025 to 2033. This steady growth trajectory is underpinned by mounting regulatory pressure to reduce no-load energy losses in electrical distribution infrastructure, accelerating investments in grid modernization, and the global pivot toward low-carbon energy systems.

Amorphous core transformers differ fundamentally from conventional silicon-steel core units in that their magnetic cores are fabricated from metallic glass alloys — materials characterized by a non-crystalline atomic structure. This configuration dramatically reduces hysteresis and eddy current losses, translating into no-load loss reductions of up to 70% compared to silicon-grain-oriented steel cores. These efficiency advantages have made amorphous core units the preferred choice for utilities and grid operators seeking compliance with international efficiency mandates such as the U.S. DOE 2016 Efficiency Standards, EU Ecodesign Directive Tier 2, and China's GB 20052 standards.

Key demand drivers include the global surge in renewable energy capacity additions, urban electrification programs across emerging economies, and the broader transition toward smart grid architectures. As solar and wind installations proliferate, the need for low-loss, highly efficient step-down transformers at the distribution level has intensified. Simultaneously, governments across Asia Pacific, Europe, and North America are enacting stricter energy efficiency regulations, directly incentivizing utilities to replace aging conventional transformer fleets with amorphous alternatives.

The market is also benefiting from tailwinds within the Power Transformer Market broadly, as utilities worldwide accelerate capital expenditure on transmission and distribution infrastructure. Rising electricity consumption in data centers, electric vehicle charging ecosystems, and industrial automation further amplifies demand for high-efficiency power conversion equipment.

On the restraint side, the higher upfront capital cost of amorphous core transformers relative to conventional counterparts — often 15% to 25% more expensive at point of purchase — continues to temper adoption rates in price-sensitive markets. Additionally, the complexity of manufacturing amorphous ribbon and handling its brittle properties elevates production challenges.

Looking ahead to 2033, the market is expected to achieve a substantially higher valuation as lifecycle cost analyses increasingly favor amorphous units over silicon-steel alternatives. The convergence of policy, technology, and economics positions this market for sustained, structurally sound growth across all major geographies.

Within the Amorphous Core Power Transformers Market, the Oil-Immersed Amorphous Core Transformers sub-segment commands the largest revenue share and is expected to maintain its dominance throughout the 2025–2033 forecast period. This segment's primacy stems from several technical, economic, and application-specific factors that collectively reinforce its market leadership.

Oil-immersed amorphous core transformers utilize mineral oil or synthetic ester fluid as both a coolant and insulating medium. This configuration enables higher continuous load capacity, superior thermal management, and extended operational lifespans — typically exceeding 30 years under standard operating conditions. For utilities managing extensive distribution networks across urban and peri-urban geographies, these characteristics are indispensable. The oil-immersed variant is particularly dominant in medium-voltage distribution applications ranging from 25 kVA to 2,500 kVA, which represent the backbone of last-mile power delivery infrastructure in most countries.

China has been the single largest driver of oil-immersed amorphous core transformer adoption globally, driven by the State Grid Corporation of China's multi-year procurement programs and the implementation of GB 20052-2020 efficiency standards. Chinese manufacturers such as Zhixin Electric Ltd, Jiangshan Scotech Electrical Co. Ltd., and San Jiang Electric Mfg. Co. Ltd. have scaled production capacity aggressively to meet domestic and export demand, reinforcing the segment's revenue concentration.

In North America and Europe, oil-immersed amorphous transformers are increasingly specified for utility-scale grid upgrades, particularly as aging transformer fleets — many installed in the 1980s and 1990s — approach end-of-life. The U.S. Department of Energy's efficiency rulemakings have created regulatory certainty that directly benefits this segment, as utilities procuring replacement units are required to meet performance thresholds that amorphous core oil-immersed designs readily satisfy.

From an application perspective, the electricity distribution end-use vertical accounts for the overwhelming majority of oil-immersed amorphous transformer installations. Substations serving residential and commercial loads, renewable energy farm step-down stations, and industrial park distribution points are the primary deployment environments. The segment also intersects with growth trends in the Smart Grid Market, where low-loss transformers are being integrated with digital monitoring and load management systems to optimize grid efficiency in real time.

Competitively, the oil-immersed segment is moderately consolidated at the global level, with Japanese and Chinese manufacturers holding the largest combined share. Hitachi Industrial Equipment Systems Inc and Toshiba Energy Systems & Solutions Corporation maintain strong positions in the premium, high-reliability segment of the market, particularly for municipal and industrial utility applications. Siemens Energy AG and ABB Ltd compete across geographies with technologically differentiated product lines that emphasize lifecycle efficiency and digital integration.

The segment's share is currently consolidating rather than expanding at the expense of dry-type variants. While dry-type amorphous transformers are gaining traction in indoor, fire-sensitive, and compact installation environments — including data centers and hospitals — oil-immersed units retain a structural advantage in outdoor, high-capacity, and rural distribution contexts. This bifurcation is expected to persist through 2033, with oil-immersed units maintaining approximately 60–65% of total market revenue.

The Amorphous Core Power Transformers Market is shaped by a distinct set of structural drivers and countervailing restraints that quantitative analysis reveals with precision.

Regulatory mandates are the single most powerful demand catalyst. The European Union's Ecodesign Regulation (EU) 2019/1783, effective since July 2021, mandates Tier 2 minimum energy performance standards for power transformers. Compliance with these standards necessitates no-load loss values that silicon-steel core units struggle to achieve cost-effectively, while amorphous core designs meet them by design. Similarly, China's GB 20052-2020 standard — implemented across a grid that added over 330 GW of new power capacity in 2023 alone — has made amorphous core transformers a de facto procurement standard for the State Grid Corporation.

Renewable energy capacity expansion is a second tier-one driver. Global solar and wind additions reached approximately 295 GW and 117 GW respectively in 2023, each requiring step-down transformer infrastructure at point of grid injection. This intersection with the Renewable Energy Integration Market creates a structural, long-duration demand pipeline for efficient, low-loss distribution transformers.

Grid modernization expenditure provides a third macro tailwind. The U.S. Infrastructure Investment and Jobs Act allocated approximately $65 billion to grid improvements, a portion of which directly funds transformer procurement and upgrade programs. European transmission system operators are collectively investing over €100 billion through 2030 in grid reinforcement aligned with the REPowerEU agenda.

On the constraint side, the elevated cost of amorphous alloy ribbon — the core raw material — introduces margin pressure and purchase price sensitivity. Amorphous ribbon is produced by a small number of specialized manufacturers globally, creating supply concentration risk. Additionally, the mechanical brittleness of amorphous metal complicates core assembly automation, limiting throughput scalability for manufacturers attempting to compress unit costs. These dynamics constrain market penetration in developing economies where initial capital cost outweighs lifecycle savings in procurement decision frameworks.

The competitive landscape of the Amorphous Core Power Transformers Market is characterized by a blend of global conglomerates, regionally dominant specialists, and vertically integrated Asian manufacturers. The following profiles capture the strategic positioning of key participants:

Toshiba Energy Systems & Solutions Corporation: A pioneer in amorphous core transformer commercialization, Toshiba leverages decades of materials science expertise to deliver premium-efficiency units for utility and industrial clients across Asia Pacific and North America. The company maintains a strong intellectual property portfolio in core assembly and loss optimization techniques.

Zhixin Electric Ltd: One of China's largest dedicated amorphous transformer manufacturers, Zhixin Electric serves the State Grid Corporation of China and regional utilities with a broad product portfolio spanning distribution and power transformer segments. The company has expanded export operations into Southeast Asia and the Middle East.

HYUNDAI ELECTRIC CO., LTD.: The South Korean conglomerate's power division competes across the full transformer value chain, with amorphous core units positioned for domestic and ASEAN export markets. Hyundai Electric is investing in digital monitoring integration for smart grid compatibility.

Siemens Energy AG: Siemens Energy brings global scale and a diversified energy portfolio to the amorphous core segment, with particular strength in European utility procurement processes. The company differentiates on lifecycle cost modeling and digital twin integration for transformer management.

ABB Ltd: A global leader in power and automation technologies, ABB competes in the amorphous core space through its distribution transformer division, emphasizing sustainability credentials, SF6-free insulation options, and grid digitalization alignment.

Jiangshan Scotech Electrical Co. Ltd.: A specialized Chinese manufacturer with deep focus on amorphous alloy transformer design and production efficiency. Scotech has established partnerships with amorphous ribbon suppliers to secure favorable input cost structures.

Eaton Inc: Eaton's electrical sector division offers amorphous core dry-type and oil-immersed transformers, primarily targeting the North American utility and commercial construction segments. The company emphasizes compliance with DOE 2016 efficiency standards as a core marketing proposition.

Hitachi Industrial Equipment Systems Inc: Hitachi brings Japanese manufacturing precision to the amorphous transformer segment, with strong positioning in high-reliability industrial and municipal utility applications across Asia and Europe.

Mitsubishi Electric Corporation: A vertically integrated Japanese manufacturer with in-house amorphous alloy processing capabilities, Mitsubishi Electric competes on product quality and long-term service contracts for utility clients.

San Jiang Electric Mfg. Co. Ltd.: A mid-tier Chinese manufacturer focused on cost-competitive amorphous distribution transformers for domestic grid projects and emerging market exports.

March 2023: ABB Ltd announced the expansion of its transformer manufacturing facility in Vadodara, India, with a dedicated production line for amorphous core distribution transformers targeting the Indian utility sector's accelerating electrification programs.

June 2023: The Chinese National Energy Administration issued updated procurement guidelines requiring all new distribution transformers below 315 kVA procured by State Grid Corporation to meet GB 20052-2020 Tier 3 efficiency specifications, effectively mandating amorphous or equivalent core technology.

September 2023: Siemens Energy AG entered a strategic supply agreement with a European transmission system operator for the delivery of 2,500 units of amorphous core oil-immersed transformers as part of a grid resilience reinforcement program through 2026.

January 2024: Hitachi Industrial Equipment Systems Inc unveiled a next-generation amorphous core transformer series achieving no-load losses 15% below existing product line benchmarks, leveraging proprietary nano-crystalline alloy blending techniques.

April 2024: The U.S. Department of Energy finalized updated efficiency standards for distribution transformers, effective 2027, raising minimum performance thresholds in ways that further advantage amorphous core designs over conventional silicon-steel alternatives.

November 2024: Eaton Inc completed the acquisition of a regional transformer services company in Canada, expanding its amorphous transformer installation and lifecycle management capabilities in the North American market.

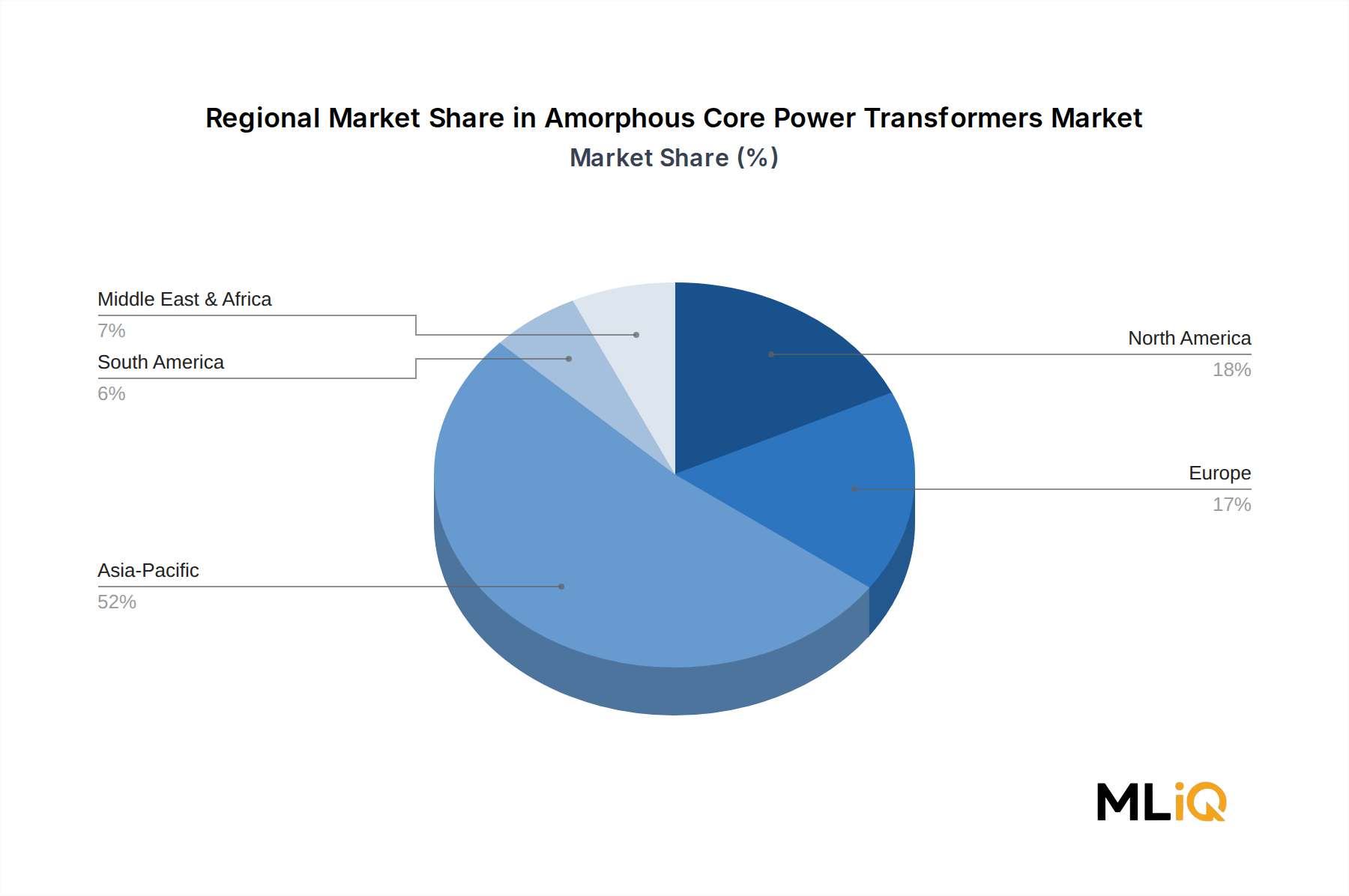

The Amorphous Core Power Transformers Market exhibits pronounced regional heterogeneity in terms of growth rates, adoption maturity, and demand drivers.

Asia Pacific is both the largest revenue contributor and the fastest-growing regional segment, accounting for an estimated 55–60% of global market revenue. China alone represents the dominant share within this region, driven by State Grid Corporation procurement volumes, stringent GB 20052-2020 efficiency mandates, and domestic manufacturing scale. India is the fastest-growing individual country market within Asia Pacific, propelled by the Revamped Distribution Sector Scheme (RDSS) allocating approximately $40 billion toward distribution infrastructure modernization. Japan and South Korea contribute premium-segment volumes through utility upgrade programs. The regional CAGR for Asia Pacific is estimated at approximately 5.5–6.0% through 2033.

North America represents the second-largest regional market, with the United States as the primary demand center. The combination of DOE efficiency regulations, the Infrastructure Investment and Jobs Act funding flows, and aging transformer fleet replacement cycles creates a structurally supportive demand environment. The North American market is estimated to grow at approximately 4.2–4.5% CAGR. Canada and Mexico contribute incremental volumes through utility modernization and industrial expansion programs respectively.

Europe is characterized by regulatory-driven demand maturity. The EU Ecodesign Tier 2 standards have effectively established amorphous core and equivalent low-loss technologies as the minimum procurement baseline across member states. Germany, France, and the United Kingdom are the largest national markets. European CAGR is estimated at approximately 3.8–4.2%, reflecting a more mature replacement cycle relative to Asia Pacific.

The Middle East and Africa region is an emerging growth frontier, with Gulf Cooperation Council (GCC) countries investing in grid expansion and smart city infrastructure. Saudi Arabia's Vision 2030 and UAE electrification programs are notable demand catalysts. Regional CAGR is estimated at approximately 5.0–5.5%, albeit from a smaller base. South America, led by Brazil and Argentina, is growing at a moderate 3.5–4.0% CAGR, constrained by currency volatility and fiscal pressures on utility capital budgets.

Investment activity within the Amorphous Core Power Transformers Market has intensified notably over the 2022–2024 period, reflecting both the market's structural growth outlook and the broader capital mobilization around energy transition infrastructure.

Mergers and acquisitions have been a primary capital deployment mechanism. Established transformer manufacturers have pursued bolt-on acquisitions of specialized amorphous core producers and transformer services companies to expand product portfolios and geographic reach. Eaton's Canadian acquisition in late 2024 exemplifies this strategy, as does ABB's ongoing facility investment in India. These transactions reflect a competitive logic in which scale and geographic diversification are prerequisites for winning large-scale utility procurement contracts.

Venture and growth capital has flowed into the adjacent amorphous alloy materials supply chain, as investors recognize that ribbon supply constraints represent a key bottleneck for market expansion. Startups and mid-tier manufacturers advancing novel amorphous alloy compositions — including nano-crystalline hybrids — have attracted funding from energy transition-focused private equity and corporate venture arms.

Strategic partnerships between transformer manufacturers and smart grid technology providers are also proliferating. These alliances aim to embed digital monitoring, predictive maintenance, and load optimization capabilities directly into transformer units, enhancing value proposition and creating recurring revenue streams through data and service contracts.

Sub-segments attracting the most capital include oil-immersed units targeting utility-scale replacement programs and dry-type units for data center and EV charging infrastructure applications. The latter is particularly notable given the exponential growth in data center construction globally. Investor interest in the Dry-Type Transformer Market segment has grown sharply as fire safety and indoor installation requirements converge with efficiency mandates in urban deployment environments.

Pricing dynamics in the Amorphous Core Power Transformers Market are shaped by the interplay

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.8% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Amorphous Core Power Transformers Market market expansion.

Key companies in the market include Toshiba Energy Systems & Solutions Corporation, Zhixin Electric Ltd, HYUNDAI ELECTRIC CO., LTD., Siemens Energy AG, ABB Ltd, Jiangshan Scotech Electrical Co., Ltd., Eaton Inc, Hitachi Industrial Equipment Systems Inc, Mitsubishi Electric Corporation, San Jiang Electric Mfg. Co., Ltd..

The market segments include Type, Application.

The market size is estimated to be USD 3.19 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4335, and USD 7261 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Amorphous Core Power Transformers Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Amorphous Core Power Transformers Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.