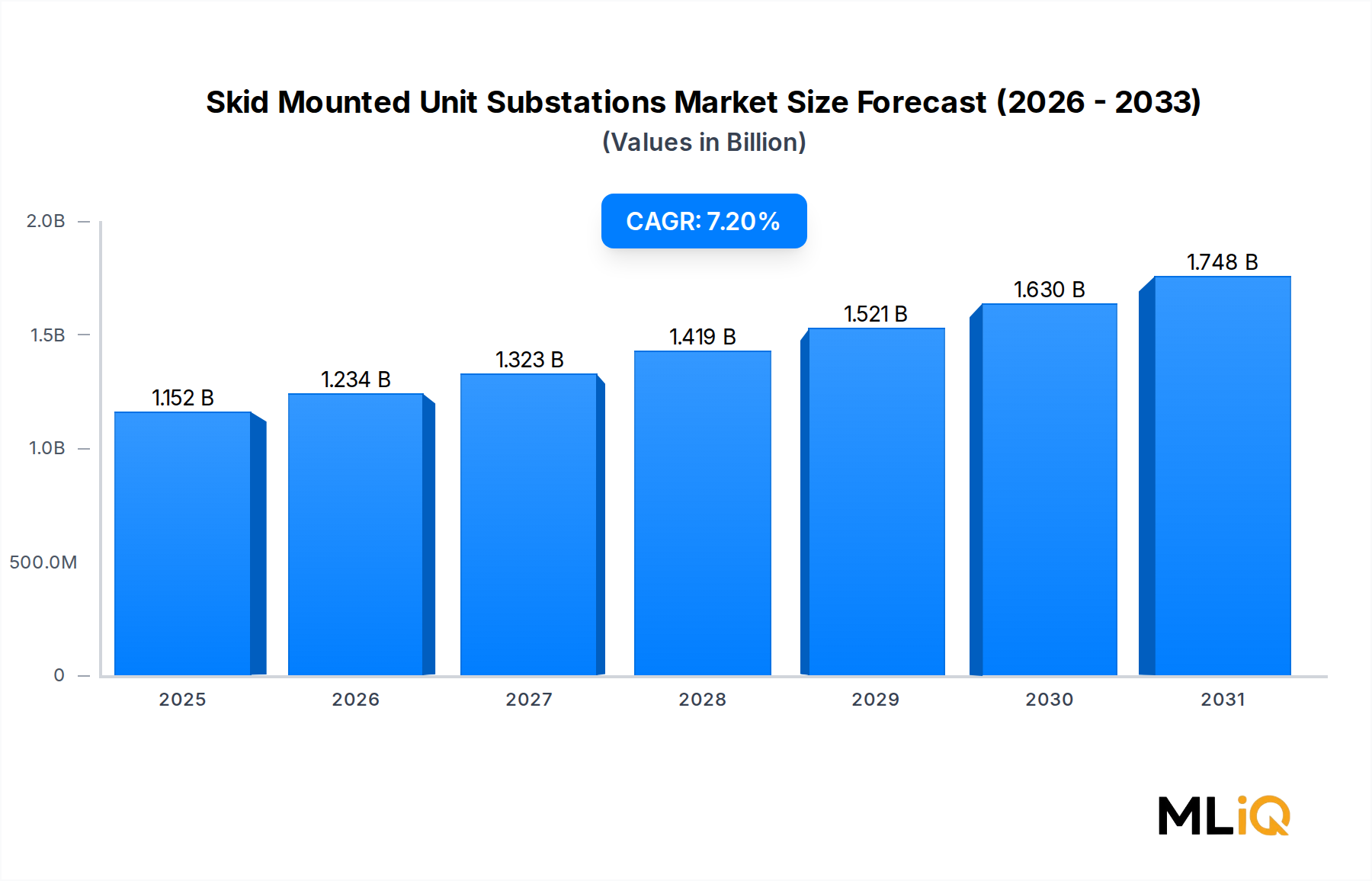

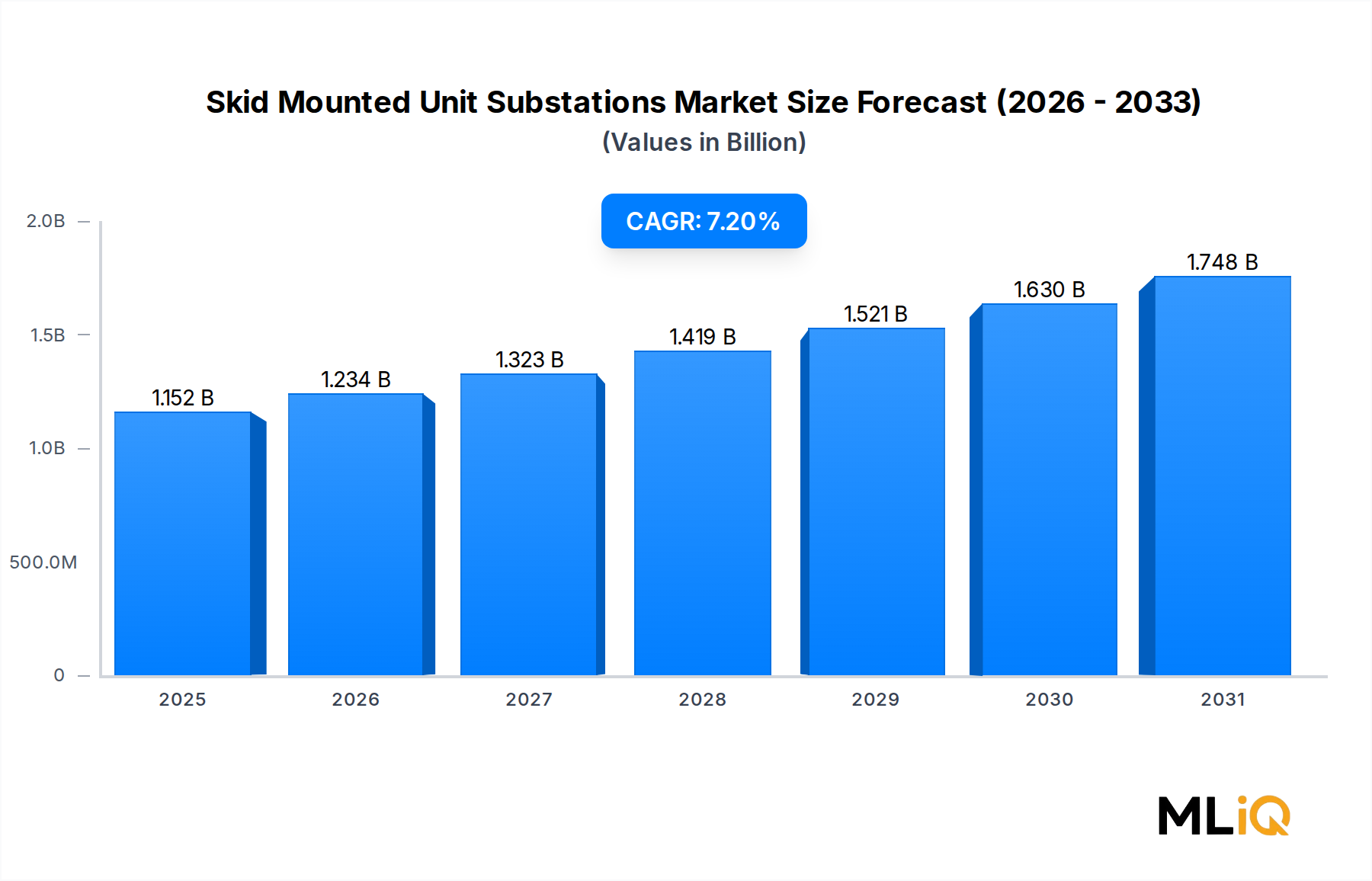

Industrial Segment Dominance in the Skid Mounted Unit Substations Market

Among the application segments defining the structure of the Skid Mounted Unit Substations Market, the Industrial segment commands the largest revenue share and is expected to maintain its leadership position throughout the forecast period. This dominance is rooted in several structurally reinforcing demand vectors that collectively make industrial end-users the most consistent and highest-volume purchasers of skid mounted substation solutions globally.

Industrial facilities — encompassing oil refineries, petrochemical complexes, mining operations, cement plants, steel mills, LNG liquefaction terminals, and large-scale food processing plants — require dependable, high-capacity power distribution infrastructure that can be deployed rapidly and reliably, often in challenging geographic or environmental contexts. The skid mounted format directly addresses these requirements by eliminating the need for extensive site-based civil works, allowing factory-assembled units to be transported to location and energized within compressed timeframes.

In the oil and gas sector specifically, which represents one of the largest sub-clusters within industrial demand, the cyclical recovery of upstream investment since 2022 has translated into meaningful capital flows toward electrical infrastructure. Onshore drilling programs in the Permian Basin, Middle Eastern NOC expansion projects, and offshore platform electrification initiatives in the North Sea and West Africa have each contributed to elevated order volumes for medium- and high-voltage skid mounted substations. Projects operating in the 33 kV–400 kV voltage range are particularly prevalent in these contexts, given the large power loads associated with compression, pumping, and processing equipment.

Mining is the second major industrial sub-cluster. The global electrification of mining operations — driven by both cost efficiency targets and decarbonization commitments from major diversified miners — is accelerating adoption of skid mounted substations as the preferred solution for both surface and underground power distribution. Copper, lithium, cobalt, and nickel mining expansions in South America, Sub-Saharan Africa, and Australia are generating multi-year demand pipelines for purpose-built electrical infrastructure.

Manufacturing represents the third pillar of industrial demand. Semiconductor fabrication facilities, battery gigafactories, and electric vehicle assembly plants — all of which are receiving substantial public and private investment across North America, Europe, and Asia — require highly reliable, precisely engineered power distribution infrastructure with low tolerance for downtime. Skid mounted substations configured with redundant switching architectures, advanced protection relaying, and digital communication interfaces are increasingly specified in these facilities.

Within the industrial segment, demand is also being shaped by the rising preference for integrated solutions that combine transformer, switchgear, and protection systems within a single factory-assembled package, reducing the number of vendor interfaces and simplifying project management for EPC contractors. This trend is pushing manufacturers toward offering increasingly comprehensive skid assemblies, including integrated metering, SCADA connectivity, and environmental monitoring.

From a voltage segmentation perspective, the 11 kV–33 kV range dominates within the industrial segment for mid-tier applications, while the 33 kV–400 kV band captures the largest revenue contribution from heavy industry and utility-interfacing installations. The industrial segment's share of total market revenue is estimated at approximately 45–48% in 2025, a figure anticipated to hold relatively stable as competing segments including commercial and power utilities grow in parallel rather than at the industrial segment's expense.

Key participants targeting industrial buyers include global electrical engineering conglomerates with vertically integrated transformer and switchgear manufacturing capabilities, as well as regional specialists with deep application knowledge in specific sectors such as mining or petrochemicals. Competitive differentiation within this segment increasingly centers on total cost of ownership modeling, after-sales service networks, and demonstrated compliance with industry-specific standards such as IECEx, ATEX, and IEEE 1814.